Hengli Petrochemical Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

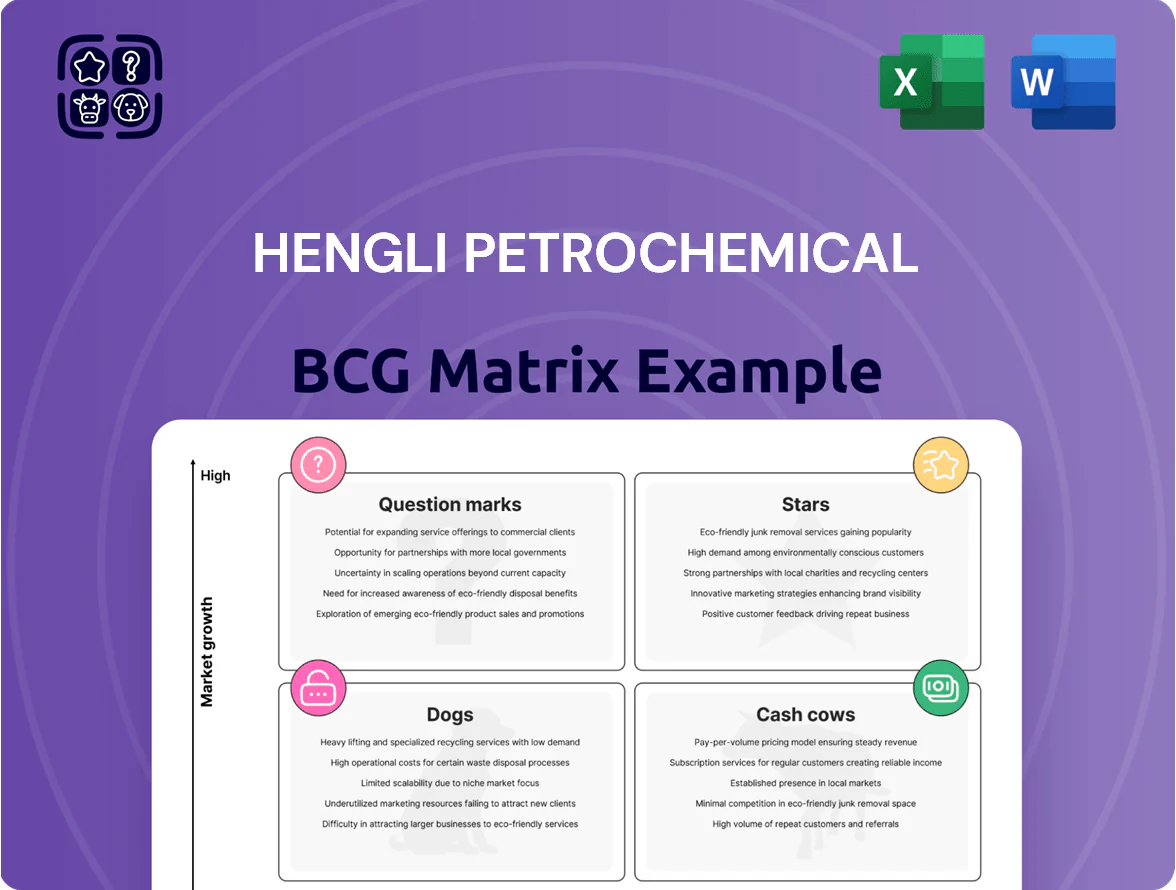

Hengli Petrochemical’s preliminary BCG Matrix indicates a mix of high-growth polymers likely sitting as Stars, mature refining segments acting as Cash Cows, and smaller niche products that may be Question Marks or Dogs depending on demand cycles; this snapshot highlights strategic allocation needs across its value chain. Purchase the full BCG Matrix to obtain quadrant-level placements, data-backed recommendations, and downloadable Word and Excel files to guide investment and operational decisions with clarity and speed.

Stars

Lithium Battery Separators

Hengli Petrochemical scaled wet- and dry-process lithium battery separator capacity to ~2.4 billion m2/year by end-2025, capturing ~12% share of China’s premium separator market and becoming a key growth engine in premium energy materials.

Revenue from separators rose to RMB 7.8 billion in 2025 (≈USD 1.1 billion), a CAGR ~85% since 2022, driven by EV and ESS demand and long-term offtake contracts with three major automakers.

Hengli deployed ~RMB 18 billion in capex 2023–2025 for advanced coating lines and R&D, positioning its separators as a strategic asset to lead industry decarbonization and margin expansion.

High-End Functional Polyester Films

Hengli Petrochemical dominates China’s BOPET optical/electronic-grade films with an estimated domestic market share ~40% in 2024, supplying high-tech displays and semiconductors as China’s high-end manufacturing grew ~12% YoY in 2024.

The segment generated about RMB 9.2bn revenue in 2024 (≈USD 1.3bn), and Hengli reinvests ~5–7% of segment sales annually into R&D to keep a tech lead over South Korean and Japanese rivals.

High-Performance Engineering Plastics

With full commissioning of new lines in 2024, Hengli Petrochemical’s PBT and PC engineering plastics captured an estimated 12–15% share of China’s automotive-grade polymer market, supplying tier-1 auto makers and electronics firms.

The segment rides the lightweighting trend as global auto polymer parts grew ~8% CAGR 2020–2025, replacing metals with high-strength polymers and boosting ASPs by ~6% in 2024.

High downstream growth (EV and 5G hardware demand up ~10–12% annually) forces Hengli to reinvest ~¥3–4 billion per major line cycle to keep capacity and tech leadership.

Integrated Refining-Chemical-Material Hubs

Hengli Petrochemical’s 20 million tpa integrated refining-chemical-material hub is a star: it converts crude into high-margin aromatics and polyesters, supplying >60% of the company’s premium feedstocks and supporting 2024 EBITDA contribution of roughly RMB 25–30 billion.

The tight upstream-downstream link raises conversion efficiency ~20% vs peers, secures scale-based pricing power, and positions Hengli to capture projected 3–4% annual growth in global specialty chemicals through 2028.

Synergy locks-in market dominance in high-end polymers and intermediates, cutting unit costs and boosting ROIC above industry averages; capital intensity matched by long-term offtake contracts and vertical integration benefits.

- 20 million tpa integrated capacity

- ~60% premium feedstock share

- 2024 EBITDA ~RMB 25–30bn

- ~20% higher conversion efficiency vs peers

- 3–4% annual specialty chemical market growth to 2028

Specialty Fine Chemicals

Hengli Petrochemical’s push into specialty fine chemicals—high-purity solvents and additives—targets pharma and electronics, where global demand grew ~7–9% CAGR through 2024; Hengli reported these lines achieved ~15% domestic market share by Q3 2025.

Heavy R&D spend (~3–4% of sales in 2024) is offset by >30% revenue growth in these products in 2024–2025, helped by integrated feedstock supply and margin expansion versus commodity petrochemicals.

- Targets: pharma, electronics

- Market share: ~15% domestic (Q3 2025)

- Revenue growth: >30% (2024–2025)

- R&D: ~3–4% of sales (2024)

- Advantage: integrated raw-material supply

Hengli’s 20Mtpa integrated hub fuels margin, market share with RMB18bn capex & strong R&D

Hengli’s Stars: integrated 20Mtpa hub (2024 EBITDA RMB25–30bn), separators capacity ~2.4bn m2/yr (2025) with RMB7.8bn revenue (2025), BOPET ~40% domestic share (2024) with RMB9.2bn revenue (2024), PBT/PC ~12–15% auto polymer share (2024); heavy capex RMB18bn (2023–25) and R&D 3–7% of sales drive margin and share gains.

| Metric | Value |

|---|---|

| Integrated capacity | 20Mtpa |

| Separators rev | RMB7.8bn (2025) |

| BOPET share | ~40% (2024) |

| Capex 2023–25 | RMB18bn |

What is included in the product

Comprehensive BCG Matrix review of Hengli Petrochemical: quadrant insights, strategic moves to invest, hold or divest, and trend-driven risks/opportunities.

One-page BCG matrix placing Hengli Petrochemical units in clear quadrants for fast strategic decisions and investor briefs.

Cash Cows

Purified Terephthalic Acid Production

Hengli Petrochemical is a global PTA leader with ~6.4 million tpa installed capacity in 2025, among the world’s largest and lowest-cost producers, driving margin resilience (2024 PTA EBITDA margin ~22%).

Polyester market maturity means PTA is a cash cow: scale, continuous processes, and feedstock integration produced RMB 38.7 billion operating cash flow in 2024.

Those cash flows fund capex into battery materials and specialty films—Hengli allocated RMB 21.5 billion to new-materials R&D and projects in 2024–25.

Refining and Ethylene Units

Hengli Petrochemical’s refining and ethylene units run at >92% utilization (2024), processing ~24 million tonnes crude/year and supplying feedstock across its polyester chain, giving stable, high-volume cash flows in a mature fuels and petrochemicals market.

Optimized crude sourcing and logistics cut feedstock costs ~6% vs peers (2024), lifting refinery EBITDA margins to ~14% and olefins margins to ~18%, driving strong free cash flow.

Given mature demand for fuels and basic ethylene, capex on these assets was just 1–2% of revenues in 2024, so they generate excess cash requiring minimal new investment relative to returns.

Conventional Polyester Chips

Conventional polyester chips (standard-grade) hold a leading market share in a low-growth textile and packaging market, with global polyester demand growth ~1.5% in 2024 and China consumption ~35 Mt; Hengli’s share in China’s chip market exceeded 12% in 2024, placing it as a cash cow.

Hengli’s vertical integration—feedstock-to-chip—kept 2024 unit COGS ~8–12% below peers, letting it partially set prices in a mature spot market where ASPs fell 3% YoY in 2024.

The segment generated ~RMB 28–32 billion operating cash flow in 2024, funding debt service (net debt/EBITDA ~1.6x) and sustaining dividends without tapping capex budgets.

Civilian Polyester Filament

Civilian polyester filament is a classic cash cow for Hengli Petrochemical: Hengli held roughly 28% share of China apparel-grade polyester filament capacity in 2024 and reported RMB 12.4 billion in yarn sales in FY2024, delivering steady EBITDA margins near 18% as clothing demand grows ~2–3% annually—focus is on cost cuts and throughput rather than expansion.

- Market share ~28% (China, 2024)

- Yarn sales RMB 12.4bn (FY2024)

- EBITDA margin ~18%

- Clothing demand growth 2–3% p.a.

- Low capex; strong free cash flow

Industrial Polyester Yarn

Industrial polyester yarn, used mainly in automotive tires and infrastructure, is a Hengli Petrochemical cash cow with stable volumes—Hengli reported ~1.2 million tonnes polyester filament capacity in 2024 supporting steady EBITDA margins near 18% for yarn-related operations.

Quality consistency and long-term supply contracts with global tire and construction manufacturers secure high barriers to entry, generating predictable free cash flow that funds Hengli’s moves into higher-growth, higher-volatility segments.

- Primary end-markets: tires, infrastructure

- 2024 yarn capacity ~1.2 Mt

- Approx. EBITDA margin ~18% (yarn ops, 2024)

- Long-term contracts with global OEMs

Hengli cash cows: strong PTA/refining margins, RMB28–32bn OCF, low leverage

Hengli’s polyester/PTA/refining lines are cash cows: 2024 PTA EBITDA ~22%, refinery EBITDA ~14%, segment OCF ~RMB28–32bn, net debt/EBITDA ~1.6x, China chip share >12%, filament share ~28%, yarn sales RMB12.4bn, 2025 PTA capacity ~6.4Mtpa, utilization >92%.

| Metric | 2024/25 |

|---|---|

| PTA EBITDA | ~22% |

| OCF | RMB28–32bn |

| Net debt/EBITDA | ~1.6x |

What You’re Viewing Is Included

Hengli Petrochemical BCG Matrix

The file you're previewing is the exact Hengli Petrochemical BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document built for strategic clarity and professional presentations.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Hengli Petrochemical’s preliminary BCG Matrix indicates a mix of high-growth polymers likely sitting as Stars, mature refining segments acting as Cash Cows, and smaller niche products that may be Question Marks or Dogs depending on demand cycles; this snapshot highlights strategic allocation needs across its value chain. Purchase the full BCG Matrix to obtain quadrant-level placements, data-backed recommendations, and downloadable Word and Excel files to guide investment and operational decisions with clarity and speed.

Stars

Lithium Battery Separators

Hengli Petrochemical scaled wet- and dry-process lithium battery separator capacity to ~2.4 billion m2/year by end-2025, capturing ~12% share of China’s premium separator market and becoming a key growth engine in premium energy materials.

Revenue from separators rose to RMB 7.8 billion in 2025 (≈USD 1.1 billion), a CAGR ~85% since 2022, driven by EV and ESS demand and long-term offtake contracts with three major automakers.

Hengli deployed ~RMB 18 billion in capex 2023–2025 for advanced coating lines and R&D, positioning its separators as a strategic asset to lead industry decarbonization and margin expansion.

High-End Functional Polyester Films

Hengli Petrochemical dominates China’s BOPET optical/electronic-grade films with an estimated domestic market share ~40% in 2024, supplying high-tech displays and semiconductors as China’s high-end manufacturing grew ~12% YoY in 2024.

The segment generated about RMB 9.2bn revenue in 2024 (≈USD 1.3bn), and Hengli reinvests ~5–7% of segment sales annually into R&D to keep a tech lead over South Korean and Japanese rivals.

High-Performance Engineering Plastics

With full commissioning of new lines in 2024, Hengli Petrochemical’s PBT and PC engineering plastics captured an estimated 12–15% share of China’s automotive-grade polymer market, supplying tier-1 auto makers and electronics firms.

The segment rides the lightweighting trend as global auto polymer parts grew ~8% CAGR 2020–2025, replacing metals with high-strength polymers and boosting ASPs by ~6% in 2024.

High downstream growth (EV and 5G hardware demand up ~10–12% annually) forces Hengli to reinvest ~¥3–4 billion per major line cycle to keep capacity and tech leadership.

Integrated Refining-Chemical-Material Hubs

Hengli Petrochemical’s 20 million tpa integrated refining-chemical-material hub is a star: it converts crude into high-margin aromatics and polyesters, supplying >60% of the company’s premium feedstocks and supporting 2024 EBITDA contribution of roughly RMB 25–30 billion.

The tight upstream-downstream link raises conversion efficiency ~20% vs peers, secures scale-based pricing power, and positions Hengli to capture projected 3–4% annual growth in global specialty chemicals through 2028.

Synergy locks-in market dominance in high-end polymers and intermediates, cutting unit costs and boosting ROIC above industry averages; capital intensity matched by long-term offtake contracts and vertical integration benefits.

- 20 million tpa integrated capacity

- ~60% premium feedstock share

- 2024 EBITDA ~RMB 25–30bn

- ~20% higher conversion efficiency vs peers

- 3–4% annual specialty chemical market growth to 2028

Specialty Fine Chemicals

Hengli Petrochemical’s push into specialty fine chemicals—high-purity solvents and additives—targets pharma and electronics, where global demand grew ~7–9% CAGR through 2024; Hengli reported these lines achieved ~15% domestic market share by Q3 2025.

Heavy R&D spend (~3–4% of sales in 2024) is offset by >30% revenue growth in these products in 2024–2025, helped by integrated feedstock supply and margin expansion versus commodity petrochemicals.

- Targets: pharma, electronics

- Market share: ~15% domestic (Q3 2025)

- Revenue growth: >30% (2024–2025)

- R&D: ~3–4% of sales (2024)

- Advantage: integrated raw-material supply

Hengli’s 20Mtpa integrated hub fuels margin, market share with RMB18bn capex & strong R&D

Hengli’s Stars: integrated 20Mtpa hub (2024 EBITDA RMB25–30bn), separators capacity ~2.4bn m2/yr (2025) with RMB7.8bn revenue (2025), BOPET ~40% domestic share (2024) with RMB9.2bn revenue (2024), PBT/PC ~12–15% auto polymer share (2024); heavy capex RMB18bn (2023–25) and R&D 3–7% of sales drive margin and share gains.

| Metric | Value |

|---|---|

| Integrated capacity | 20Mtpa |

| Separators rev | RMB7.8bn (2025) |

| BOPET share | ~40% (2024) |

| Capex 2023–25 | RMB18bn |

What is included in the product

Comprehensive BCG Matrix review of Hengli Petrochemical: quadrant insights, strategic moves to invest, hold or divest, and trend-driven risks/opportunities.

One-page BCG matrix placing Hengli Petrochemical units in clear quadrants for fast strategic decisions and investor briefs.

Cash Cows

Purified Terephthalic Acid Production

Hengli Petrochemical is a global PTA leader with ~6.4 million tpa installed capacity in 2025, among the world’s largest and lowest-cost producers, driving margin resilience (2024 PTA EBITDA margin ~22%).

Polyester market maturity means PTA is a cash cow: scale, continuous processes, and feedstock integration produced RMB 38.7 billion operating cash flow in 2024.

Those cash flows fund capex into battery materials and specialty films—Hengli allocated RMB 21.5 billion to new-materials R&D and projects in 2024–25.

Refining and Ethylene Units

Hengli Petrochemical’s refining and ethylene units run at >92% utilization (2024), processing ~24 million tonnes crude/year and supplying feedstock across its polyester chain, giving stable, high-volume cash flows in a mature fuels and petrochemicals market.

Optimized crude sourcing and logistics cut feedstock costs ~6% vs peers (2024), lifting refinery EBITDA margins to ~14% and olefins margins to ~18%, driving strong free cash flow.

Given mature demand for fuels and basic ethylene, capex on these assets was just 1–2% of revenues in 2024, so they generate excess cash requiring minimal new investment relative to returns.

Conventional Polyester Chips

Conventional polyester chips (standard-grade) hold a leading market share in a low-growth textile and packaging market, with global polyester demand growth ~1.5% in 2024 and China consumption ~35 Mt; Hengli’s share in China’s chip market exceeded 12% in 2024, placing it as a cash cow.

Hengli’s vertical integration—feedstock-to-chip—kept 2024 unit COGS ~8–12% below peers, letting it partially set prices in a mature spot market where ASPs fell 3% YoY in 2024.

The segment generated ~RMB 28–32 billion operating cash flow in 2024, funding debt service (net debt/EBITDA ~1.6x) and sustaining dividends without tapping capex budgets.

Civilian Polyester Filament

Civilian polyester filament is a classic cash cow for Hengli Petrochemical: Hengli held roughly 28% share of China apparel-grade polyester filament capacity in 2024 and reported RMB 12.4 billion in yarn sales in FY2024, delivering steady EBITDA margins near 18% as clothing demand grows ~2–3% annually—focus is on cost cuts and throughput rather than expansion.

- Market share ~28% (China, 2024)

- Yarn sales RMB 12.4bn (FY2024)

- EBITDA margin ~18%

- Clothing demand growth 2–3% p.a.

- Low capex; strong free cash flow

Industrial Polyester Yarn

Industrial polyester yarn, used mainly in automotive tires and infrastructure, is a Hengli Petrochemical cash cow with stable volumes—Hengli reported ~1.2 million tonnes polyester filament capacity in 2024 supporting steady EBITDA margins near 18% for yarn-related operations.

Quality consistency and long-term supply contracts with global tire and construction manufacturers secure high barriers to entry, generating predictable free cash flow that funds Hengli’s moves into higher-growth, higher-volatility segments.

- Primary end-markets: tires, infrastructure

- 2024 yarn capacity ~1.2 Mt

- Approx. EBITDA margin ~18% (yarn ops, 2024)

- Long-term contracts with global OEMs

Hengli cash cows: strong PTA/refining margins, RMB28–32bn OCF, low leverage

Hengli’s polyester/PTA/refining lines are cash cows: 2024 PTA EBITDA ~22%, refinery EBITDA ~14%, segment OCF ~RMB28–32bn, net debt/EBITDA ~1.6x, China chip share >12%, filament share ~28%, yarn sales RMB12.4bn, 2025 PTA capacity ~6.4Mtpa, utilization >92%.

| Metric | 2024/25 |

|---|---|

| PTA EBITDA | ~22% |

| OCF | RMB28–32bn |

| Net debt/EBITDA | ~1.6x |

What You’re Viewing Is Included

Hengli Petrochemical BCG Matrix

The file you're previewing is the exact Hengli Petrochemical BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document built for strategic clarity and professional presentations.