HDFC Bank PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Navigate HDFC Bank’s external landscape with our concise PESTLE snapshot—highlighting regulatory shifts, macroeconomic pressures, tech disruption, and social trends that will shape future performance; buy the full PESTLE to unlock detailed risks, opportunities, and strategic actions you can apply immediately.

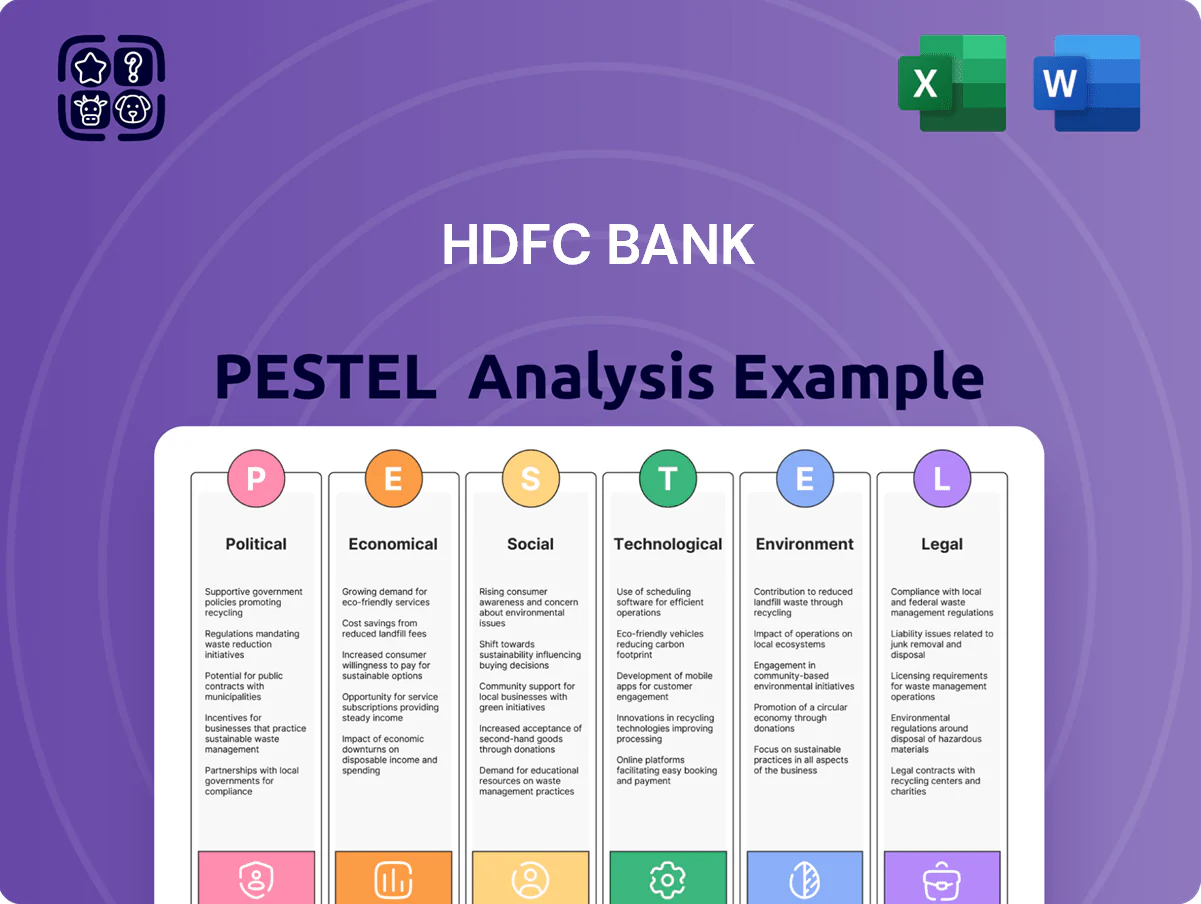

Political factors

Government Stability and Policy Continuity

The continued political stability in India through 2025 has created a predictable operating environment for HDFC Bank; GDP growth held near 7.2% in FY2024 and government capex rose to about INR 11.2 trillion, supporting credit demand.

Regulatory Oversight by RBI

The Reserve Bank of India maintains stringent oversight to ensure systemic stability, especially after the 2023 HDFC-HDFC Bank merger that expanded consolidated assets to about ₹22.5 trillion by FY2024; RBI scrutiny tightened on integration risks and capital adequacy. Political pressure to keep CPI inflation near the 4% target while supporting 6–7% growth shapes RBI rate moves, affecting HDFC Bank’s lending rates and margins. HDFC Bank must meet RBI-mandated liquidity coverage ratio (LCR) norms—LCR remained above 100% for scheduled banks in 2024—and adhere to priority sector lending targets (40% overall, 18% agriculture), constraining asset allocation and capital deployment.

Digital India Initiatives

The government’s cashless push and expansion of digital public infrastructure—UPI transactions reached 86.4 billion in 2024 with value of Rs 162 trillion—provide a strong tailwind for HDFC Bank; UPI adoption and e-KYC lower customer acquisition costs and boost fee-free transaction volumes. HDFC Bank’s digital-led strategy, which contributed to a 24% YoY rise in digital CASA in FY2024, aligns with national goals to capture incremental market share.

Geopolitical Trade Relations

India’s evolving trade ties with the US, EU and UAE shape HDFC Bank’s wholesale banking and remittance volumes; FY2024-25 merchandise exports were about USD 770bn, influencing trade finance demand.

Political tensions or trade pacts affect FDI flows—India attracted USD 59.9bn FDI in FY2023-24—which alters corporate lending exposure in sectors HDFC funds.

HDFC Bank tracks these shifts to hedge international trade finance risks and manage volatility from FX swings and global supply-chain disruptions.

- Exports USD 770bn (FY2024-25) drive trade finance

- FDI USD 59.9bn (FY2023-24) impacts corporate lending

- Active monitoring for FX and supply-chain risk mitigation

Rural Development Mandates

Political focus on financial inclusion and the goal to double farmers’ incomes by 2025 drives HDFC Bank’s rural expansion; rural and semi-urban branches rose to over 5,200 outlets by FY2024, supporting agri credit growth of 18% YoY.

Government schemes like PM-KISAN and crop insurance require deep on-ground presence, prompting the bank to scale rural BC networks (over 120,000 agents in 2024) to distribute credit and insurance.

Aligning with these mandates is vital for regulatory goodwill and public trust, influencing license approvals and priority sector lending compliance.

- 5,200+ rural/semi-urban branches (FY2024)

- Agri credit growth ~18% YoY (FY2024)

- 120,000+ banking correspondents (2024)

HDFC Bank: RBI-backed scale, digital low-cost growth, rural push amid strong GDP & trade

Political stability and pro-growth fiscal policy (GDP ~7.2% FY2024) and RBI oversight post-merger (consolidated assets ~₹22.5tn FY2024) shape HDFC Bank’s lending, LCR and PSL compliance; digital public infrastructure (UPI 86.4bn txns 2024) aids low-cost acquisition; exports USD 770bn and FDI USD 59.9bn affect trade finance and FX risk; rural push (5,200+ rural branches, 120k BCs, agri credit +18% YoY) drives priority lending.

| Metric | Value |

|---|---|

| GDP FY2024 | ~7.2% |

| Consolidated assets | ₹22.5tn |

| UPI txns 2024 | 86.4bn |

| Exports FY2024-25 | USD 770bn |

| FDI FY2023-24 | USD 59.9bn |

| Rural branches | 5,200+ |

| Banking correspondents | 120,000+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect HDFC Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and investor communications.

A concise, visually segmented PESTLE summary of HDFC Bank that can be dropped into presentations or shared across teams to quickly align on external risks, regulatory shifts, and market positioning during planning sessions.

Economic factors

GDP Growth and Credit Demand

As India remained one of the fastest-growing major economies in 2025 with IMF-estimated GDP growth of about 6.8%, HDFC Bank reported stronger credit demand, noting retail and corporate loan growth of ~14% YoY in FY2025.

Robust expansion in manufacturing and services—industry GVA rising ~7% and services GVA ~6.5% in 2024–25—boosted working capital and term-loan requests, lifting corporate loan disbursals.

HDFC Bank’s asset quality and net interest income are tightly linked to macro health; with industrial output (IIP) up ~5% in 2025, credit uptake and margins showed positive correlation.

Interest Rate Environment

The MPC-driven repo rate at 6.50% (Dec 2025) directly compresses or expands HDFC Bank's NIM, which stood at 4.00% in FY2024; rate hikes raise funding costs, squeezing margins unless lending yields adjust.

In a volatile rate cycle, the bank must price deposits—CASA ratio 45.6% in FY2024—against advance yields to preserve profitability; mismatches erode net interest income.

Robust asset-liability management, including duration matching and liquidity coverage (LCR ~132% in 2024), is vital to mitigate interest-rate and tightening-liquidity risks.

Inflationary Pressures

Persisting inflation in India—CPI at 5.1% in Dec 2025 vs RBI target band—erodes retail disposable income, risking higher delinquencies and lower savings, pressuring HDFC Bank’s retail loan collections; the bank reported GNPA 0.69% in FY2025, reflecting resilient asset quality so far. Rising inflation raises operating costs, with employee expenses up 11% YoY in FY2025. HDFC Bank leverages analytics—credit models and dynamic pricing—to tighten underwriting and adjust loan yields amid inflationary trends.

Currency Fluctuations

Volatility in the INR/USD rate affects HDFC Bank’s treasury and corporate clients; in 2024 the rupee moved ~7% vs the dollar, increasing hedging demand and trading volumes.

HDFC Bank offers forwards, options and swaps, generating fee income—treasury fee income grew 5% YoY in FY2024—while exposure to sharp swings raises balance-sheet risk.

Significant depreciation raises costs for imported IT systems and increases burden on borrowers with foreign-currency debt, amplifying credit-risk pressures.

- INR moved ~7% vs USD in 2024

- Treasury/FX fee income +5% YoY FY2024

- Depreciation ups imported IT and FX-denominated debt costs

Capital Market Performance

The performance of Indian equity and debt markets directly affects HDFC Bank’s wealth management and investment banking, with FY2024 equity market cap rising ~18% YoY boosting AUM across HDFC Mutual Fund-linked channels.

Bull runs increased brokerage and transaction fees—NSE turnover averaged ~Rs 1.2 lakh crore/day in 2024 vs ~Rs 0.9 lakh crore/day in 2023—lifting retail activity and HDFC Securities revenues.

Market downturns compress AUM and fees; a 2022-23 correction saw industry-wide brokerage volumes drop ~25%, highlighting sensitivity of fee income to market cycles.

- Equity market cap +18% YoY (2024)

- NSE avg turnover ~Rs 1.2 lakh crore/day (2024)

- Brokerage volumes fell ~25% in 2022-23 correction

HDFC Bank: 14% Loan Growth, Strong CASA & GNPA 0.69% amid 6.8% GDP

India GDP ~6.8% (2025) boosted HDFC Bank loans (~14% YoY FY2025); IIP +5% (2025) aided credit demand. Repo 6.50% (Dec 2025) pressures NIM (4.00% FY2024); CASA 45.6% (FY2024) and LCR ~132% (2024) guide ALM. CPI 5.1% (Dec 2025) risks delinquencies; GNPA 0.69% (FY2025). INR moved ~7% vs USD (2024); treasury fees +5% YoY (FY2024).

| Metric | Value |

|---|---|

| GDP (2025) | 6.8% |

| Loan growth FY2025 | ~14% YoY |

| Repo (Dec 2025) | 6.50% |

| NIM FY2024 | 4.00% |

| GNPA FY2025 | 0.69% |

What You See Is What You Get

HDFC Bank PESTLE Analysis

The preview shown here is the exact HDFC Bank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. The file you see is the final version and will be available for instant download after payment. The layout, content, and structure match the product delivered, ensuring you get the complete, actionable analysis as displayed.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Navigate HDFC Bank’s external landscape with our concise PESTLE snapshot—highlighting regulatory shifts, macroeconomic pressures, tech disruption, and social trends that will shape future performance; buy the full PESTLE to unlock detailed risks, opportunities, and strategic actions you can apply immediately.

Political factors

Government Stability and Policy Continuity

The continued political stability in India through 2025 has created a predictable operating environment for HDFC Bank; GDP growth held near 7.2% in FY2024 and government capex rose to about INR 11.2 trillion, supporting credit demand.

Regulatory Oversight by RBI

The Reserve Bank of India maintains stringent oversight to ensure systemic stability, especially after the 2023 HDFC-HDFC Bank merger that expanded consolidated assets to about ₹22.5 trillion by FY2024; RBI scrutiny tightened on integration risks and capital adequacy. Political pressure to keep CPI inflation near the 4% target while supporting 6–7% growth shapes RBI rate moves, affecting HDFC Bank’s lending rates and margins. HDFC Bank must meet RBI-mandated liquidity coverage ratio (LCR) norms—LCR remained above 100% for scheduled banks in 2024—and adhere to priority sector lending targets (40% overall, 18% agriculture), constraining asset allocation and capital deployment.

Digital India Initiatives

The government’s cashless push and expansion of digital public infrastructure—UPI transactions reached 86.4 billion in 2024 with value of Rs 162 trillion—provide a strong tailwind for HDFC Bank; UPI adoption and e-KYC lower customer acquisition costs and boost fee-free transaction volumes. HDFC Bank’s digital-led strategy, which contributed to a 24% YoY rise in digital CASA in FY2024, aligns with national goals to capture incremental market share.

Geopolitical Trade Relations

India’s evolving trade ties with the US, EU and UAE shape HDFC Bank’s wholesale banking and remittance volumes; FY2024-25 merchandise exports were about USD 770bn, influencing trade finance demand.

Political tensions or trade pacts affect FDI flows—India attracted USD 59.9bn FDI in FY2023-24—which alters corporate lending exposure in sectors HDFC funds.

HDFC Bank tracks these shifts to hedge international trade finance risks and manage volatility from FX swings and global supply-chain disruptions.

- Exports USD 770bn (FY2024-25) drive trade finance

- FDI USD 59.9bn (FY2023-24) impacts corporate lending

- Active monitoring for FX and supply-chain risk mitigation

Rural Development Mandates

Political focus on financial inclusion and the goal to double farmers’ incomes by 2025 drives HDFC Bank’s rural expansion; rural and semi-urban branches rose to over 5,200 outlets by FY2024, supporting agri credit growth of 18% YoY.

Government schemes like PM-KISAN and crop insurance require deep on-ground presence, prompting the bank to scale rural BC networks (over 120,000 agents in 2024) to distribute credit and insurance.

Aligning with these mandates is vital for regulatory goodwill and public trust, influencing license approvals and priority sector lending compliance.

- 5,200+ rural/semi-urban branches (FY2024)

- Agri credit growth ~18% YoY (FY2024)

- 120,000+ banking correspondents (2024)

HDFC Bank: RBI-backed scale, digital low-cost growth, rural push amid strong GDP & trade

Political stability and pro-growth fiscal policy (GDP ~7.2% FY2024) and RBI oversight post-merger (consolidated assets ~₹22.5tn FY2024) shape HDFC Bank’s lending, LCR and PSL compliance; digital public infrastructure (UPI 86.4bn txns 2024) aids low-cost acquisition; exports USD 770bn and FDI USD 59.9bn affect trade finance and FX risk; rural push (5,200+ rural branches, 120k BCs, agri credit +18% YoY) drives priority lending.

| Metric | Value |

|---|---|

| GDP FY2024 | ~7.2% |

| Consolidated assets | ₹22.5tn |

| UPI txns 2024 | 86.4bn |

| Exports FY2024-25 | USD 770bn |

| FDI FY2023-24 | USD 59.9bn |

| Rural branches | 5,200+ |

| Banking correspondents | 120,000+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect HDFC Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and investor communications.

A concise, visually segmented PESTLE summary of HDFC Bank that can be dropped into presentations or shared across teams to quickly align on external risks, regulatory shifts, and market positioning during planning sessions.

Economic factors

GDP Growth and Credit Demand

As India remained one of the fastest-growing major economies in 2025 with IMF-estimated GDP growth of about 6.8%, HDFC Bank reported stronger credit demand, noting retail and corporate loan growth of ~14% YoY in FY2025.

Robust expansion in manufacturing and services—industry GVA rising ~7% and services GVA ~6.5% in 2024–25—boosted working capital and term-loan requests, lifting corporate loan disbursals.

HDFC Bank’s asset quality and net interest income are tightly linked to macro health; with industrial output (IIP) up ~5% in 2025, credit uptake and margins showed positive correlation.

Interest Rate Environment

The MPC-driven repo rate at 6.50% (Dec 2025) directly compresses or expands HDFC Bank's NIM, which stood at 4.00% in FY2024; rate hikes raise funding costs, squeezing margins unless lending yields adjust.

In a volatile rate cycle, the bank must price deposits—CASA ratio 45.6% in FY2024—against advance yields to preserve profitability; mismatches erode net interest income.

Robust asset-liability management, including duration matching and liquidity coverage (LCR ~132% in 2024), is vital to mitigate interest-rate and tightening-liquidity risks.

Inflationary Pressures

Persisting inflation in India—CPI at 5.1% in Dec 2025 vs RBI target band—erodes retail disposable income, risking higher delinquencies and lower savings, pressuring HDFC Bank’s retail loan collections; the bank reported GNPA 0.69% in FY2025, reflecting resilient asset quality so far. Rising inflation raises operating costs, with employee expenses up 11% YoY in FY2025. HDFC Bank leverages analytics—credit models and dynamic pricing—to tighten underwriting and adjust loan yields amid inflationary trends.

Currency Fluctuations

Volatility in the INR/USD rate affects HDFC Bank’s treasury and corporate clients; in 2024 the rupee moved ~7% vs the dollar, increasing hedging demand and trading volumes.

HDFC Bank offers forwards, options and swaps, generating fee income—treasury fee income grew 5% YoY in FY2024—while exposure to sharp swings raises balance-sheet risk.

Significant depreciation raises costs for imported IT systems and increases burden on borrowers with foreign-currency debt, amplifying credit-risk pressures.

- INR moved ~7% vs USD in 2024

- Treasury/FX fee income +5% YoY FY2024

- Depreciation ups imported IT and FX-denominated debt costs

Capital Market Performance

The performance of Indian equity and debt markets directly affects HDFC Bank’s wealth management and investment banking, with FY2024 equity market cap rising ~18% YoY boosting AUM across HDFC Mutual Fund-linked channels.

Bull runs increased brokerage and transaction fees—NSE turnover averaged ~Rs 1.2 lakh crore/day in 2024 vs ~Rs 0.9 lakh crore/day in 2023—lifting retail activity and HDFC Securities revenues.

Market downturns compress AUM and fees; a 2022-23 correction saw industry-wide brokerage volumes drop ~25%, highlighting sensitivity of fee income to market cycles.

- Equity market cap +18% YoY (2024)

- NSE avg turnover ~Rs 1.2 lakh crore/day (2024)

- Brokerage volumes fell ~25% in 2022-23 correction

HDFC Bank: 14% Loan Growth, Strong CASA & GNPA 0.69% amid 6.8% GDP

India GDP ~6.8% (2025) boosted HDFC Bank loans (~14% YoY FY2025); IIP +5% (2025) aided credit demand. Repo 6.50% (Dec 2025) pressures NIM (4.00% FY2024); CASA 45.6% (FY2024) and LCR ~132% (2024) guide ALM. CPI 5.1% (Dec 2025) risks delinquencies; GNPA 0.69% (FY2025). INR moved ~7% vs USD (2024); treasury fees +5% YoY (FY2024).

| Metric | Value |

|---|---|

| GDP (2025) | 6.8% |

| Loan growth FY2025 | ~14% YoY |

| Repo (Dec 2025) | 6.50% |

| NIM FY2024 | 4.00% |

| GNPA FY2025 | 0.69% |

What You See Is What You Get

HDFC Bank PESTLE Analysis

The preview shown here is the exact HDFC Bank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. The file you see is the final version and will be available for instant download after payment. The layout, content, and structure match the product delivered, ensuring you get the complete, actionable analysis as displayed.