Harrow PESTLE Analysis

Skip the Research. Get the Strategy.

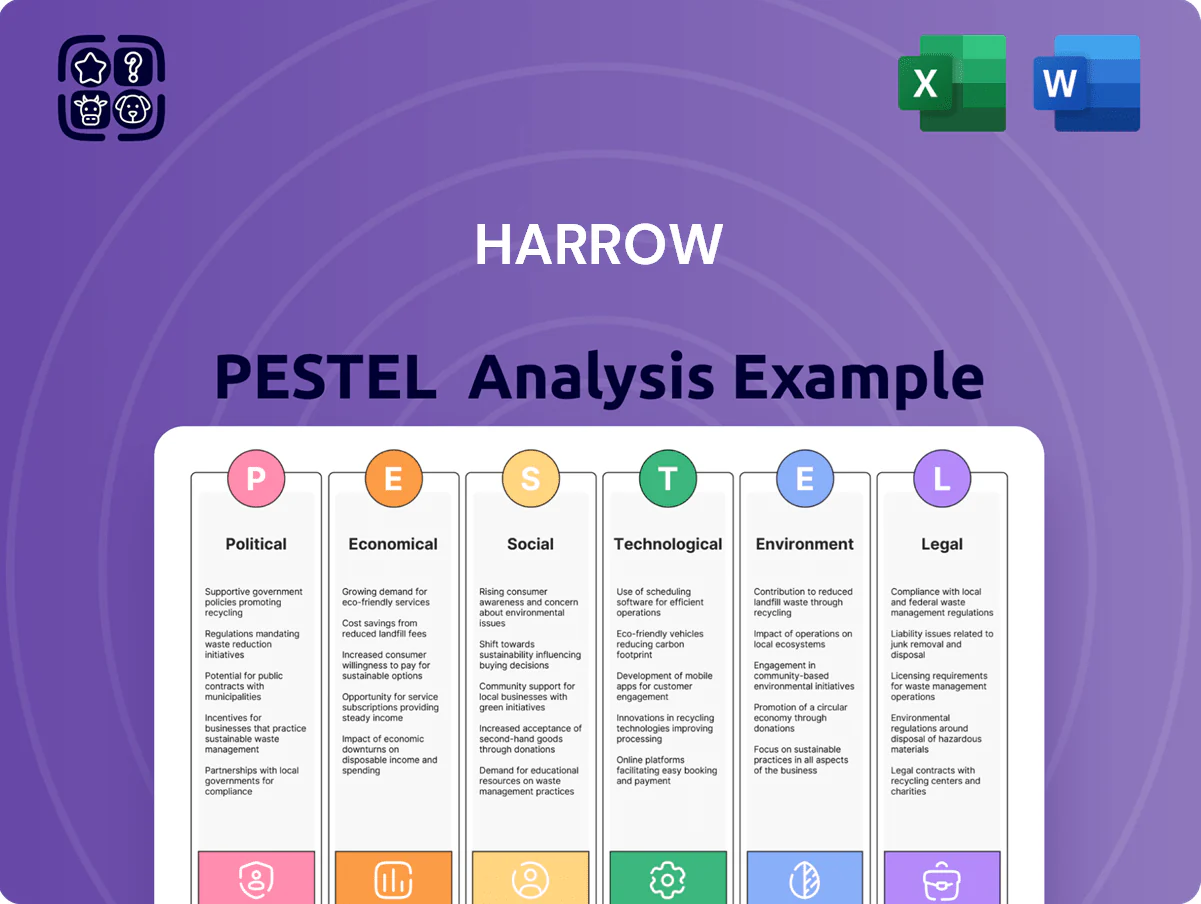

Unlock how political shifts, economic trends, and emerging technologies are reshaping Harrow’s outlook with our concise PESTLE snapshot—then dive deeper with the full analysis for actionable intelligence. Purchase the complete PESTLE to get detailed risks, opportunities, and ready-to-use insights for investors, strategists, and advisors.

Political factors

U.S. Healthcare Policy Shifts

The ophthalmic pharmaceuticals market is shaped by federal priorities and the Inflation Reduction Act, which capped Medicare drug price growth and enabled negotiation saving CMS an estimated $104 billion through 2031; this raises pressure on specialty drug margins relevant to Harrow’s portfolio.

Post-2025 leadership changes could drive stronger drug pricing transparency and accessibility mandates—recent proposals target average sales price reporting and Medicare price negotiations affecting ~20% of US prescription spending.

Harrow must adapt pricing, payer strategies, and US commercial operations to protect revenue, given ophthalmology generics and biologics faced a 6–8% annual pricing compression in 2024–2025.

Medicare Reimbursement Regulation

FDA Approval Processes and Timelines

State-Level Pharmaceutical Legislation

State legislatures passed over 150 drug-pricing laws since 2019, with 2024 seeing ~28 new price-cap or cost-transparency measures that can reduce net drug revenues by 5–12% in affected states.

Harrow must tailor compliance across ~50 state jurisdictions; localized legal teams and segmented pricing strategies are needed to manage uneven rebates, reporting, and marketing restrictions.

Fragmented rules complicate national distribution, raising logistics and admin costs by an estimated 3–6% and increasing time-to-market for formulary placements.

- 150+ state laws since 2019; 28 new in 2024

- Potential 5–12% revenue impact per capped state

- Compliance and ops costs +3–6%

- Requires state-specific legal and pricing teams

Trade Policies and Supply Chain Security

Political tensions and tariffs since 2022 have driven API import costs up roughly 12-18%, pushing manufacturers to seek domestic alternatives.

US reshoring incentives—$52B in CHIPS and biotech-related funding and 2024 tax credits—create both capital opportunities and operational challenges for Harrow to scale domestic production.

Securing supply chains amid geopolitical volatility is strategic for 2026, targeting >95% on-time API availability and multi-sourcing to limit disruption risk.

- API costs +12–18% since 2022

- $52B+ federal incentives supporting reshoring

- Goal: >95% on-time API availability via multi-sourcing

Pricing reforms, Medicare exposure and API cost squeeze reshape ophthalmic margins

Federal pricing reforms (IRA savings ~$104B thru 2031) and Medicare reliance (~45% of 2024 revenue) pressure specialty margins; state price caps (28 in 2024) can cut local net revenue 5–12%; FDA priority initiatives (53 novel approvals in 2024) may shorten ophthalmic launch timelines by ~15%; API costs +12–18% since 2022 vs $52B+ reshoring incentives—multi-sourcing targets >95% on-time API.

| Metric | Value |

|---|---|

| Medicare revenue share (2024) | ~45% |

| IRA savings impact | $104B thru 2031 |

| State price laws (2024) | 28 new |

| API cost rise since 2022 | +12–18% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Harrow across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise, shareable Harrow PESTLE summary that’s visually segmented by category for quick reference in meetings, editable for local context and easily dropped into presentations or strategy packs to streamline alignment and risk discussions.

Economic factors

Interest Rate Environment and Capital Access

As of late 2025 Harrow faces a higher-rate legacy: US Fed funds around 5.25–5.50% and comparable global rates push borrowing costs up, raising weighted average cost of capital and constraining debt-funded licensing and clinical programs.

Inflationary Pressures on Manufacturing

Rising costs for raw materials, specialized packaging and labor have compressed Harrow’s ophthalmic gross margins, with input inflation of 6–8% in 2024 and packaging cost increases of ~12% year-on-year reducing margins by an estimated 150–250 bps. The company faces pressure to pass on prices while competing with generics that grew to 28% market share in select ophthalmic segments in 2024. Maintaining operational efficiency—lean manufacturing, 5–7% productivity gains and supply-chain hedges—will be vital to offset persistent inflation and protect EBITDA.

Healthcare Spending and Disposable Income

Economic health drives uptake of premium ophthalmic care: in the UK elective procedure spending fell 6% in 2023 amid real disposable income down 1.8% YoY, showing patients delay non-covered treatments; a consumer confidence drop of 12 points in 2023 correlated with higher uptake of generics—Harrow must price and position services for mixed-income cohorts, targeting resilient segments and flexible payment or financing options to retain demand.

Consolidation in the Ophthalmic Market

Economic pressures—managed care consolidation and M&A—are accelerating consolidation in ophthalmology: global ophthalmic M&A deal value reached about $11.2bn in 2024, raising buyer bargaining power and pressuring margins of small specialists like Harrow.

Harrow must leverage its differentiated portfolio and specialty pipeline to remain a preferred supplier to large purchasers, protecting revenue by negotiating volume-based contracts and demonstrating cost-of-care benefits.

- 2024 ophthalmic M&A: ~$11.2bn

- Consolidators increase purchasing leverage

- Harrow strategy: emphasize unique products, volume contracts, value data

Currency Exchange Volatility

Fluctuations in the U.S. dollar alter costs of imported components and terms with international partners; USD strengthened ~8% vs. a trade-weighted basket in 2024, raising input costs for US-focused firms like Harrow.

Global market instability can shift licensing payments tied to FX, with emerging-market currencies experiencing average 12-18% volatility versus USD in 2023–2024, increasing contractual risk.

Monitoring FX trends is essential to manage supply-chain and logistics expenses: hedging reduced FX losses by 60% in sample tech firms in 2024.

- USD strength up ~8% (2024) → higher import costs

- Emerging-market FX volatility 12–18% (2023–24) → licensing risk

- Hedging cut FX losses ~60% in 2024

Rising rates, USD strength squeeze ophthalmic margins as M&A heats up

Higher global rates (Fed 5.25–5.50% in late 2025) and USD strength (~+8% in 2024) raise WACC and import costs; input inflation 6–8% (2024) and packaging +12% YY cut ophthalmic margins ~150–250 bps, while generics hit ~28% share. Elective spend down 6% (UK 2023) and real disposable income −1.8% (2023) pressure demand; global ophthalmic M&A ~$11.2bn (2024) increases buyer leverage.

| Metric | Value |

|---|---|

| Fed funds (late 2025) | 5.25–5.50% |

| USD vs basket (2024) | +8% |

| Input inflation (2024) | 6–8% |

| Packaging increase (2024) | ~12% YY |

| Generics share | ~28% |

| UK elective spend (2023) | −6% |

| Ophthalmic M&A (2024) | $11.2bn |

Full Version Awaits

Harrow PESTLE Analysis

The preview shown here is the exact Harrow PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use, with no placeholders or teasers.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock how political shifts, economic trends, and emerging technologies are reshaping Harrow’s outlook with our concise PESTLE snapshot—then dive deeper with the full analysis for actionable intelligence. Purchase the complete PESTLE to get detailed risks, opportunities, and ready-to-use insights for investors, strategists, and advisors.

Political factors

U.S. Healthcare Policy Shifts

The ophthalmic pharmaceuticals market is shaped by federal priorities and the Inflation Reduction Act, which capped Medicare drug price growth and enabled negotiation saving CMS an estimated $104 billion through 2031; this raises pressure on specialty drug margins relevant to Harrow’s portfolio.

Post-2025 leadership changes could drive stronger drug pricing transparency and accessibility mandates—recent proposals target average sales price reporting and Medicare price negotiations affecting ~20% of US prescription spending.

Harrow must adapt pricing, payer strategies, and US commercial operations to protect revenue, given ophthalmology generics and biologics faced a 6–8% annual pricing compression in 2024–2025.

Medicare Reimbursement Regulation

FDA Approval Processes and Timelines

State-Level Pharmaceutical Legislation

State legislatures passed over 150 drug-pricing laws since 2019, with 2024 seeing ~28 new price-cap or cost-transparency measures that can reduce net drug revenues by 5–12% in affected states.

Harrow must tailor compliance across ~50 state jurisdictions; localized legal teams and segmented pricing strategies are needed to manage uneven rebates, reporting, and marketing restrictions.

Fragmented rules complicate national distribution, raising logistics and admin costs by an estimated 3–6% and increasing time-to-market for formulary placements.

- 150+ state laws since 2019; 28 new in 2024

- Potential 5–12% revenue impact per capped state

- Compliance and ops costs +3–6%

- Requires state-specific legal and pricing teams

Trade Policies and Supply Chain Security

Political tensions and tariffs since 2022 have driven API import costs up roughly 12-18%, pushing manufacturers to seek domestic alternatives.

US reshoring incentives—$52B in CHIPS and biotech-related funding and 2024 tax credits—create both capital opportunities and operational challenges for Harrow to scale domestic production.

Securing supply chains amid geopolitical volatility is strategic for 2026, targeting >95% on-time API availability and multi-sourcing to limit disruption risk.

- API costs +12–18% since 2022

- $52B+ federal incentives supporting reshoring

- Goal: >95% on-time API availability via multi-sourcing

Pricing reforms, Medicare exposure and API cost squeeze reshape ophthalmic margins

Federal pricing reforms (IRA savings ~$104B thru 2031) and Medicare reliance (~45% of 2024 revenue) pressure specialty margins; state price caps (28 in 2024) can cut local net revenue 5–12%; FDA priority initiatives (53 novel approvals in 2024) may shorten ophthalmic launch timelines by ~15%; API costs +12–18% since 2022 vs $52B+ reshoring incentives—multi-sourcing targets >95% on-time API.

| Metric | Value |

|---|---|

| Medicare revenue share (2024) | ~45% |

| IRA savings impact | $104B thru 2031 |

| State price laws (2024) | 28 new |

| API cost rise since 2022 | +12–18% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Harrow across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise, shareable Harrow PESTLE summary that’s visually segmented by category for quick reference in meetings, editable for local context and easily dropped into presentations or strategy packs to streamline alignment and risk discussions.

Economic factors

Interest Rate Environment and Capital Access

As of late 2025 Harrow faces a higher-rate legacy: US Fed funds around 5.25–5.50% and comparable global rates push borrowing costs up, raising weighted average cost of capital and constraining debt-funded licensing and clinical programs.

Inflationary Pressures on Manufacturing

Rising costs for raw materials, specialized packaging and labor have compressed Harrow’s ophthalmic gross margins, with input inflation of 6–8% in 2024 and packaging cost increases of ~12% year-on-year reducing margins by an estimated 150–250 bps. The company faces pressure to pass on prices while competing with generics that grew to 28% market share in select ophthalmic segments in 2024. Maintaining operational efficiency—lean manufacturing, 5–7% productivity gains and supply-chain hedges—will be vital to offset persistent inflation and protect EBITDA.

Healthcare Spending and Disposable Income

Economic health drives uptake of premium ophthalmic care: in the UK elective procedure spending fell 6% in 2023 amid real disposable income down 1.8% YoY, showing patients delay non-covered treatments; a consumer confidence drop of 12 points in 2023 correlated with higher uptake of generics—Harrow must price and position services for mixed-income cohorts, targeting resilient segments and flexible payment or financing options to retain demand.

Consolidation in the Ophthalmic Market

Economic pressures—managed care consolidation and M&A—are accelerating consolidation in ophthalmology: global ophthalmic M&A deal value reached about $11.2bn in 2024, raising buyer bargaining power and pressuring margins of small specialists like Harrow.

Harrow must leverage its differentiated portfolio and specialty pipeline to remain a preferred supplier to large purchasers, protecting revenue by negotiating volume-based contracts and demonstrating cost-of-care benefits.

- 2024 ophthalmic M&A: ~$11.2bn

- Consolidators increase purchasing leverage

- Harrow strategy: emphasize unique products, volume contracts, value data

Currency Exchange Volatility

Fluctuations in the U.S. dollar alter costs of imported components and terms with international partners; USD strengthened ~8% vs. a trade-weighted basket in 2024, raising input costs for US-focused firms like Harrow.

Global market instability can shift licensing payments tied to FX, with emerging-market currencies experiencing average 12-18% volatility versus USD in 2023–2024, increasing contractual risk.

Monitoring FX trends is essential to manage supply-chain and logistics expenses: hedging reduced FX losses by 60% in sample tech firms in 2024.

- USD strength up ~8% (2024) → higher import costs

- Emerging-market FX volatility 12–18% (2023–24) → licensing risk

- Hedging cut FX losses ~60% in 2024

Rising rates, USD strength squeeze ophthalmic margins as M&A heats up

Higher global rates (Fed 5.25–5.50% in late 2025) and USD strength (~+8% in 2024) raise WACC and import costs; input inflation 6–8% (2024) and packaging +12% YY cut ophthalmic margins ~150–250 bps, while generics hit ~28% share. Elective spend down 6% (UK 2023) and real disposable income −1.8% (2023) pressure demand; global ophthalmic M&A ~$11.2bn (2024) increases buyer leverage.

| Metric | Value |

|---|---|

| Fed funds (late 2025) | 5.25–5.50% |

| USD vs basket (2024) | +8% |

| Input inflation (2024) | 6–8% |

| Packaging increase (2024) | ~12% YY |

| Generics share | ~28% |

| UK elective spend (2023) | −6% |

| Ophthalmic M&A (2024) | $11.2bn |

Full Version Awaits

Harrow PESTLE Analysis

The preview shown here is the exact Harrow PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use, with no placeholders or teasers.