Harvey Norman Porter's Five Forces Analysis

From Overview to Strategy Blueprint

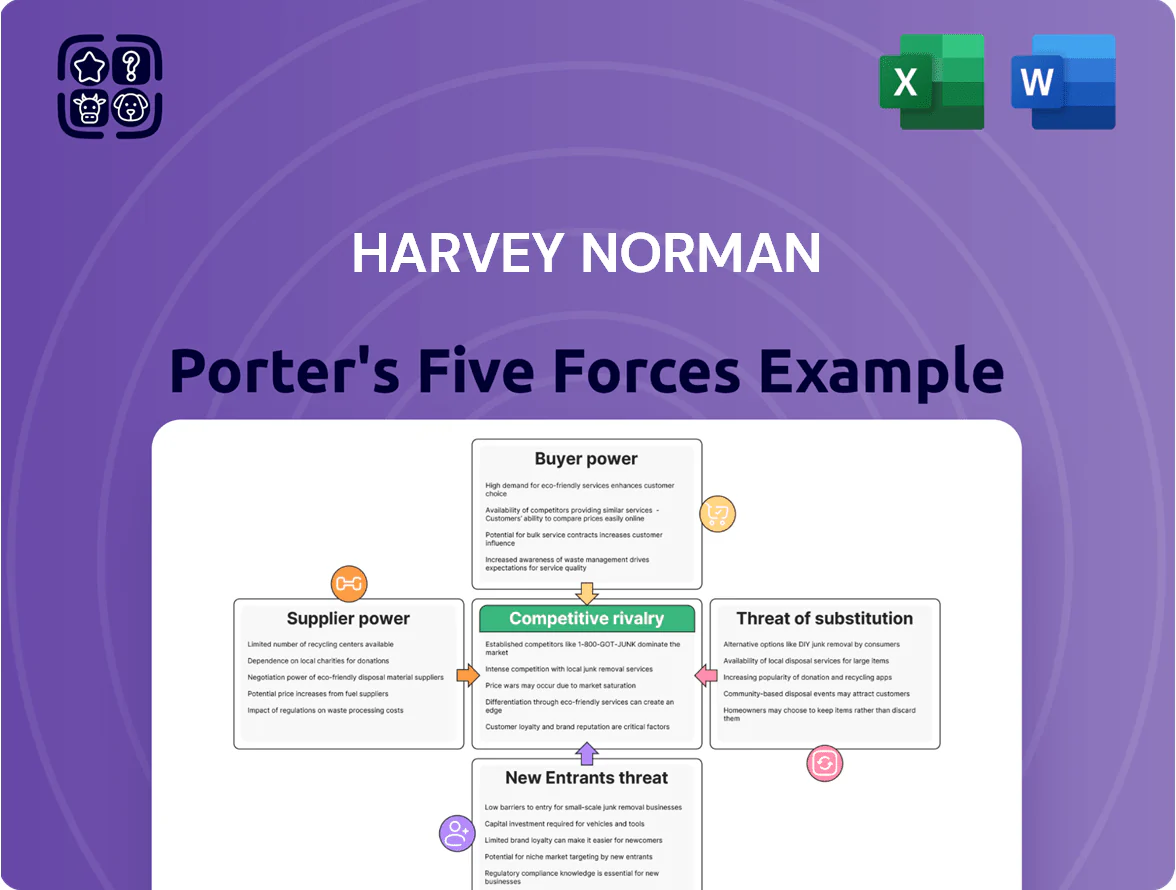

Harvey Norman faces mixed competitive pressures: strong supplier relationships but intense retail rivalry and shifting consumer power due to online competitors; substitutes and the threat of new entrants are moderate, while firm rivalry remains high—this snapshot highlights strategic tensions and operational risks.

Suppliers Bargaining Power

Concentration of global technology brands

The supplier side is concentrated: Samsung, Apple and LG together held about 62% of global smartphone and premium TV market share in 2024, limiting Harvey Norman’s bargaining leverage. These brands set prices and control allocations, driven by strong consumer demand and Apple’s 2024 iPhone ASP of ~USD 860. Harvey Norman must secure preferred terms and joint promotions to keep high-margin electronics stocked. Losing priority allocation would cut gross margin and sales velocity quickly.

Importance of volume to suppliers

As one of Australia’s largest retailers with FY2024 group revenue of A$6.3 billion, Harvey Norman delivers suppliers high-volume access across ~200 domestic stores and 290+ franchisees internationally, boosting negotiation leverage for bulk discounts and marketing support.

This scale helps secure exclusive product launches and better payment terms versus small independents; suppliers gain faster sell-through and larger reorder cycles.

Therefore, while key suppliers (electronics, appliances) retain product power, Harvey Norman’s volume-moving role meaningfully counterbalances supplier bargaining power.

Franchisee procurement autonomy

Harvey Norman’s franchise model gives local franchisees control over stock decisions, which can weaken collective supplier leverage versus a fully owned chain; about 60% of Australian stores are franchised, so buying choices are fragmented. Centralised initiatives—national marketing and a corporate supply team—reclaim bargaining power for major deals, contributing to reported group-level procurement savings of ~3–5% in FY2024. Still, supplier negotiations can be uneven across regions, raising price variance risk.

Supplier vertical integration trends

Suppliers are shifting to direct-to-consumer (DTC): global DTC retail sales reached about US$111bn in 2024, up ~12% year-on-year, letting suppliers keep larger margins and reduce reliance on Harvey Norman.

This vertical integration raises supplier bargaining power, as brands can pull sales from third-party channels and demand better terms or exclusive services.

Harvey Norman must offer value-added services—omnichannel fulfilment, premium in-store experiences, exclusive launches—to retain partner suppliers and protect margins.

- 2024 DTC sales ~US$111bn (+12% YoY)

- Suppliers capturing higher margins, pressuring retailer margins

- Need for Harvey Norman: omnichannel, exclusives, premium services

Switching costs for retail inventory

Switching costs for Harvey Norman are high: electronics need certified installers and warranties while furniture demands specific floor layouts, driving re-fit costs of A$2–5m per large store based on 2024 remodel estimates.

Leaving major brands risks logistics complexity, stock write-offs (averaging 1.8% of inventory per FY2024) and reduced footfall; Harvey Norman thus follows suppliers’ product cycles.

- High re-fit cost A$2–5m/store

- Inventory write-offs ~1.8% FY2024

- Dependent on supplier product cycles

Supplier Power Upends Harvey Norman: 62% Premium Grip, DTC Surge, High Switching Costs

Suppliers (Samsung, Apple, LG) held ~62% of premium categories in 2024, boosting their price and allocation power vs Harvey Norman; Apple’s 2024 iPhone ASP ≈ USD860. Harvey Norman’s FY2024 revenue A$6.3bn and ~200 AU stores + 290+ franchisees give scale to win bulk terms, but 60% franchised stores fragment buying. DTC reached ~US$111bn (2024), raising supplier leverage; store refit costs A$2–5m and inventory write-offs ~1.8% raise switching costs.

| Metric | 2024 value |

|---|---|

| Key suppliers share | ~62% |

| Harvey Norman revenue | A$6.3bn |

| Stores (AU) | ~200 |

| Franchised stores | ~60% |

| DTC sales | US$111bn (+12% YoY) |

| iPhone ASP | ~USD860 |

| Refit cost / large store | A$2–5m |

| Inventory write-offs | ~1.8% revenue |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and industry rivalry specific to Harvey Norman, highlighting disruptive threats, pricing influence, and strategic levers to protect market share.

A concise Porter's Five Forces snapshot for Harvey Norman—distilling competitive pressures into one-sheet clarity to speed strategic decisions and boardroom discussion.

Customers Bargaining Power

High price sensitivity and transparency

Customers in electronics and home goods are highly price-sensitive; 78% of Australian shoppers used price comparison tools in 2024, pushing Harvey Norman to match online rivals to retain sales.

Real-time transparency means Harvey Norman often runs price-matching and promotional campaigns; in FY2024 comparable sales grew only 2.3%, showing margin pressure from discounts.

Switching is easy for identical branded goods, keeping bargaining power with consumers and forcing tighter gross margins—Harvey Norman’s gross profit margin fell to 29.1% in FY2024.

Low switching costs for shoppers

Low switching costs mean Australian shoppers can pick a competitor for laptops or sofas with little friction; 2024 Roy Morgan data shows 45% of electronics buyers choose based on price and availability rather than brand. Brand loyalty yields to same-day stock and discounts, so Harvey Norman faced a 2.8% like-for-like sales dip in FY2024 quarters when rivals ran heavy promos. That forces ongoing spend on loyalty programs and frontline service to avoid churn.

Impact of consumer sentiment and interest rates

Harvey Norman sells high-ticket discretionary goods—furniture and premium electronics—so higher interest rates and falling consumer confidence sharply cut demand; Australia’s household saving ratio rose to 6.3% in Q3 2024 while the RBA cash rate hit 4.35% in Nov 2024, letting buyers defer purchases or trade down.

This shifts bargaining power to consumers, who in 2024 drove a 4.2% drop in Australian retail furniture sales year-on-year, forcing Harvey Norman into deeper discounting and extended promotions to protect volumes.

The rise of online marketplaces

The rise of online marketplaces like Amazon and eBay gives Australian consumers far more choice than Harvey Norman, with Amazon Australia hitting an estimated AU$4.3bn GMV in 2023 and eBay reporting AU$3.1bn in 2024, pressuring Harvey Norman to prove its value.

Lower online overhead and broader assortment force customers to demand better service, faster delivery (same-day or 2‑3 day), and sharper pricing, squeezing Harvey Norman’s margins and forcing omnichannel investments.

- Amazon AU GMV ~AU$4.3bn (2023)

- eBay AU GMV ~AU$3.1bn (2024)

- Customers expect 2–3 day delivery or same-day

- Price and service now primary loyalty drivers

Influence of product reviews and social proof

Modern buyers rely on peer reviews and social media; 72% of Australian shoppers consult online reviews before big-ticket purchases (2024 Nielsen study), so negative sentiment can quickly cut Harvey Norman’s share as consumers favor better-rated rivals.

The rise of review platforms and influencers shifts information symmetry, giving individual buyers more power than in past decades and making digital reputation a direct driver of sales and margin.

- 72% consult reviews (2024)

- Negative review spike can lower conversion rates by ~20%

- Digital reputation now directly affects market share

Price-savvy consumers squeeze Harvey Norman: margins fall as promos, omnichannel rise

Customers hold strong bargaining power: price transparency (78% used price tools, 2024) and low switching costs drove Harvey Norman to price-match, cutting gross margin to 29.1% (FY2024) and comparable sales growth to 2.3%; higher rates (RBA 4.35% Nov 2024) and 4.2% drop in furniture sales (2024) forced deeper promos and omnichannel spend.

| Metric | Value |

|---|---|

| Price tools (2024) | 78% |

| Gross margin FY2024 | 29.1% |

| Comp sales growth FY2024 | 2.3% |

| RBA cash rate Nov 2024 | 4.35% |

| Furniture sales change 2024 | -4.2% |

Full Version Awaits

Harvey Norman Porter's Five Forces Analysis

This preview shows the exact Harvey Norman Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

You're looking at the actual, professionally written file; once you complete your purchase, you’ll get instant access to this same document, ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Harvey Norman faces mixed competitive pressures: strong supplier relationships but intense retail rivalry and shifting consumer power due to online competitors; substitutes and the threat of new entrants are moderate, while firm rivalry remains high—this snapshot highlights strategic tensions and operational risks.

Suppliers Bargaining Power

Concentration of global technology brands

The supplier side is concentrated: Samsung, Apple and LG together held about 62% of global smartphone and premium TV market share in 2024, limiting Harvey Norman’s bargaining leverage. These brands set prices and control allocations, driven by strong consumer demand and Apple’s 2024 iPhone ASP of ~USD 860. Harvey Norman must secure preferred terms and joint promotions to keep high-margin electronics stocked. Losing priority allocation would cut gross margin and sales velocity quickly.

Importance of volume to suppliers

As one of Australia’s largest retailers with FY2024 group revenue of A$6.3 billion, Harvey Norman delivers suppliers high-volume access across ~200 domestic stores and 290+ franchisees internationally, boosting negotiation leverage for bulk discounts and marketing support.

This scale helps secure exclusive product launches and better payment terms versus small independents; suppliers gain faster sell-through and larger reorder cycles.

Therefore, while key suppliers (electronics, appliances) retain product power, Harvey Norman’s volume-moving role meaningfully counterbalances supplier bargaining power.

Franchisee procurement autonomy

Harvey Norman’s franchise model gives local franchisees control over stock decisions, which can weaken collective supplier leverage versus a fully owned chain; about 60% of Australian stores are franchised, so buying choices are fragmented. Centralised initiatives—national marketing and a corporate supply team—reclaim bargaining power for major deals, contributing to reported group-level procurement savings of ~3–5% in FY2024. Still, supplier negotiations can be uneven across regions, raising price variance risk.

Supplier vertical integration trends

Suppliers are shifting to direct-to-consumer (DTC): global DTC retail sales reached about US$111bn in 2024, up ~12% year-on-year, letting suppliers keep larger margins and reduce reliance on Harvey Norman.

This vertical integration raises supplier bargaining power, as brands can pull sales from third-party channels and demand better terms or exclusive services.

Harvey Norman must offer value-added services—omnichannel fulfilment, premium in-store experiences, exclusive launches—to retain partner suppliers and protect margins.

- 2024 DTC sales ~US$111bn (+12% YoY)

- Suppliers capturing higher margins, pressuring retailer margins

- Need for Harvey Norman: omnichannel, exclusives, premium services

Switching costs for retail inventory

Switching costs for Harvey Norman are high: electronics need certified installers and warranties while furniture demands specific floor layouts, driving re-fit costs of A$2–5m per large store based on 2024 remodel estimates.

Leaving major brands risks logistics complexity, stock write-offs (averaging 1.8% of inventory per FY2024) and reduced footfall; Harvey Norman thus follows suppliers’ product cycles.

- High re-fit cost A$2–5m/store

- Inventory write-offs ~1.8% FY2024

- Dependent on supplier product cycles

Supplier Power Upends Harvey Norman: 62% Premium Grip, DTC Surge, High Switching Costs

Suppliers (Samsung, Apple, LG) held ~62% of premium categories in 2024, boosting their price and allocation power vs Harvey Norman; Apple’s 2024 iPhone ASP ≈ USD860. Harvey Norman’s FY2024 revenue A$6.3bn and ~200 AU stores + 290+ franchisees give scale to win bulk terms, but 60% franchised stores fragment buying. DTC reached ~US$111bn (2024), raising supplier leverage; store refit costs A$2–5m and inventory write-offs ~1.8% raise switching costs.

| Metric | 2024 value |

|---|---|

| Key suppliers share | ~62% |

| Harvey Norman revenue | A$6.3bn |

| Stores (AU) | ~200 |

| Franchised stores | ~60% |

| DTC sales | US$111bn (+12% YoY) |

| iPhone ASP | ~USD860 |

| Refit cost / large store | A$2–5m |

| Inventory write-offs | ~1.8% revenue |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, substitutes, and industry rivalry specific to Harvey Norman, highlighting disruptive threats, pricing influence, and strategic levers to protect market share.

A concise Porter's Five Forces snapshot for Harvey Norman—distilling competitive pressures into one-sheet clarity to speed strategic decisions and boardroom discussion.

Customers Bargaining Power

High price sensitivity and transparency

Customers in electronics and home goods are highly price-sensitive; 78% of Australian shoppers used price comparison tools in 2024, pushing Harvey Norman to match online rivals to retain sales.

Real-time transparency means Harvey Norman often runs price-matching and promotional campaigns; in FY2024 comparable sales grew only 2.3%, showing margin pressure from discounts.

Switching is easy for identical branded goods, keeping bargaining power with consumers and forcing tighter gross margins—Harvey Norman’s gross profit margin fell to 29.1% in FY2024.

Low switching costs for shoppers

Low switching costs mean Australian shoppers can pick a competitor for laptops or sofas with little friction; 2024 Roy Morgan data shows 45% of electronics buyers choose based on price and availability rather than brand. Brand loyalty yields to same-day stock and discounts, so Harvey Norman faced a 2.8% like-for-like sales dip in FY2024 quarters when rivals ran heavy promos. That forces ongoing spend on loyalty programs and frontline service to avoid churn.

Impact of consumer sentiment and interest rates

Harvey Norman sells high-ticket discretionary goods—furniture and premium electronics—so higher interest rates and falling consumer confidence sharply cut demand; Australia’s household saving ratio rose to 6.3% in Q3 2024 while the RBA cash rate hit 4.35% in Nov 2024, letting buyers defer purchases or trade down.

This shifts bargaining power to consumers, who in 2024 drove a 4.2% drop in Australian retail furniture sales year-on-year, forcing Harvey Norman into deeper discounting and extended promotions to protect volumes.

The rise of online marketplaces

The rise of online marketplaces like Amazon and eBay gives Australian consumers far more choice than Harvey Norman, with Amazon Australia hitting an estimated AU$4.3bn GMV in 2023 and eBay reporting AU$3.1bn in 2024, pressuring Harvey Norman to prove its value.

Lower online overhead and broader assortment force customers to demand better service, faster delivery (same-day or 2‑3 day), and sharper pricing, squeezing Harvey Norman’s margins and forcing omnichannel investments.

- Amazon AU GMV ~AU$4.3bn (2023)

- eBay AU GMV ~AU$3.1bn (2024)

- Customers expect 2–3 day delivery or same-day

- Price and service now primary loyalty drivers

Influence of product reviews and social proof

Modern buyers rely on peer reviews and social media; 72% of Australian shoppers consult online reviews before big-ticket purchases (2024 Nielsen study), so negative sentiment can quickly cut Harvey Norman’s share as consumers favor better-rated rivals.

The rise of review platforms and influencers shifts information symmetry, giving individual buyers more power than in past decades and making digital reputation a direct driver of sales and margin.

- 72% consult reviews (2024)

- Negative review spike can lower conversion rates by ~20%

- Digital reputation now directly affects market share

Price-savvy consumers squeeze Harvey Norman: margins fall as promos, omnichannel rise

Customers hold strong bargaining power: price transparency (78% used price tools, 2024) and low switching costs drove Harvey Norman to price-match, cutting gross margin to 29.1% (FY2024) and comparable sales growth to 2.3%; higher rates (RBA 4.35% Nov 2024) and 4.2% drop in furniture sales (2024) forced deeper promos and omnichannel spend.

| Metric | Value |

|---|---|

| Price tools (2024) | 78% |

| Gross margin FY2024 | 29.1% |

| Comp sales growth FY2024 | 2.3% |

| RBA cash rate Nov 2024 | 4.35% |

| Furniture sales change 2024 | -4.2% |

Full Version Awaits

Harvey Norman Porter's Five Forces Analysis

This preview shows the exact Harvey Norman Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

You're looking at the actual, professionally written file; once you complete your purchase, you’ll get instant access to this same document, ready for immediate use.