HD Korea Shipbuilding & Offshore Engineering Porter's Five Forces Analysis

Don't Miss the Bigger Picture

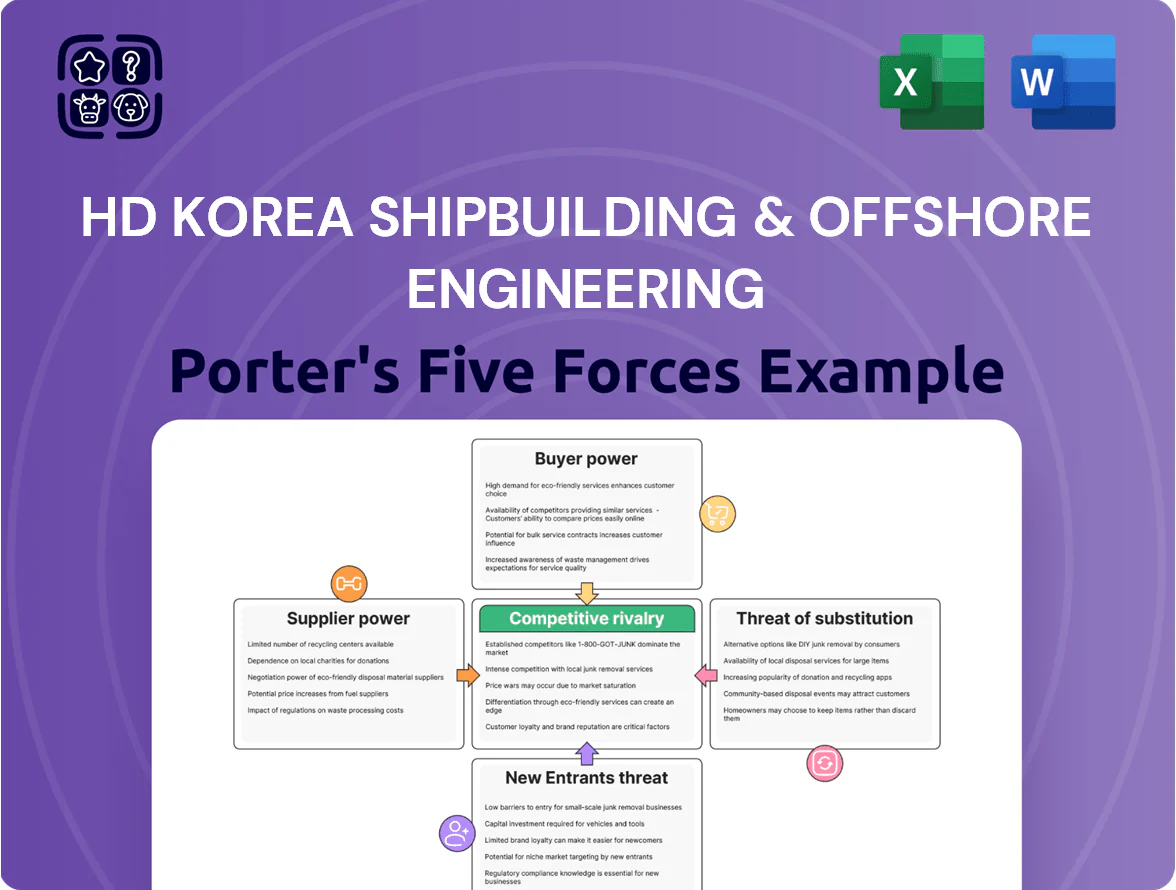

HD Korea Shipbuilding & Offshore Engineering faces high competitive rivalry and capital intensity, with moderate supplier power and buyer leverage shaped by large OEMs and long contract cycles.

Threats from new entrants are low due to scale barriers, while substitutes and technological shifts create selective disruption risks in specialized offshore segments.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore HD Korea Shipbuilding & Offshore Engineering’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Domestic Steel Producers

The cost of thick steel plates — about 18–22% of newbuild ship costs and roughly KRW 1.1–1.3 trillion of HD KSOE’s 2024 materials spend — gives POSCO and Hyundai Steel strong leverage; they tied pricing moves to iron ore benchmarks and raised semi-annual contract prices by ~9% in 2024. HD KSOE now faces intense semi-annual negotiations and hedging needs, and through end-2025 raw-material volatility keeps supplier pricing a key swing for margin, affecting EBIT by an estimated 120–180 bps.

Specialized Propulsion and Engine Technology

HD KSOE makes many engines internally, but relies heavily on niche global vendors for dual-fuel and ammonia-ready engine modules; these suppliers command leverage because their tech is critical to meet IMO 2026 CO2 and NOx limits and IMO 2030 GHG targets. In 2025, dual-fuel orders rose 38% in the merchant fleet, pushing component lead times to 9–14 months and giving suppliers pricing power; HD KSOE must keep strategic partnerships and long-term contracts to secure supply and cap costs.

Labor Shortages and Subcontractor Influence

The Korean shipbuilding sector faces a structural shortfall of skilled labor—KOSHIPA estimates a 15–20% gap in welders/engineers in 2024—boosting bargaining power of specialized labor outsourcers. As HD Korea Shipbuilding & Offshore Engineering manages a backlog worth about $25–30 billion (2024 est.), subcontractors can command premium rates for welders and marine engineers. That upward wage pressure pushed HD KSOE to plan capital spending increases, including KRW 500–700 billion through 2026 for automation and robotic welding. Persistent higher labor costs make automation investment a strategic necessity to protect margins.

Cryogenic Material Suppliers for LNG Carriers

HD Korea Shipbuilding & Offshore Engineering (HD KSOE) relies on a handful of patent‑protected suppliers for cryogenic insulation and membrane systems; these vendors control ~70–80% of the market for Moss and GTT-type membranes as of 2025, creating supplier concentration risk.

Because HD KSOE leads global gas carrier deliveries (roughly 35% market share in newbuild LNG carriers in 2024), any supplier price increase or delivery slip directly raises project costs and delays timelines, squeezing margins on 2024–25 contracts.

Disruption exposure is material: a single major supplier outage could delay 20–40% of concurrent LNG newbuild schedules, and replacement membranes carry retrofit and certification costs often exceeding $1–3 million per vessel.

Global Logistics and Energy Costs

Suppliers of electricity and global logistics directly affect HD Korea Shipbuilding & Offshore Engineering’s unit costs; Korea industrial electricity rose ~18% 2023–2024, raising yard power bills for large builds by millions of USD annually.

Freight for blocks and heavy equipment spiked 120% in 2021–22 and remains ~40% above pre‑pandemic levels, squeezing margins on fixed‑price contracts.

By late 2025, buyers demand green energy and low‑carbon shipping; sourcing certified renewables and green logistics adds 5–12% to supplier costs and complicates long‑term supplier commitments.

- Energy price volatility: +18% Korea electricity (2023–24)

- Logistics cost baseline: ~40% above 2019 levels (2025)

- Green premium: +5–12% on supplier services (late 2025)

- Impact: higher operational OPEX, narrower fixed‑price margins

Supplier power squeezes margins: steel, membranes, engines drive 120–180bps EBIT risk

Suppliers hold strong leverage: steel (18–22% of newbuild cost; KRW 1.1–1.3T materials spend in 2024) and membrane vendors (70–80% patent share) drive price and delivery risk, lifting raw‑material volatility to ~120–180bps EBIT swing through 2025; dual‑fuel engine lead times (9–14 months) and 15–20% skilled‑labor gap add premium costs, while electricity (+18% 2023–24) and logistics (~+40% vs 2019) further squeeze margins.

| Metric | Value |

|---|---|

| Steel spend (2024) | KRW 1.1–1.3T |

| Steel % of build | 18–22% |

| Membrane patent share (2025) | 70–80% |

| HD KSOE LNG share (2024) | ~35% |

| Engine lead times (2025) | 9–14 months |

| Skilled labor gap (2024) | 15–20% |

| Electricity change (2023–24) | +18% |

| Logistics vs 2019 (2025) | ~+40% |

| EBIT swing risk | 120–180 bps |

What is included in the product

Tailored Porter's Five Forces analysis for HD Korea Shipbuilding & Offshore Engineering revealing competitive intensity, buyer/supplier leverage, entry barriers, threat of substitutes, and rivalry—identifying disruptive risks, pricing pressures, and strategic levers to protect market share and inform investor or strategic decisions.

A concise, one-sheet Porter's Five Forces summary for HD Korea Shipbuilding & Offshore Engineering—ideal for quick strategic decisions and boardroom slides.

Customers Bargaining Power

Concentration of Mega-Shipping Lines

The customer base for HD KSOE is highly concentrated—top clients like AP Moller-Maersk (Denmark), Mediterranean Shipping Company (Switzerland), and energy majors such as QatarEnergy place multi-ship orders often worth $500m–$2bn each, giving them strong leverage to demand lower prices and bespoke specs; in 2024, a single container line accounted for ~18% of global newbuild demand, and the option to move orders to Chinese yards (which captured ~45% of global shipbuilding by DWT in 2024) or other Korean yards keeps continuous pricing and delivery pressure on HD KSOE.

Availability of Shipbuilding Slots

By end-2025, global dry dock utilization hit roughly 92% for high-spec vessels, making slots scarce and shifting bargaining power toward HD Korea Shipbuilding & Offshore Engineering (HD KSOE); major yards are booked 2–4 years out, so customers pay 5–15% premiums for earlier delivery of eco-friendly ships. This imbalance lets HD KSOE reject low-margin bids and prioritize higher-margin LNG carrier and FPSO contracts, supporting margin recovery and backlog quality.

High Switching Costs Post-Contract

Once HD Korea Shipbuilding & Offshore Engineering begins design post-contract, switching costs spike as vessel specifics, proprietary engine interfaces and smart-ship systems lock buyers in; mid-2025 industry data shows change orders cost 8–15% of contract value and can delay delivery 6–18 months.

Buyers can still wield strong leverage during tendering—top 5 global yards competed for 72% of large containership orders in 2024—letting shipowners extract price concessions before designs are fixed.

Demand for Green Transition Compliance

Shipowners face strict IMO and EU rules to cut CO2 and are rapidly ordering ammonia/hydrogen-capable vessels, pushing demand for HD KSOE’s green designs; global newbuild green fuel orders rose ~18% in 2024 to about 220 ships. Customers now force contractual fuel-efficiency and emission guarantees, shifting risk and cost onto builders. HD KSOE must innovate in fuel systems and digital efficiency to keep these buyers and avoid margin erosion.

- 220 green-fuel newbuilds in 2024 (~+18%)

- Buyers demand measurable emission guarantees

- Innovation = contract retention and risk control

Financing and Payment Terms

Large ship buyers often push heavy-tail payment terms—commonly 70–90% on delivery—forcing HD Korea Shipbuilding & Offshore Engineering (HD KSOE) to finance construction via debt or internal cash; HD KSOE reported net debt of KRW 16.2 trillion at end-2025, so this timing squeezes liquidity and raises financing costs.

Customers’ ability to set these terms amplifies industry cyclicality: when orderbooks fall (global newbuild orders dropped ~28% in 2024), payment delays hit margins and cash conversion hard.

- Typical heavy-tail: 70–90% at delivery

- HD KSOE net debt: KRW 16.2 trillion (end-2025)

- Global newbuild orders fell ~28% in 2024

HD KSOE: Strong demand meets margin squeeze—green builds shift risk, debt strains

Customers hold mixed power: a few giant shipowners (multi-$500m orders) and Chinese yard alternatives exert strong price pressure, but 92% utilization for high-spec vessels by end-2025 and 2–4 year bookings give HD KSOE leverage to reject low-margin work; heavy-tail payments (70–90% at delivery) strain HD KSOE’s KRW 16.2T net debt, while 220 green newbuilds in 2024 and emission guarantees shift tech/risk onto builders.

| Metric | Value |

|---|---|

| Top buyer share (single line) | ~18% of 2024 newbuild demand |

| Chinese yards DWT share | ~45% (2024) |

| High-spec utilization | ~92% (end-2025) |

| Green newbuilds | 220 (+18% in 2024) |

| Payment terms | 70–90% at delivery |

| HD KSOE net debt | KRW 16.2 trillion (end-2025) |

What You See Is What You Get

HD Korea Shipbuilding & Offshore Engineering Porter's Five Forces Analysis

This preview shows the exact HD Korea Shipbuilding & Offshore Engineering Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups. The document displayed is the professionally formatted, ready-to-use file included in the full version and will be available for instant download upon payment. What you see here is the complete deliverable, prepared for immediate application in strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

HD Korea Shipbuilding & Offshore Engineering faces high competitive rivalry and capital intensity, with moderate supplier power and buyer leverage shaped by large OEMs and long contract cycles.

Threats from new entrants are low due to scale barriers, while substitutes and technological shifts create selective disruption risks in specialized offshore segments.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore HD Korea Shipbuilding & Offshore Engineering’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Domestic Steel Producers

The cost of thick steel plates — about 18–22% of newbuild ship costs and roughly KRW 1.1–1.3 trillion of HD KSOE’s 2024 materials spend — gives POSCO and Hyundai Steel strong leverage; they tied pricing moves to iron ore benchmarks and raised semi-annual contract prices by ~9% in 2024. HD KSOE now faces intense semi-annual negotiations and hedging needs, and through end-2025 raw-material volatility keeps supplier pricing a key swing for margin, affecting EBIT by an estimated 120–180 bps.

Specialized Propulsion and Engine Technology

HD KSOE makes many engines internally, but relies heavily on niche global vendors for dual-fuel and ammonia-ready engine modules; these suppliers command leverage because their tech is critical to meet IMO 2026 CO2 and NOx limits and IMO 2030 GHG targets. In 2025, dual-fuel orders rose 38% in the merchant fleet, pushing component lead times to 9–14 months and giving suppliers pricing power; HD KSOE must keep strategic partnerships and long-term contracts to secure supply and cap costs.

Labor Shortages and Subcontractor Influence

The Korean shipbuilding sector faces a structural shortfall of skilled labor—KOSHIPA estimates a 15–20% gap in welders/engineers in 2024—boosting bargaining power of specialized labor outsourcers. As HD Korea Shipbuilding & Offshore Engineering manages a backlog worth about $25–30 billion (2024 est.), subcontractors can command premium rates for welders and marine engineers. That upward wage pressure pushed HD KSOE to plan capital spending increases, including KRW 500–700 billion through 2026 for automation and robotic welding. Persistent higher labor costs make automation investment a strategic necessity to protect margins.

Cryogenic Material Suppliers for LNG Carriers

HD Korea Shipbuilding & Offshore Engineering (HD KSOE) relies on a handful of patent‑protected suppliers for cryogenic insulation and membrane systems; these vendors control ~70–80% of the market for Moss and GTT-type membranes as of 2025, creating supplier concentration risk.

Because HD KSOE leads global gas carrier deliveries (roughly 35% market share in newbuild LNG carriers in 2024), any supplier price increase or delivery slip directly raises project costs and delays timelines, squeezing margins on 2024–25 contracts.

Disruption exposure is material: a single major supplier outage could delay 20–40% of concurrent LNG newbuild schedules, and replacement membranes carry retrofit and certification costs often exceeding $1–3 million per vessel.

Global Logistics and Energy Costs

Suppliers of electricity and global logistics directly affect HD Korea Shipbuilding & Offshore Engineering’s unit costs; Korea industrial electricity rose ~18% 2023–2024, raising yard power bills for large builds by millions of USD annually.

Freight for blocks and heavy equipment spiked 120% in 2021–22 and remains ~40% above pre‑pandemic levels, squeezing margins on fixed‑price contracts.

By late 2025, buyers demand green energy and low‑carbon shipping; sourcing certified renewables and green logistics adds 5–12% to supplier costs and complicates long‑term supplier commitments.

- Energy price volatility: +18% Korea electricity (2023–24)

- Logistics cost baseline: ~40% above 2019 levels (2025)

- Green premium: +5–12% on supplier services (late 2025)

- Impact: higher operational OPEX, narrower fixed‑price margins

Supplier power squeezes margins: steel, membranes, engines drive 120–180bps EBIT risk

Suppliers hold strong leverage: steel (18–22% of newbuild cost; KRW 1.1–1.3T materials spend in 2024) and membrane vendors (70–80% patent share) drive price and delivery risk, lifting raw‑material volatility to ~120–180bps EBIT swing through 2025; dual‑fuel engine lead times (9–14 months) and 15–20% skilled‑labor gap add premium costs, while electricity (+18% 2023–24) and logistics (~+40% vs 2019) further squeeze margins.

| Metric | Value |

|---|---|

| Steel spend (2024) | KRW 1.1–1.3T |

| Steel % of build | 18–22% |

| Membrane patent share (2025) | 70–80% |

| HD KSOE LNG share (2024) | ~35% |

| Engine lead times (2025) | 9–14 months |

| Skilled labor gap (2024) | 15–20% |

| Electricity change (2023–24) | +18% |

| Logistics vs 2019 (2025) | ~+40% |

| EBIT swing risk | 120–180 bps |

What is included in the product

Tailored Porter's Five Forces analysis for HD Korea Shipbuilding & Offshore Engineering revealing competitive intensity, buyer/supplier leverage, entry barriers, threat of substitutes, and rivalry—identifying disruptive risks, pricing pressures, and strategic levers to protect market share and inform investor or strategic decisions.

A concise, one-sheet Porter's Five Forces summary for HD Korea Shipbuilding & Offshore Engineering—ideal for quick strategic decisions and boardroom slides.

Customers Bargaining Power

Concentration of Mega-Shipping Lines

The customer base for HD KSOE is highly concentrated—top clients like AP Moller-Maersk (Denmark), Mediterranean Shipping Company (Switzerland), and energy majors such as QatarEnergy place multi-ship orders often worth $500m–$2bn each, giving them strong leverage to demand lower prices and bespoke specs; in 2024, a single container line accounted for ~18% of global newbuild demand, and the option to move orders to Chinese yards (which captured ~45% of global shipbuilding by DWT in 2024) or other Korean yards keeps continuous pricing and delivery pressure on HD KSOE.

Availability of Shipbuilding Slots

By end-2025, global dry dock utilization hit roughly 92% for high-spec vessels, making slots scarce and shifting bargaining power toward HD Korea Shipbuilding & Offshore Engineering (HD KSOE); major yards are booked 2–4 years out, so customers pay 5–15% premiums for earlier delivery of eco-friendly ships. This imbalance lets HD KSOE reject low-margin bids and prioritize higher-margin LNG carrier and FPSO contracts, supporting margin recovery and backlog quality.

High Switching Costs Post-Contract

Once HD Korea Shipbuilding & Offshore Engineering begins design post-contract, switching costs spike as vessel specifics, proprietary engine interfaces and smart-ship systems lock buyers in; mid-2025 industry data shows change orders cost 8–15% of contract value and can delay delivery 6–18 months.

Buyers can still wield strong leverage during tendering—top 5 global yards competed for 72% of large containership orders in 2024—letting shipowners extract price concessions before designs are fixed.

Demand for Green Transition Compliance

Shipowners face strict IMO and EU rules to cut CO2 and are rapidly ordering ammonia/hydrogen-capable vessels, pushing demand for HD KSOE’s green designs; global newbuild green fuel orders rose ~18% in 2024 to about 220 ships. Customers now force contractual fuel-efficiency and emission guarantees, shifting risk and cost onto builders. HD KSOE must innovate in fuel systems and digital efficiency to keep these buyers and avoid margin erosion.

- 220 green-fuel newbuilds in 2024 (~+18%)

- Buyers demand measurable emission guarantees

- Innovation = contract retention and risk control

Financing and Payment Terms

Large ship buyers often push heavy-tail payment terms—commonly 70–90% on delivery—forcing HD Korea Shipbuilding & Offshore Engineering (HD KSOE) to finance construction via debt or internal cash; HD KSOE reported net debt of KRW 16.2 trillion at end-2025, so this timing squeezes liquidity and raises financing costs.

Customers’ ability to set these terms amplifies industry cyclicality: when orderbooks fall (global newbuild orders dropped ~28% in 2024), payment delays hit margins and cash conversion hard.

- Typical heavy-tail: 70–90% at delivery

- HD KSOE net debt: KRW 16.2 trillion (end-2025)

- Global newbuild orders fell ~28% in 2024

HD KSOE: Strong demand meets margin squeeze—green builds shift risk, debt strains

Customers hold mixed power: a few giant shipowners (multi-$500m orders) and Chinese yard alternatives exert strong price pressure, but 92% utilization for high-spec vessels by end-2025 and 2–4 year bookings give HD KSOE leverage to reject low-margin work; heavy-tail payments (70–90% at delivery) strain HD KSOE’s KRW 16.2T net debt, while 220 green newbuilds in 2024 and emission guarantees shift tech/risk onto builders.

| Metric | Value |

|---|---|

| Top buyer share (single line) | ~18% of 2024 newbuild demand |

| Chinese yards DWT share | ~45% (2024) |

| High-spec utilization | ~92% (end-2025) |

| Green newbuilds | 220 (+18% in 2024) |

| Payment terms | 70–90% at delivery |

| HD KSOE net debt | KRW 16.2 trillion (end-2025) |

What You See Is What You Get

HD Korea Shipbuilding & Offshore Engineering Porter's Five Forces Analysis

This preview shows the exact HD Korea Shipbuilding & Offshore Engineering Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups. The document displayed is the professionally formatted, ready-to-use file included in the full version and will be available for instant download upon payment. What you see here is the complete deliverable, prepared for immediate application in strategic or investment decisions.