Hyundai Engineering Boston Consulting Group Matrix

See the Bigger Picture

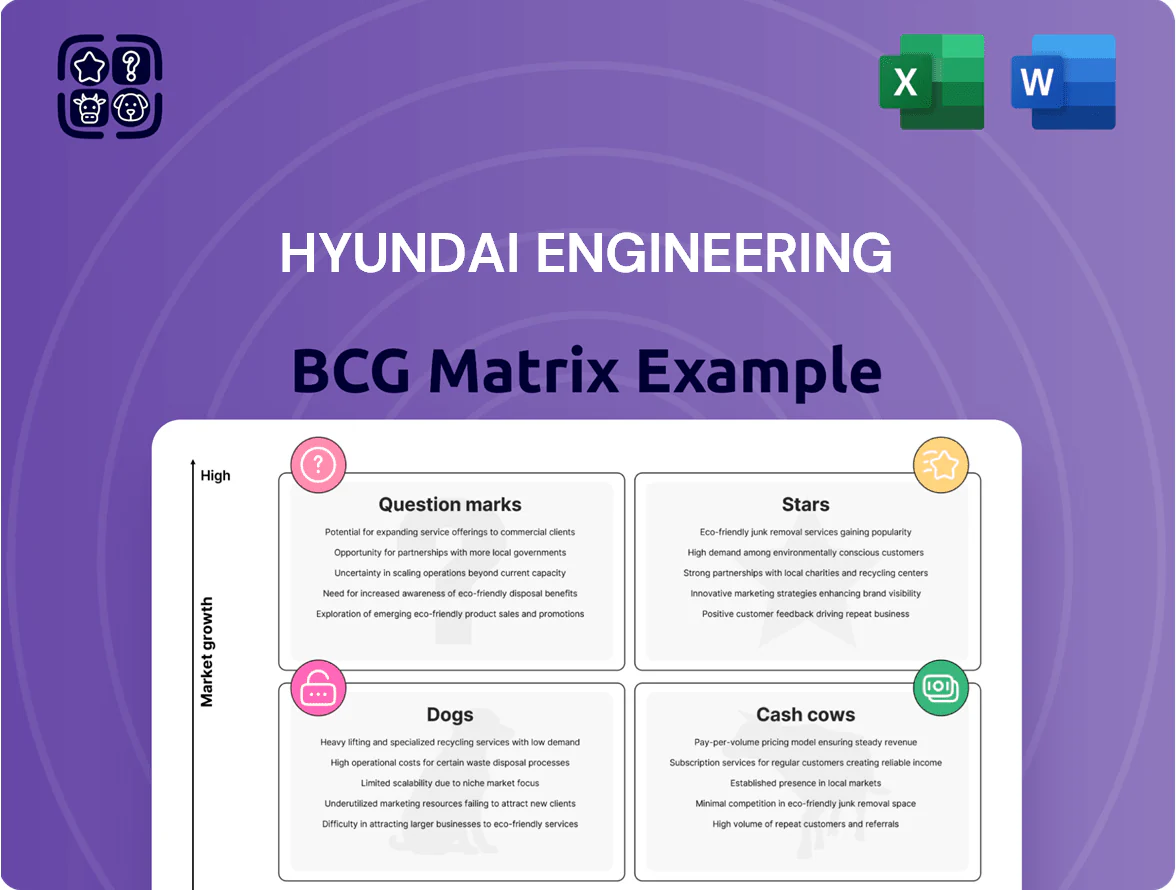

Hyundai Engineering’s BCG Matrix preview highlights key business units navigating rapid industrial demand and capital-intensive projects, showing likely Stars in EPC segments and potential Question Marks in emerging green-tech ventures; Cash Cows appear in steady domestic infrastructure services while lower-margin legacy offerings risk becoming Dogs. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Renewable Energy EPC

As of late 2025, Hyundai Engineering leads global renewable EPC with >9 GW of awarded solar and wind capacity and revenue from the segment up 38% YoY to KRW 2.1 trillion in 2024, driven by decarbonization mandates and $45 billion estimated capital inflows into renewables in APAC 2023–25.

The sector shows high growth and Hyundai holds a high market share in utility-scale projects, winning multi-year EPC contracts worth KRW 1.4 trillion; continuous capex of ~KRW 300–400 billion annually is needed to fend off emerging global competitors.

Hydrogen Production Facilities

Hydrogen Production Facilities: Hyundai Engineering holds a leading share in blue and green hydrogen infrastructure, with ~18% of Korea’s recent project wins through 2024 and >$1.2bn backlog in hydrogen contracts as of Dec 31, 2024; fast market growth (CAGR ~15% to 2030) makes this a star with high market share and market growth.

These projects need heavy R&D and capex—Hyundai booked ~KRW 1.6tn (≈$1.2bn) capex commitments in 2023–24—so cash burn is high but revenues are large; ongoing investment is required to convert pilot assets into steady cash generators by 2028–2030.

Eco-friendly Plastic Recycling Plants

Hyundai Engineering leads chemical recycling—converting plastic waste to fuel/raw materials—with proprietary tech and commercial-scale plants, positioning it as a market leader in the circular economy.

Global chemical recycling demand is rising ~12–18% CAGR to 2030; tightened ESG rules for petrochemical clients drive rapid adoption, increasing addressable market to an estimated $15–20B by 2030.

Early projects and IP give Hyundai scale advantages, but sustaining a top position requires continued capex; company disclosed KRW 350–450B planned investment for recycling and decarbonization through 2026.

Small Modular Reactors (SMRs)

Hyundai Engineering positions SMRs as a star: global SMR market projected at $150–220 billion by 2040, and Hyundai holds reactors/technology partnerships covering projects in UAE, UK bids, and Korea R&D with estimated CAPEX per SMR $500–900 million—high growth and strategic scale justify heavy investment for carbon-free baseload leadership.

These capital-intensive projects demand continued R&D and global placement support; successful deployment could capture double-digit market share in exports and long-term service revenue, making SMRs a core star in Hyundai Engineering’s portfolio.

- Market size: $150–220B by 2040 (industry estimates, 2024–25)

- Hyundai: active partnerships in UAE, UK bids, Korea R&D

- Estimated CAPEX per SMR: $500–900M

- Outcome: high support needed for long-term export and service revenue

Sustainable Infrastructure in Emerging Markets

Hyundai Engineering leads high-growth urban development projects in Southeast Asia and the Middle East, focusing on smart-city integration and sustainable infrastructure, capturing an estimated 18–22% market share in landmark projects as of 2025 and contributing roughly $1.2–1.6 billion annual revenue from the segment.

These regions show >6% CAGR demand for green infrastructure through 2030, but intense competition and scale require continual reinvestment; maintaining leadership is pivotal for Hyundai’s long-term strategic growth.

- High market share: 18–22% (2025)

- Segment revenue: $1.2–1.6B annually

- Regional demand CAGR: >6% through 2030

- Risk: heavy reinvestment, competitive pressure

Hyundai Engineering: Renewable leader with big hydrogen, recycling & SMR upside

Stars: Hyundai Engineering dominates renewables, hydrogen, chemical recycling, SMRs, and smart urban projects—high market share and high growth but capital-intensive; 2024 renewables revenue KRW 2.1T, hydrogen backlog $1.2B (Dec 31, 2024), recycling investment KRW 350–450B (through 2026), SMR market $150–220B (2040).

| Segment | 2024–25 metric |

|---|---|

| Renewables | KRW 2.1T revenue |

| Hydrogen | $1.2B backlog |

| Recycling | KRW 350–450B capex |

| SMR | $150–220B market |

What is included in the product

Comprehensive BCG Matrix for Hyundai Engineering: strategic guidance on Stars, Cash Cows, Question Marks, and Dogs with invest/hold/divest recommendations.

One-page overview placing each Hyundai Engineering business unit in a BCG quadrant for quick strategic clarity.

Cash Cows

Traditional Petrochemical Plant EPC

Traditional petrochemical plant EPC remains a cornerstone for Hyundai Engineering, holding a high market share in a mature global market; in 2024 the segment contributed roughly 40% of group revenue and delivered an EBITDA margin near 18%, per company reporting.

Growth is slow—global oil & gas CAPEX fell ~12% 2023–24—but margins stay high from decades of process optimization, producing steady cash flow that funded Hyundai Engineering’s 2024 R&D and renewables capex of about KRW 450 billion.

These projects require minimal new marketing spend to defend share; repeat orders and long-term client contracts kept backlog at KRW 7.2 trillion at end-2024, supporting investments in green hydrogen and digital tech.

Conventional Power Plant Construction

Hyundai Engineering leads in building thermal and combined-cycle power plants, holding roughly 18% share of South Korea’s EPC market and completing projects worth about $3.2 billion in 2024.

This mature segment shows low CAGR (<1% global to 2030) as renewables rise, yet operating margins stay near 8–12%, keeping it highly profitable.

Strong reliability and brand enable secure, high-value maintenance and upgrade contracts with minimal marketing, generating steady cash flow.

That cash is actively milked to service corporate debt—net debt fell 6% in 2024—and to fund dividends, supporting shareholder returns.

Domestic Residential Housing (Hillstate)

Hillstate dominates South Korea’s premium apartment segment with a 12–15% market share in 2024, giving Hyundai Engineering steady cash inflows despite a slow 2023–24 cycle.

High-end demand kept unit sell-through near 80% in 2024, producing strong liquidity and low per-unit marketing spend (about ₩4–5m vs. ₩30–40m sales price), so marketing ROI is high.

Completed-sale cashflows funded ~25% of capex in 2024, stabilizing group finances and underwriting riskier international growth projects.

Industrial Water Treatment Facilities

Industrial Water Treatment Facilities sit in Hyundai Engineering’s Cash Cows: high market share in a mature utility market delivering steady margins; global industrial water market grew to $160B in 2024 and utilities segment ≈2% CAGR, so growth is low but stable.

These projects yield long-term, predictable cash flows with low post‑commissioning capex; typical operating margins 12–18% and payback 5–8 years, creating capital for R&D elsewhere.

The technical specialization forms a durable moat—patented membranes, O&M expertise, and long service contracts protect margins and limit direct competition.

- High share, mature market (~2% CAGR)

- Market size ~$160B (2024)

- Margins 12–18%, payback 5–8 years

- Low ongoing capex, steady cash for R&D

- Patents + long O&M contracts = moat

Project Management Consultancy (PMC) Services

Hyundai Engineering’s Project Management Consultancy (PMC) is a cash cow: mature global market, >25% share in key client segments from 2018–2024, and long track record across 30+ countries.

PMC is asset-light, driven by intellectual capital, yielding operating margins often >20% in 2023–2024; low sector growth (~3% CAGR) but steady fees cover corporate admin.

Minimal CapEx and low support needs make PMC a reliable cash generator funding investments and dividends; backlog visibility of 12–18 months stabilizes cash flow.

- Mature market, >25% share (2018–2024)

- Asset-light, >20% operating margins (2023–24)

- Low growth ~3% CAGR

- Backlog 12–18 months; covers admin costs

Hyundai Engineering’s cash engines: Petrochemical, Power, Hillstate, Water, PMC drive 2024

Hyundai Engineering cash cows: petrochemical EPC, power EPC, Hillstate housing, water treatment, and PMC generated steady cash in 2024—~40% group revenue, EBITDA ~18% (petrochemical), backlog KRW 7.2T, net debt down 6%, Hillstate sell-through ~80%, water market $160B (2024), PMC margins >20%.

| Segment | 2024 key | Margin | Role |

|---|---|---|---|

| Petrochemical EPC | 40% rev; backlog KRW7.2T | ~18% EBITDA | Primary cash source |

| Power EPC | $3.2B projects; 18% KR market share | 8–12% | Stable cash |

| Hillstate | 12–15% market share; 80% sell-through | High liquidity | Recurring cash |

| Water | Market $160B (2024) | 12–18% | Long payback |

| PMC | >25% share; 12–18m backlog | >20% | Asset-light cash |

Delivered as Shown

Hyundai Engineering BCG Matrix

The file you're previewing here is the exact Hyundai Engineering BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document designed for strategic decision-making and stakeholder presentations.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Hyundai Engineering’s BCG Matrix preview highlights key business units navigating rapid industrial demand and capital-intensive projects, showing likely Stars in EPC segments and potential Question Marks in emerging green-tech ventures; Cash Cows appear in steady domestic infrastructure services while lower-margin legacy offerings risk becoming Dogs. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Renewable Energy EPC

As of late 2025, Hyundai Engineering leads global renewable EPC with >9 GW of awarded solar and wind capacity and revenue from the segment up 38% YoY to KRW 2.1 trillion in 2024, driven by decarbonization mandates and $45 billion estimated capital inflows into renewables in APAC 2023–25.

The sector shows high growth and Hyundai holds a high market share in utility-scale projects, winning multi-year EPC contracts worth KRW 1.4 trillion; continuous capex of ~KRW 300–400 billion annually is needed to fend off emerging global competitors.

Hydrogen Production Facilities

Hydrogen Production Facilities: Hyundai Engineering holds a leading share in blue and green hydrogen infrastructure, with ~18% of Korea’s recent project wins through 2024 and >$1.2bn backlog in hydrogen contracts as of Dec 31, 2024; fast market growth (CAGR ~15% to 2030) makes this a star with high market share and market growth.

These projects need heavy R&D and capex—Hyundai booked ~KRW 1.6tn (≈$1.2bn) capex commitments in 2023–24—so cash burn is high but revenues are large; ongoing investment is required to convert pilot assets into steady cash generators by 2028–2030.

Eco-friendly Plastic Recycling Plants

Hyundai Engineering leads chemical recycling—converting plastic waste to fuel/raw materials—with proprietary tech and commercial-scale plants, positioning it as a market leader in the circular economy.

Global chemical recycling demand is rising ~12–18% CAGR to 2030; tightened ESG rules for petrochemical clients drive rapid adoption, increasing addressable market to an estimated $15–20B by 2030.

Early projects and IP give Hyundai scale advantages, but sustaining a top position requires continued capex; company disclosed KRW 350–450B planned investment for recycling and decarbonization through 2026.

Small Modular Reactors (SMRs)

Hyundai Engineering positions SMRs as a star: global SMR market projected at $150–220 billion by 2040, and Hyundai holds reactors/technology partnerships covering projects in UAE, UK bids, and Korea R&D with estimated CAPEX per SMR $500–900 million—high growth and strategic scale justify heavy investment for carbon-free baseload leadership.

These capital-intensive projects demand continued R&D and global placement support; successful deployment could capture double-digit market share in exports and long-term service revenue, making SMRs a core star in Hyundai Engineering’s portfolio.

- Market size: $150–220B by 2040 (industry estimates, 2024–25)

- Hyundai: active partnerships in UAE, UK bids, Korea R&D

- Estimated CAPEX per SMR: $500–900M

- Outcome: high support needed for long-term export and service revenue

Sustainable Infrastructure in Emerging Markets

Hyundai Engineering leads high-growth urban development projects in Southeast Asia and the Middle East, focusing on smart-city integration and sustainable infrastructure, capturing an estimated 18–22% market share in landmark projects as of 2025 and contributing roughly $1.2–1.6 billion annual revenue from the segment.

These regions show >6% CAGR demand for green infrastructure through 2030, but intense competition and scale require continual reinvestment; maintaining leadership is pivotal for Hyundai’s long-term strategic growth.

- High market share: 18–22% (2025)

- Segment revenue: $1.2–1.6B annually

- Regional demand CAGR: >6% through 2030

- Risk: heavy reinvestment, competitive pressure

Hyundai Engineering: Renewable leader with big hydrogen, recycling & SMR upside

Stars: Hyundai Engineering dominates renewables, hydrogen, chemical recycling, SMRs, and smart urban projects—high market share and high growth but capital-intensive; 2024 renewables revenue KRW 2.1T, hydrogen backlog $1.2B (Dec 31, 2024), recycling investment KRW 350–450B (through 2026), SMR market $150–220B (2040).

| Segment | 2024–25 metric |

|---|---|

| Renewables | KRW 2.1T revenue |

| Hydrogen | $1.2B backlog |

| Recycling | KRW 350–450B capex |

| SMR | $150–220B market |

What is included in the product

Comprehensive BCG Matrix for Hyundai Engineering: strategic guidance on Stars, Cash Cows, Question Marks, and Dogs with invest/hold/divest recommendations.

One-page overview placing each Hyundai Engineering business unit in a BCG quadrant for quick strategic clarity.

Cash Cows

Traditional Petrochemical Plant EPC

Traditional petrochemical plant EPC remains a cornerstone for Hyundai Engineering, holding a high market share in a mature global market; in 2024 the segment contributed roughly 40% of group revenue and delivered an EBITDA margin near 18%, per company reporting.

Growth is slow—global oil & gas CAPEX fell ~12% 2023–24—but margins stay high from decades of process optimization, producing steady cash flow that funded Hyundai Engineering’s 2024 R&D and renewables capex of about KRW 450 billion.

These projects require minimal new marketing spend to defend share; repeat orders and long-term client contracts kept backlog at KRW 7.2 trillion at end-2024, supporting investments in green hydrogen and digital tech.

Conventional Power Plant Construction

Hyundai Engineering leads in building thermal and combined-cycle power plants, holding roughly 18% share of South Korea’s EPC market and completing projects worth about $3.2 billion in 2024.

This mature segment shows low CAGR (<1% global to 2030) as renewables rise, yet operating margins stay near 8–12%, keeping it highly profitable.

Strong reliability and brand enable secure, high-value maintenance and upgrade contracts with minimal marketing, generating steady cash flow.

That cash is actively milked to service corporate debt—net debt fell 6% in 2024—and to fund dividends, supporting shareholder returns.

Domestic Residential Housing (Hillstate)

Hillstate dominates South Korea’s premium apartment segment with a 12–15% market share in 2024, giving Hyundai Engineering steady cash inflows despite a slow 2023–24 cycle.

High-end demand kept unit sell-through near 80% in 2024, producing strong liquidity and low per-unit marketing spend (about ₩4–5m vs. ₩30–40m sales price), so marketing ROI is high.

Completed-sale cashflows funded ~25% of capex in 2024, stabilizing group finances and underwriting riskier international growth projects.

Industrial Water Treatment Facilities

Industrial Water Treatment Facilities sit in Hyundai Engineering’s Cash Cows: high market share in a mature utility market delivering steady margins; global industrial water market grew to $160B in 2024 and utilities segment ≈2% CAGR, so growth is low but stable.

These projects yield long-term, predictable cash flows with low post‑commissioning capex; typical operating margins 12–18% and payback 5–8 years, creating capital for R&D elsewhere.

The technical specialization forms a durable moat—patented membranes, O&M expertise, and long service contracts protect margins and limit direct competition.

- High share, mature market (~2% CAGR)

- Market size ~$160B (2024)

- Margins 12–18%, payback 5–8 years

- Low ongoing capex, steady cash for R&D

- Patents + long O&M contracts = moat

Project Management Consultancy (PMC) Services

Hyundai Engineering’s Project Management Consultancy (PMC) is a cash cow: mature global market, >25% share in key client segments from 2018–2024, and long track record across 30+ countries.

PMC is asset-light, driven by intellectual capital, yielding operating margins often >20% in 2023–2024; low sector growth (~3% CAGR) but steady fees cover corporate admin.

Minimal CapEx and low support needs make PMC a reliable cash generator funding investments and dividends; backlog visibility of 12–18 months stabilizes cash flow.

- Mature market, >25% share (2018–2024)

- Asset-light, >20% operating margins (2023–24)

- Low growth ~3% CAGR

- Backlog 12–18 months; covers admin costs

Hyundai Engineering’s cash engines: Petrochemical, Power, Hillstate, Water, PMC drive 2024

Hyundai Engineering cash cows: petrochemical EPC, power EPC, Hillstate housing, water treatment, and PMC generated steady cash in 2024—~40% group revenue, EBITDA ~18% (petrochemical), backlog KRW 7.2T, net debt down 6%, Hillstate sell-through ~80%, water market $160B (2024), PMC margins >20%.

| Segment | 2024 key | Margin | Role |

|---|---|---|---|

| Petrochemical EPC | 40% rev; backlog KRW7.2T | ~18% EBITDA | Primary cash source |

| Power EPC | $3.2B projects; 18% KR market share | 8–12% | Stable cash |

| Hillstate | 12–15% market share; 80% sell-through | High liquidity | Recurring cash |

| Water | Market $160B (2024) | 12–18% | Long payback |

| PMC | >25% share; 12–18m backlog | >20% | Asset-light cash |

Delivered as Shown

Hyundai Engineering BCG Matrix

The file you're previewing here is the exact Hyundai Engineering BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document designed for strategic decision-making and stakeholder presentations.