Huadian Power International PESTLE Analysis

Your Competitive Advantage Starts with This Report

Navigate the external forces shaping Huadian Power International with our concise PESTLE snapshot—spot regulatory risks, market shifts, and technological opportunities that could redefine growth and compliance. Ideal for investors and strategists, this analysis distills complex trends into actionable insight. Purchase the full PESTLE to access the complete, editable breakdown and make informed decisions faster.

Political factors

State Ownership and Strategic Alignment

As a major state-owned enterprise, Huadian Power International is tightly integrated with Chinese national strategy, with state ownership exceeding 50% and parent-level coordination through China Huadian Corporation.

By end-2025 its operations target full compliance with the 14th Five-Year Plan final metrics and preliminary 15th Five-Year Plan goals, guiding ~18 GW renewables deployment commitments and coal-to-gas transition targets in ongoing projects.

This strategic alignment secures strong government support, reflected in priority access to state-led infrastructure funding—2024 group-level CAPEX ~RMB 60 billion—and preferred project approvals across multiple provinces.

Energy Security and Transition Mandates

The political emphasis on energy security forces Huadian Power International to ensure stable supply amid volatile fuel costs—coal price spikes in 2024 pushed thermal margins down 18%, pressuring operations to secure fuel contracts and reserve capacity.

Government mandates require balancing coal-fired generation with rapid renewable expansion; China aims for 1,200 GW wind and solar by 2030, driving Huadian to accelerate ~15% annual renewables capex allocation in 2025 guidance.

Political pressure to cut carbon intensity influences every major board investment: Huadian targets a 30% CO2 intensity reduction by 2030 versus 2020 levels, altering project approvals and shifting financing toward low-carbon assets.

Geopolitical Influence on Fuel Supply

Geopolitical tensions and trade relations directly affect Huadian Power International’s coal imports and component supply; for example, China’s coal imports from Indonesia fell 12% in 2024 while Australian coal supplies were intermittently disrupted, raising delivered coal costs by ~8–15% YTD for major generators. Shifts in diplomatic ties with Indonesia or Australia could force rapid procurement shifts, increasing hedging and inventory costs to maintain fuel reliability and price stability.

Regional Development and Grid Integration

Government incentives for inland and western development are pushing Huadian Power International to expand into provinces like Xinjiang and Gansu, where the company added 1.2 GW of capacity in 2024, aligning with national West-to-East Power Transmission priorities that favor approvals for large-scale thermal and renewable projects along transmission corridors.

This regional push enables Huadian to access emerging industrial demand—western fixed-asset investment rose 8.5% year-on-year in 2024—supporting urbanization targets and potentially lifting regional power sales and utilization rates.

- 1.2 GW added in western provinces (2024)

- West-to-East directives prioritize transmission corridor projects

- Western fixed-asset investment +8.5% YoY (2024)

- Strategic alignment with national urbanization and grid integration

Policy Support for Decarbonization

The central government's pledge to peak CO2 by 2030 underpins Huadian Power International's green shift, aligning its target of 20% non-fossil capacity by 2025 and accelerated coal-to-gas conversions; national subsidies and tax breaks funneled RMB 18.7 billion into low-carbon projects in 2024–2025, shaping capital allocation decisions.

Preferential lending lowered financing costs—green loans reached RMB 42.3 billion for power firms in 2025—while political backing for the national carbon trading market, which traded 1.1 billion tonnes CO2e in 2025, creates revenue prospects from efficiency gains.

- 2030 peak-carbon goal aligns strategy

- RMB 18.7bn subsidies/tax incentives (2024–25)

- RMB 42.3bn green loans (2025)

- National carbon market 1.1bn tCO2e traded (2025)

State-backed Huadian ramps RMB60bn CAPEX for 18GW renewables as coal costs surge

State ownership (>50%) ties Huadian to national energy strategy, securing priority funding (group CAPEX ~RMB60bn in 2024) and approvals while forcing compliance with Five-Year Plan renewables (≈18GW by 2025) and carbon targets (30% CO2 intensity cut by 2030). Geopolitics raised delivered coal costs ~8–15% YTD (2024), driving hedging and faster coal-to-gas/renewables capex (≈15% annual shift in 2025 guidance).

| Metric | Value |

|---|---|

| Group CAPEX (2024) | RMB60bn |

| Planned renewables (by 2025) | ≈18GW |

| CO2 intensity target (2030 vs 2020) | -30% |

| Delivered coal cost change (2024) | +8–15% YTD |

| Green loans to sector (2025) | RMB42.3bn |

What is included in the product

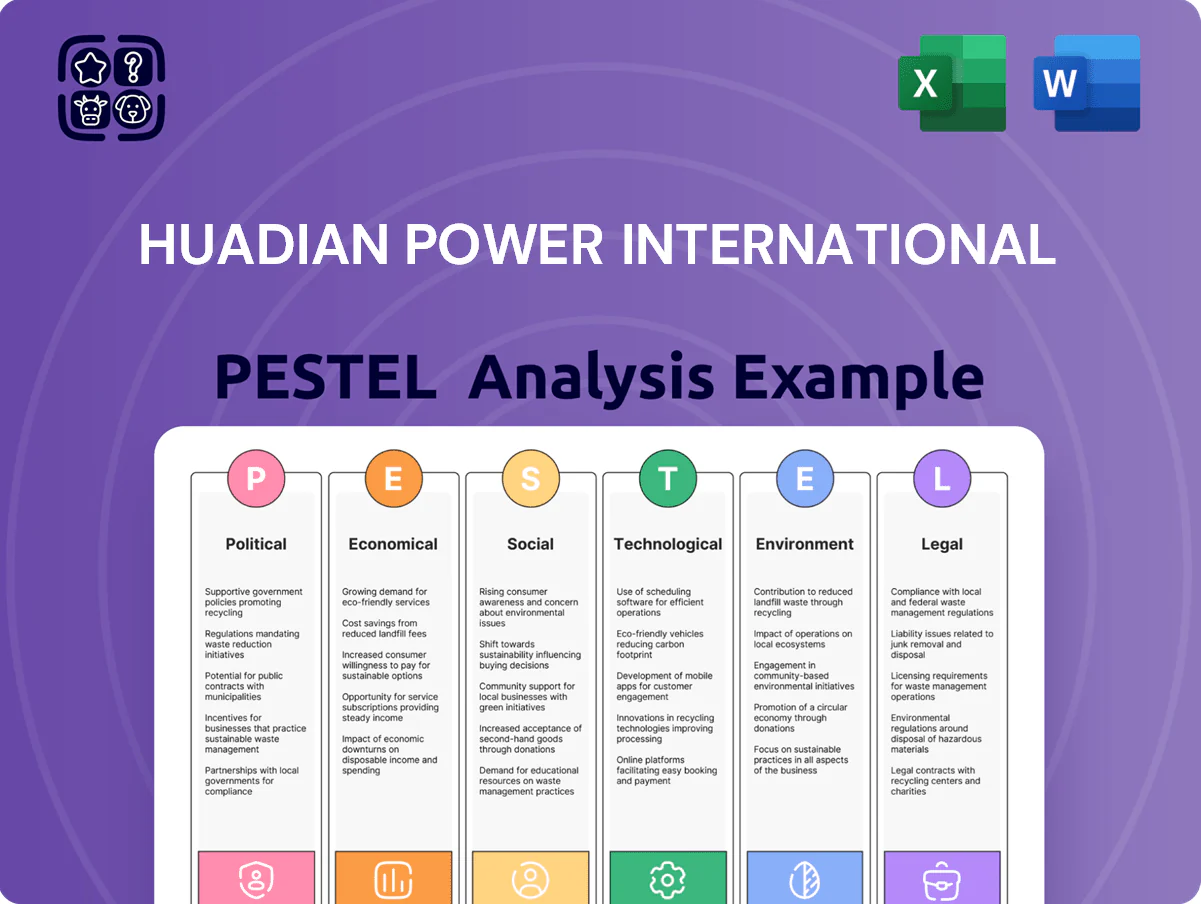

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Huadian Power International, using current market and regulatory trends to identify strategic risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary of Huadian Power International that simplifies external risk assessment for quick inclusion in presentations, team alignments, or consultant reports while allowing easy annotation for region- or business-specific context.

Economic factors

Fluctuations in Coal Procurement Costs

Coal prices remain the largest driver of Huadian Power International’s margins; thermal coal cost swings altered Chinese coal CIF prices from about $120/ton in Jan 2024 to peaks near $180/ton in late 2024, squeezing utility margins.

Despite 2024 domestic output rising 3.5% YoY, global volatility and supply-chain disruptions—including Black Sea and Australian export constraints—led to sudden price spikes that raised fuel costs unpredictably.

The company leans on multi-year supply contracts and strategic stockpiles covering roughly 60–90 days of burn to dampen shocks, yet coal-price sensitivity still materially affects quarterly earnings and unit generation costs.

Impact of Electricity Market Liberalization

China's push to liberalize electricity pricing has shifted Huadian Power International's sales mix: by Q4 2025 about 62% of its generation was sold via spot and forward market mechanisms versus ~38% under regulated tariffs, increasing exposure to wholesale volatility.

This trend heightens competition from IPPs and requires Huadian to deploy advanced price-hedging and dynamic bidding; FY2024 market revenue rose 14% year-on-year, underscoring opportunity but compressing margin variability.

Capital Expenditure for Green Transition

Decommissioning Huadian Power Internationals coal fleet and building renewables requires capital expenditures estimated at over CNY 100 billion through 2028, straining the balance sheet and raising leverage risks as capex-to-assets rises toward 12% in 2024–25.

Financing relies on green bonds and specialized loans; Huadian tapped a CNY 5.2 billion green bond in 2023 and explores syndicated green loans, adding complexity in covenant and ESG reporting.

Long-term O&M and fuel savings from renewables could cut generation costs by an estimated 10–15% vs coal, but high upfront capital intensity increases short-term financing costs and ROE pressure.

Macroeconomic Growth and Power Demand

China's 2024 GDP growth slowed to an estimated 4.5% year-on-year, directly dampening industrial and residential electricity and heat demand for Huadian Power International and shifting load patterns as services and high-tech manufacturing rise.

Growth in high-tech sectors raises daytime baseload and peak variability, forcing Huadian to adapt dispatch and ramp-up schedules; 2024 industrial power consumption rose ~2.1% while tertiary sector electricity use grew ~6.8%.

Accelerations or slowdowns require real-time adjustments to generation mixes and capex timing—Huadian must align capacity expansion with projected demand elasticity and 2025 forecasts showing modest recovery toward 5.0% GDP.

- 2024 China GDP ~4.5%

- Industrial power +2.1% (2024)

- Tertiary sector electricity +6.8% (2024)

- 2025 GDP forecast ~5.0% — impacts capex and dispatch

Interest Rate Trends and Debt Financing

Huadian Power International, as a capital-intensive utility, is highly sensitive to interest rate shifts and Chinese credit availability; a 2024 PBOC policy rate cut to 2.50% for MLF-like operations eased refinancing costs, lowering average corporate borrowing yields by about 40–70 bps versus 2023.

Lower rates support cheaper expansion and debt refinancing, helping maintain its debt-to-equity (2024 reported adjusted net debt/equity ~1.1x) and reduce interest expense pressure.

The company’s financial health remains closely tied to People's Bank of China decisions, with tighter policy or credit retraction potentially raising borrowing costs and refinancing risks.

- 2024 PBOC easing cut ~40–70 bps corporate yields

- Huadian adjusted net debt/equity ~1.1x (2024)

- High exposure to Chinese bank credit conditions for capex/refinancing

Huadian faces margin & leverage pressure as coal volatility, CNY100bn+ capex bite

Coal-price volatility, liberalized power pricing (62% market sales by Q4 2025), and CNY 100bn+ transition capex through 2028 drive margin and leverage risk; 2024 GDP ~4.5%, industrial power +2.1%, tertiary +6.8%; PBOC easing cut corporate yields ~40–70bps, Huadian adj net debt/equity ~1.1x (2024).

| Metric | 2024/2025 |

|---|---|

| Coal CIF ($/t) | $120–$180 |

| Market sales | ~62% |

| Capex to 2028 | CNY>100bn |

| Adj net debt/equity | 1.1x |

Same Document Delivered

Huadian Power International PESTLE Analysis

The preview shown here is the exact Huadian Power International PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the content, layout, and structure visible in the preview are identical to the file you’ll download immediately after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Navigate the external forces shaping Huadian Power International with our concise PESTLE snapshot—spot regulatory risks, market shifts, and technological opportunities that could redefine growth and compliance. Ideal for investors and strategists, this analysis distills complex trends into actionable insight. Purchase the full PESTLE to access the complete, editable breakdown and make informed decisions faster.

Political factors

State Ownership and Strategic Alignment

As a major state-owned enterprise, Huadian Power International is tightly integrated with Chinese national strategy, with state ownership exceeding 50% and parent-level coordination through China Huadian Corporation.

By end-2025 its operations target full compliance with the 14th Five-Year Plan final metrics and preliminary 15th Five-Year Plan goals, guiding ~18 GW renewables deployment commitments and coal-to-gas transition targets in ongoing projects.

This strategic alignment secures strong government support, reflected in priority access to state-led infrastructure funding—2024 group-level CAPEX ~RMB 60 billion—and preferred project approvals across multiple provinces.

Energy Security and Transition Mandates

The political emphasis on energy security forces Huadian Power International to ensure stable supply amid volatile fuel costs—coal price spikes in 2024 pushed thermal margins down 18%, pressuring operations to secure fuel contracts and reserve capacity.

Government mandates require balancing coal-fired generation with rapid renewable expansion; China aims for 1,200 GW wind and solar by 2030, driving Huadian to accelerate ~15% annual renewables capex allocation in 2025 guidance.

Political pressure to cut carbon intensity influences every major board investment: Huadian targets a 30% CO2 intensity reduction by 2030 versus 2020 levels, altering project approvals and shifting financing toward low-carbon assets.

Geopolitical Influence on Fuel Supply

Geopolitical tensions and trade relations directly affect Huadian Power International’s coal imports and component supply; for example, China’s coal imports from Indonesia fell 12% in 2024 while Australian coal supplies were intermittently disrupted, raising delivered coal costs by ~8–15% YTD for major generators. Shifts in diplomatic ties with Indonesia or Australia could force rapid procurement shifts, increasing hedging and inventory costs to maintain fuel reliability and price stability.

Regional Development and Grid Integration

Government incentives for inland and western development are pushing Huadian Power International to expand into provinces like Xinjiang and Gansu, where the company added 1.2 GW of capacity in 2024, aligning with national West-to-East Power Transmission priorities that favor approvals for large-scale thermal and renewable projects along transmission corridors.

This regional push enables Huadian to access emerging industrial demand—western fixed-asset investment rose 8.5% year-on-year in 2024—supporting urbanization targets and potentially lifting regional power sales and utilization rates.

- 1.2 GW added in western provinces (2024)

- West-to-East directives prioritize transmission corridor projects

- Western fixed-asset investment +8.5% YoY (2024)

- Strategic alignment with national urbanization and grid integration

Policy Support for Decarbonization

The central government's pledge to peak CO2 by 2030 underpins Huadian Power International's green shift, aligning its target of 20% non-fossil capacity by 2025 and accelerated coal-to-gas conversions; national subsidies and tax breaks funneled RMB 18.7 billion into low-carbon projects in 2024–2025, shaping capital allocation decisions.

Preferential lending lowered financing costs—green loans reached RMB 42.3 billion for power firms in 2025—while political backing for the national carbon trading market, which traded 1.1 billion tonnes CO2e in 2025, creates revenue prospects from efficiency gains.

- 2030 peak-carbon goal aligns strategy

- RMB 18.7bn subsidies/tax incentives (2024–25)

- RMB 42.3bn green loans (2025)

- National carbon market 1.1bn tCO2e traded (2025)

State-backed Huadian ramps RMB60bn CAPEX for 18GW renewables as coal costs surge

State ownership (>50%) ties Huadian to national energy strategy, securing priority funding (group CAPEX ~RMB60bn in 2024) and approvals while forcing compliance with Five-Year Plan renewables (≈18GW by 2025) and carbon targets (30% CO2 intensity cut by 2030). Geopolitics raised delivered coal costs ~8–15% YTD (2024), driving hedging and faster coal-to-gas/renewables capex (≈15% annual shift in 2025 guidance).

| Metric | Value |

|---|---|

| Group CAPEX (2024) | RMB60bn |

| Planned renewables (by 2025) | ≈18GW |

| CO2 intensity target (2030 vs 2020) | -30% |

| Delivered coal cost change (2024) | +8–15% YTD |

| Green loans to sector (2025) | RMB42.3bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Huadian Power International, using current market and regulatory trends to identify strategic risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary of Huadian Power International that simplifies external risk assessment for quick inclusion in presentations, team alignments, or consultant reports while allowing easy annotation for region- or business-specific context.

Economic factors

Fluctuations in Coal Procurement Costs

Coal prices remain the largest driver of Huadian Power International’s margins; thermal coal cost swings altered Chinese coal CIF prices from about $120/ton in Jan 2024 to peaks near $180/ton in late 2024, squeezing utility margins.

Despite 2024 domestic output rising 3.5% YoY, global volatility and supply-chain disruptions—including Black Sea and Australian export constraints—led to sudden price spikes that raised fuel costs unpredictably.

The company leans on multi-year supply contracts and strategic stockpiles covering roughly 60–90 days of burn to dampen shocks, yet coal-price sensitivity still materially affects quarterly earnings and unit generation costs.

Impact of Electricity Market Liberalization

China's push to liberalize electricity pricing has shifted Huadian Power International's sales mix: by Q4 2025 about 62% of its generation was sold via spot and forward market mechanisms versus ~38% under regulated tariffs, increasing exposure to wholesale volatility.

This trend heightens competition from IPPs and requires Huadian to deploy advanced price-hedging and dynamic bidding; FY2024 market revenue rose 14% year-on-year, underscoring opportunity but compressing margin variability.

Capital Expenditure for Green Transition

Decommissioning Huadian Power Internationals coal fleet and building renewables requires capital expenditures estimated at over CNY 100 billion through 2028, straining the balance sheet and raising leverage risks as capex-to-assets rises toward 12% in 2024–25.

Financing relies on green bonds and specialized loans; Huadian tapped a CNY 5.2 billion green bond in 2023 and explores syndicated green loans, adding complexity in covenant and ESG reporting.

Long-term O&M and fuel savings from renewables could cut generation costs by an estimated 10–15% vs coal, but high upfront capital intensity increases short-term financing costs and ROE pressure.

Macroeconomic Growth and Power Demand

China's 2024 GDP growth slowed to an estimated 4.5% year-on-year, directly dampening industrial and residential electricity and heat demand for Huadian Power International and shifting load patterns as services and high-tech manufacturing rise.

Growth in high-tech sectors raises daytime baseload and peak variability, forcing Huadian to adapt dispatch and ramp-up schedules; 2024 industrial power consumption rose ~2.1% while tertiary sector electricity use grew ~6.8%.

Accelerations or slowdowns require real-time adjustments to generation mixes and capex timing—Huadian must align capacity expansion with projected demand elasticity and 2025 forecasts showing modest recovery toward 5.0% GDP.

- 2024 China GDP ~4.5%

- Industrial power +2.1% (2024)

- Tertiary sector electricity +6.8% (2024)

- 2025 GDP forecast ~5.0% — impacts capex and dispatch

Interest Rate Trends and Debt Financing

Huadian Power International, as a capital-intensive utility, is highly sensitive to interest rate shifts and Chinese credit availability; a 2024 PBOC policy rate cut to 2.50% for MLF-like operations eased refinancing costs, lowering average corporate borrowing yields by about 40–70 bps versus 2023.

Lower rates support cheaper expansion and debt refinancing, helping maintain its debt-to-equity (2024 reported adjusted net debt/equity ~1.1x) and reduce interest expense pressure.

The company’s financial health remains closely tied to People's Bank of China decisions, with tighter policy or credit retraction potentially raising borrowing costs and refinancing risks.

- 2024 PBOC easing cut ~40–70 bps corporate yields

- Huadian adjusted net debt/equity ~1.1x (2024)

- High exposure to Chinese bank credit conditions for capex/refinancing

Huadian faces margin & leverage pressure as coal volatility, CNY100bn+ capex bite

Coal-price volatility, liberalized power pricing (62% market sales by Q4 2025), and CNY 100bn+ transition capex through 2028 drive margin and leverage risk; 2024 GDP ~4.5%, industrial power +2.1%, tertiary +6.8%; PBOC easing cut corporate yields ~40–70bps, Huadian adj net debt/equity ~1.1x (2024).

| Metric | 2024/2025 |

|---|---|

| Coal CIF ($/t) | $120–$180 |

| Market sales | ~62% |

| Capex to 2028 | CNY>100bn |

| Adj net debt/equity | 1.1x |

Same Document Delivered

Huadian Power International PESTLE Analysis

The preview shown here is the exact Huadian Power International PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the content, layout, and structure visible in the preview are identical to the file you’ll download immediately after payment.