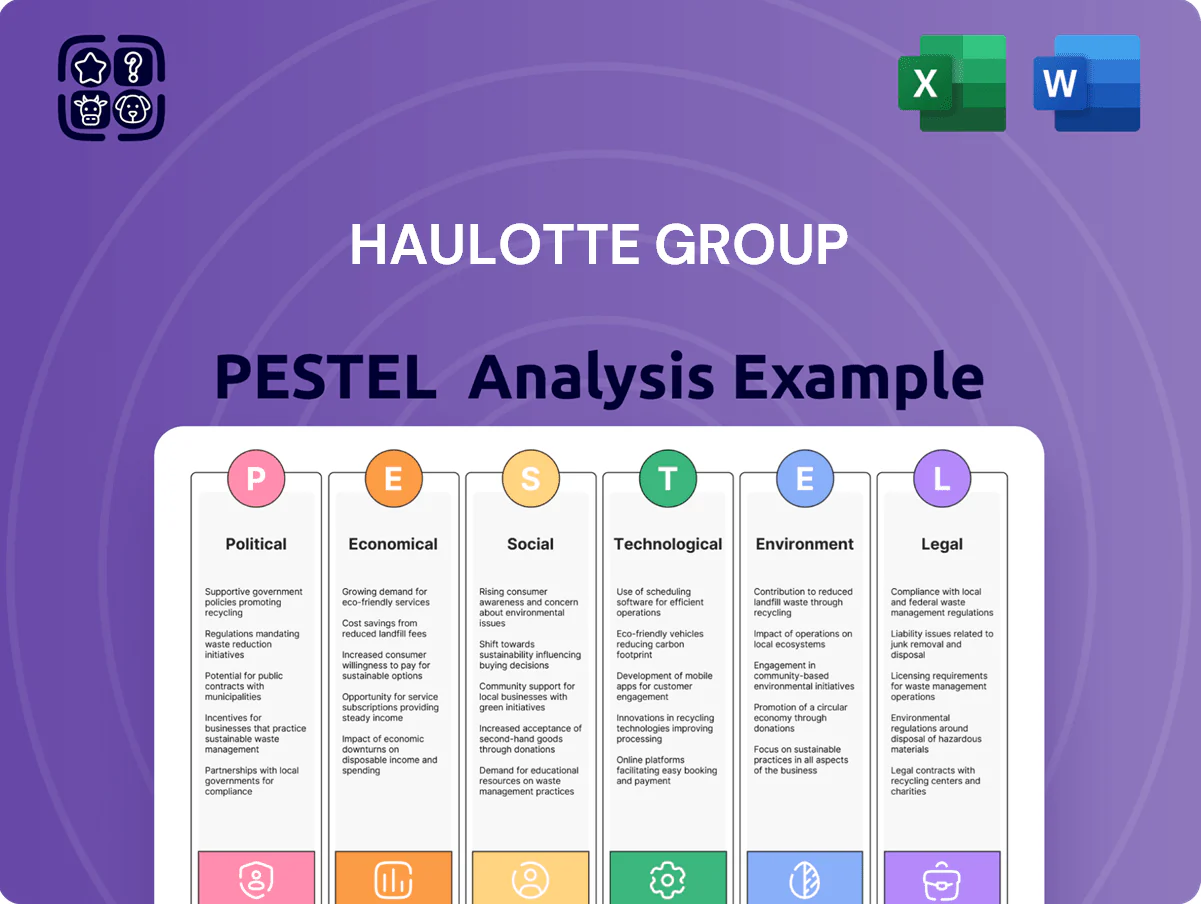

Haulotte Group PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic edge with our targeted PESTLE Analysis of Haulotte Group—uncover how political shifts, economic cycles, and technological innovation will shape its market position and risk profile; perfect for investors and strategists seeking actionable insights. Purchase the full report to access the complete, fully editable breakdown and make smarter decisions with confidence.

Political factors

Trade Protectionism and Anti-Dumping Duties

The 2019 EU provisional anti-dumping measures and subsequent 2023 US investigations into Chinese aerial-work platforms have curtailed low-priced imports, helping Haulotte preserve roughly its 12–15% share of the European market and support FY2024 reported average selling prices up ~4% year-on-year.

These duties bolster Haulotte’s pricing power and margins versus Chinese competitors, contributing to its 2024 EBITDA margin resilience (around 8–9% reported).

Strategists must track periodic reviews and negotiations between the EU, US and China, as tariff adjustments or trade deals could quickly shift competitive dynamics and market access.

Government Infrastructure Stimulus Programs

Large-scale public investments like the European Green Deal and EU Recovery and Resilience Facility (€723bn) boost demand for aerial work platforms, driving orders for Haulotte tied to infrastructure and retrofit projects.

National recovery plans—France’s €100bn France 2030 and Germany’s €50bn climate package—prioritize energy-efficient renovations, increasing need for specialized lifting equipment Haulotte supplies.

These multi-year funding commitments create a stable project pipeline for Haulotte’s rental-company clients through 2026, supporting recurring fleet demand and aftermarket services.

Geopolitical Instability and Supply Chain Security

Ongoing tensions in Eastern Europe and the Middle East have raised global supply-chain risk, with IHS Markit reporting 12%+ surge in logistics costs in 2024 and semiconductor lead times averaging 20 weeks, pressuring Haulotte to diversify suppliers and boost local sourcing to protect margins.

Labor Regulations and Workforce Policy

As a major employer in France and globally, Haulotte is exposed to changes in working hours, retirement age and social protections; France’s 2024 pension reform raised retirement age to 64, affecting labor costs and HR planning for firms with >3,000 employees—Haulotte had ~1,900 employees in 2023, concentrating impact in French sites.

Political moves toward flexible labor markets could lower unit labor costs, while stronger protections (social charges ~45% employer for some schemes) raise manufacturing overhead and reduce agility.

Strict compliance is essential to avoid strikes (French strike frequency remains among highest in EU) and legal fines; industrial disputes can halt production and hit FY revenue (2023 group revenue €652m) and margin.

- 2023 employees ~1,900; 2023 revenue €652m

- Pension reform 2024: retirement age 64 — affects staffing costs

- Employer social charges can approach 45% in France

- High strike risk in France increases operational disruption exposure

Export Control and International Sanctions

Compliance with export control regimes (Wassenaar Arrangement, EU Dual-Use Regulation) is mandatory for Haulotte, which exported €575m worldwide in 2024, making due diligence on dual-use technologies critical.

Political sanctions—e.g., EU/US restrictions on Russia and Iran—limit market access and force enhanced end-user checks to prevent diversion to prohibited jurisdictions.

Non-compliance risks fines (up to 10% of annual revenue in some jurisdictions), supply-chain disruptions and reputational loss, as seen in 2023–24 enforcement actions across the sector.

- Mandatory adherence to Wassenaar and EU dual-use rules

- Sanctions restrict access to sanctioned countries (Russia, Iran) requiring strict end-user verification

- Enforcement risk: fines up to ~10% revenue, plus reputational damage

Haulotte buoyed by EU/US protection and public funds despite rising logistics, sourcing

EU/US anti-dumping and investigations have protected Haulotte’s ~12–15% EU share and supported FY2024 ASPs up ~4%, aiding ~8–9% EBITDA margin; public funds (EU Recovery €723bn, France 2030 €100bn) sustain order pipelines through 2026; geopolitical tensions raised logistics costs ~12% in 2024 and semiconductor lead times ~20 weeks, pressuring sourcing; France pension reform to 64 affects labor costs for Haulotte’s ~1,900 employees (2023, revenue €652m).

| Metric | Value |

|---|---|

| EU market share | 12–15% |

| FY2024 ASP change | +4% YoY |

| EBITDA margin (2024) | ~8–9% |

| 2023 employees / revenue | ~1,900 / €652m |

| Logistics cost rise (2024) | ~12% |

| Semiconductor lead time | ~20 weeks |

| EU Recovery fund | €723bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Haulotte Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven insights and forward-looking implications tailored to its aerial work platform and access-equipment markets.

A concise, visually segmented PESTLE summary for Haulotte that’s easy to drop into presentations or share across teams, enabling quick risk assessment and alignment during planning sessions.

Economic factors

Interest Rate Environment and Financing Costs

The prevailing interest rate environment directly affects purchasing power for equipment rental firms, Haulotte's primary customers; euro-area policy rates rose to 4.5% in 2024 and averaged ~3.8% in 2025, increasing financing costs and slowing fleet renewals. High borrowing costs pushed rental companies to extend machinery life, contributing to a 2024–25 industry order decline of roughly 10–15% in Europe. If rates stabilize or fall toward 2026, cheaper credit could trigger a rebound in new equipment orders and capex, potentially restoring pre-2022 demand levels within 12–18 months.

Raw Material and Commodity Price Volatility

The cost of steel, aluminum and advanced polymers—steel up ~15% in 2023–24 and aluminum spot prices averaging $2,200/ton in 2024—remains a primary driver of Haulotte’s manufacturing expenses, accounting for an estimated 30–40% of COGS. Economic volatility forces dynamic pricing and hedging; Haulotte reported using commodity hedges covering roughly 20% of expected purchases in FY2024. Analysts monitor the group’s ability to pass costs to end customers without eroding market share in a crowded global aerial work platform market.

Currency Exchange Rate Fluctuations

As a Euro-reporting firm with large Americas and Asia operations, Haulotte faces sizable transaction and translation risk; in 2024 roughly 30% of revenue was non-euro denominated, amplifying FX exposure. A 10% euro appreciation vs USD or CNY would materially erode export competitiveness and reduce reported earnings—2024 EBITDA margin sensitivity estimated at ~120–180 bps per 10% move. Analysts track Haulotte’s hedging: as of FY2024 about 65% of short-term FX flows were hedged via forwards/options. Robust hedging execution is viewed as critical to earnings stability amid 2024–25 USD and CNY volatility.

Growth of the Equipment Rental Market

- Global rental market ~USD 120B (2024), CAGR ~5-6% to 2028

- Consolidated rental firms increase share of fleet purchases

- Better demand forecasting vs. higher buyer bargaining power

Global Inflation and Operating Expenditure

- Energy/materials +6–12% impact on unit costs

- Technician wage growth ~5% (EU 2024)

- OPEX pressure 8–12% for OEMs (2023–24)

- Focus: lean ops, supplier diversification, wage competitiveness

Higher euro rates, commodity inflation squeeze margins; rental market growth offsets FX risk

Higher euro-area rates (~4.5% in 2024, ~3.8% avg 2025) raised financing costs and cut fleet renewals; commodity inflation (steel +15% 2023–24, aluminum ~$2,200/t 2024) increased COGS ~30–40%; rental market ~USD120B (2024) growing 5–6% CAGR to 2028 boosts demand but consolidation raises buyer power; FX exposure ~30% non-euro revenue with ~120–180bps EBITDA sensitivity per 10% move.

| Metric | Value |

|---|---|

| Euro policy rate (2024) | 4.5% |

| Avg rate (2025) | ~3.8% |

| Rental market (2024) | USD 120B |

| Steel change (2023–24) | +15% |

| Aluminum (2024) | $2,200/t |

| Non-euro revenue | ~30% |

| EBITDA sensitivity per 10% FX | 120–180bps |

Preview Before You Purchase

Haulotte Group PESTLE Analysis

The Haulotte Group PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic and investment decisions.

No placeholders or teasers: the content, layout, and structure visible in this preview are the real, final file you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic edge with our targeted PESTLE Analysis of Haulotte Group—uncover how political shifts, economic cycles, and technological innovation will shape its market position and risk profile; perfect for investors and strategists seeking actionable insights. Purchase the full report to access the complete, fully editable breakdown and make smarter decisions with confidence.

Political factors

Trade Protectionism and Anti-Dumping Duties

The 2019 EU provisional anti-dumping measures and subsequent 2023 US investigations into Chinese aerial-work platforms have curtailed low-priced imports, helping Haulotte preserve roughly its 12–15% share of the European market and support FY2024 reported average selling prices up ~4% year-on-year.

These duties bolster Haulotte’s pricing power and margins versus Chinese competitors, contributing to its 2024 EBITDA margin resilience (around 8–9% reported).

Strategists must track periodic reviews and negotiations between the EU, US and China, as tariff adjustments or trade deals could quickly shift competitive dynamics and market access.

Government Infrastructure Stimulus Programs

Large-scale public investments like the European Green Deal and EU Recovery and Resilience Facility (€723bn) boost demand for aerial work platforms, driving orders for Haulotte tied to infrastructure and retrofit projects.

National recovery plans—France’s €100bn France 2030 and Germany’s €50bn climate package—prioritize energy-efficient renovations, increasing need for specialized lifting equipment Haulotte supplies.

These multi-year funding commitments create a stable project pipeline for Haulotte’s rental-company clients through 2026, supporting recurring fleet demand and aftermarket services.

Geopolitical Instability and Supply Chain Security

Ongoing tensions in Eastern Europe and the Middle East have raised global supply-chain risk, with IHS Markit reporting 12%+ surge in logistics costs in 2024 and semiconductor lead times averaging 20 weeks, pressuring Haulotte to diversify suppliers and boost local sourcing to protect margins.

Labor Regulations and Workforce Policy

As a major employer in France and globally, Haulotte is exposed to changes in working hours, retirement age and social protections; France’s 2024 pension reform raised retirement age to 64, affecting labor costs and HR planning for firms with >3,000 employees—Haulotte had ~1,900 employees in 2023, concentrating impact in French sites.

Political moves toward flexible labor markets could lower unit labor costs, while stronger protections (social charges ~45% employer for some schemes) raise manufacturing overhead and reduce agility.

Strict compliance is essential to avoid strikes (French strike frequency remains among highest in EU) and legal fines; industrial disputes can halt production and hit FY revenue (2023 group revenue €652m) and margin.

- 2023 employees ~1,900; 2023 revenue €652m

- Pension reform 2024: retirement age 64 — affects staffing costs

- Employer social charges can approach 45% in France

- High strike risk in France increases operational disruption exposure

Export Control and International Sanctions

Compliance with export control regimes (Wassenaar Arrangement, EU Dual-Use Regulation) is mandatory for Haulotte, which exported €575m worldwide in 2024, making due diligence on dual-use technologies critical.

Political sanctions—e.g., EU/US restrictions on Russia and Iran—limit market access and force enhanced end-user checks to prevent diversion to prohibited jurisdictions.

Non-compliance risks fines (up to 10% of annual revenue in some jurisdictions), supply-chain disruptions and reputational loss, as seen in 2023–24 enforcement actions across the sector.

- Mandatory adherence to Wassenaar and EU dual-use rules

- Sanctions restrict access to sanctioned countries (Russia, Iran) requiring strict end-user verification

- Enforcement risk: fines up to ~10% revenue, plus reputational damage

Haulotte buoyed by EU/US protection and public funds despite rising logistics, sourcing

EU/US anti-dumping and investigations have protected Haulotte’s ~12–15% EU share and supported FY2024 ASPs up ~4%, aiding ~8–9% EBITDA margin; public funds (EU Recovery €723bn, France 2030 €100bn) sustain order pipelines through 2026; geopolitical tensions raised logistics costs ~12% in 2024 and semiconductor lead times ~20 weeks, pressuring sourcing; France pension reform to 64 affects labor costs for Haulotte’s ~1,900 employees (2023, revenue €652m).

| Metric | Value |

|---|---|

| EU market share | 12–15% |

| FY2024 ASP change | +4% YoY |

| EBITDA margin (2024) | ~8–9% |

| 2023 employees / revenue | ~1,900 / €652m |

| Logistics cost rise (2024) | ~12% |

| Semiconductor lead time | ~20 weeks |

| EU Recovery fund | €723bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Haulotte Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven insights and forward-looking implications tailored to its aerial work platform and access-equipment markets.

A concise, visually segmented PESTLE summary for Haulotte that’s easy to drop into presentations or share across teams, enabling quick risk assessment and alignment during planning sessions.

Economic factors

Interest Rate Environment and Financing Costs

The prevailing interest rate environment directly affects purchasing power for equipment rental firms, Haulotte's primary customers; euro-area policy rates rose to 4.5% in 2024 and averaged ~3.8% in 2025, increasing financing costs and slowing fleet renewals. High borrowing costs pushed rental companies to extend machinery life, contributing to a 2024–25 industry order decline of roughly 10–15% in Europe. If rates stabilize or fall toward 2026, cheaper credit could trigger a rebound in new equipment orders and capex, potentially restoring pre-2022 demand levels within 12–18 months.

Raw Material and Commodity Price Volatility

The cost of steel, aluminum and advanced polymers—steel up ~15% in 2023–24 and aluminum spot prices averaging $2,200/ton in 2024—remains a primary driver of Haulotte’s manufacturing expenses, accounting for an estimated 30–40% of COGS. Economic volatility forces dynamic pricing and hedging; Haulotte reported using commodity hedges covering roughly 20% of expected purchases in FY2024. Analysts monitor the group’s ability to pass costs to end customers without eroding market share in a crowded global aerial work platform market.

Currency Exchange Rate Fluctuations

As a Euro-reporting firm with large Americas and Asia operations, Haulotte faces sizable transaction and translation risk; in 2024 roughly 30% of revenue was non-euro denominated, amplifying FX exposure. A 10% euro appreciation vs USD or CNY would materially erode export competitiveness and reduce reported earnings—2024 EBITDA margin sensitivity estimated at ~120–180 bps per 10% move. Analysts track Haulotte’s hedging: as of FY2024 about 65% of short-term FX flows were hedged via forwards/options. Robust hedging execution is viewed as critical to earnings stability amid 2024–25 USD and CNY volatility.

Growth of the Equipment Rental Market

- Global rental market ~USD 120B (2024), CAGR ~5-6% to 2028

- Consolidated rental firms increase share of fleet purchases

- Better demand forecasting vs. higher buyer bargaining power

Global Inflation and Operating Expenditure

- Energy/materials +6–12% impact on unit costs

- Technician wage growth ~5% (EU 2024)

- OPEX pressure 8–12% for OEMs (2023–24)

- Focus: lean ops, supplier diversification, wage competitiveness

Higher euro rates, commodity inflation squeeze margins; rental market growth offsets FX risk

Higher euro-area rates (~4.5% in 2024, ~3.8% avg 2025) raised financing costs and cut fleet renewals; commodity inflation (steel +15% 2023–24, aluminum ~$2,200/t 2024) increased COGS ~30–40%; rental market ~USD120B (2024) growing 5–6% CAGR to 2028 boosts demand but consolidation raises buyer power; FX exposure ~30% non-euro revenue with ~120–180bps EBITDA sensitivity per 10% move.

| Metric | Value |

|---|---|

| Euro policy rate (2024) | 4.5% |

| Avg rate (2025) | ~3.8% |

| Rental market (2024) | USD 120B |

| Steel change (2023–24) | +15% |

| Aluminum (2024) | $2,200/t |

| Non-euro revenue | ~30% |

| EBITDA sensitivity per 10% FX | 120–180bps |

Preview Before You Purchase

Haulotte Group PESTLE Analysis

The Haulotte Group PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic and investment decisions.

No placeholders or teasers: the content, layout, and structure visible in this preview are the real, final file you’ll download immediately after payment.