HDFC Bank Business Model Canvas

HDFC Bank Business Model Canvas: Strategy, Value, Partnerships, and Revenue

Unlock the full strategic blueprint behind HDFC Bank’s business model—this concise Business Model Canvas reveals how the bank creates customer value, leverages partnerships, and monetizes services across retail and corporate segments.

Partnerships

Strategic Fintech Collaborations

HDFC Bank partners with fintech startups like Razorpay and Pine Labs to expand its digital ecosystem and scale payment solutions, supporting over 200 million merchant transactions in FY2024; these alliances enable AI-driven underwriting models that cut loan decision times by ~40% and boost approval rates. By end-2025, such collaborations are central to retaining market share in India’s digital payments market, projected to reach $1.3 trillion in GMV.

Insurance and Investment Product Providers

HDFC Bank partners with HDFC Life and HDFC ERGO to distribute insurance, earning commission income—insurance distribution contributed about ₹5,200 crore in fee income across bancassurance channels in FY2024, with HDFC Bank a top distributor.

The bank also ties with mutual fund houses to sell wealth products; as of Dec 2024, third-party product distribution drove over ₹3,000 crore in AUM-linked fees and expanded customer share in retail AUM by ~18% year-on-year.

Global Payment Networks

HDFC Bank partners with Visa, Mastercard, and RuPay to power over 150 million debit and credit cards (FY2024 end), using their global processing, tokenization, and fraud controls to enable secure cross‑border payments and NPCI-RuPay national rails. The bank issues co-branded cards and segment-specific rewards—over 12 million premium cards with exclusive benefits—driving higher spends and interchange revenue.

Business Correspondents and Rural Partners

HDFC Bank uses ~150,000 business correspondents and partnerships with local agri-cooperatives to extend basic banking to semi-urban and rural India, boosting branchless transactions and supporting a rural loan book that grew ~12% YoY to ₹1.2 trillion in FY2024-25.

- ~150,000 business correspondents deployed

- Rural loans ~₹1.2 trillion (FY2024-25), +12% YoY

- Focus: cash-in/cash-out, small credit, account opening

Corporate and Institutional Alliances

HDFC Bank partners with large corporates for payroll, supply-chain finance, and institutional banking, securing low-cost salary deposits—salary account deposits were ~INR 1.9 trillion in FY2024—while driving high-volume transactions and fee income.

These alliances also generate long-term advisory and investment-banking mandates; corporate-linked loan book and transaction banking helped HDFC Bank report ~15% of non-interest income in FY2024.

- Payroll: stable low-cost CASA flow (~INR 1.9T FY2024)

- Supply-chain: working-capital fees, lower NPL risk

- Institutional banking: high-volume processing, cross-sell

- Advisory/IB: multi-year mandates, recurring fee streams

HDFC Bank's partnership engine: fintechs, insurers & 150k BCs powering ₹1.9T payroll

HDFC Bank leverages fintechs (Razorpay, Pine Labs), insurers (HDFC Life, ERGO), card networks (Visa, Mastercard, RuPay), mutual funds, corporates, and ~150,000 business correspondents to drive digital payments, bancassurance, wealth distribution, payroll deposits (~₹1.9T FY2024), rural loans (~₹1.2T FY2024-25) and non-interest income (~15% FY2024).

| Partnership | Key metric |

|---|---|

| Fintechs | 200M txn FY2024 |

| Cards | 150M cards FY2024 |

| Bancassurance | ₹5,200cr fees FY2024 |

| Rural BCs | ~150,000 BCs |

What is included in the product

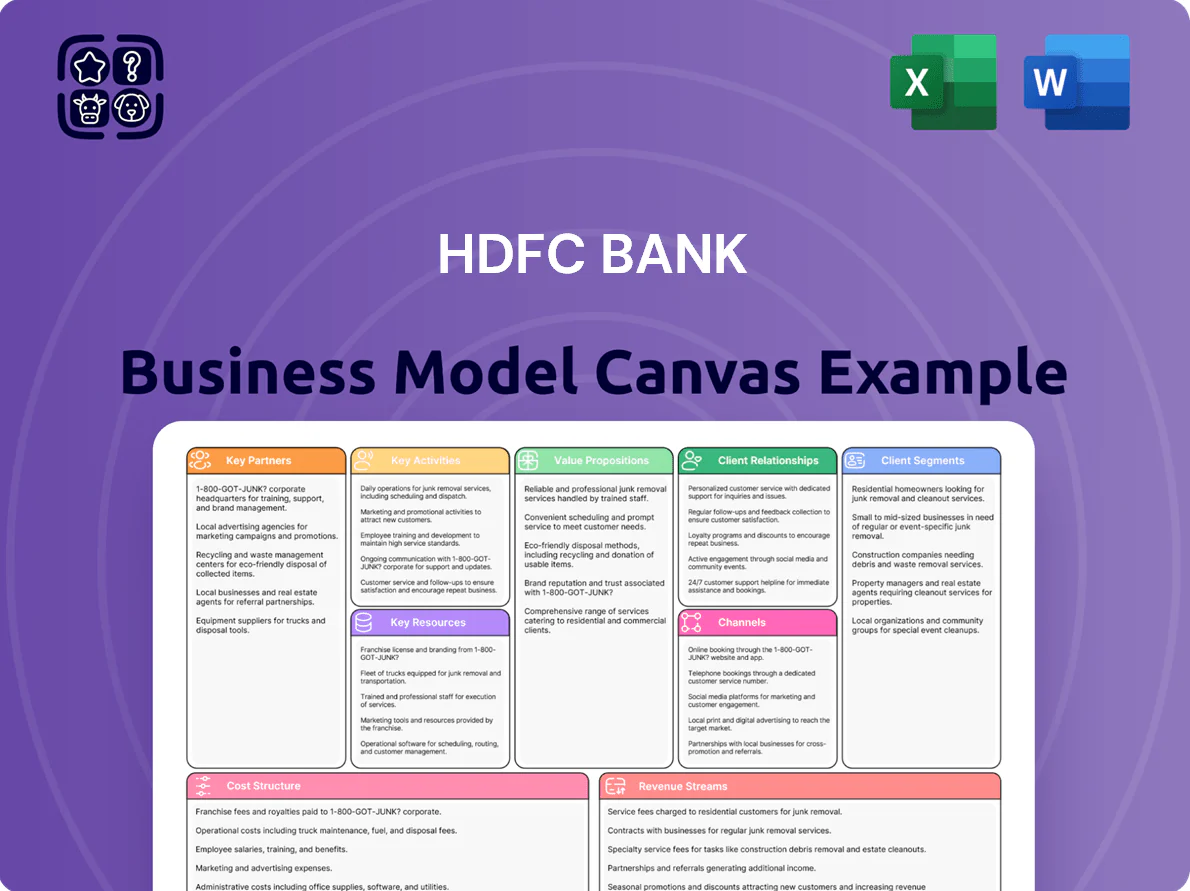

A concise, pre-written Business Model Canvas for HDFC Bank that maps its nine core blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure—reflecting real-world retail and corporate banking operations and strategic priorities.

High-level view of HDFC Bank’s business model with editable cells to quickly pinpoint how the bank alleviates customer pain points—streamlining lending, digital banking, and customer service—into a one-page, board-ready snapshot.

Activities

Credit and Loan Lifecycle Management

Credit and Loan Lifecycle Management covers end-to-end credit appraisal, disbursement, and monitoring across retail and corporate portfolios; by FY2025 HDFC Bank reported a GNPA ratio of ~0.34% (Q3 2025) and used AI-driven analytics and credit-scoring models to cut approval times by ~30% and reduce new NPA incidence by ~18% year-on-year. Efficient asset management sustained ROA near 1.6% in 2025, supporting long-term profitability and capital stability.

Digital Banking and Tech Innovation

HDFC Bank continuously develops its mobile app and netbanking—over 70% of retail transactions were digital in FY2024 (March 2024), driving a focus on frictionless UX and a 15% YoY uplift in active mobile users. The bank spends materially on automation and cybersecurity, with tech and digital investments of ~INR 3,200 crore in FY2024, to protect customer data and win younger, tech‑savvy and professional clients.

Risk Management and Regulatory Compliance

HDFC Bank must follow Reserve Bank of India rules while managing market, credit, and operational risks, keeping CET1 ratio and overall CRAR above RBI-mandated buffers—CRAR was 18.5% as of Dec 31, 2025—while running continuous capital adequacy monitoring and stress tests.

The bank runs robust internal audit and risk controls, with governance metrics, board risk committees, and compliance frameworks to protect investor trust and avoid penalties—RBI fines to banks totaled ~₹1,200 crore in FY2024, underscoring enforcement risk.

Customer Acquisition and Relationship Management

HDFC Bank drives customer acquisition through aggressive marketing and targeted sales campaigns, adding 6.9 million CASA (current and savings account) customers in FY2024 and raising retail deposits by 18% year-on-year; relationship managers then deepen engagement by cross-selling insurance, mutual funds, and loans to boost share-of-wallet. The bank focuses on increasing customer lifetime value via tailored wealth-management and lending solutions, with branch-led RM networks supporting a retail loan book of INR 6.2 trillion as of Mar 31, 2025.

- 6.9M new CASA customers FY2024

- Retail deposits +18% YoY

- Retail loan book INR 6.2T (Mar 31, 2025)

- Cross-sell: insurance, mutual funds, wealth mgmt

Treasury and Investment Operations

The treasury actively trades government securities and FX to meet liquidity and statutory reserve ratios; as of FY2024 (year ended Mar 31, 2024) HDFC Bank reported a liquidity coverage ratio around 121% and held government securities and treasury bills totaling ~₹3.2 lakh crore, helping keep funding costs near 6.5% and supporting NII and margins.

These operations optimize cost of funds and returns on idle capital, contributing to core fee and treasury profits that helped the bank deliver a FY2024 PAT of ₹54,819 crore and a net interest margin of 4.5%.

- Liquidity coverage ~121% (FY2024)

- Govt securities/t-bills ~₹3.2 lakh crore (FY2024)

- Funding cost ~6.5% (approx.)

- Net interest margin 4.5% (FY2024)

- PAT ₹54,819 crore (FY2024)

Strong credit metrics, digital scale & liquidity—0.34% GNPA, 70%+ digital, CRAR 18.5%

Key activities: end-to-end credit & loan management (GNPA ~0.34% Q3 2025), digital banking scale (70%+ digital transactions FY2024; tech spend ~₹3,200 cr FY2024), risk & compliance (CRAR 18.5% Dec 31, 2025), treasury liquidity (LCR ~121% FY2024; govt securities ~₹3.2 lakh cr), customer growth (6.9M new CASA FY2024; retail loans ₹6.2T Mar 31, 2025).

| Metric | Value |

|---|---|

| GNPA (Q3 2025) | 0.34% |

| Digital txn share (FY2024) | 70%+ |

| Tech spend (FY2024) | ₹3,200 cr |

| CRAR (Dec 31, 2025) | 18.5% |

| LCR (FY2024) | 121% |

| Govt sec (FY2024) | ₹3.2 lakh cr |

| New CASA (FY2024) | 6.9M |

| Retail loan book (Mar 31, 2025) | ₹6.2T |

Delivered as Displayed

Business Model Canvas

The preview shown is the actual HDFC Bank Business Model Canvas you’ll receive upon purchase—not a mockup or sample.

When you complete your order, you’ll get this same professional, ready-to-use document in full, editable formats with all content and pages included.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

HDFC Bank Business Model Canvas: Strategy, Value, Partnerships, and Revenue

Unlock the full strategic blueprint behind HDFC Bank’s business model—this concise Business Model Canvas reveals how the bank creates customer value, leverages partnerships, and monetizes services across retail and corporate segments.

Partnerships

Strategic Fintech Collaborations

HDFC Bank partners with fintech startups like Razorpay and Pine Labs to expand its digital ecosystem and scale payment solutions, supporting over 200 million merchant transactions in FY2024; these alliances enable AI-driven underwriting models that cut loan decision times by ~40% and boost approval rates. By end-2025, such collaborations are central to retaining market share in India’s digital payments market, projected to reach $1.3 trillion in GMV.

Insurance and Investment Product Providers

HDFC Bank partners with HDFC Life and HDFC ERGO to distribute insurance, earning commission income—insurance distribution contributed about ₹5,200 crore in fee income across bancassurance channels in FY2024, with HDFC Bank a top distributor.

The bank also ties with mutual fund houses to sell wealth products; as of Dec 2024, third-party product distribution drove over ₹3,000 crore in AUM-linked fees and expanded customer share in retail AUM by ~18% year-on-year.

Global Payment Networks

HDFC Bank partners with Visa, Mastercard, and RuPay to power over 150 million debit and credit cards (FY2024 end), using their global processing, tokenization, and fraud controls to enable secure cross‑border payments and NPCI-RuPay national rails. The bank issues co-branded cards and segment-specific rewards—over 12 million premium cards with exclusive benefits—driving higher spends and interchange revenue.

Business Correspondents and Rural Partners

HDFC Bank uses ~150,000 business correspondents and partnerships with local agri-cooperatives to extend basic banking to semi-urban and rural India, boosting branchless transactions and supporting a rural loan book that grew ~12% YoY to ₹1.2 trillion in FY2024-25.

- ~150,000 business correspondents deployed

- Rural loans ~₹1.2 trillion (FY2024-25), +12% YoY

- Focus: cash-in/cash-out, small credit, account opening

Corporate and Institutional Alliances

HDFC Bank partners with large corporates for payroll, supply-chain finance, and institutional banking, securing low-cost salary deposits—salary account deposits were ~INR 1.9 trillion in FY2024—while driving high-volume transactions and fee income.

These alliances also generate long-term advisory and investment-banking mandates; corporate-linked loan book and transaction banking helped HDFC Bank report ~15% of non-interest income in FY2024.

- Payroll: stable low-cost CASA flow (~INR 1.9T FY2024)

- Supply-chain: working-capital fees, lower NPL risk

- Institutional banking: high-volume processing, cross-sell

- Advisory/IB: multi-year mandates, recurring fee streams

HDFC Bank's partnership engine: fintechs, insurers & 150k BCs powering ₹1.9T payroll

HDFC Bank leverages fintechs (Razorpay, Pine Labs), insurers (HDFC Life, ERGO), card networks (Visa, Mastercard, RuPay), mutual funds, corporates, and ~150,000 business correspondents to drive digital payments, bancassurance, wealth distribution, payroll deposits (~₹1.9T FY2024), rural loans (~₹1.2T FY2024-25) and non-interest income (~15% FY2024).

| Partnership | Key metric |

|---|---|

| Fintechs | 200M txn FY2024 |

| Cards | 150M cards FY2024 |

| Bancassurance | ₹5,200cr fees FY2024 |

| Rural BCs | ~150,000 BCs |

What is included in the product

A concise, pre-written Business Model Canvas for HDFC Bank that maps its nine core blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure—reflecting real-world retail and corporate banking operations and strategic priorities.

High-level view of HDFC Bank’s business model with editable cells to quickly pinpoint how the bank alleviates customer pain points—streamlining lending, digital banking, and customer service—into a one-page, board-ready snapshot.

Activities

Credit and Loan Lifecycle Management

Credit and Loan Lifecycle Management covers end-to-end credit appraisal, disbursement, and monitoring across retail and corporate portfolios; by FY2025 HDFC Bank reported a GNPA ratio of ~0.34% (Q3 2025) and used AI-driven analytics and credit-scoring models to cut approval times by ~30% and reduce new NPA incidence by ~18% year-on-year. Efficient asset management sustained ROA near 1.6% in 2025, supporting long-term profitability and capital stability.

Digital Banking and Tech Innovation

HDFC Bank continuously develops its mobile app and netbanking—over 70% of retail transactions were digital in FY2024 (March 2024), driving a focus on frictionless UX and a 15% YoY uplift in active mobile users. The bank spends materially on automation and cybersecurity, with tech and digital investments of ~INR 3,200 crore in FY2024, to protect customer data and win younger, tech‑savvy and professional clients.

Risk Management and Regulatory Compliance

HDFC Bank must follow Reserve Bank of India rules while managing market, credit, and operational risks, keeping CET1 ratio and overall CRAR above RBI-mandated buffers—CRAR was 18.5% as of Dec 31, 2025—while running continuous capital adequacy monitoring and stress tests.

The bank runs robust internal audit and risk controls, with governance metrics, board risk committees, and compliance frameworks to protect investor trust and avoid penalties—RBI fines to banks totaled ~₹1,200 crore in FY2024, underscoring enforcement risk.

Customer Acquisition and Relationship Management

HDFC Bank drives customer acquisition through aggressive marketing and targeted sales campaigns, adding 6.9 million CASA (current and savings account) customers in FY2024 and raising retail deposits by 18% year-on-year; relationship managers then deepen engagement by cross-selling insurance, mutual funds, and loans to boost share-of-wallet. The bank focuses on increasing customer lifetime value via tailored wealth-management and lending solutions, with branch-led RM networks supporting a retail loan book of INR 6.2 trillion as of Mar 31, 2025.

- 6.9M new CASA customers FY2024

- Retail deposits +18% YoY

- Retail loan book INR 6.2T (Mar 31, 2025)

- Cross-sell: insurance, mutual funds, wealth mgmt

Treasury and Investment Operations

The treasury actively trades government securities and FX to meet liquidity and statutory reserve ratios; as of FY2024 (year ended Mar 31, 2024) HDFC Bank reported a liquidity coverage ratio around 121% and held government securities and treasury bills totaling ~₹3.2 lakh crore, helping keep funding costs near 6.5% and supporting NII and margins.

These operations optimize cost of funds and returns on idle capital, contributing to core fee and treasury profits that helped the bank deliver a FY2024 PAT of ₹54,819 crore and a net interest margin of 4.5%.

- Liquidity coverage ~121% (FY2024)

- Govt securities/t-bills ~₹3.2 lakh crore (FY2024)

- Funding cost ~6.5% (approx.)

- Net interest margin 4.5% (FY2024)

- PAT ₹54,819 crore (FY2024)

Strong credit metrics, digital scale & liquidity—0.34% GNPA, 70%+ digital, CRAR 18.5%

Key activities: end-to-end credit & loan management (GNPA ~0.34% Q3 2025), digital banking scale (70%+ digital transactions FY2024; tech spend ~₹3,200 cr FY2024), risk & compliance (CRAR 18.5% Dec 31, 2025), treasury liquidity (LCR ~121% FY2024; govt securities ~₹3.2 lakh cr), customer growth (6.9M new CASA FY2024; retail loans ₹6.2T Mar 31, 2025).

| Metric | Value |

|---|---|

| GNPA (Q3 2025) | 0.34% |

| Digital txn share (FY2024) | 70%+ |

| Tech spend (FY2024) | ₹3,200 cr |

| CRAR (Dec 31, 2025) | 18.5% |

| LCR (FY2024) | 121% |

| Govt sec (FY2024) | ₹3.2 lakh cr |

| New CASA (FY2024) | 6.9M |

| Retail loan book (Mar 31, 2025) | ₹6.2T |

Delivered as Displayed

Business Model Canvas

The preview shown is the actual HDFC Bank Business Model Canvas you’ll receive upon purchase—not a mockup or sample.

When you complete your order, you’ll get this same professional, ready-to-use document in full, editable formats with all content and pages included.