Hearthside Food Solutions PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, supply-chain pressures, and rising sustainability expectations are reshaping Hearthside Food Solutions’ competitive landscape—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter strategy and investment calls. Purchase the full PESTLE for a detailed, ready-to-use analysis that equips you with actionable insights and downloadable charts to drive confident decisions.

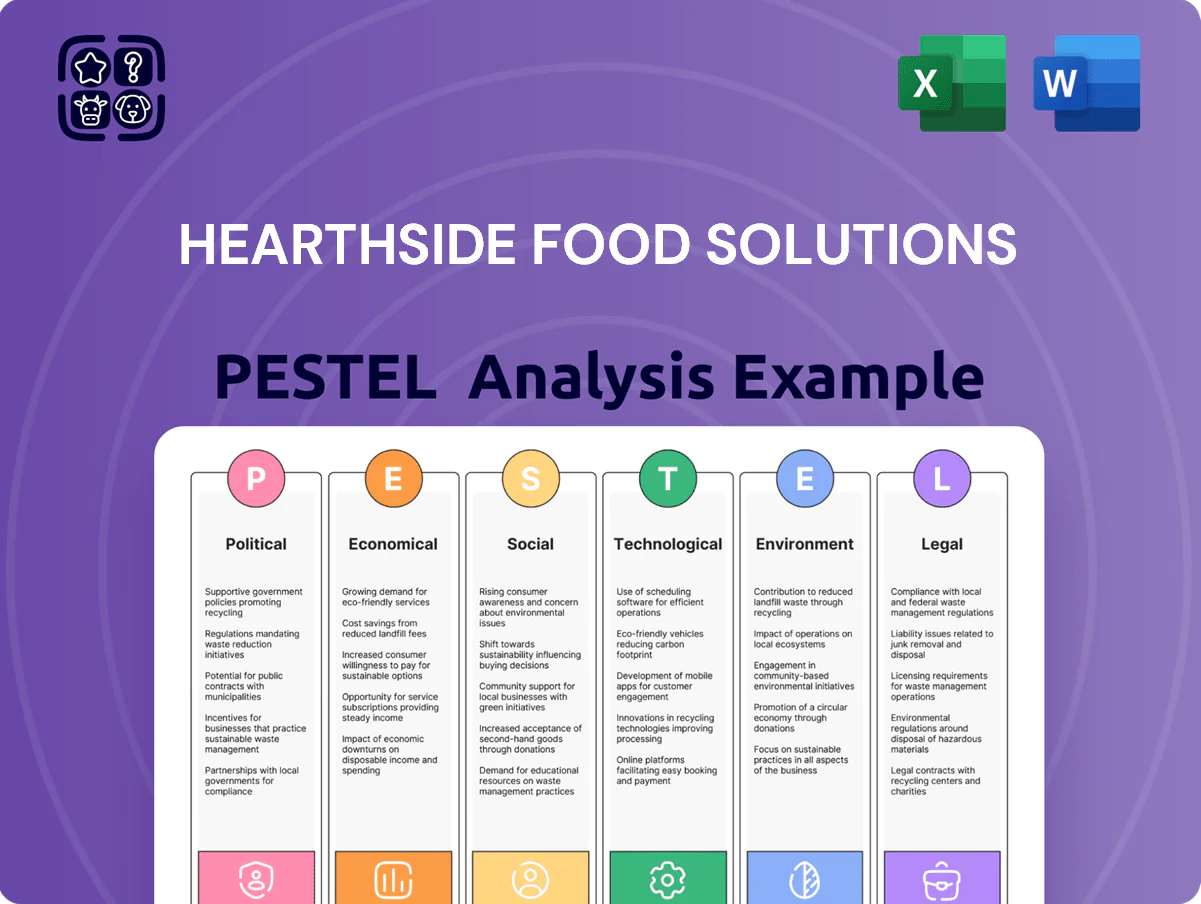

Political factors

Trade Policy and Import Tariffs

Changes in trade agreements and tariffs on inputs like cocoa and specialty grains can raise Hearthside Food Solutions’ COGS; a 10% tariff on cocoa could add roughly $10–15 million annually given industry cocoa spend estimates. As a contract manufacturer for global brands, Hearthside faces supply-chain risk from geopolitical tensions—Russia/Ukraine and recent 2023–24 export restrictions increased volatility in agri-exports. Analysts should track US-Mexico-Canada and US-EU trade relations and 2024 agricultural import volumes to gauge margin pressure.

Agricultural Subsidies and Farm Bills

Government subsidies for corn, wheat and soy—U.S. farm program payments totaling about $22.7 billion in 2023—directly lower raw-material costs for Hearthside, since corn-derived starches and soy-based fats are key inputs.

Changes in the 2023 Farm Bill implementation and potential 2025 amendments could shift subsidy allocations, affecting input price volatility and supply economics for large-scale processors.

Procurement and finance teams should monitor USDA reports and Congressional schedules to model multi-year price scenarios and hedge strategies for baking and snack ingredients.

Labor Regulation and Immigration Policy

As a major manufacturing employer, Hearthside is exposed to federal and state labor and immigration shifts; tighter enforcement or H-2B/H-2A visa restrictions could shrink its labor pool—US manufacturing job openings hit 611,000 in Dec 2025, amplifying competition for workers.

Political-driven labor law changes, such as higher minimums or union activity, may force wage increases; Hearthside reported 2024 labor expense growth of ~8% year-over-year, raising margin pressure.

Consequently, strategic planning must weigh costs of higher wages versus automation: capital expenditures on automation in food manufacturing rose ~12% in 2024, a likely response pathway.

Food Labeling and Nutritional Mandates

- 42% US adult obesity (2024)

- 60%+ SKUs potentially impacted

- 3–7% higher COGS for reformulation

- <90-day required lead times

- $1.2M average avoided recall cost

Geopolitical Supply Chain Stability

Regional conflicts in key suppliers—notably sunflower oil from Ukraine (over 50% of global exports pre-2022) and safflower/citrus flavor hubs—have caused price spikes up to 40% and shipment delays, creating sudden bottlenecks for processors like Hearthside.

Hearthside must diversify sourcing; as of 2024 the company reported sourcing from over 15 countries across three continents, reducing single-country exposure to under 20% per ingredient.

Investors should assess Hearthside’s supplier concentration metrics and geographic footprint—low supplier Herfindahl indices and multi-region contracts indicate stronger hedges against geopolitical disruption.

- Supply shocks: commodity price spikes up to 40% in recent conflicts

- Diversification: Hearthside sources from 15+ countries (2024)

- Investor metric: target supplier share <20% per country; lower Herfindahl preferred

Rising tariffs, labor costs & reformulation pressures squeeze COGS as automation offsets

Trade/tariff shifts and 2023–25 farm policy can raise COGS (10% cocoa tariff ≈ $10–15M); 2023 US farm payments $22.7B lowered input costs. Labor/visa enforcement and rising wages (2024 labor expense +8%) increase payroll pressure; automation CAPEX +12% (2024) is a mitigation. FDA labeling/sugar rules affect >60% SKUs; reformulation adds 3–7% COGS; supplier shocks spiked prices up to 40%.

| Metric | Value |

|---|---|

| US farm payments (2023) | $22.7B |

| Labor expense change (2024) | +8% |

| Automation CAPEX (2024) | +12% |

| Obesity (2024) | 42% |

What is included in the product

Explores how external macro-environmental factors uniquely impact Hearthside Food Solutions across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights tailored for executives, investors, and strategists to identify threats, opportunities, and actionable responses.

A clean, concise PESTLE summary of Hearthside Food Solutions that’s visually segmented for quick meeting use, easily dropped into slides or shared across teams to align on external risks and market positioning.

Economic factors

Commodity Price Volatility

Commodity price volatility for inputs like flour, sugar and edible oils—whose global prices swung 10–25% year-over-year in 2023–2024 due to weather and demand shocks—directly affects Hearthside Food Solutions; operating at high volumes means a 1% input-cost rise can cut margins materially across production lines. Effective hedging (futures, options) and pass-through or transparent pricing with clients are essential to stabilize EBITDA, given industry input cost share often exceeds 30% of COGS. In 2024, food-ingredient futures showed heightened basis risk, underscoring the need for dynamic risk limits and monthly reporting to protect profitability.

Inflationary Pressure on Operating Costs

Persistent inflation raised input costs for co-manufacturers like Hearthside, with US headline CPI averaging 3.4% in 2024 and industrial energy prices up ~12% year-over-year, while corrugated packaging saw pulp and paper prices rise ~8–10% in 2024; pass-through clauses help, but price elasticity limits consumer tolerance, so management must drive operational efficiency—lean manufacturing, yield improvements, and renegotiated supplier contracts—to protect margins and maintain competitive co-manufacturing pricing.

Consumer Shift Toward Private Labels

During downturns consumers trade down to private labels—U.S. private-label grocery share rose to 17.7% in 2024 (IRI), boosting demand for lower-cost snacks and bars. Hearthside, producing for national brands and private-label retailers, captures both premium and value segments, reducing revenue cyclicality. In 2025 hedge terms, mixed client exposure supported a stable margin profile as private-label volumes grew mid-single digits year-over-year. This dual exposure is attractive to institutional investors assessing cash-flow resilience.

Labor Market Tightness and Wage Growth

Rising minimum wages—federal proposals and 22 state increases in 2024 lifted entry-level pay by up to 12% in some regions—plus a tight industrial labor market (US manufacturing job openings averaging 465,000 in 2024) are elevating Hearthside’s labor costs, pressuring margins.

The company must weigh higher wages against capital investment: automation reduces hourly labor needs but requires CapEx; industry robotic investment rose 8% in 2024, guiding Hearthside’s 2025 strategy trade-off.

- 22 states raised minimums in 2024; entry-level pay up to +12%

- US manufacturing openings ~465,000 (2024)

- Industrial robot investment +8% (2024)

- 2025 focus: balance wage inflation vs CapEx for automation

Interest Rates and Capital Expenditures

The recent rise in US benchmark rates—the federal funds target averaging about 5.25–5.50% in 2024—raises borrowing costs for Hearthside, increasing financing expenses for capacity expansions or tech upgrades and potentially delaying new plant builds or acquisitions.

Analysts should review Hearthside’s leverage: as of FY2024 the company carried significant debt after private-equity buyouts, so free cash flow and interest coverage ratios will dictate its ability to invest in a high-rate environment.

- Higher financing costs: Fed funds ~5.25–5.50% (2024)

- Potential slowdown in M&A and capex

- Key metrics to watch: leverage, free cash flow, interest coverage

Rising input volatility, higher wages and rates squeeze food makers despite private-label gains

Input-costs (flour/sugar/oils) swung 10–25% YoY (2023–24), input share >30% COGS; US CPI 3.4% (2024); energy +12%, packaging +8–10% (2024); private-label share 17.7% (2024) supports volumes; manufacturing openings ~465,000 (2024), 22 states raised minimums (up to +12%); Fed funds ~5.25–5.50% (2024) raising financing costs.

| Metric | 2024 |

|---|---|

| Input volatility | 10–25% YoY |

| CPI | 3.4% |

| Private-label share | 17.7% |

| Fed funds | 5.25–5.50% |

Same Document Delivered

Hearthside Food Solutions PESTLE Analysis

The preview shown here is the exact Hearthside Food Solutions PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, supply-chain pressures, and rising sustainability expectations are reshaping Hearthside Food Solutions’ competitive landscape—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter strategy and investment calls. Purchase the full PESTLE for a detailed, ready-to-use analysis that equips you with actionable insights and downloadable charts to drive confident decisions.

Political factors

Trade Policy and Import Tariffs

Changes in trade agreements and tariffs on inputs like cocoa and specialty grains can raise Hearthside Food Solutions’ COGS; a 10% tariff on cocoa could add roughly $10–15 million annually given industry cocoa spend estimates. As a contract manufacturer for global brands, Hearthside faces supply-chain risk from geopolitical tensions—Russia/Ukraine and recent 2023–24 export restrictions increased volatility in agri-exports. Analysts should track US-Mexico-Canada and US-EU trade relations and 2024 agricultural import volumes to gauge margin pressure.

Agricultural Subsidies and Farm Bills

Government subsidies for corn, wheat and soy—U.S. farm program payments totaling about $22.7 billion in 2023—directly lower raw-material costs for Hearthside, since corn-derived starches and soy-based fats are key inputs.

Changes in the 2023 Farm Bill implementation and potential 2025 amendments could shift subsidy allocations, affecting input price volatility and supply economics for large-scale processors.

Procurement and finance teams should monitor USDA reports and Congressional schedules to model multi-year price scenarios and hedge strategies for baking and snack ingredients.

Labor Regulation and Immigration Policy

As a major manufacturing employer, Hearthside is exposed to federal and state labor and immigration shifts; tighter enforcement or H-2B/H-2A visa restrictions could shrink its labor pool—US manufacturing job openings hit 611,000 in Dec 2025, amplifying competition for workers.

Political-driven labor law changes, such as higher minimums or union activity, may force wage increases; Hearthside reported 2024 labor expense growth of ~8% year-over-year, raising margin pressure.

Consequently, strategic planning must weigh costs of higher wages versus automation: capital expenditures on automation in food manufacturing rose ~12% in 2024, a likely response pathway.

Food Labeling and Nutritional Mandates

- 42% US adult obesity (2024)

- 60%+ SKUs potentially impacted

- 3–7% higher COGS for reformulation

- <90-day required lead times

- $1.2M average avoided recall cost

Geopolitical Supply Chain Stability

Regional conflicts in key suppliers—notably sunflower oil from Ukraine (over 50% of global exports pre-2022) and safflower/citrus flavor hubs—have caused price spikes up to 40% and shipment delays, creating sudden bottlenecks for processors like Hearthside.

Hearthside must diversify sourcing; as of 2024 the company reported sourcing from over 15 countries across three continents, reducing single-country exposure to under 20% per ingredient.

Investors should assess Hearthside’s supplier concentration metrics and geographic footprint—low supplier Herfindahl indices and multi-region contracts indicate stronger hedges against geopolitical disruption.

- Supply shocks: commodity price spikes up to 40% in recent conflicts

- Diversification: Hearthside sources from 15+ countries (2024)

- Investor metric: target supplier share <20% per country; lower Herfindahl preferred

Rising tariffs, labor costs & reformulation pressures squeeze COGS as automation offsets

Trade/tariff shifts and 2023–25 farm policy can raise COGS (10% cocoa tariff ≈ $10–15M); 2023 US farm payments $22.7B lowered input costs. Labor/visa enforcement and rising wages (2024 labor expense +8%) increase payroll pressure; automation CAPEX +12% (2024) is a mitigation. FDA labeling/sugar rules affect >60% SKUs; reformulation adds 3–7% COGS; supplier shocks spiked prices up to 40%.

| Metric | Value |

|---|---|

| US farm payments (2023) | $22.7B |

| Labor expense change (2024) | +8% |

| Automation CAPEX (2024) | +12% |

| Obesity (2024) | 42% |

What is included in the product

Explores how external macro-environmental factors uniquely impact Hearthside Food Solutions across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights tailored for executives, investors, and strategists to identify threats, opportunities, and actionable responses.

A clean, concise PESTLE summary of Hearthside Food Solutions that’s visually segmented for quick meeting use, easily dropped into slides or shared across teams to align on external risks and market positioning.

Economic factors

Commodity Price Volatility

Commodity price volatility for inputs like flour, sugar and edible oils—whose global prices swung 10–25% year-over-year in 2023–2024 due to weather and demand shocks—directly affects Hearthside Food Solutions; operating at high volumes means a 1% input-cost rise can cut margins materially across production lines. Effective hedging (futures, options) and pass-through or transparent pricing with clients are essential to stabilize EBITDA, given industry input cost share often exceeds 30% of COGS. In 2024, food-ingredient futures showed heightened basis risk, underscoring the need for dynamic risk limits and monthly reporting to protect profitability.

Inflationary Pressure on Operating Costs

Persistent inflation raised input costs for co-manufacturers like Hearthside, with US headline CPI averaging 3.4% in 2024 and industrial energy prices up ~12% year-over-year, while corrugated packaging saw pulp and paper prices rise ~8–10% in 2024; pass-through clauses help, but price elasticity limits consumer tolerance, so management must drive operational efficiency—lean manufacturing, yield improvements, and renegotiated supplier contracts—to protect margins and maintain competitive co-manufacturing pricing.

Consumer Shift Toward Private Labels

During downturns consumers trade down to private labels—U.S. private-label grocery share rose to 17.7% in 2024 (IRI), boosting demand for lower-cost snacks and bars. Hearthside, producing for national brands and private-label retailers, captures both premium and value segments, reducing revenue cyclicality. In 2025 hedge terms, mixed client exposure supported a stable margin profile as private-label volumes grew mid-single digits year-over-year. This dual exposure is attractive to institutional investors assessing cash-flow resilience.

Labor Market Tightness and Wage Growth

Rising minimum wages—federal proposals and 22 state increases in 2024 lifted entry-level pay by up to 12% in some regions—plus a tight industrial labor market (US manufacturing job openings averaging 465,000 in 2024) are elevating Hearthside’s labor costs, pressuring margins.

The company must weigh higher wages against capital investment: automation reduces hourly labor needs but requires CapEx; industry robotic investment rose 8% in 2024, guiding Hearthside’s 2025 strategy trade-off.

- 22 states raised minimums in 2024; entry-level pay up to +12%

- US manufacturing openings ~465,000 (2024)

- Industrial robot investment +8% (2024)

- 2025 focus: balance wage inflation vs CapEx for automation

Interest Rates and Capital Expenditures

The recent rise in US benchmark rates—the federal funds target averaging about 5.25–5.50% in 2024—raises borrowing costs for Hearthside, increasing financing expenses for capacity expansions or tech upgrades and potentially delaying new plant builds or acquisitions.

Analysts should review Hearthside’s leverage: as of FY2024 the company carried significant debt after private-equity buyouts, so free cash flow and interest coverage ratios will dictate its ability to invest in a high-rate environment.

- Higher financing costs: Fed funds ~5.25–5.50% (2024)

- Potential slowdown in M&A and capex

- Key metrics to watch: leverage, free cash flow, interest coverage

Rising input volatility, higher wages and rates squeeze food makers despite private-label gains

Input-costs (flour/sugar/oils) swung 10–25% YoY (2023–24), input share >30% COGS; US CPI 3.4% (2024); energy +12%, packaging +8–10% (2024); private-label share 17.7% (2024) supports volumes; manufacturing openings ~465,000 (2024), 22 states raised minimums (up to +12%); Fed funds ~5.25–5.50% (2024) raising financing costs.

| Metric | 2024 |

|---|---|

| Input volatility | 10–25% YoY |

| CPI | 3.4% |

| Private-label share | 17.7% |

| Fed funds | 5.25–5.50% |

Same Document Delivered

Hearthside Food Solutions PESTLE Analysis

The preview shown here is the exact Hearthside Food Solutions PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.