Hyundai Engineering PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how geopolitical shifts, regulatory changes, and rapid tech adoption are reshaping Hyundai Engineering’s prospects—our PESTLE distills the external forces that matter. Purchase the full analysis for a complete, actionable report that investors, strategists, and consultants can use immediately to inform decisions and mitigate risks.

Political factors

Geopolitical instability in key markets

Hyundai Engineering’s heavy exposure in the Middle East and Central Asia—regions accounting for roughly 35% of its 2024 international backlog—faces heightened risk from governance shifts and diplomatic tensions.

By late 2025, ongoing conflicts and realignments demand active monitoring as 18% of projects reported security incidents in 2023–24, threatening supply-chain continuity.

Political instability may trigger project delays, contract renegotiations, or asset freezes; a single major dispute in 2024 caused a client to suspend $420m in EPC work.

South Korean government export support

The South Korean government provided over $50 billion in export financing and guarantees in 2024 via KEXIM and K-SURE, enhancing Hyundai Engineering’s bid competitiveness; state-led diplomatic missions and 12 bilateral agreements in 2023–2025 helped secure projects across Southeast Asia and Eastern Europe, contributing to Hyundai Engineering’s 18% international revenue growth in 2024 and aiding wins in multi‑billion‑dollar infrastructure and energy contracts versus global rivals.

Trade protectionism and tariffs

By end-2025 rising protectionism saw global tariff actions increase 12% year-on-year, pressuring Hyundai Engineering as duties on steelsaverage 5–15% across major markets and tariffs on imported construction machinery up to 20%, elevating input costs.

Localized content rules now apply in 28% more host countries, forcing Hyundai Engineering to source more locally to maintain competitiveness and bid eligibility on EPC contracts.

Adopting a localized procurement strategy reduced exposure to tariffs and saved an estimated 3–6% on project costs in recent pilots, while ensuring compliance with complex, varying tariff regimes.

Energy security policies

National energy-independence policies boost demand for Hyundai Engineering’s petrochemical and power-plant services; government capital expenditure on energy grew 6.2% globally in 2024, with emerging markets allocating $320bn to energy infrastructure.

Policy-driven diversification is driving mandates for nuclear and renewables — global renewable capacity additions hit 520 GW in 2024 and nuclear new-build commitments reached $48bn.

Hyundai must realign project mix toward government-led nuclear and renewable contracts to access cyclical public funding and a projected $1.7tn of clean-energy investment through 2025–2026.

- Align portfolio to capture $1.7tn clean-energy spend

- Target renewables: 520 GW additions (2024)

- Pursue nuclear: $48bn new-build commitments (2024)

- Leverage $320bn emerging-market energy CAPEX (2024)

Regulatory shifts in international relations

Proactive diplomatic risk management is essential to preserve Hyundai Engineerings global footprint and prevent reputational losses that could impact contract awards and insurer underwriting.

- 12% revenue exposure to Middle East (2024)

- 28% of project debt as ESG-linked loans (2024)

- High diplomatic risk raises insurance and bidding costs

Middle East exposure fuels risk amid strong state support and $1.7T clean‑energy pipeline

Political risks — concentrated Middle East/Central Asia exposure (~35% intl backlog, 12% revenue tied to Middle East in 2024) — raise project disruption, sanctions and tariff costs (steel duties 5–15%, machinery up to 20%). State support (KEXIM/K-SURE >$50bn in 2024) and $320bn emerging-market energy CAPEX sustain bids; 28% of project debt was ESG‑linked in 2024, and clean‑energy spend pipeline ~$1.7tn through 2026.

| Metric | Value (2024) |

|---|---|

| Intl backlog exposure | 35% |

| Middle East revenue | 12% |

| KEXIM/K-SURE support | $50bn+ |

| ESG‑linked project debt | 28% |

What is included in the product

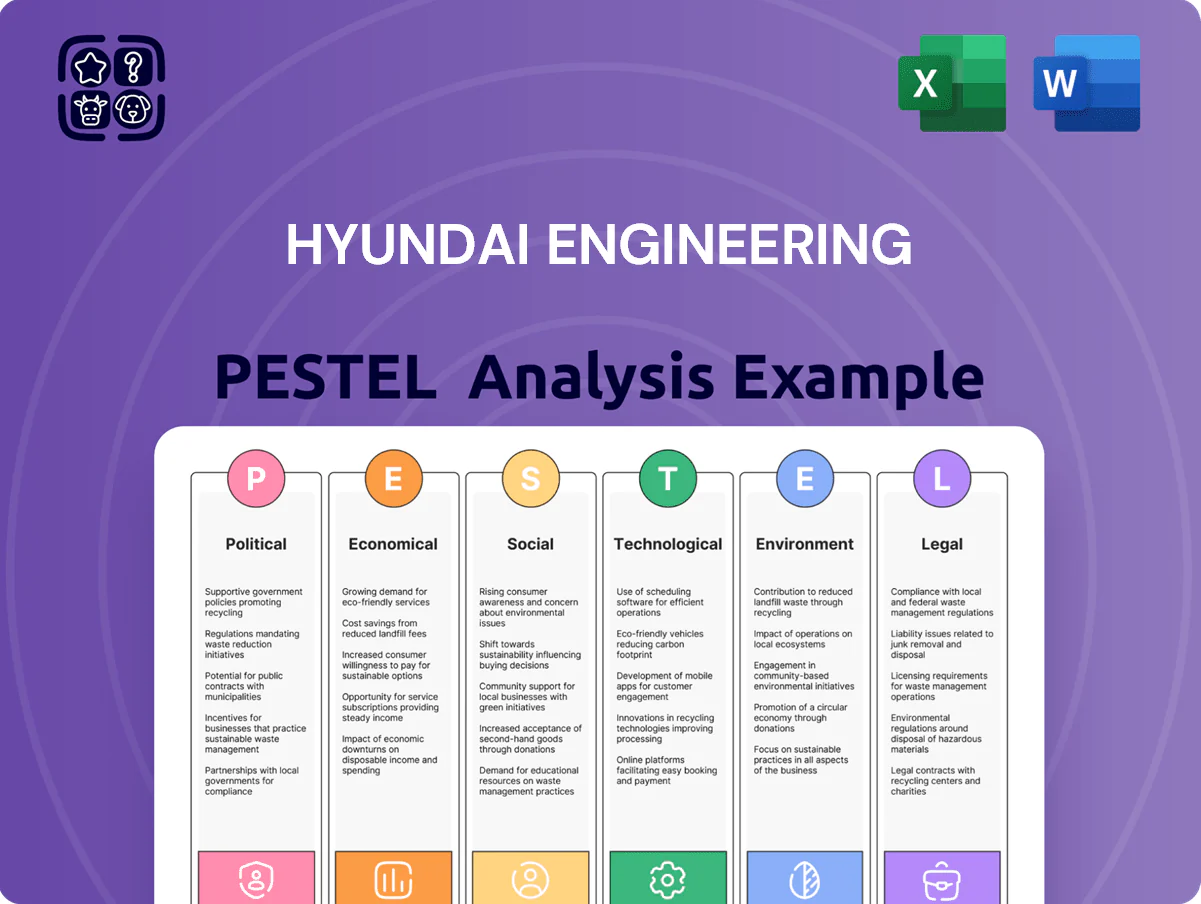

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces specifically impact Hyundai Engineering, with data-backed trends and regionally relevant examples to identify risks and opportunities for executives, consultants, and investors.

Condensed Hyundai Engineering PESTLE summary for quick reference in meetings or presentations, visually segmented by category for rapid interpretation and ready to drop into slides or strategy packs.

Economic factors

Global interest rate environment

By end-2025, global policy rates largely stabilized after the 2022–24 tightening cycle, with the IMF noting advanced-economy policy rates near 4.5% in 2024; for Hyundai Engineering this raises capital costs for large projects, as typical project finance spreads of 200–400 bps push all-in borrowing above 6–8%, deterring some private investment.

Currency exchange rate volatility

As a global EPC contractor, Hyundai Engineering faces KRW/USD volatility; KRW weakened ~5.2% vs USD in 2023 and traded near 1,350 KRW/USD in 2024, amplifying FX risk on US-dollar contracts and dollar-priced imports.

Rapid devaluations in emerging markets (e.g., TRY -44% 2021–24 cumulative vs USD) can erode margins on fixed-price projects and inflate local procurement costs.

Management must deploy dynamic hedging—forwards, options, and natural hedges—to contain FX losses; Hyundai Engineering reported FX losses impacting 2024 margins in segment disclosures.

Fluctuating commodity and material prices

The cost of steel, cement and copper remains volatile—steel HRC futures rose about 18% in 2024 while copper averaged near $9,000/t in 2024–2025—driven by supply disruptions and demand cycles. Economic shifts in major consumers like China, which accounted for roughly 55% of global steel demand in 2024, materially influence input pricing and project feasibility. Hyundai Engineering mitigates risk via long‑term supply agreements and price escalation clauses, which helped contain input cost exposure in FY2024 where raw material inflation pressured margins.

Investment trends in energy transition

Economic capital shifted sharply to green energy by 2025, with global clean energy investment reaching about USD 1.2 trillion in 2024 and projected to top USD 1.5 trillion in 2025; this reallocates opportunity toward hydrogen and carbon-capture projects where Hyundai Engineering can scale.

Hyundai Engineering should adapt its business model to capture flows—targeting hydrogen production and CCUS can drive long-term revenue growth given rising project finance and government subsidies in Korea and OECD markets.

- Global clean energy investment ~USD 1.2T (2024), ~USD 1.5T proj. (2025)

- Hydrogen market growth: investment pipeline >USD 200B by 2025

- CCUS projects expanding with ~$30–50B annual spend in 2024–25

- Business model pivot needed to capture project finance, subsidies, EPC contracts

Labor market dynamics and wage inflation

Hyundai Engineering faces rising labor costs and a global shortage of skilled technical staff, with construction wage growth averaging about 5–7% annually in key markets in 2024–2025, pressuring margins on fixed-price EPC contracts.

Wage inflation pushes the company to optimize human-resource allocation and accelerate automation; capital spending on digitalization/robotics in construction rose ~10–12% industry-wide in 2024.

Effective labor-cost management is critical to winning competitive bids and preserving project-level EBITDA, where every 1% rise in labor costs can cut margins materially on large projects.

- Construction wage growth: ~5–7% (2024–25)

- Industry digital/automation capex growth: ~10–12% (2024)

- 1% labor-cost increase significantly reduces project EBITDA on EPC contracts

Higher rates, FX pain and input shocks squeeze margins as clean‑energy capex shifts opportunity

Higher policy rates (advanced-econ. ~4.5% in 2024) push project borrowing >6–8%, raising capex hurdles; KRW~1,350/USD (2024) and EM devaluations (e.g., TRY -44% 2021–24) amplify FX risk and margin erosion; input costs volatile (HRC +18% 2024, copper ~$9,000/t) while clean‑energy flows (~USD1.2T 2024, ~1.5T proj. 2025) shift opportunity to hydrogen/CCUS; wage growth ~5–7% (2024–25) pressures margins.

| Metric | 2024/25 |

|---|---|

| Policy rate (adv. economies) | ~4.5% |

| KRW/USD (avg) | ~1,350 |

| Clean‑energy inv. | ~USD1.2T (2024), ~1.5T proj. (2025) |

| Steel HRC | +18% (2024) |

| Copper | ~USD9,000/t |

| Wage growth (construction) | ~5–7% |

What You See Is What You Get

Hyundai Engineering PESTLE Analysis

The preview shown here is the exact Hyundai Engineering PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how geopolitical shifts, regulatory changes, and rapid tech adoption are reshaping Hyundai Engineering’s prospects—our PESTLE distills the external forces that matter. Purchase the full analysis for a complete, actionable report that investors, strategists, and consultants can use immediately to inform decisions and mitigate risks.

Political factors

Geopolitical instability in key markets

Hyundai Engineering’s heavy exposure in the Middle East and Central Asia—regions accounting for roughly 35% of its 2024 international backlog—faces heightened risk from governance shifts and diplomatic tensions.

By late 2025, ongoing conflicts and realignments demand active monitoring as 18% of projects reported security incidents in 2023–24, threatening supply-chain continuity.

Political instability may trigger project delays, contract renegotiations, or asset freezes; a single major dispute in 2024 caused a client to suspend $420m in EPC work.

South Korean government export support

The South Korean government provided over $50 billion in export financing and guarantees in 2024 via KEXIM and K-SURE, enhancing Hyundai Engineering’s bid competitiveness; state-led diplomatic missions and 12 bilateral agreements in 2023–2025 helped secure projects across Southeast Asia and Eastern Europe, contributing to Hyundai Engineering’s 18% international revenue growth in 2024 and aiding wins in multi‑billion‑dollar infrastructure and energy contracts versus global rivals.

Trade protectionism and tariffs

By end-2025 rising protectionism saw global tariff actions increase 12% year-on-year, pressuring Hyundai Engineering as duties on steelsaverage 5–15% across major markets and tariffs on imported construction machinery up to 20%, elevating input costs.

Localized content rules now apply in 28% more host countries, forcing Hyundai Engineering to source more locally to maintain competitiveness and bid eligibility on EPC contracts.

Adopting a localized procurement strategy reduced exposure to tariffs and saved an estimated 3–6% on project costs in recent pilots, while ensuring compliance with complex, varying tariff regimes.

Energy security policies

National energy-independence policies boost demand for Hyundai Engineering’s petrochemical and power-plant services; government capital expenditure on energy grew 6.2% globally in 2024, with emerging markets allocating $320bn to energy infrastructure.

Policy-driven diversification is driving mandates for nuclear and renewables — global renewable capacity additions hit 520 GW in 2024 and nuclear new-build commitments reached $48bn.

Hyundai must realign project mix toward government-led nuclear and renewable contracts to access cyclical public funding and a projected $1.7tn of clean-energy investment through 2025–2026.

- Align portfolio to capture $1.7tn clean-energy spend

- Target renewables: 520 GW additions (2024)

- Pursue nuclear: $48bn new-build commitments (2024)

- Leverage $320bn emerging-market energy CAPEX (2024)

Regulatory shifts in international relations

Proactive diplomatic risk management is essential to preserve Hyundai Engineerings global footprint and prevent reputational losses that could impact contract awards and insurer underwriting.

- 12% revenue exposure to Middle East (2024)

- 28% of project debt as ESG-linked loans (2024)

- High diplomatic risk raises insurance and bidding costs

Middle East exposure fuels risk amid strong state support and $1.7T clean‑energy pipeline

Political risks — concentrated Middle East/Central Asia exposure (~35% intl backlog, 12% revenue tied to Middle East in 2024) — raise project disruption, sanctions and tariff costs (steel duties 5–15%, machinery up to 20%). State support (KEXIM/K-SURE >$50bn in 2024) and $320bn emerging-market energy CAPEX sustain bids; 28% of project debt was ESG‑linked in 2024, and clean‑energy spend pipeline ~$1.7tn through 2026.

| Metric | Value (2024) |

|---|---|

| Intl backlog exposure | 35% |

| Middle East revenue | 12% |

| KEXIM/K-SURE support | $50bn+ |

| ESG‑linked project debt | 28% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces specifically impact Hyundai Engineering, with data-backed trends and regionally relevant examples to identify risks and opportunities for executives, consultants, and investors.

Condensed Hyundai Engineering PESTLE summary for quick reference in meetings or presentations, visually segmented by category for rapid interpretation and ready to drop into slides or strategy packs.

Economic factors

Global interest rate environment

By end-2025, global policy rates largely stabilized after the 2022–24 tightening cycle, with the IMF noting advanced-economy policy rates near 4.5% in 2024; for Hyundai Engineering this raises capital costs for large projects, as typical project finance spreads of 200–400 bps push all-in borrowing above 6–8%, deterring some private investment.

Currency exchange rate volatility

As a global EPC contractor, Hyundai Engineering faces KRW/USD volatility; KRW weakened ~5.2% vs USD in 2023 and traded near 1,350 KRW/USD in 2024, amplifying FX risk on US-dollar contracts and dollar-priced imports.

Rapid devaluations in emerging markets (e.g., TRY -44% 2021–24 cumulative vs USD) can erode margins on fixed-price projects and inflate local procurement costs.

Management must deploy dynamic hedging—forwards, options, and natural hedges—to contain FX losses; Hyundai Engineering reported FX losses impacting 2024 margins in segment disclosures.

Fluctuating commodity and material prices

The cost of steel, cement and copper remains volatile—steel HRC futures rose about 18% in 2024 while copper averaged near $9,000/t in 2024–2025—driven by supply disruptions and demand cycles. Economic shifts in major consumers like China, which accounted for roughly 55% of global steel demand in 2024, materially influence input pricing and project feasibility. Hyundai Engineering mitigates risk via long‑term supply agreements and price escalation clauses, which helped contain input cost exposure in FY2024 where raw material inflation pressured margins.

Investment trends in energy transition

Economic capital shifted sharply to green energy by 2025, with global clean energy investment reaching about USD 1.2 trillion in 2024 and projected to top USD 1.5 trillion in 2025; this reallocates opportunity toward hydrogen and carbon-capture projects where Hyundai Engineering can scale.

Hyundai Engineering should adapt its business model to capture flows—targeting hydrogen production and CCUS can drive long-term revenue growth given rising project finance and government subsidies in Korea and OECD markets.

- Global clean energy investment ~USD 1.2T (2024), ~USD 1.5T proj. (2025)

- Hydrogen market growth: investment pipeline >USD 200B by 2025

- CCUS projects expanding with ~$30–50B annual spend in 2024–25

- Business model pivot needed to capture project finance, subsidies, EPC contracts

Labor market dynamics and wage inflation

Hyundai Engineering faces rising labor costs and a global shortage of skilled technical staff, with construction wage growth averaging about 5–7% annually in key markets in 2024–2025, pressuring margins on fixed-price EPC contracts.

Wage inflation pushes the company to optimize human-resource allocation and accelerate automation; capital spending on digitalization/robotics in construction rose ~10–12% industry-wide in 2024.

Effective labor-cost management is critical to winning competitive bids and preserving project-level EBITDA, where every 1% rise in labor costs can cut margins materially on large projects.

- Construction wage growth: ~5–7% (2024–25)

- Industry digital/automation capex growth: ~10–12% (2024)

- 1% labor-cost increase significantly reduces project EBITDA on EPC contracts

Higher rates, FX pain and input shocks squeeze margins as clean‑energy capex shifts opportunity

Higher policy rates (advanced-econ. ~4.5% in 2024) push project borrowing >6–8%, raising capex hurdles; KRW~1,350/USD (2024) and EM devaluations (e.g., TRY -44% 2021–24) amplify FX risk and margin erosion; input costs volatile (HRC +18% 2024, copper ~$9,000/t) while clean‑energy flows (~USD1.2T 2024, ~1.5T proj. 2025) shift opportunity to hydrogen/CCUS; wage growth ~5–7% (2024–25) pressures margins.

| Metric | 2024/25 |

|---|---|

| Policy rate (adv. economies) | ~4.5% |

| KRW/USD (avg) | ~1,350 |

| Clean‑energy inv. | ~USD1.2T (2024), ~1.5T proj. (2025) |

| Steel HRC | +18% (2024) |

| Copper | ~USD9,000/t |

| Wage growth (construction) | ~5–7% |

What You See Is What You Get

Hyundai Engineering PESTLE Analysis

The preview shown here is the exact Hyundai Engineering PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.