HEXPOL PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Uncover how political shifts, economic cycles, and emerging technologies are reshaping HEXPOL’s competitive landscape with our concise PESTLE snapshot—designed to spark actionable strategy and investment decisions; buy the full PESTLE for the complete, editable analysis and deeper insights you can use immediately.

Political factors

Global Trade Protectionism and Tariffs

As of late 2025 the rise in trade barriers and regional tariffs between the US, EU and China has increased input costs for HEXPOL, with average import duties on chemical precursors rising by about 4–6 percentage points in contested categories and adding an estimated €15–25m in annual supply-chain costs company-wide.

Tariff volatility exposes HEXPOL to sudden margin compression on specialized rubber compounds, with lead-time-sensitive shipments facing duty swings up to 8% during geopolitical spikes in 2024–25.

HEXPOL mitigates these risks through a decentralized manufacturing footprint of over 40 plants across 20 countries, producing closer to end customers to cut reliance on sensitive trade corridors and lower cross-border sourcing by an estimated 12% of volume.

Geopolitical Stability in Manufacturing Hubs

The stability of regions housing HEXPOLs large compounding plants—notably in Malaysia, the US and Thailand, which accounted for roughly 60% of 2024 production capacity—is critical to uninterrupted output; political unrest or regime shifts in emerging markets can prompt abrupt labor-law changes and infrastructure failures that risk supply chain delays. HEXPOL monitors regional political indicators and allocates assets to keep geographic concentration below 30% per region, using diversification to protect market leadership amid volatility.

Government Incentives for Electrification

Political mandates and subsidies accelerating EV adoption—EU aiming for 100% zero-emission new car sales by 2035 and several countries advancing ICE phase-outs to 2025—boost demand for HEXPOL’s polymer gaskets and seals used in battery thermal management; global EV sales reached ~14 million in 2023 and 2024 growth estimates projected ~20% YoY. HEXPOL targets R&D to capture these high-growth segments and is a preferred OEM partner meeting stricter efficiency rules.

Supply Chain De-risking Policies

- 22% rise in friend-shoring incentives (2025 OECD data)

- HEXPOL presence in stable regions = higher eligibility for subsidies

- Defense/critical infrastructure spending +8% (2024–25)

- Improved access to government contracts and strategic procurement

Defense and Aerospace Strategic Spending

Rising global defense budgets—projected at a 3.6% CAGR to 2025 with total spending near $2.2 trillion in 2024—boost demand for high-performance engineered polymers, where HEXPOL supplies materials meeting MIL-STD durability and heat-resistance specs.

Compliance with stringent government procurement rules enables HEXPOL to secure multi-year, high-margin aerospace and defense contracts, supporting sustained growth in its engineered products division as national defense priorities rise.

- Global defense spend ~ $2.2T (2024); 3.6% CAGR to 2025

- HEXPOL supplies MIL-STD-grade polymers for heat/durability

- Government procurement compliance → multi-year contracts

- Defense/aerospace = high-margin, stable revenue stream

Geopolitical costs raise €15–25m; friend‑shoring +22% and defense demand boosts HEXPOL

Political risks (trade barriers, duty swings) raised supply-chain costs ~€15–25m and duty volatility up to 8% (2024–25); friend‑shoring incentives rose 22% (2025 OECD); defense spending ~ $2.2T (2024) at 3.6% CAGR to 2025, boosting demand for MIL‑STD polymers; HEXPOL’s 40+ plants across 20 countries and <30% regional concentration mitigate disruption and increase subsidy/contract eligibility.

| Metric | Value |

|---|---|

| Added supply-chain cost | €15–25m |

| Duty volatility | up to 8% |

| Friend‑shoring incentives | +22% (2025) |

| Defense spend | $2.2T (2024) |

| Plants / countries | 40+ / 20 |

What is included in the product

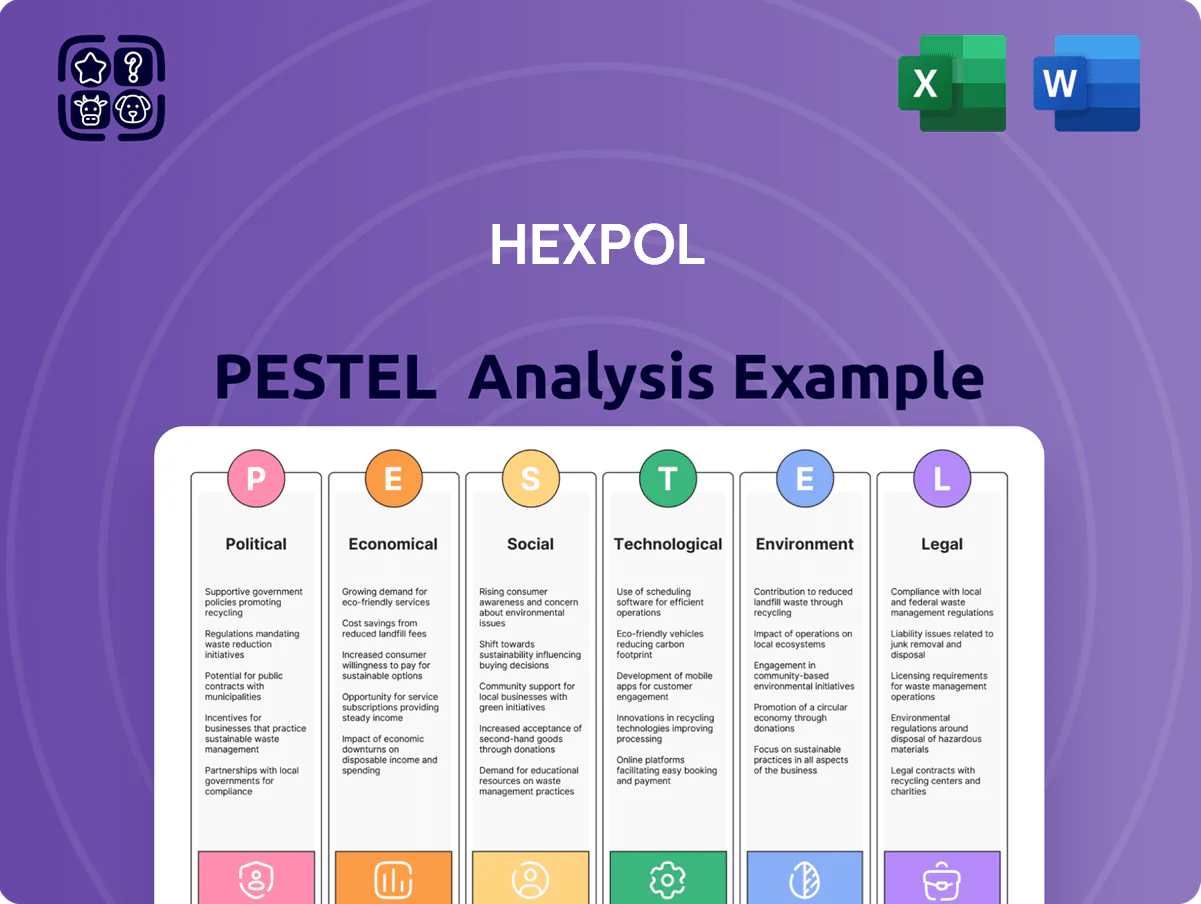

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact HEXPOL’s polymer and rubber businesses, with data-driven trends and region-specific regulatory context.

Provides a clean, summarized PESTLE of HEXPOL for quick reference in meetings, visually segmented for instant interpretation and easily dropped into PowerPoints or shared across teams to support risk discussions and strategic alignment.

Economic factors

Raw Material Price Volatility

Raw material price volatility, especially synthetic rubber and oil-based feedstocks, remained a key profitability driver for HEXPOL in late 2025 as crude oil swings of ±20% year-on-year pushed COGS; Brent averaged about 82–95 USD/bbl in 2024–2025, contributing to input-cost inflation of roughly 6–9% for polymer inputs.

Global Interest Rate Environments

Central bank tightening into late 2025—with the ECB policy rate around 3.75% and the Fed funds rate near 5.25%—has constrained capex in construction and automotive, slowing demand for polymer components and elongating order cycles for HEXPOL.

Higher borrowing costs depress industry investment, yet HEXPOL’s net debt/EBITDA near 0.3x and liquid cash positions above SEK 1.5bn (2024 figures) give it acquisition firepower when competitors face expensive financing.

This financial resilience lets HEXPOL press on with targeted capacity expansions and strategic M&A despite a tighter rate environment that may force rivals to retrench.

Currency Exchange Rate Fluctuations

As a Swedish-headquartered group with global operations, HEXPOL faces translation and transaction risks across SEK, USD and EUR; in 2024 FX effects swung reported EBIT by about SEK 120m versus 2023, per interim reports.

Significant exchange moves can erode export competitiveness at specific plants—a 10% SEK weakening vs USD/EUR materially shifts margins on US/EU sales from Swedish and Eastern European sites.

HEXPOL uses hedging to limit short-term volatility—cash-flow hedges covered roughly 60–70% of near-term exposures in 2024—while persistent currency trends prompt strategic production shifts.

Managing this multi-currency environment is a core competency for HEXPOL’s finance team in 2025, balancing hedging, pricing and relocation to protect reported earnings and operational competitiveness.

Economic Growth in Emerging Markets

Rapid industrialization in Southeast Asia and parts of Latin America has boosted demand for HEXPOL’s polymer solutions, with these regions contributing over 18% of group organic growth by late 2025 as local manufacturing matures.

HEXPOL strategically targets these high-growth markets to offset stagnant Western demand, investing in local technical support and production—adding two plants in Vietnam and Mexico by 2024 and raising regional sales by ~22% year-on-year.

- Emerging markets >18% of organic growth (late 2025)

- Regional sales +22% YoY after local investments

- Two new plants (Vietnam, Mexico) added by 2024

- Strategy offsets flat Western demand

Labor Market Inflation and Talent Scarcity

- OECD wage growth ~4.0% (2025 est)

- HEXPOL capex SEK 870m (2024)

- Automation reduces labor share in compounding

- Skilled talent scarcity risks innovation and margin pressure

Strong cash, low leverage and capex fueled growth despite oil-driven polymer cost shocks

Input-cost shocks from oil/polymer swings (Brent ~82–95 USD/bbl in 2024–25) raised polymer COGS ~6–9%; FX effects moved EBIT ~SEK 120m (2024 vs 2023); net debt/EBITDA ~0.3x and cash >SEK 1.5bn (2024) enable M&A; emerging markets ≈18% of organic growth (late 2025) while capex rose to SEK 870m (2024) to fund automation amid ~4% OECD wage growth (2025 est).

| Metric | Value |

|---|---|

| Brent (2024–25) | 82–95 USD/bbl |

| Polymer input inflation | 6–9% |

| Net debt/EBITDA | ~0.3x (2024) |

| Cash | >SEK 1.5bn (2024) |

| Capex | SEK 870m (2024) |

| Emerging markets contribution | ~18% organic growth (late 2025) |

| OECD wage growth | ~4.0% (2025 est) |

| FX EBIT swing | ~SEK 120m (2024 vs 2023) |

Preview Before You Purchase

HEXPOL PESTLE Analysis

The preview shown here is the exact HEXPOL PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible in the preview are exactly what you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Uncover how political shifts, economic cycles, and emerging technologies are reshaping HEXPOL’s competitive landscape with our concise PESTLE snapshot—designed to spark actionable strategy and investment decisions; buy the full PESTLE for the complete, editable analysis and deeper insights you can use immediately.

Political factors

Global Trade Protectionism and Tariffs

As of late 2025 the rise in trade barriers and regional tariffs between the US, EU and China has increased input costs for HEXPOL, with average import duties on chemical precursors rising by about 4–6 percentage points in contested categories and adding an estimated €15–25m in annual supply-chain costs company-wide.

Tariff volatility exposes HEXPOL to sudden margin compression on specialized rubber compounds, with lead-time-sensitive shipments facing duty swings up to 8% during geopolitical spikes in 2024–25.

HEXPOL mitigates these risks through a decentralized manufacturing footprint of over 40 plants across 20 countries, producing closer to end customers to cut reliance on sensitive trade corridors and lower cross-border sourcing by an estimated 12% of volume.

Geopolitical Stability in Manufacturing Hubs

The stability of regions housing HEXPOLs large compounding plants—notably in Malaysia, the US and Thailand, which accounted for roughly 60% of 2024 production capacity—is critical to uninterrupted output; political unrest or regime shifts in emerging markets can prompt abrupt labor-law changes and infrastructure failures that risk supply chain delays. HEXPOL monitors regional political indicators and allocates assets to keep geographic concentration below 30% per region, using diversification to protect market leadership amid volatility.

Government Incentives for Electrification

Political mandates and subsidies accelerating EV adoption—EU aiming for 100% zero-emission new car sales by 2035 and several countries advancing ICE phase-outs to 2025—boost demand for HEXPOL’s polymer gaskets and seals used in battery thermal management; global EV sales reached ~14 million in 2023 and 2024 growth estimates projected ~20% YoY. HEXPOL targets R&D to capture these high-growth segments and is a preferred OEM partner meeting stricter efficiency rules.

Supply Chain De-risking Policies

- 22% rise in friend-shoring incentives (2025 OECD data)

- HEXPOL presence in stable regions = higher eligibility for subsidies

- Defense/critical infrastructure spending +8% (2024–25)

- Improved access to government contracts and strategic procurement

Defense and Aerospace Strategic Spending

Rising global defense budgets—projected at a 3.6% CAGR to 2025 with total spending near $2.2 trillion in 2024—boost demand for high-performance engineered polymers, where HEXPOL supplies materials meeting MIL-STD durability and heat-resistance specs.

Compliance with stringent government procurement rules enables HEXPOL to secure multi-year, high-margin aerospace and defense contracts, supporting sustained growth in its engineered products division as national defense priorities rise.

- Global defense spend ~ $2.2T (2024); 3.6% CAGR to 2025

- HEXPOL supplies MIL-STD-grade polymers for heat/durability

- Government procurement compliance → multi-year contracts

- Defense/aerospace = high-margin, stable revenue stream

Geopolitical costs raise €15–25m; friend‑shoring +22% and defense demand boosts HEXPOL

Political risks (trade barriers, duty swings) raised supply-chain costs ~€15–25m and duty volatility up to 8% (2024–25); friend‑shoring incentives rose 22% (2025 OECD); defense spending ~ $2.2T (2024) at 3.6% CAGR to 2025, boosting demand for MIL‑STD polymers; HEXPOL’s 40+ plants across 20 countries and <30% regional concentration mitigate disruption and increase subsidy/contract eligibility.

| Metric | Value |

|---|---|

| Added supply-chain cost | €15–25m |

| Duty volatility | up to 8% |

| Friend‑shoring incentives | +22% (2025) |

| Defense spend | $2.2T (2024) |

| Plants / countries | 40+ / 20 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact HEXPOL’s polymer and rubber businesses, with data-driven trends and region-specific regulatory context.

Provides a clean, summarized PESTLE of HEXPOL for quick reference in meetings, visually segmented for instant interpretation and easily dropped into PowerPoints or shared across teams to support risk discussions and strategic alignment.

Economic factors

Raw Material Price Volatility

Raw material price volatility, especially synthetic rubber and oil-based feedstocks, remained a key profitability driver for HEXPOL in late 2025 as crude oil swings of ±20% year-on-year pushed COGS; Brent averaged about 82–95 USD/bbl in 2024–2025, contributing to input-cost inflation of roughly 6–9% for polymer inputs.

Global Interest Rate Environments

Central bank tightening into late 2025—with the ECB policy rate around 3.75% and the Fed funds rate near 5.25%—has constrained capex in construction and automotive, slowing demand for polymer components and elongating order cycles for HEXPOL.

Higher borrowing costs depress industry investment, yet HEXPOL’s net debt/EBITDA near 0.3x and liquid cash positions above SEK 1.5bn (2024 figures) give it acquisition firepower when competitors face expensive financing.

This financial resilience lets HEXPOL press on with targeted capacity expansions and strategic M&A despite a tighter rate environment that may force rivals to retrench.

Currency Exchange Rate Fluctuations

As a Swedish-headquartered group with global operations, HEXPOL faces translation and transaction risks across SEK, USD and EUR; in 2024 FX effects swung reported EBIT by about SEK 120m versus 2023, per interim reports.

Significant exchange moves can erode export competitiveness at specific plants—a 10% SEK weakening vs USD/EUR materially shifts margins on US/EU sales from Swedish and Eastern European sites.

HEXPOL uses hedging to limit short-term volatility—cash-flow hedges covered roughly 60–70% of near-term exposures in 2024—while persistent currency trends prompt strategic production shifts.

Managing this multi-currency environment is a core competency for HEXPOL’s finance team in 2025, balancing hedging, pricing and relocation to protect reported earnings and operational competitiveness.

Economic Growth in Emerging Markets

Rapid industrialization in Southeast Asia and parts of Latin America has boosted demand for HEXPOL’s polymer solutions, with these regions contributing over 18% of group organic growth by late 2025 as local manufacturing matures.

HEXPOL strategically targets these high-growth markets to offset stagnant Western demand, investing in local technical support and production—adding two plants in Vietnam and Mexico by 2024 and raising regional sales by ~22% year-on-year.

- Emerging markets >18% of organic growth (late 2025)

- Regional sales +22% YoY after local investments

- Two new plants (Vietnam, Mexico) added by 2024

- Strategy offsets flat Western demand

Labor Market Inflation and Talent Scarcity

- OECD wage growth ~4.0% (2025 est)

- HEXPOL capex SEK 870m (2024)

- Automation reduces labor share in compounding

- Skilled talent scarcity risks innovation and margin pressure

Strong cash, low leverage and capex fueled growth despite oil-driven polymer cost shocks

Input-cost shocks from oil/polymer swings (Brent ~82–95 USD/bbl in 2024–25) raised polymer COGS ~6–9%; FX effects moved EBIT ~SEK 120m (2024 vs 2023); net debt/EBITDA ~0.3x and cash >SEK 1.5bn (2024) enable M&A; emerging markets ≈18% of organic growth (late 2025) while capex rose to SEK 870m (2024) to fund automation amid ~4% OECD wage growth (2025 est).

| Metric | Value |

|---|---|

| Brent (2024–25) | 82–95 USD/bbl |

| Polymer input inflation | 6–9% |

| Net debt/EBITDA | ~0.3x (2024) |

| Cash | >SEK 1.5bn (2024) |

| Capex | SEK 870m (2024) |

| Emerging markets contribution | ~18% organic growth (late 2025) |

| OECD wage growth | ~4.0% (2025 est) |

| FX EBIT swing | ~SEK 120m (2024 vs 2023) |

Preview Before You Purchase

HEXPOL PESTLE Analysis

The preview shown here is the exact HEXPOL PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible in the preview are exactly what you’ll download immediately after payment.