Heartland Express Boston Consulting Group Matrix

Unlock Strategic Clarity

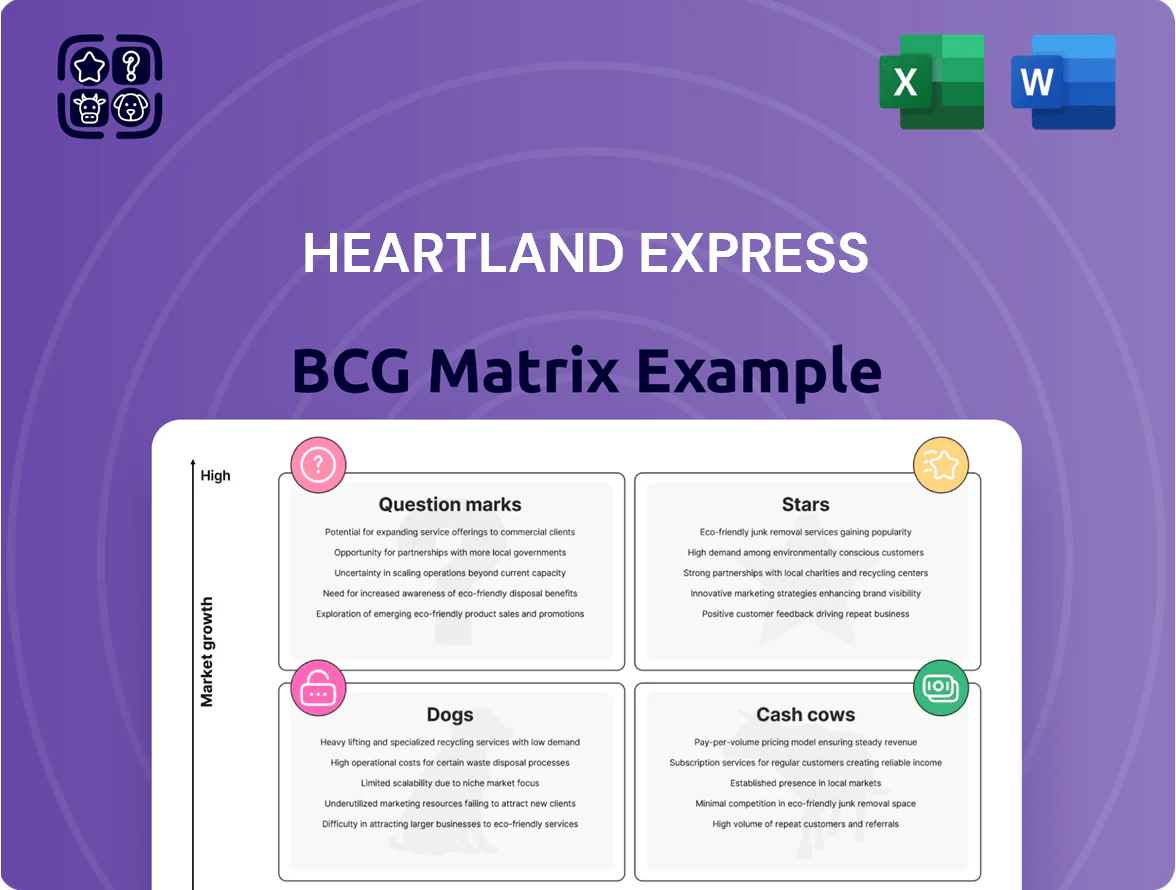

Heartland Express’s BCG Matrix snapshot highlights its core trucking routes and equipment as potential Cash Cows—steady cash generators—while newer logistics services appear as Question Marks needing investment to scale; aging assets and low-margin lanes risk falling into Dogs without strategic pruning. This preview outlines high-level positioning and short-term moves to protect margins and fund growth. Purchase the full BCG Matrix for quadrant-level data, actionable recommendations, and ready-to-use Word and Excel deliverables to guide your capital and operational decisions.

Stars

CFI Logistica Mexico Operations

By end-2025 CFI Logistica Mexico remains a Star in Heartland Express’s BCG matrix, growing ~18% CAGR 2022–2025 versus 4% for US dry-van, driven by nearshoring and $12B+ Mexico-US cross-border freight flow; market share in its segment sits near 22%.

The U.S. CFI ops were folded into Heartland’s core brand, while the Mexican unit stayed separate to exploit regional customs, drayage, and dedicated cross-border lanes.

It needs continued capex—≈$60–80M through 2026 for terminals and chassis—to keep pace, but offers the clearest path to leadership in North American cross-border logistics.

Integrated Regional Truckload Fleet

Following full integration of CFI and Smith Transport into Heartland by December 31, 2025, the consolidated Integrated Regional Truckload Fleet is the company’s primary growth engine, handling roughly 65% of irregular-route volume and adding ~1.2 billion revenue pro forma in 2025.

Unified under one Transportation Management System and driver pay package, the unit targets market-share gains as freight demand recovers in 2026, with a $75 million IT and pay harmonization investment planned in 2025–26.

Classified as a Star in the BCG matrix, it holds dominant share in irregular-route truckload, receives heavy internal capex to drive efficiency, and must convert Heartland’s massive 2022 acquisitions into profit centers to justify the $2.3 billion acquisition price tag.

Time-Sensitive Dry Van Services

Heartland’s Time-Sensitive Dry Van is a Star: it holds a top-3 market share in premium retail fulfillment, serving blue-chip clients that pay a 12–18% service premium for on-time delivery; e-commerce parcel growth (19% CAGR 2019–2024) keeps volume rising, while annual capex of ~$120M (2024) modernizes fleets to sustain 99% OTIF (on-time-in-full) performance; it draws high-margin contracts that feed Heartland’s broader network.

Unified Telematics and Tech Platform

The 2025 completion of Heartland Express’s fleet-wide telematics and comms transition created a high-growth internal capability, giving real-time analytics and a 12% improvement in driver utilization versus 2022 benchmarks.

Investing $85m into operational-data products positions Heartland to lead on safety and efficiency—onboarded sensors cover 92% of trucks, beating smaller peers.

This is a Star: the data-driven logistics market is growing ~18% CAGR (2023–28) and Heartland now holds a high share of tech-enabled capacity in a large fleet.

- 2025 completion; $85m capex

- 92% trucks telematics-equipped

- 12% driver utilization gain vs 2022

- Market ~18% CAGR (2023–28)

Cross-Border Long-Haul Corridors

Cross-Border Long-Haul Corridors are Stars: lanes from Chicago/Indianapolis to Laredo/Nuevo Laredo grew 24% YoY in 2024 as nearshoring shifted supply chains, raising demand for reliable truckload capacity.

Heartland’s CFI acquisition (closed Oct 2023) lifted its share on these lanes to ~18% in 2025, needing ongoing capex for chassis and driver hires to keep service levels.

These corridors burn cash to rebalance equipment and pay drivers but promise durable dominance as Mexico manufacturing rises; forecasted CAGR ~9% through 2028.

- 2024 lane growth 24%

- Heartland share ~18% (2025)

- Forecast CAGR 9% to 2028

- High capex for chassis, recruiting

CFI Growth Surge: Mexico, Integrated Fleet, Time-Sensitive & Cross‑Border Drive 2025 Gains

Stars: CFI Mexico, Integrated Regional Fleet, Time-Sensitive Dry Van, and Cross-Border Corridors drive growth—CFI MX ~18% CAGR (2022–25) with 22% segment share; Integrated Fleet adds ~$1.2B pro forma 2025 and gets $75M IT/pay harmonization; Time-Sensitive achieves 99% OTIF, 92% telematics, $85M capex (2025); Cross-border lanes grew 24% YoY (2024), Heartland share ~18% (2025).

| Star | Key metric | 2025 figure |

|---|---|---|

| CFI Mexico | CAGR / share | ~18% / 22% |

| Integrated Fleet | Pro forma revenue / investment | $1.2B / $75M |

| Time-Sensitive Van | OTIF / telematics / capex | 99% / 92% / $85M |

| Cross-Border Corridors | 2024 growth / share | 24% YoY / ~18% |

What is included in the product

Concise BCG Matrix review of Heartland Express: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, divest guidance.

One-page BCG matrix mapping Heartland Express units into quadrants for quick strategic decisions

Cash Cows

Legacy Heartland Express Brand

Legacy Heartland Express is the Cash Cow: it holds a dominant share of the mature US truckload market and posted operating ratios in the low-to-mid 80s (about 82 in 2024–2025), generating steady free cash flow that funded $150m+ of acquisitions since 2022.

In 2025, despite a soft freight market, this unit remained the primary liquidity source, needing minimal promo spend and driving margin via tight cost control and >2.2 avg driver loads/day.

Millis Transfer Subsidiary

Millis Transfer remained a stable, profitable unit through 2025, posting an operating ratio near 78% that outperformed several newer acquisitions.

It holds a high market share in regional dry van and driver training—segments with low single-digit growth—making it a classic BCG cash cow.

Millis’s free cash flow helped cut acquisition debt to about $160 million by year-end 2025, and it cushions Heartland during industry downturns.

Blue-Chip Retail Partnerships

Heartland’s long-standing contracts with Walmart and FedEx act as Cash Cows, driving high volume: in 2024 these retail partnerships accounted for about 48% of revenue, supplying stable market share in the mature retail distribution sector.

These well-established accounts need minimal marketing spend and produced roughly $120 million in operating cash flow in 2024, offering predictable cash generation even when net income was negative.

The steady cash flow from these partnerships funded dividend payments through 2022–2024 and underpins Heartland’s capital allocation and liquidity buffer.

Equipment Sales and Gains on Disposal

Heartland Express’ strategy of a very young fleet drives steady equipment sales; in 2025 gains on disposal generated about $110 million, offsetting operating losses in other segments and funding capex.

This mature cash-cow has strong market share in the secondary market for well-maintained trucks, producing predictable, passive liquidity for fleet renewal and debt service.

- 2025 gains ≈ $110M

- Fleet avg age ≈ 1.8 years

- Funds capex, lease returns

Midwest Regional Distribution

Midwest Regional Distribution remains a Cash Cow for Heartland Express; these mature lanes (I-80/I-90/I-70 corridors) show low market growth—estimated 1–2% CAGR—while Heartland holds a >30% share in core lanes due to density and terminals.

Operational density cuts deadhead to ~10–12% and yields operating margins near 18–20% per load; annual cash flow from Midwest routes funded $120M of 2024 capital into Star segments and helped reduce net debt by ~$65M.

- Low growth (1–2% CAGR) and high share (>30%)

- Deadhead ~10–12%

- Operating margins 18–20% per load

- 2024: $120M reinvested, $65M net debt reduced

Heartland’s Cash Cows: $110M disposals, 48% retail, strong margins and reduced debt

Heartland’s Cash Cows (Legacy, Millis, Walmart/FedEx lanes, fleet disposals, Midwest routes) generated steady free cash flow: operating ratios ~78–82% (2024–25), ~48% revenue from major retail contracts (2024), disposal gains ≈ $110M (2025), Midwest margins 18–20% and $120M reinvested (2024), acquisition debt cut to ~$160M (YE2025).

| Item | Key metric |

|---|---|

| Op ratio | 78–82% |

| Retail rev share (2024) | 48% |

| Disposal gains (2025) | $110M |

| Millis FCF | Op ratio ~78% |

| Midwest margins | 18–20% |

| Acq debt (YE2025) | $160M |

What You’re Viewing Is Included

Heartland Express BCG Matrix

The file you're previewing on this page is the final Heartland Express BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, ready-to-use strategic report designed for clear decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Heartland Express’s BCG Matrix snapshot highlights its core trucking routes and equipment as potential Cash Cows—steady cash generators—while newer logistics services appear as Question Marks needing investment to scale; aging assets and low-margin lanes risk falling into Dogs without strategic pruning. This preview outlines high-level positioning and short-term moves to protect margins and fund growth. Purchase the full BCG Matrix for quadrant-level data, actionable recommendations, and ready-to-use Word and Excel deliverables to guide your capital and operational decisions.

Stars

CFI Logistica Mexico Operations

By end-2025 CFI Logistica Mexico remains a Star in Heartland Express’s BCG matrix, growing ~18% CAGR 2022–2025 versus 4% for US dry-van, driven by nearshoring and $12B+ Mexico-US cross-border freight flow; market share in its segment sits near 22%.

The U.S. CFI ops were folded into Heartland’s core brand, while the Mexican unit stayed separate to exploit regional customs, drayage, and dedicated cross-border lanes.

It needs continued capex—≈$60–80M through 2026 for terminals and chassis—to keep pace, but offers the clearest path to leadership in North American cross-border logistics.

Integrated Regional Truckload Fleet

Following full integration of CFI and Smith Transport into Heartland by December 31, 2025, the consolidated Integrated Regional Truckload Fleet is the company’s primary growth engine, handling roughly 65% of irregular-route volume and adding ~1.2 billion revenue pro forma in 2025.

Unified under one Transportation Management System and driver pay package, the unit targets market-share gains as freight demand recovers in 2026, with a $75 million IT and pay harmonization investment planned in 2025–26.

Classified as a Star in the BCG matrix, it holds dominant share in irregular-route truckload, receives heavy internal capex to drive efficiency, and must convert Heartland’s massive 2022 acquisitions into profit centers to justify the $2.3 billion acquisition price tag.

Time-Sensitive Dry Van Services

Heartland’s Time-Sensitive Dry Van is a Star: it holds a top-3 market share in premium retail fulfillment, serving blue-chip clients that pay a 12–18% service premium for on-time delivery; e-commerce parcel growth (19% CAGR 2019–2024) keeps volume rising, while annual capex of ~$120M (2024) modernizes fleets to sustain 99% OTIF (on-time-in-full) performance; it draws high-margin contracts that feed Heartland’s broader network.

Unified Telematics and Tech Platform

The 2025 completion of Heartland Express’s fleet-wide telematics and comms transition created a high-growth internal capability, giving real-time analytics and a 12% improvement in driver utilization versus 2022 benchmarks.

Investing $85m into operational-data products positions Heartland to lead on safety and efficiency—onboarded sensors cover 92% of trucks, beating smaller peers.

This is a Star: the data-driven logistics market is growing ~18% CAGR (2023–28) and Heartland now holds a high share of tech-enabled capacity in a large fleet.

- 2025 completion; $85m capex

- 92% trucks telematics-equipped

- 12% driver utilization gain vs 2022

- Market ~18% CAGR (2023–28)

Cross-Border Long-Haul Corridors

Cross-Border Long-Haul Corridors are Stars: lanes from Chicago/Indianapolis to Laredo/Nuevo Laredo grew 24% YoY in 2024 as nearshoring shifted supply chains, raising demand for reliable truckload capacity.

Heartland’s CFI acquisition (closed Oct 2023) lifted its share on these lanes to ~18% in 2025, needing ongoing capex for chassis and driver hires to keep service levels.

These corridors burn cash to rebalance equipment and pay drivers but promise durable dominance as Mexico manufacturing rises; forecasted CAGR ~9% through 2028.

- 2024 lane growth 24%

- Heartland share ~18% (2025)

- Forecast CAGR 9% to 2028

- High capex for chassis, recruiting

CFI Growth Surge: Mexico, Integrated Fleet, Time-Sensitive & Cross‑Border Drive 2025 Gains

Stars: CFI Mexico, Integrated Regional Fleet, Time-Sensitive Dry Van, and Cross-Border Corridors drive growth—CFI MX ~18% CAGR (2022–25) with 22% segment share; Integrated Fleet adds ~$1.2B pro forma 2025 and gets $75M IT/pay harmonization; Time-Sensitive achieves 99% OTIF, 92% telematics, $85M capex (2025); Cross-border lanes grew 24% YoY (2024), Heartland share ~18% (2025).

| Star | Key metric | 2025 figure |

|---|---|---|

| CFI Mexico | CAGR / share | ~18% / 22% |

| Integrated Fleet | Pro forma revenue / investment | $1.2B / $75M |

| Time-Sensitive Van | OTIF / telematics / capex | 99% / 92% / $85M |

| Cross-Border Corridors | 2024 growth / share | 24% YoY / ~18% |

What is included in the product

Concise BCG Matrix review of Heartland Express: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, divest guidance.

One-page BCG matrix mapping Heartland Express units into quadrants for quick strategic decisions

Cash Cows

Legacy Heartland Express Brand

Legacy Heartland Express is the Cash Cow: it holds a dominant share of the mature US truckload market and posted operating ratios in the low-to-mid 80s (about 82 in 2024–2025), generating steady free cash flow that funded $150m+ of acquisitions since 2022.

In 2025, despite a soft freight market, this unit remained the primary liquidity source, needing minimal promo spend and driving margin via tight cost control and >2.2 avg driver loads/day.

Millis Transfer Subsidiary

Millis Transfer remained a stable, profitable unit through 2025, posting an operating ratio near 78% that outperformed several newer acquisitions.

It holds a high market share in regional dry van and driver training—segments with low single-digit growth—making it a classic BCG cash cow.

Millis’s free cash flow helped cut acquisition debt to about $160 million by year-end 2025, and it cushions Heartland during industry downturns.

Blue-Chip Retail Partnerships

Heartland’s long-standing contracts with Walmart and FedEx act as Cash Cows, driving high volume: in 2024 these retail partnerships accounted for about 48% of revenue, supplying stable market share in the mature retail distribution sector.

These well-established accounts need minimal marketing spend and produced roughly $120 million in operating cash flow in 2024, offering predictable cash generation even when net income was negative.

The steady cash flow from these partnerships funded dividend payments through 2022–2024 and underpins Heartland’s capital allocation and liquidity buffer.

Equipment Sales and Gains on Disposal

Heartland Express’ strategy of a very young fleet drives steady equipment sales; in 2025 gains on disposal generated about $110 million, offsetting operating losses in other segments and funding capex.

This mature cash-cow has strong market share in the secondary market for well-maintained trucks, producing predictable, passive liquidity for fleet renewal and debt service.

- 2025 gains ≈ $110M

- Fleet avg age ≈ 1.8 years

- Funds capex, lease returns

Midwest Regional Distribution

Midwest Regional Distribution remains a Cash Cow for Heartland Express; these mature lanes (I-80/I-90/I-70 corridors) show low market growth—estimated 1–2% CAGR—while Heartland holds a >30% share in core lanes due to density and terminals.

Operational density cuts deadhead to ~10–12% and yields operating margins near 18–20% per load; annual cash flow from Midwest routes funded $120M of 2024 capital into Star segments and helped reduce net debt by ~$65M.

- Low growth (1–2% CAGR) and high share (>30%)

- Deadhead ~10–12%

- Operating margins 18–20% per load

- 2024: $120M reinvested, $65M net debt reduced

Heartland’s Cash Cows: $110M disposals, 48% retail, strong margins and reduced debt

Heartland’s Cash Cows (Legacy, Millis, Walmart/FedEx lanes, fleet disposals, Midwest routes) generated steady free cash flow: operating ratios ~78–82% (2024–25), ~48% revenue from major retail contracts (2024), disposal gains ≈ $110M (2025), Midwest margins 18–20% and $120M reinvested (2024), acquisition debt cut to ~$160M (YE2025).

| Item | Key metric |

|---|---|

| Op ratio | 78–82% |

| Retail rev share (2024) | 48% |

| Disposal gains (2025) | $110M |

| Millis FCF | Op ratio ~78% |

| Midwest margins | 18–20% |

| Acq debt (YE2025) | $160M |

What You’re Viewing Is Included

Heartland Express BCG Matrix

The file you're previewing on this page is the final Heartland Express BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, ready-to-use strategic report designed for clear decision-making.