Heineken Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Heineken faces intense rivalry from global brewers, shifting consumer tastes toward craft and low‑alcohol options, and strong buyer power from large retailers—while supplier concentration and regulatory pressures add complexity to margin management.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Heineken’s competitive dynamics, market pressures, and strategic advantages in detail.

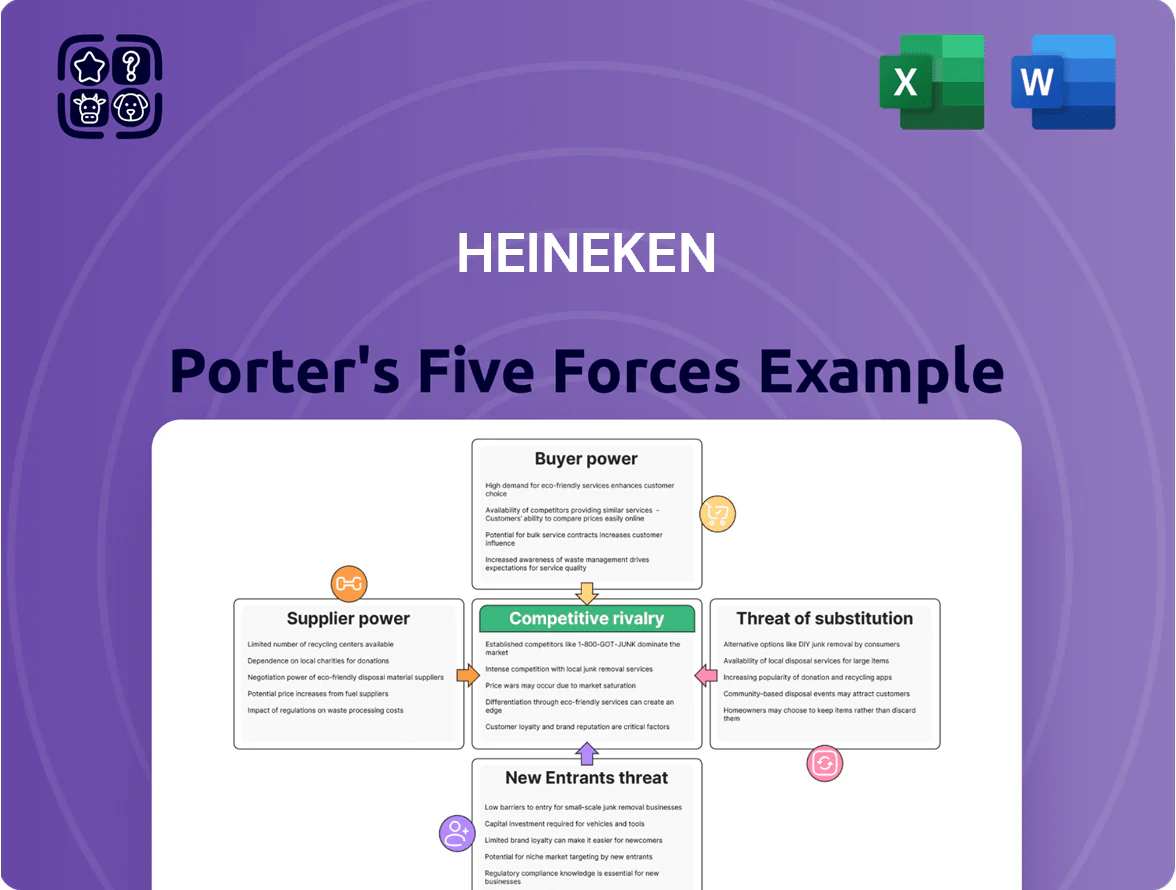

Suppliers Bargaining Power

Fragmentation of agricultural raw material providers

Heineken buys malting barley and hops from thousands of global and local farmers; these inputs are undifferentiated commodities so no single supplier wields major power. In 2024 Heineken reported procurement of ~3.1 million hectolitres worth of barley-related inputs, using scale to secure discounts and fixed-price contracts. The brewer diversifies across regions and contracts, cutting single-supplier exposure and lowering supply risk.

Volatility of packaging material costs

Heineken depends on suppliers for glass, aluminium and cardboard, exposing it to global commodity swings—glass rose 18% and aluminium 12% in 2023-24 supply cycles, pushing packaging to ~8-10% of COGS for brewers.

Heineken uses multi-year hedges and 60- to 36-month contracts to smooth costs, but a few large glass and metal firms give suppliers moderate bargaining power.

By end-2025, sustainability rules and circular-packaging specs cut the qualified supplier pool by about 25%, raising switch costs and supplier leverage.

Impact of climate change on crop yields

Suppliers of premium hops and barley face rising yield volatility from heatwaves and droughts; global barley yields fell 4.5% in 2023 vs. 2019, tightening supply and lifting prices about 12% in 2022–24 for malting barley. Heineken invested €100m by 2025 in regenerative agriculture and farmer programs to boost resilience and yield, which eases risk but supplier power rises slightly as climate-resilient seedstock remains scarce.

Energy and utility dependence

Brewing is energy-intensive, making Heineken dependent on electricity, gas and water; in 2024 Heineken reported 61% of global production sites sourcing renewable electricity, yet utilities often remain local monopolies that set prices and limit infrastructure.

This dependence is a measurable external cost: energy made up about 4–6% of COGS in recent years, so Heineken offsets risk via efficiency programs and investing in onsite solar, biomass and localized cogeneration.

- 61% sites on renewable electricity (2024)

- Energy ≈4–6% of COGS

- Onsite solar, biomass, cogeneration investments

- Local utility monopolies constrain pricing and capacity

Strategic procurement and vertical integration

Heineken limits supplier power via long-term strategic contracts and regional vertical integration into malting and packaging; in 2024 Heineken owned or co-invested in facilities covering ~8% of its malting and 6% of packaging needs in key markets.

Controlling these nodes trims exposure to input-price shocks—reducing raw-material cost volatility by an estimated 1.2 percentage points of COGS in 2023—and secures priority capacity versus small craft brewers.

- Long-term contracts, global scale

- Vertical assets in select regions (~8% malting, ~6% packaging)

- Estimated 1.2 pp COGS volatility reduction (2023)

- Preferential supplier access vs craft brewers

Heineken tames supplier pressure via scale, verticals & €100m farmer investments

Suppliers exert moderate power: undifferentiated agri inputs limit leverage, but concentrated glass/metal firms, local utility monopolies, and shrinking sustainable-certified supplier pools (−25% by end‑2025) raise costs. Heineken’s scale, long‑term hedges, 8% malting/6% packaging verticals and €100m farmer investment cut volatility (~1.2 pp COGS in 2023) and keep supplier power contained.

| Metric | Value |

|---|---|

| Renewable sites (2024) | 61% |

| Energy of COGS | 4–6% |

| Vertical malting/packaging | 8% / 6% |

| Farmer investment | €100m (by 2025) |

What is included in the product

Tailored exclusively for Heineken, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, substitute threats, and entry barriers shaping its profitability and strategic positioning.

Clear, one-sheet Porter's Five Forces summary for Heineken—fast insights into competitive intensity, supplier/buyer power, substitutes, and entry threats to guide strategic moves.

Customers Bargaining Power

Concentration of large scale retail chains

In mature markets like Western Europe, roughly 40–50% of Heineken NV's beer volume moves through a handful of supermarket and big-box chains that wield strong bargaining power.

These retailers demand lower wholesale prices, co‑funded promotions, and prime shelf placement—pressuring Heineken's gross margins (Heineken reported a 2024 gross margin around 49%).

To stay prioritized, Heineken must keep innovating—new SKUs, premium lines, and marketing—to preserve brand pull and offset retailer leverage.

Low switching costs for individual consumers

End consumers face virtually zero switching costs when moving from Heineken to rivals or other drinks, so habitual buying is weak and churn risk is high.

That lack of friction makes brand loyalty Heineken’s main defense; in 2024 Heineken spent EUR 1.7bn on commercial and marketing activities to protect share and support pricing.

As a result Heineken prioritizes experiential marketing and sponsorships to justify a premium price and sustain margins—EBIT margin 2024: ~10.6%.

Influence of the on-trade channel

The on-trade channel—bars, restaurants, hotels—is central to Heineken’s premium branding and drove ~28% of global beer consumer occasions in 2024; these buyers hold moderate bargaining power by curating limited tap lists and steering choices through staff recommendations. Heineken defends share via exclusive pouring-rights deals and by supplying premium draught systems—over 150,000 served installations by end-2024—locking venues into long-term relationships.

Growth of e-commerce and direct-to-consumer platforms

By 2025, e-commerce growth gave consumers clearer price transparency and more choices, with global online alcohol sales reaching ~14% of off‑trade volume (IWSR, 2024); this raised customer bargaining power.

Heineken launched B2B and B2C platforms—including e‑commerce pilots in 30+ markets and data lakes aggregating sales and CRM—by 2024 to capture first‑party data and shorten channels.

These platforms aim to cut intermediaries’ influence, boost repeat buying, and lift direct margin; early pilots reported 5–8% higher retention and 3–5% higher gross margin.

- Online alcohol ~14% of off‑trade volume (2024)

- Heineken digital pilots in 30+ markets (2024)

- Retention +5–8% in pilots; gross margin +3–5%

Price sensitivity in emerging markets

In many emerging markets median household income stays below US 10,000/year, so price drives beer choice; Heineken must mix premium positioning with lower-priced SKUs to win volume.

Customers can trade down to local lagers; in Nigeria and India up to 60% of beer volume is low-price brands, so high Heineken prices risk losing share.

- Lower incomes — price-led buying

- Need premium + value SKUs

- High trade-down risk (eg 60% volume low-price in some markets)

Heineken: Retail power, €1.7bn marketing, 49% margin—digital pilots lift retention & margins

Customers have high bargaining power: retailers channel ~40–50% volume in Western Europe, online off‑trade ~14% (2024), and low‑income markets see up to 60% trade‑down. Heineken spent EUR 1.7bn on marketing in 2024; gross margin ~49%, EBIT ~10.6%. Digital pilots (30+ markets) raised retention +5–8% and gross margin +3–5%.

| Metric | 2024 |

|---|---|

| Retail share (WE) | 40–50% |

| Online off‑trade | ~14% |

| Marketing spend | EUR 1.7bn |

| Gross margin | ~49% |

What You See Is What You Get

Heineken Porter's Five Forces Analysis

This preview shows the exact Heineken Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy. You're looking at the actual, professionally formatted file; once you complete your purchase, you’ll get instant access to this same document. No mockups, no samples—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Heineken faces intense rivalry from global brewers, shifting consumer tastes toward craft and low‑alcohol options, and strong buyer power from large retailers—while supplier concentration and regulatory pressures add complexity to margin management.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Heineken’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmentation of agricultural raw material providers

Heineken buys malting barley and hops from thousands of global and local farmers; these inputs are undifferentiated commodities so no single supplier wields major power. In 2024 Heineken reported procurement of ~3.1 million hectolitres worth of barley-related inputs, using scale to secure discounts and fixed-price contracts. The brewer diversifies across regions and contracts, cutting single-supplier exposure and lowering supply risk.

Volatility of packaging material costs

Heineken depends on suppliers for glass, aluminium and cardboard, exposing it to global commodity swings—glass rose 18% and aluminium 12% in 2023-24 supply cycles, pushing packaging to ~8-10% of COGS for brewers.

Heineken uses multi-year hedges and 60- to 36-month contracts to smooth costs, but a few large glass and metal firms give suppliers moderate bargaining power.

By end-2025, sustainability rules and circular-packaging specs cut the qualified supplier pool by about 25%, raising switch costs and supplier leverage.

Impact of climate change on crop yields

Suppliers of premium hops and barley face rising yield volatility from heatwaves and droughts; global barley yields fell 4.5% in 2023 vs. 2019, tightening supply and lifting prices about 12% in 2022–24 for malting barley. Heineken invested €100m by 2025 in regenerative agriculture and farmer programs to boost resilience and yield, which eases risk but supplier power rises slightly as climate-resilient seedstock remains scarce.

Energy and utility dependence

Brewing is energy-intensive, making Heineken dependent on electricity, gas and water; in 2024 Heineken reported 61% of global production sites sourcing renewable electricity, yet utilities often remain local monopolies that set prices and limit infrastructure.

This dependence is a measurable external cost: energy made up about 4–6% of COGS in recent years, so Heineken offsets risk via efficiency programs and investing in onsite solar, biomass and localized cogeneration.

- 61% sites on renewable electricity (2024)

- Energy ≈4–6% of COGS

- Onsite solar, biomass, cogeneration investments

- Local utility monopolies constrain pricing and capacity

Strategic procurement and vertical integration

Heineken limits supplier power via long-term strategic contracts and regional vertical integration into malting and packaging; in 2024 Heineken owned or co-invested in facilities covering ~8% of its malting and 6% of packaging needs in key markets.

Controlling these nodes trims exposure to input-price shocks—reducing raw-material cost volatility by an estimated 1.2 percentage points of COGS in 2023—and secures priority capacity versus small craft brewers.

- Long-term contracts, global scale

- Vertical assets in select regions (~8% malting, ~6% packaging)

- Estimated 1.2 pp COGS volatility reduction (2023)

- Preferential supplier access vs craft brewers

Heineken tames supplier pressure via scale, verticals & €100m farmer investments

Suppliers exert moderate power: undifferentiated agri inputs limit leverage, but concentrated glass/metal firms, local utility monopolies, and shrinking sustainable-certified supplier pools (−25% by end‑2025) raise costs. Heineken’s scale, long‑term hedges, 8% malting/6% packaging verticals and €100m farmer investment cut volatility (~1.2 pp COGS in 2023) and keep supplier power contained.

| Metric | Value |

|---|---|

| Renewable sites (2024) | 61% |

| Energy of COGS | 4–6% |

| Vertical malting/packaging | 8% / 6% |

| Farmer investment | €100m (by 2025) |

What is included in the product

Tailored exclusively for Heineken, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, substitute threats, and entry barriers shaping its profitability and strategic positioning.

Clear, one-sheet Porter's Five Forces summary for Heineken—fast insights into competitive intensity, supplier/buyer power, substitutes, and entry threats to guide strategic moves.

Customers Bargaining Power

Concentration of large scale retail chains

In mature markets like Western Europe, roughly 40–50% of Heineken NV's beer volume moves through a handful of supermarket and big-box chains that wield strong bargaining power.

These retailers demand lower wholesale prices, co‑funded promotions, and prime shelf placement—pressuring Heineken's gross margins (Heineken reported a 2024 gross margin around 49%).

To stay prioritized, Heineken must keep innovating—new SKUs, premium lines, and marketing—to preserve brand pull and offset retailer leverage.

Low switching costs for individual consumers

End consumers face virtually zero switching costs when moving from Heineken to rivals or other drinks, so habitual buying is weak and churn risk is high.

That lack of friction makes brand loyalty Heineken’s main defense; in 2024 Heineken spent EUR 1.7bn on commercial and marketing activities to protect share and support pricing.

As a result Heineken prioritizes experiential marketing and sponsorships to justify a premium price and sustain margins—EBIT margin 2024: ~10.6%.

Influence of the on-trade channel

The on-trade channel—bars, restaurants, hotels—is central to Heineken’s premium branding and drove ~28% of global beer consumer occasions in 2024; these buyers hold moderate bargaining power by curating limited tap lists and steering choices through staff recommendations. Heineken defends share via exclusive pouring-rights deals and by supplying premium draught systems—over 150,000 served installations by end-2024—locking venues into long-term relationships.

Growth of e-commerce and direct-to-consumer platforms

By 2025, e-commerce growth gave consumers clearer price transparency and more choices, with global online alcohol sales reaching ~14% of off‑trade volume (IWSR, 2024); this raised customer bargaining power.

Heineken launched B2B and B2C platforms—including e‑commerce pilots in 30+ markets and data lakes aggregating sales and CRM—by 2024 to capture first‑party data and shorten channels.

These platforms aim to cut intermediaries’ influence, boost repeat buying, and lift direct margin; early pilots reported 5–8% higher retention and 3–5% higher gross margin.

- Online alcohol ~14% of off‑trade volume (2024)

- Heineken digital pilots in 30+ markets (2024)

- Retention +5–8% in pilots; gross margin +3–5%

Price sensitivity in emerging markets

In many emerging markets median household income stays below US 10,000/year, so price drives beer choice; Heineken must mix premium positioning with lower-priced SKUs to win volume.

Customers can trade down to local lagers; in Nigeria and India up to 60% of beer volume is low-price brands, so high Heineken prices risk losing share.

- Lower incomes — price-led buying

- Need premium + value SKUs

- High trade-down risk (eg 60% volume low-price in some markets)

Heineken: Retail power, €1.7bn marketing, 49% margin—digital pilots lift retention & margins

Customers have high bargaining power: retailers channel ~40–50% volume in Western Europe, online off‑trade ~14% (2024), and low‑income markets see up to 60% trade‑down. Heineken spent EUR 1.7bn on marketing in 2024; gross margin ~49%, EBIT ~10.6%. Digital pilots (30+ markets) raised retention +5–8% and gross margin +3–5%.

| Metric | 2024 |

|---|---|

| Retail share (WE) | 40–50% |

| Online off‑trade | ~14% |

| Marketing spend | EUR 1.7bn |

| Gross margin | ~49% |

What You See Is What You Get

Heineken Porter's Five Forces Analysis

This preview shows the exact Heineken Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy. You're looking at the actual, professionally formatted file; once you complete your purchase, you’ll get instant access to this same document. No mockups, no samples—what you see is what you get.