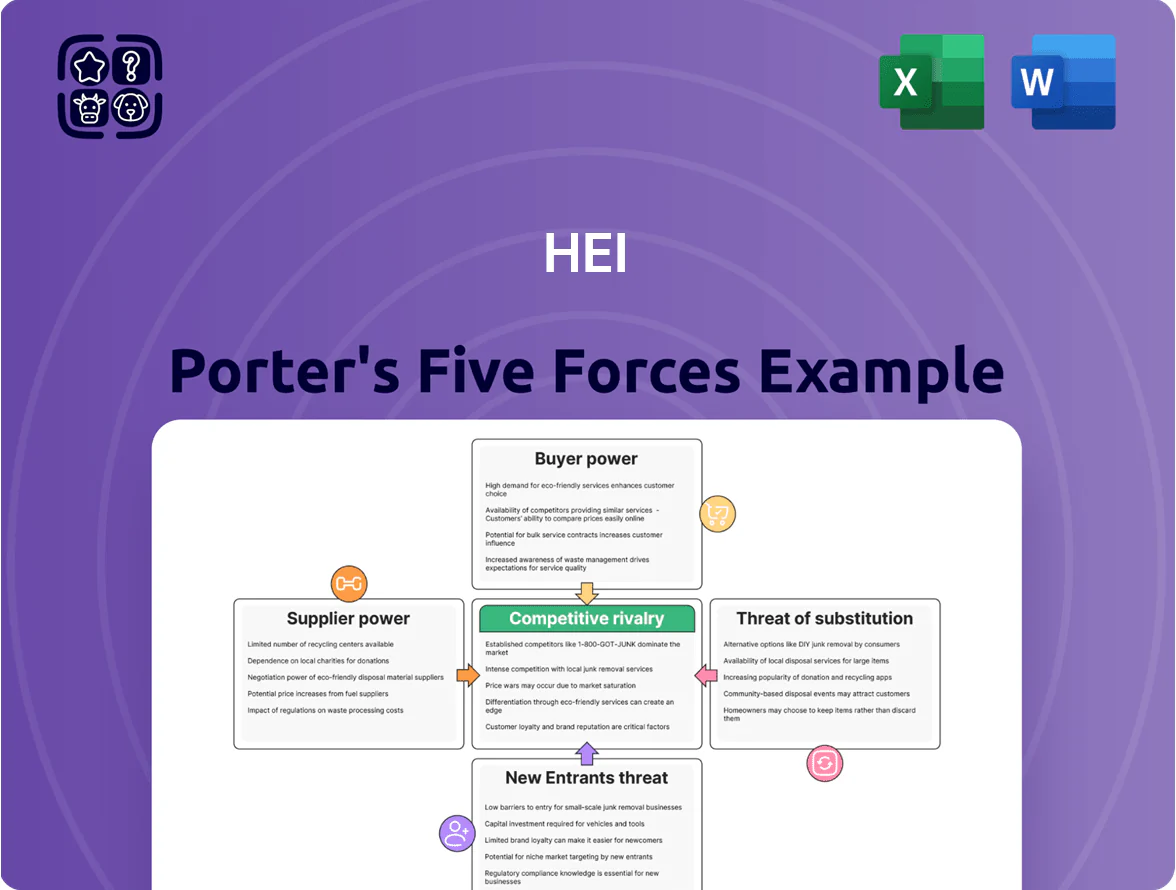

HEI Porter's Five Forces Analysis

Don't Miss the Bigger Picture

HEI faces moderate buyer power, concentrated supplier dynamics, and evolving substitute threats driven by technology and regulatory shifts; competitive rivalry is steady but ripe for disruption.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore HEI’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Heavy reliance on specialized renewable energy technology providers

HEI’s push to meet Hawaii’s 2045 100% renewable goal makes it dependent on a few global suppliers for utility‑scale battery storage and PV components; in 2024 Hawaii added ~150 MW of battery capacity but needs several GW more, so vendors hold leverage.

High technical specs for island grid stability raise switching costs; firms like Tesla and Fluence, which supplied ~60–70% of recent U.S. battery deployments, concentrate expertise, leaving HEI limited options and weaker bargaining power.

Volatility in imported fuel and purchased power agreements

HEI still depends on imported oil and IPPs for ~20–30% of generation; imported oil prices rose ~45% 2021–2024, increasing fuel cost risk for HEI.

Long-term IPP PPAs often include inflation escalators (CPI-linked), locking HEI into rising payments—IPP capacity contracts cover roughly 25% of peak demand.

That gives suppliers pricing power over core inputs, forcing HEI to hedge, renegotiate, or pass costs to customers; in 2024 fuel & PPA costs represented ~28% of operating expenses.

Shortage of skilled labor and specialized utility contractors

The Hawaii labor market is tight due to isolation, so specialized electrical and utility unions have high bargaining power; HEI (Hawaiian Electric Industries) competes for niche grid engineers and contractors amid a 2024 statewide unemployment rate of ~2.3%, lifting wage premiums 10–20% above US averages for skilled trades.

Limited availability of capital from risk-averse financial markets

Following the 2023 Maui wildfires, credit ratings and insurers raised HEI's cost of capital—Moody’s placed Hawaiian Electric on negative watch in 2023 and insurers pushed premiums up ~20–40%, forcing higher debt yields for funding rebuilds.

When agencies and insurers view elevated ESG or litigation risk, they demand higher interest and premium rates, directly lifting financing costs and squeezing HEI's margins.

- Credit watch: Moody’s negative watch 2023

- Insurance premium rise: ~20–40%

- Higher debt yields: increases HEI financing costs

Constraint on physical land and resource availability

Landowners in Hawaii control scarce usable land for solar and wind projects, forcing Hawaiian Electric Industries (HEI) to negotiate with a few private estates and agencies; Hawaii has less than 1% of land classified as high-solar potential and utility-scale sites are often on leased agricultural or conservation parcels.

That concentration lets suppliers demand high lease rates—reported parcel rents in 2024 reached up to $3,000–$6,000 per acre-year for coastal usable sites—and impose strict environmental and cultural conditions tied to NHPA and state rules.

As a result, HEI faces higher upfront site costs and project delays; a 2023 state study estimated land-related permitting and mitigation can add 10–18% to project capital costs and extend timelines by 12–30 months.

- Few suppliers: private estates + state/federal agencies

- High rents: $3,000–$6,000 per acre-year (2024 examples)

- Added costs: +10–18% capex, +12–30 months delays (2023 study)

Suppliers Squeeze HEI: Limited Battery, Rising Fuel, Land & Insurance Costs Force Tough Choices

Suppliers hold strong leverage over HEI: critical battery/PV vendors (Tesla, Fluence) and few landowners limit alternatives, while IPP PPAs and imported oil raise input-cost exposure; 2024 figures—battery add ~150 MW vs multi-GW need, fuel & PPA costs ~28% OPEX, land rents $3k–$6k/acre‑yr, insurers +20–40% premiums—force hedging, renegotiation, or rate hikes.

| Metric | 2024 value |

|---|---|

| Battery additions | ~150 MW |

| Fuel & PPA share of OPEX | ~28% |

| Land rents (usable sites) | $3,000–$6,000/acre‑yr |

| Insurance premium rise | ~20–40% |

| Unemployment rate (HI) | ~2.3% |

What is included in the product

Tailored Porter’s Five Forces analysis for HEI that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats to inform strategic decisions and investor materials.

A single-sheet Porter's Five Forces summary that quantifies competitive pressure and highlights strategic levers—ideal for rapid decision-making and slide-ready presentations.

Customers Bargaining Power

Regulatory oversight by the Public Utilities Commission

The Hawaii Public Utilities Commission (PUC) serves as a proxy for residential and commercial customers, tightly regulating Hawaiian Electric Industries (HEI) rates and constraining monopoly pricing power. In 2024 the PUC approved average rate increases of about 2.1% vs HEI’s requested 4.5%, showing customers’ collective leverage in practice. Rate-change petitions face exhaustive hearings and cost-recovery tests, often lowering HEI’s allowed returns on equity and protecting consumer bills. This regulatory oversight makes customer bargaining power effectively strong and institutionalized.

Rapid adoption of residential rooftop solar systems

Hawaii has ~35% household rooftop solar penetration as of 2024, so many customers can self-generate and cut purchases from Hawaiian Electric Industries (HEI), reducing utility sales and margin. This high adoption lowers HEI’s bargaining power since customers face lower switching costs and can use net metering to monetize excess generation. Falling battery costs—pack prices down ~60% since 2015 to ~$120/kWh in 2024—raise the chance of full grid defection, increasing customer leverage.

High sensitivity to electricity rates among low-income residents

Hawaii’s average retail electricity price was about 0.44 USD/kWh in 2024, the highest in the US, so low-income households are extremely price-sensitive and react quickly to rate increases.

This sensitivity creates strong political pressure on Hawaiian Electric Industries (HEI) to keep rates affordable while funding grid upgrades—HEI faces scrutiny over proposed rate hikes tied to ~$1.5–2.0 billion decarbonization investments through 2030.

Large commercial customers push back as well; several firms have signaled plans for on-site generation or microgrids if utility costs rise, increasing customer bargaining leverage.

Community and environmental advocacy group influence

Local communities and environmental NGOs exert strong influence on HEI project approvals; 2024 Hawaii polling showed 62% oppose new high-impact developments without cultural safeguards, and 4 litigation cases since 2021 delayed $320M in planned capital spending.

Customer sentiment on land use, cultural preservation, and environmental harm has halted projects via public hearings and lawsuits, giving communities de facto veto power over timelines and costs.

The social license to operate forces HEI to factor community demands into strategy, raising mitigation costs and prolonging approval cycles by 12–24 months on average.

- 62% public opposition (2024 Hawaii poll)

- $320M delayed capex from 4 lawsuits (2021–2024)

- Approval delays typically 12–24 months

Banking customer mobility in the financial services sector

HEI, via American Savings Bank, faces high customer mobility: low switching costs let depositors move to national banks or fintechs; FDIC data (2024) shows online savings rates ranged 0.50–4.50%, so yield-seeking customers can exit quickly.

High 2023–2025 interest rates raised customer demand for competitive yields and digital-first services, forcing HEI to keep service and tech investments high while local credit unions and banks in Hawaii offer many close alternatives.

- Low switching costs → easy deposit outflows

- Online savings rates 0.50–4.50% (2024)

- Higher rates (2023–25) increased yield pressure

- Numerous Hawaii credit unions/local banks

PUC, rooftop solar and protests cap HEI rate hikes amid high prices and project risk

Regulatory oversight (PUC) and high rooftop solar (~35% 2024) give customers institutional and practical leverage, constraining HEI rate requests (PUC approved ~2.1% vs requested 4.5% in 2024). High retail price (~$0.44/kWh 2024), vocal communities (62% oppose high-impact projects 2024) and lawsuits ($320M delayed capex 2021–24) raise political and project risk; large users and banks (online rates 0.50–4.50% 2024) can switch, keeping bargaining power high.

| Metric | Value |

|---|---|

| PUC 2024 rate approval | ~2.1% (vs 4.5% request) |

| Rooftop solar | ~35% households (2024) |

| Retail price | $0.44/kWh (2024) |

| Public opposition | 62% (2024 poll) |

| Delayed capex | $320M (2021–24) |

| Battery pack price | ~$120/kWh (2024) |

| Online savings range | 0.50–4.50% (2024) |

Preview Before You Purchase

HEI Porter's Five Forces Analysis

This preview shows the exact HEI Porter's Five Forces analysis document you'll receive immediately after purchase—no surprises, no placeholders.

The file displayed is the complete, professionally formatted analysis, ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

HEI faces moderate buyer power, concentrated supplier dynamics, and evolving substitute threats driven by technology and regulatory shifts; competitive rivalry is steady but ripe for disruption.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore HEI’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Heavy reliance on specialized renewable energy technology providers

HEI’s push to meet Hawaii’s 2045 100% renewable goal makes it dependent on a few global suppliers for utility‑scale battery storage and PV components; in 2024 Hawaii added ~150 MW of battery capacity but needs several GW more, so vendors hold leverage.

High technical specs for island grid stability raise switching costs; firms like Tesla and Fluence, which supplied ~60–70% of recent U.S. battery deployments, concentrate expertise, leaving HEI limited options and weaker bargaining power.

Volatility in imported fuel and purchased power agreements

HEI still depends on imported oil and IPPs for ~20–30% of generation; imported oil prices rose ~45% 2021–2024, increasing fuel cost risk for HEI.

Long-term IPP PPAs often include inflation escalators (CPI-linked), locking HEI into rising payments—IPP capacity contracts cover roughly 25% of peak demand.

That gives suppliers pricing power over core inputs, forcing HEI to hedge, renegotiate, or pass costs to customers; in 2024 fuel & PPA costs represented ~28% of operating expenses.

Shortage of skilled labor and specialized utility contractors

The Hawaii labor market is tight due to isolation, so specialized electrical and utility unions have high bargaining power; HEI (Hawaiian Electric Industries) competes for niche grid engineers and contractors amid a 2024 statewide unemployment rate of ~2.3%, lifting wage premiums 10–20% above US averages for skilled trades.

Limited availability of capital from risk-averse financial markets

Following the 2023 Maui wildfires, credit ratings and insurers raised HEI's cost of capital—Moody’s placed Hawaiian Electric on negative watch in 2023 and insurers pushed premiums up ~20–40%, forcing higher debt yields for funding rebuilds.

When agencies and insurers view elevated ESG or litigation risk, they demand higher interest and premium rates, directly lifting financing costs and squeezing HEI's margins.

- Credit watch: Moody’s negative watch 2023

- Insurance premium rise: ~20–40%

- Higher debt yields: increases HEI financing costs

Constraint on physical land and resource availability

Landowners in Hawaii control scarce usable land for solar and wind projects, forcing Hawaiian Electric Industries (HEI) to negotiate with a few private estates and agencies; Hawaii has less than 1% of land classified as high-solar potential and utility-scale sites are often on leased agricultural or conservation parcels.

That concentration lets suppliers demand high lease rates—reported parcel rents in 2024 reached up to $3,000–$6,000 per acre-year for coastal usable sites—and impose strict environmental and cultural conditions tied to NHPA and state rules.

As a result, HEI faces higher upfront site costs and project delays; a 2023 state study estimated land-related permitting and mitigation can add 10–18% to project capital costs and extend timelines by 12–30 months.

- Few suppliers: private estates + state/federal agencies

- High rents: $3,000–$6,000 per acre-year (2024 examples)

- Added costs: +10–18% capex, +12–30 months delays (2023 study)

Suppliers Squeeze HEI: Limited Battery, Rising Fuel, Land & Insurance Costs Force Tough Choices

Suppliers hold strong leverage over HEI: critical battery/PV vendors (Tesla, Fluence) and few landowners limit alternatives, while IPP PPAs and imported oil raise input-cost exposure; 2024 figures—battery add ~150 MW vs multi-GW need, fuel & PPA costs ~28% OPEX, land rents $3k–$6k/acre‑yr, insurers +20–40% premiums—force hedging, renegotiation, or rate hikes.

| Metric | 2024 value |

|---|---|

| Battery additions | ~150 MW |

| Fuel & PPA share of OPEX | ~28% |

| Land rents (usable sites) | $3,000–$6,000/acre‑yr |

| Insurance premium rise | ~20–40% |

| Unemployment rate (HI) | ~2.3% |

What is included in the product

Tailored Porter’s Five Forces analysis for HEI that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats to inform strategic decisions and investor materials.

A single-sheet Porter's Five Forces summary that quantifies competitive pressure and highlights strategic levers—ideal for rapid decision-making and slide-ready presentations.

Customers Bargaining Power

Regulatory oversight by the Public Utilities Commission

The Hawaii Public Utilities Commission (PUC) serves as a proxy for residential and commercial customers, tightly regulating Hawaiian Electric Industries (HEI) rates and constraining monopoly pricing power. In 2024 the PUC approved average rate increases of about 2.1% vs HEI’s requested 4.5%, showing customers’ collective leverage in practice. Rate-change petitions face exhaustive hearings and cost-recovery tests, often lowering HEI’s allowed returns on equity and protecting consumer bills. This regulatory oversight makes customer bargaining power effectively strong and institutionalized.

Rapid adoption of residential rooftop solar systems

Hawaii has ~35% household rooftop solar penetration as of 2024, so many customers can self-generate and cut purchases from Hawaiian Electric Industries (HEI), reducing utility sales and margin. This high adoption lowers HEI’s bargaining power since customers face lower switching costs and can use net metering to monetize excess generation. Falling battery costs—pack prices down ~60% since 2015 to ~$120/kWh in 2024—raise the chance of full grid defection, increasing customer leverage.

High sensitivity to electricity rates among low-income residents

Hawaii’s average retail electricity price was about 0.44 USD/kWh in 2024, the highest in the US, so low-income households are extremely price-sensitive and react quickly to rate increases.

This sensitivity creates strong political pressure on Hawaiian Electric Industries (HEI) to keep rates affordable while funding grid upgrades—HEI faces scrutiny over proposed rate hikes tied to ~$1.5–2.0 billion decarbonization investments through 2030.

Large commercial customers push back as well; several firms have signaled plans for on-site generation or microgrids if utility costs rise, increasing customer bargaining leverage.

Community and environmental advocacy group influence

Local communities and environmental NGOs exert strong influence on HEI project approvals; 2024 Hawaii polling showed 62% oppose new high-impact developments without cultural safeguards, and 4 litigation cases since 2021 delayed $320M in planned capital spending.

Customer sentiment on land use, cultural preservation, and environmental harm has halted projects via public hearings and lawsuits, giving communities de facto veto power over timelines and costs.

The social license to operate forces HEI to factor community demands into strategy, raising mitigation costs and prolonging approval cycles by 12–24 months on average.

- 62% public opposition (2024 Hawaii poll)

- $320M delayed capex from 4 lawsuits (2021–2024)

- Approval delays typically 12–24 months

Banking customer mobility in the financial services sector

HEI, via American Savings Bank, faces high customer mobility: low switching costs let depositors move to national banks or fintechs; FDIC data (2024) shows online savings rates ranged 0.50–4.50%, so yield-seeking customers can exit quickly.

High 2023–2025 interest rates raised customer demand for competitive yields and digital-first services, forcing HEI to keep service and tech investments high while local credit unions and banks in Hawaii offer many close alternatives.

- Low switching costs → easy deposit outflows

- Online savings rates 0.50–4.50% (2024)

- Higher rates (2023–25) increased yield pressure

- Numerous Hawaii credit unions/local banks

PUC, rooftop solar and protests cap HEI rate hikes amid high prices and project risk

Regulatory oversight (PUC) and high rooftop solar (~35% 2024) give customers institutional and practical leverage, constraining HEI rate requests (PUC approved ~2.1% vs requested 4.5% in 2024). High retail price (~$0.44/kWh 2024), vocal communities (62% oppose high-impact projects 2024) and lawsuits ($320M delayed capex 2021–24) raise political and project risk; large users and banks (online rates 0.50–4.50% 2024) can switch, keeping bargaining power high.

| Metric | Value |

|---|---|

| PUC 2024 rate approval | ~2.1% (vs 4.5% request) |

| Rooftop solar | ~35% households (2024) |

| Retail price | $0.44/kWh (2024) |

| Public opposition | 62% (2024 poll) |

| Delayed capex | $320M (2021–24) |

| Battery pack price | ~$120/kWh (2024) |

| Online savings range | 0.50–4.50% (2024) |

Preview Before You Purchase

HEI Porter's Five Forces Analysis

This preview shows the exact HEI Porter's Five Forces analysis document you'll receive immediately after purchase—no surprises, no placeholders.

The file displayed is the complete, professionally formatted analysis, ready for download and use the moment you buy.