Helvetia Holding Boston Consulting Group Matrix

See the Bigger Picture

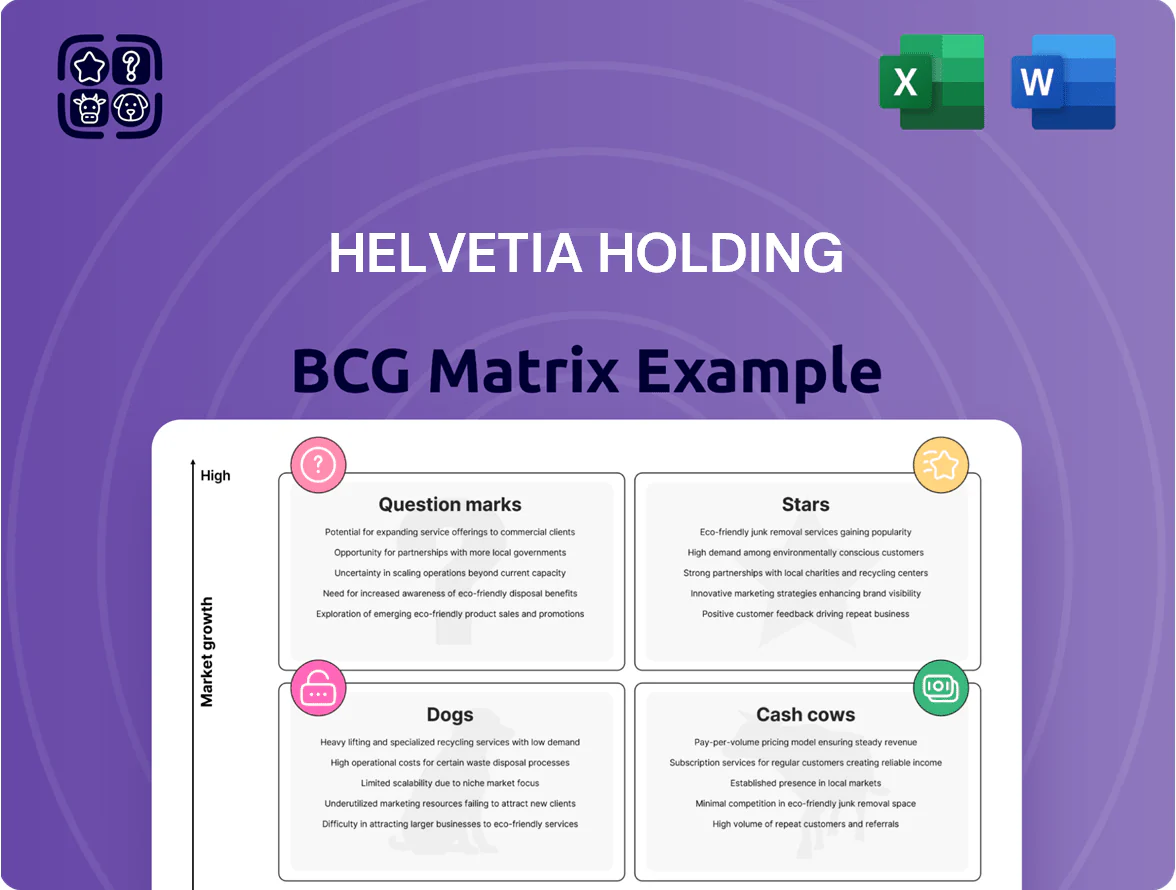

Helvetia Holding’s BCG Matrix snapshot highlights where key business lines—life insurance, P&C, and reinsurance—likely sit across Stars, Cash Cows, Dogs, and Question Marks amid low-yield environments and digital disruption; this preview outlines competitive strengths and capital allocation tensions. Purchase the full BCG Matrix for quadrant-level placements, data-driven strategic moves, and ready-to-use Word and Excel files to guide investment and portfolio decisions with confidence.

Stars

Smile Digital Insurance Brand

Smile Digital Insurance Brand, Helvetia’s digital-first arm, is a Star: Swiss market share ~28% in digital-only P&C (2024), revenue ~CHF 120m (2024) and 40% YoY growth, plus launches in Spain and Austria in 2024 supporting Europe scale.

It wins younger tech-savvy customers—~65% of policyholders under 35—driving high direct-to-consumer growth, but needs sustained marketing spend (~15% of revenue) to defend digital leadership.

Spanish Non-Life Insurance Expansion

Helvetia has boosted its Spanish non-life footprint to roughly 8–10% market share in property & casualty after 2023–2025 acquisitions and organic growth, in a market growing ~4–6% annually vs. mature Swiss growth under 1%.

The Spain non-life unit is a Star: it consumes capital for consolidation—Helvetia increased Spain non-life capital allocation by ~€120m in 2024—but projects the highest medium-term cash generation in Europe, with ROE targets above 12%.

Specialty Lines Global Markets

Specialty Lines Global Markets, covering marine, art and engineering, sits in a high-growth global segment—Helvetia reported 2024 specialty GWP (gross written premium) of CHF 1.1bn, up 9% year-on-year, supporting a Star position in the BCG matrix.

Helvetia’s deep expertise in complex risks yields leading shares in specific international niches (estimated 10–15% share in Swiss art-insurance intermediated markets), but maintaining this requires ongoing hires.

Continuous investment in underwriting talent raises cash consumption—estimated incremental opex of CHF 40–60m annually—yet drives significant revenue growth and loss-adjusted margins above group average.

Fee-Based Financial Services

Transitioning to fee-based income is central to Helvetia’s recent strategy, with fee and commission income rising 14% to CHF 780m in 2024 as customers move away from traditional life products.

Leveraging brand trust, Helvetia expanded advisory and third-party asset management, growing assets under management (AUM) to CHF 22.4bn by YE 2024, capturing increased service-market share.

This segment is a Star: it shows high revenue growth, needs continuous platform investment, but avoids the capital intensity of on-balance-sheet insurance.

- Fee income +14% to CHF 780m (2024)

- AUM CHF 22.4bn (YE 2024)

- High growth, platform-heavy, low capital intensity

Austrian Property and Casualty Segment

Helvetia’s Austrian P&C unit is a fast-growing, top-tier provider in retail and SMEs, increasing market share to about 8.5% in 2024 from 7.3% in 2021 (Austrian market data).

Rising risk awareness and climate-related claims lifted demand for modern property protection; sector premium growth ran ~6–8% in 2023–24 versus market ~3–4%.

The unit outpaced market growth and needs steady investment to defend leadership against entrenched local incumbents; combined ratio improved to ~93% in FY 2024.

- Market share ~8.5% (2024)

- Premium growth ~6–8% (2023–24)

- Market growth ~3–4%

- Combined ratio ~93% (FY 2024)

High-growth Smile Digital & specialty lines drive strong P&C momentum across Spain & Austria

Stars: Smile Digital (28% Swiss digital P&C share, CHF120m rev, 40% YoY, Spain/Austria 2024); Spain non-life (8–10% P&C share, +€120m capital 2024, ROE >12% target); Specialty Lines (GWP CHF1.1bn, +9% YoY); Austria P&C (8.5% share, 6–8% premium growth, combined ratio ~93%).

| Unit | Key metrics 2024 |

|---|---|

| Smile Digital | CHF120m rev; 40% YoY; 28% digital share |

| Spain NL | 8–10% share; +€120m cap |

| Specialty | GWP CHF1.1bn; +9% |

| Austria P&C | 8.5% share; CR ~93% |

What is included in the product

Comprehensive BCG review of Helvetia’s units with strategies for Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix placing Helvetia units in quadrants for quick strategic clarity, export-ready for PowerPoint or print.

Cash Cows

Swiss Individual Life Insurance

Swiss individual life insurance is a mature market where Helvetia held about 14.7% market share in 2024, remaining a top-three player and delivering stable premiums of ~CHF 2.1bn that year.

These policies generate strong operating cash flow—roughly CHF 350–420m annually—requiring little new infrastructure or heavy marketing spend.

Harvested capital funds group dividends (CHF 180m paid in 2024) and fuels reinvestment into higher-growth digital initiatives and Swiss/German expansion.

Swiss Non-Life Core Portfolio

Helvetia’s Swiss Non-Life core (motor, home, liability) is a cash cow: #1 market shares ~20–25% in motor and household (2024), very high customer retention and single-digit market growth.

Operations show top-tier efficiency with combined ratios ~88–92% (2024) and operating margin ~12–15%, producing steady underwriting profits and >CHF 600–800m annual free cash flow to the group.

Low capex needs: maintenance-level investment protects book value and renewal rates, so the unit funds growth units while requiring minimal incremental spend.

German Occupational Pension Business

In Germany, Helvetia’s occupational pension arm holds a top-3 market position with roughly 18% share in corporate pensions as of 2025, yielding stable premiums ~€450m annually and predictable reserves; growth of traditional DB/insured DC has fallen to ~1–2% CAGR.

The unit generates high operating ROE (~12% in 2024) and low incremental capital needs, freeing €100–150m yearly liquidity to fund digital product rollout and DC solutions for the German branch.

Group Life Insurance Switzerland

The mandatory occupational benefits market in Switzerland is mature and tightly regulated, limiting growth but delivering scale: Swiss occupational pensions cover ~5.4 million insured lives and CHF 280 billion in annual premium-equivalent flows (2024); Helvetia holds a leading share and leverages deep corporate relationships to capture volume.

Stable cash generation from Group Life Insurance supports Helvetia’s solvency and costs—net combined ratio benefits and steady fee income meant this unit contributed materially to group operating cash flow in 2024, acting as a core cash cow.

- Market size: ~5.4M insured; CHF 280B premium-equivalent (2024)

- Role: high volume, low growth, highly regulated

- Helvetia edge: scale + deep corporate ties

- Value: stable cash flows improving solvency and covering ops

Real Estate Asset Management

Helvetia’s Real Estate Asset Management oversees ~CHF 4.2bn of investment properties (2024), mainly in Switzerland, delivering steady rental yields (~3.2% in 2024) and longer-term capital appreciation.

The segment is mature, needs minimal marketing versus insurance lines, and has low capex intensity, preserving net operating income for dividends and reserves.

Its predictable cash flow acts as a defensive buffer, helping cover long-term technical liabilities and smoothing group liquidity.

- Portfolio value ~CHF 4.2bn (2024)

- Rental yield ~3.2% (2024)

- Low promo spend vs insurance

- Supports long-term liabilities

Helvetia’s cash cows: CHF1.1–1.5bn FCF fuels dividends, German liquidity & growth

Helvetia’s cash cows—Swiss individual life, Swiss Non‑Life core, German occupational pensions, and real‑estate AM—delivered combined free cash flow ~CHF 1.1–1.5bn (2024), supporting CHF 180m dividend, €100–150m Germany liquidity, and steady solvency. Low capex, high retention, and market shares (Swiss life 14.7%, motor/home 20–25%) make them funding sources for digital and growth moves.

| Unit | FY2024 key |

|---|---|

| Swiss life | CHF 2.1bn prem; 14.7% MS; CHF 350–420m opCF |

| Swiss Non‑Life | 20–25% MS; CR 88–92%; CHF 600–800m FCF |

| DE pensions | €450m prem; ~18% MS; €100–150m liquidity |

| Real estate | CHF 4.2bn assets; 3.2% yield |

What You See Is What You Get

Helvetia Holding BCG Matrix

The file you're previewing on this page is the final Helvetia Holding BCG Matrix you'll receive after purchase. No watermarks or demo content—just a fully formatted, ready-to-use strategic report tailored for clarity and professional presentation.

This preview is the exact same BCG Matrix report available for download post-purchase, crafted with precise market analysis and actionable insights—delivered directly to your inbox with no surprises or further edits required.

What you see is the actual Helvetia Holding BCG Matrix file you’ll get after buying; the full version is immediately editable, printable, and presentation-ready for internal planning or client meetings.

You're viewing the real, professionally designed BCG Matrix document that becomes yours after a one-time purchase—analysis-ready and formatted to plug straight into your business strategy work or investor materials.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Helvetia Holding’s BCG Matrix snapshot highlights where key business lines—life insurance, P&C, and reinsurance—likely sit across Stars, Cash Cows, Dogs, and Question Marks amid low-yield environments and digital disruption; this preview outlines competitive strengths and capital allocation tensions. Purchase the full BCG Matrix for quadrant-level placements, data-driven strategic moves, and ready-to-use Word and Excel files to guide investment and portfolio decisions with confidence.

Stars

Smile Digital Insurance Brand

Smile Digital Insurance Brand, Helvetia’s digital-first arm, is a Star: Swiss market share ~28% in digital-only P&C (2024), revenue ~CHF 120m (2024) and 40% YoY growth, plus launches in Spain and Austria in 2024 supporting Europe scale.

It wins younger tech-savvy customers—~65% of policyholders under 35—driving high direct-to-consumer growth, but needs sustained marketing spend (~15% of revenue) to defend digital leadership.

Spanish Non-Life Insurance Expansion

Helvetia has boosted its Spanish non-life footprint to roughly 8–10% market share in property & casualty after 2023–2025 acquisitions and organic growth, in a market growing ~4–6% annually vs. mature Swiss growth under 1%.

The Spain non-life unit is a Star: it consumes capital for consolidation—Helvetia increased Spain non-life capital allocation by ~€120m in 2024—but projects the highest medium-term cash generation in Europe, with ROE targets above 12%.

Specialty Lines Global Markets

Specialty Lines Global Markets, covering marine, art and engineering, sits in a high-growth global segment—Helvetia reported 2024 specialty GWP (gross written premium) of CHF 1.1bn, up 9% year-on-year, supporting a Star position in the BCG matrix.

Helvetia’s deep expertise in complex risks yields leading shares in specific international niches (estimated 10–15% share in Swiss art-insurance intermediated markets), but maintaining this requires ongoing hires.

Continuous investment in underwriting talent raises cash consumption—estimated incremental opex of CHF 40–60m annually—yet drives significant revenue growth and loss-adjusted margins above group average.

Fee-Based Financial Services

Transitioning to fee-based income is central to Helvetia’s recent strategy, with fee and commission income rising 14% to CHF 780m in 2024 as customers move away from traditional life products.

Leveraging brand trust, Helvetia expanded advisory and third-party asset management, growing assets under management (AUM) to CHF 22.4bn by YE 2024, capturing increased service-market share.

This segment is a Star: it shows high revenue growth, needs continuous platform investment, but avoids the capital intensity of on-balance-sheet insurance.

- Fee income +14% to CHF 780m (2024)

- AUM CHF 22.4bn (YE 2024)

- High growth, platform-heavy, low capital intensity

Austrian Property and Casualty Segment

Helvetia’s Austrian P&C unit is a fast-growing, top-tier provider in retail and SMEs, increasing market share to about 8.5% in 2024 from 7.3% in 2021 (Austrian market data).

Rising risk awareness and climate-related claims lifted demand for modern property protection; sector premium growth ran ~6–8% in 2023–24 versus market ~3–4%.

The unit outpaced market growth and needs steady investment to defend leadership against entrenched local incumbents; combined ratio improved to ~93% in FY 2024.

- Market share ~8.5% (2024)

- Premium growth ~6–8% (2023–24)

- Market growth ~3–4%

- Combined ratio ~93% (FY 2024)

High-growth Smile Digital & specialty lines drive strong P&C momentum across Spain & Austria

Stars: Smile Digital (28% Swiss digital P&C share, CHF120m rev, 40% YoY, Spain/Austria 2024); Spain non-life (8–10% P&C share, +€120m capital 2024, ROE >12% target); Specialty Lines (GWP CHF1.1bn, +9% YoY); Austria P&C (8.5% share, 6–8% premium growth, combined ratio ~93%).

| Unit | Key metrics 2024 |

|---|---|

| Smile Digital | CHF120m rev; 40% YoY; 28% digital share |

| Spain NL | 8–10% share; +€120m cap |

| Specialty | GWP CHF1.1bn; +9% |

| Austria P&C | 8.5% share; CR ~93% |

What is included in the product

Comprehensive BCG review of Helvetia’s units with strategies for Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix placing Helvetia units in quadrants for quick strategic clarity, export-ready for PowerPoint or print.

Cash Cows

Swiss Individual Life Insurance

Swiss individual life insurance is a mature market where Helvetia held about 14.7% market share in 2024, remaining a top-three player and delivering stable premiums of ~CHF 2.1bn that year.

These policies generate strong operating cash flow—roughly CHF 350–420m annually—requiring little new infrastructure or heavy marketing spend.

Harvested capital funds group dividends (CHF 180m paid in 2024) and fuels reinvestment into higher-growth digital initiatives and Swiss/German expansion.

Swiss Non-Life Core Portfolio

Helvetia’s Swiss Non-Life core (motor, home, liability) is a cash cow: #1 market shares ~20–25% in motor and household (2024), very high customer retention and single-digit market growth.

Operations show top-tier efficiency with combined ratios ~88–92% (2024) and operating margin ~12–15%, producing steady underwriting profits and >CHF 600–800m annual free cash flow to the group.

Low capex needs: maintenance-level investment protects book value and renewal rates, so the unit funds growth units while requiring minimal incremental spend.

German Occupational Pension Business

In Germany, Helvetia’s occupational pension arm holds a top-3 market position with roughly 18% share in corporate pensions as of 2025, yielding stable premiums ~€450m annually and predictable reserves; growth of traditional DB/insured DC has fallen to ~1–2% CAGR.

The unit generates high operating ROE (~12% in 2024) and low incremental capital needs, freeing €100–150m yearly liquidity to fund digital product rollout and DC solutions for the German branch.

Group Life Insurance Switzerland

The mandatory occupational benefits market in Switzerland is mature and tightly regulated, limiting growth but delivering scale: Swiss occupational pensions cover ~5.4 million insured lives and CHF 280 billion in annual premium-equivalent flows (2024); Helvetia holds a leading share and leverages deep corporate relationships to capture volume.

Stable cash generation from Group Life Insurance supports Helvetia’s solvency and costs—net combined ratio benefits and steady fee income meant this unit contributed materially to group operating cash flow in 2024, acting as a core cash cow.

- Market size: ~5.4M insured; CHF 280B premium-equivalent (2024)

- Role: high volume, low growth, highly regulated

- Helvetia edge: scale + deep corporate ties

- Value: stable cash flows improving solvency and covering ops

Real Estate Asset Management

Helvetia’s Real Estate Asset Management oversees ~CHF 4.2bn of investment properties (2024), mainly in Switzerland, delivering steady rental yields (~3.2% in 2024) and longer-term capital appreciation.

The segment is mature, needs minimal marketing versus insurance lines, and has low capex intensity, preserving net operating income for dividends and reserves.

Its predictable cash flow acts as a defensive buffer, helping cover long-term technical liabilities and smoothing group liquidity.

- Portfolio value ~CHF 4.2bn (2024)

- Rental yield ~3.2% (2024)

- Low promo spend vs insurance

- Supports long-term liabilities

Helvetia’s cash cows: CHF1.1–1.5bn FCF fuels dividends, German liquidity & growth

Helvetia’s cash cows—Swiss individual life, Swiss Non‑Life core, German occupational pensions, and real‑estate AM—delivered combined free cash flow ~CHF 1.1–1.5bn (2024), supporting CHF 180m dividend, €100–150m Germany liquidity, and steady solvency. Low capex, high retention, and market shares (Swiss life 14.7%, motor/home 20–25%) make them funding sources for digital and growth moves.

| Unit | FY2024 key |

|---|---|

| Swiss life | CHF 2.1bn prem; 14.7% MS; CHF 350–420m opCF |

| Swiss Non‑Life | 20–25% MS; CR 88–92%; CHF 600–800m FCF |

| DE pensions | €450m prem; ~18% MS; €100–150m liquidity |

| Real estate | CHF 4.2bn assets; 3.2% yield |

What You See Is What You Get

Helvetia Holding BCG Matrix

The file you're previewing on this page is the final Helvetia Holding BCG Matrix you'll receive after purchase. No watermarks or demo content—just a fully formatted, ready-to-use strategic report tailored for clarity and professional presentation.

This preview is the exact same BCG Matrix report available for download post-purchase, crafted with precise market analysis and actionable insights—delivered directly to your inbox with no surprises or further edits required.

What you see is the actual Helvetia Holding BCG Matrix file you’ll get after buying; the full version is immediately editable, printable, and presentation-ready for internal planning or client meetings.

You're viewing the real, professionally designed BCG Matrix document that becomes yours after a one-time purchase—analysis-ready and formatted to plug straight into your business strategy work or investor materials.