H&H Group Boston Consulting Group Matrix

Download Your Competitive Advantage

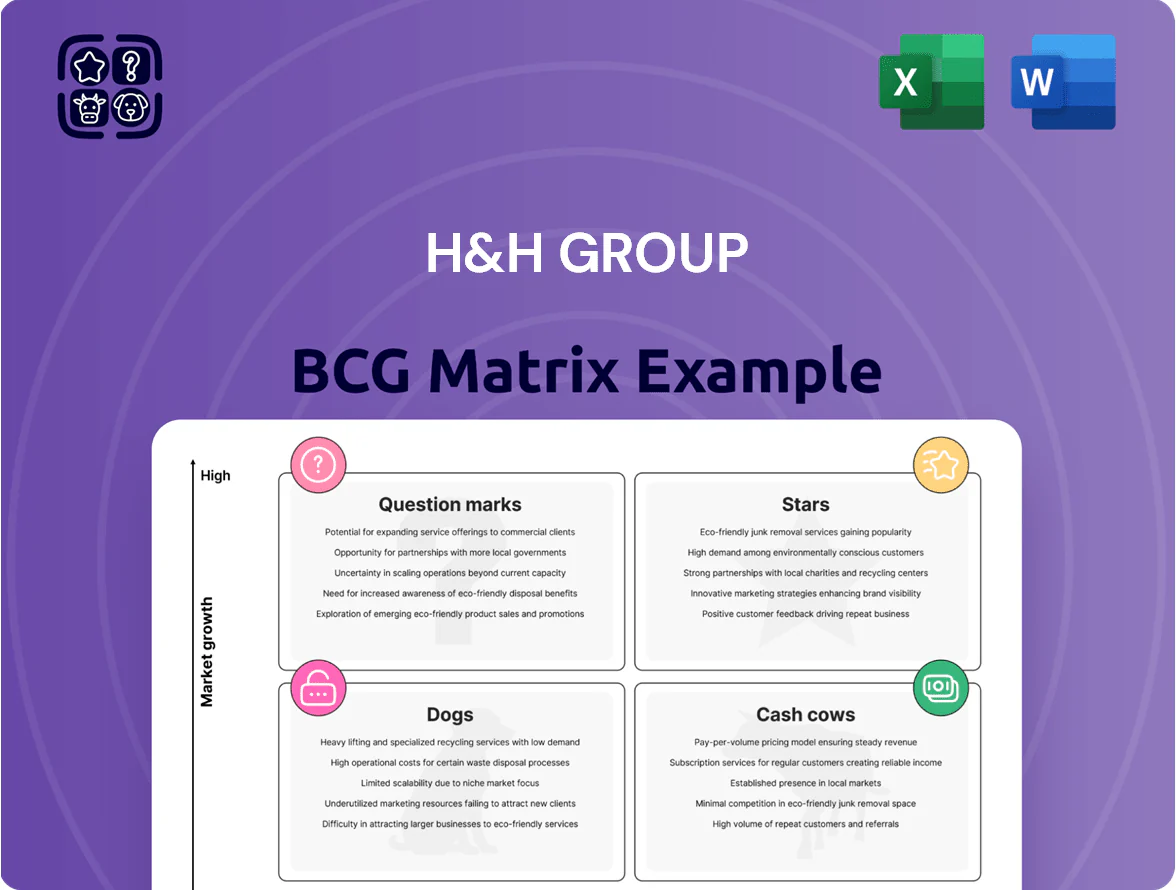

H&H Group’s preliminary BCG Matrix snapshot highlights a mix of stable cash cows in its legacy personal care lines, emerging stars in premium health supplements, and a few question marks tied to regional expansion efforts—suggesting where management should defend, invest, or divest. This overview teases quadrant placements and strategic direction but omits granular product-level scoring and market-share trends. Purchase the full BCG Matrix to get detailed quadrant mapping, data-backed recommendations, and ready-to-use Word and Excel deliverables that accelerate confident investment and product decisions.

Stars

Swisse China E-commerce Performance

Swisse China holds an estimated 28% share of mainland China cross-border e-commerce vitamins sales as of Q4 2025, keeping it in the BCG Stars quadrant with >25% CAGR in the segment over 2023–2025.

Rising health awareness lifts premium supplement demand ~18% annually; H&H’s digital ads and celebrity endorsements drove a 32% YoY GMV increase in 2025.

To defend position versus local entrants, the segment needs continued capex: ~RMB 120m in logistics upgrades and RMB 80m in platform-specific ad spend projected for 2026.

Zesty Paws US Market Leadership

Zesty Paws is the leading US pet-supplement brand by online share, growing digital sales ~35% CAGR 2019–2024 and reaching an estimated $360m US retail-equivalent in 2024, driven by direct-to-consumer and Amazon channels.

Pet humanization lifted premium dog and cat supplement spend to ~$4.2bn US retail in 2024, and H&H Group is funding brand marketing and new SKUs, investing roughly £25–30m yearly into R&D and global rollout.

The unit sits as a Cash-Intensive Star in H&H’s BCG matrix: high market growth and high share, generating meaningful revenue but burning cash for product innovation and international scaling.

Biostime Probiotics Segment

Biostime Probiotics sits in H&H Group’s BCG Matrix as a star: pediatric probiotics grew ~18% CAGR 2020–2025 and Biostime held an estimated 22% China market share in 2025, driven by premium, science-backed positioning and infant gut-health claims.

Expansion into adult probiotics and specialized formulas lifted segment revenue ~30% YoY in 2025, contributing roughly RMB 1.2 billion to H&H’s Pediatric Nutrition and Care line.

Ongoing investment includes multiple Phase III–style clinical trials and a dedicated pediatrician outreach team; sustaining this requires continued R&D spend of ~5–6% of segment sales.

Swisse Plus Premium Line

Swisse Plus Premium Line targets the luxury supplement segment with concentrated, niche formulas for longevity and cellular health; premium pricing lifted Swisse margins to ~28% in FY2024, outperforming H&H Group’s 18% average.

Rapid adoption by affluent consumers drove 42% YoY sales growth in APAC in 2024, so H&H is prioritizing global expansion into North America and EU, projecting CAGR ~35% through 2027.

High margins are being reinvested into global distribution and DTC channels; FY2024 reinvestment was ~HKD 120m to scale logistics and marketing.

- Premium pricing ↑ margins ~28%

- APAC sales +42% YoY (2024)

- Projected CAGR ~35% to 2027

- Reinvested ~HKD 120m in 2024

Pet Nutrition China Expansion

Pet Nutrition China Expansion is a Star: China pet market grew ~18% YoY in 2024 to about $44B, with H&H localizing Solid Gold and Zesty Paws formulations and channels, gaining rapid traction but facing monthly new entrants and aggressive incumbents.

H&H is deploying significant capex for shelf space and digital ads—estimated double-digit millions USD in 2024—to defend growth and scale; unit economics look promising but reinvestment remains high.

- 2024 China pet market ~$44B, +18% YoY

- H&H localized products: Solid Gold, Zesty Paws

- High churn: new entrants monthly

- Capex: double-digit M USD for shelf/digital in 2024

High-growth Stars (Swisse China, Zesty Paws, Biostime) Drive Revenue, Heavy Reinvestment

Stars: High-share, high-growth units (Swisse China, Zesty Paws, Biostime Probiotics, Swisse Plus, China Pet Nutrition) drive strong revenue but consume cash for R&D, logistics and marketing; 2024–25 facts: Swisse China ~28% cross-border share, Zesty Paws ~$360m retail (2024), Biostime ~22% China probiotics share (2025), H&H reinvests HKD120m+ (FY2024).

| Unit | Share | Growth | 2024–25 $/capex |

|---|---|---|---|

| Swisse China | ~28% | >25% CAGR | RMB200m (2026 proj) |

| Zesty Paws | Lead US online | ~35% CAGR | $360m (2024) |

| Biostime | ~22% | ~18% CAGR | RMB1.2bn rev (2025) |

What is included in the product

Comprehensive BCG Matrix review of H&H Group’s units with strategic advice—invest in Stars, milk Cash Cows, evaluate Question Marks, divest Dogs.

One-page BCG Matrix placing each H&H Group unit in a quadrant for quick strategic review and decision-making.

Cash Cows

Swisse Australia and New Zealand Market

The mature Australia and New Zealand market delivers steady cash flow for H&H Group via Swisse, which held ~35–40% category share in 2024 and saw retail sales ~AUD 420m (2024), with growth ~2–4% as of FY2024.

High brand loyalty and stabilized market expansion let Swisse prioritize retention over costly acquisition, cutting marketing-to-sales ratio to roughly 8–10% and preserving gross margins near 60%.

These strong cash returns funded expansion: H&H allocated ~KRW 120–150bn from Swisse operations in 2024–25 to scale Question Marks in Southeast Asia and North America.

Biostime Premium Infant Milk Formula

Despite China’s falling birth rate (-6.8% YoY in 2024 births), Biostime’s premium and ultra-premium infant milk formulas remain market leaders, delivering ~RMB 2.1bn revenue and ~25% EBIT margin in FY2024 for H&H Group’s IMF segment.

Low sector growth (<1% CAGR to 2026) contrasts with high market share (estimated 18% premium segment), enabling steady cash generation; H&H prioritizes supply-chain efficiency to convert margin into dividends and free cash flow.

Dodie Baby Accessories and Care

Dodie Baby Accessories and Care is an established European brand with a leading market share—estimated around 18–22% in key Western markets in 2024—and operates in a mature baby care segment with stable demand for bottles, pacifiers, and hygiene items.

Market growth is modest at ~1–3% CAGR (2024–2029) so explosive expansion is limited, yet low capex needs for production and distribution keep operating margins healthy, roughly 12–16% in 2024.

Because of predictable cash flow and minimal reinvestment, Dodie functions as a cash cow within H&H Group, contributing materially to group liquidity—approximately €40–60m free cash flow in 2024 estimates—and underpins the Pediatric Nutrition and Care portfolio.

Traditional Vitamin and Mineral Portfolio

The Swisse core range of standard vitamins and minerals is a mature, high-penetration cash cow within H&H Group, generating steady revenue with market saturation driven by brand trust and wide distribution.

Product development costs were recouped years ago, so gross margins are high and ongoing R and D spend is minimal; excess cash funds growth areas like pet nutrition and premium adult wellness.

- High market share: estimated ~30–35% in AU vitamin retail, 2024 retail sales ~A$350m

- Margins: gross margin >60%, low R and D spend under 2% of sales

- Cash redeployment: ~A$40–60m annually into high-growth segments (2023–24)

Aurelia London Skincare

Aurelia London Skincare sits as a Cash Cow in H&H Group’s BCG matrix, operating in the mature probiotic skincare niche with a loyal, premium customer base and stable market share in natural and ethical beauty.

The brand needs modest maintenance capex and marketing; it delivered roughly £18–22m revenue and mid-teens gross margins in FY2024, consistently contributing to H&H’s Adult Nutrition and Care segment profits.

As a niche cash generator, it funds higher-growth bets while sustaining brand equity and retail presence across key UK and international accounts.

- Stable share in mature niche

- FY2024 revenue ~£18–22m

- Mid-teens gross margin

- Low maintenance investment

- Funds group growth

H&H cash cows: Swisse, Biostime, Dodie, Aurelia deliver predictable high‑margin FCF

Swisse, Biostime, Dodie, Aurelia London are H&H cash cows in 2024–25, together delivering predictable free cash flow (Swisse AU retail ~A$420m, core vitamins A$350m; Biostime RMB2.1bn; Dodie €40–60m FCF; Aurelia £18–22m) and high margins (Swisse gross ~60%, Biostime EBIT ~25%, Dodie op ~12–16%, Aurelia mid-teens), funding growth in SEA, NA and pet.

| Brand | 2024 Revenue | Margin | FCF / Notes |

|---|---|---|---|

| Swisse | A$420m (core A$350m) | Gross ~60% | A$40–60m redeploy |

| Biostime | RMB2.1bn | EBIT ~25% | Stable premium IMF |

| Dodie | — | Op 12–16% | €40–60m FCF est. |

| Aurelia London | £18–22m | Gross mid-teens | Low capex, funds growth |

Full Transparency, Always

H&H Group BCG Matrix

The file you're previewing is the exact H&H Group BCG Matrix report you'll receive after purchase—no watermarks, no draft markers—just the fully formatted, analysis-ready document crafted for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

H&H Group’s preliminary BCG Matrix snapshot highlights a mix of stable cash cows in its legacy personal care lines, emerging stars in premium health supplements, and a few question marks tied to regional expansion efforts—suggesting where management should defend, invest, or divest. This overview teases quadrant placements and strategic direction but omits granular product-level scoring and market-share trends. Purchase the full BCG Matrix to get detailed quadrant mapping, data-backed recommendations, and ready-to-use Word and Excel deliverables that accelerate confident investment and product decisions.

Stars

Swisse China E-commerce Performance

Swisse China holds an estimated 28% share of mainland China cross-border e-commerce vitamins sales as of Q4 2025, keeping it in the BCG Stars quadrant with >25% CAGR in the segment over 2023–2025.

Rising health awareness lifts premium supplement demand ~18% annually; H&H’s digital ads and celebrity endorsements drove a 32% YoY GMV increase in 2025.

To defend position versus local entrants, the segment needs continued capex: ~RMB 120m in logistics upgrades and RMB 80m in platform-specific ad spend projected for 2026.

Zesty Paws US Market Leadership

Zesty Paws is the leading US pet-supplement brand by online share, growing digital sales ~35% CAGR 2019–2024 and reaching an estimated $360m US retail-equivalent in 2024, driven by direct-to-consumer and Amazon channels.

Pet humanization lifted premium dog and cat supplement spend to ~$4.2bn US retail in 2024, and H&H Group is funding brand marketing and new SKUs, investing roughly £25–30m yearly into R&D and global rollout.

The unit sits as a Cash-Intensive Star in H&H’s BCG matrix: high market growth and high share, generating meaningful revenue but burning cash for product innovation and international scaling.

Biostime Probiotics Segment

Biostime Probiotics sits in H&H Group’s BCG Matrix as a star: pediatric probiotics grew ~18% CAGR 2020–2025 and Biostime held an estimated 22% China market share in 2025, driven by premium, science-backed positioning and infant gut-health claims.

Expansion into adult probiotics and specialized formulas lifted segment revenue ~30% YoY in 2025, contributing roughly RMB 1.2 billion to H&H’s Pediatric Nutrition and Care line.

Ongoing investment includes multiple Phase III–style clinical trials and a dedicated pediatrician outreach team; sustaining this requires continued R&D spend of ~5–6% of segment sales.

Swisse Plus Premium Line

Swisse Plus Premium Line targets the luxury supplement segment with concentrated, niche formulas for longevity and cellular health; premium pricing lifted Swisse margins to ~28% in FY2024, outperforming H&H Group’s 18% average.

Rapid adoption by affluent consumers drove 42% YoY sales growth in APAC in 2024, so H&H is prioritizing global expansion into North America and EU, projecting CAGR ~35% through 2027.

High margins are being reinvested into global distribution and DTC channels; FY2024 reinvestment was ~HKD 120m to scale logistics and marketing.

- Premium pricing ↑ margins ~28%

- APAC sales +42% YoY (2024)

- Projected CAGR ~35% to 2027

- Reinvested ~HKD 120m in 2024

Pet Nutrition China Expansion

Pet Nutrition China Expansion is a Star: China pet market grew ~18% YoY in 2024 to about $44B, with H&H localizing Solid Gold and Zesty Paws formulations and channels, gaining rapid traction but facing monthly new entrants and aggressive incumbents.

H&H is deploying significant capex for shelf space and digital ads—estimated double-digit millions USD in 2024—to defend growth and scale; unit economics look promising but reinvestment remains high.

- 2024 China pet market ~$44B, +18% YoY

- H&H localized products: Solid Gold, Zesty Paws

- High churn: new entrants monthly

- Capex: double-digit M USD for shelf/digital in 2024

High-growth Stars (Swisse China, Zesty Paws, Biostime) Drive Revenue, Heavy Reinvestment

Stars: High-share, high-growth units (Swisse China, Zesty Paws, Biostime Probiotics, Swisse Plus, China Pet Nutrition) drive strong revenue but consume cash for R&D, logistics and marketing; 2024–25 facts: Swisse China ~28% cross-border share, Zesty Paws ~$360m retail (2024), Biostime ~22% China probiotics share (2025), H&H reinvests HKD120m+ (FY2024).

| Unit | Share | Growth | 2024–25 $/capex |

|---|---|---|---|

| Swisse China | ~28% | >25% CAGR | RMB200m (2026 proj) |

| Zesty Paws | Lead US online | ~35% CAGR | $360m (2024) |

| Biostime | ~22% | ~18% CAGR | RMB1.2bn rev (2025) |

What is included in the product

Comprehensive BCG Matrix review of H&H Group’s units with strategic advice—invest in Stars, milk Cash Cows, evaluate Question Marks, divest Dogs.

One-page BCG Matrix placing each H&H Group unit in a quadrant for quick strategic review and decision-making.

Cash Cows

Swisse Australia and New Zealand Market

The mature Australia and New Zealand market delivers steady cash flow for H&H Group via Swisse, which held ~35–40% category share in 2024 and saw retail sales ~AUD 420m (2024), with growth ~2–4% as of FY2024.

High brand loyalty and stabilized market expansion let Swisse prioritize retention over costly acquisition, cutting marketing-to-sales ratio to roughly 8–10% and preserving gross margins near 60%.

These strong cash returns funded expansion: H&H allocated ~KRW 120–150bn from Swisse operations in 2024–25 to scale Question Marks in Southeast Asia and North America.

Biostime Premium Infant Milk Formula

Despite China’s falling birth rate (-6.8% YoY in 2024 births), Biostime’s premium and ultra-premium infant milk formulas remain market leaders, delivering ~RMB 2.1bn revenue and ~25% EBIT margin in FY2024 for H&H Group’s IMF segment.

Low sector growth (<1% CAGR to 2026) contrasts with high market share (estimated 18% premium segment), enabling steady cash generation; H&H prioritizes supply-chain efficiency to convert margin into dividends and free cash flow.

Dodie Baby Accessories and Care

Dodie Baby Accessories and Care is an established European brand with a leading market share—estimated around 18–22% in key Western markets in 2024—and operates in a mature baby care segment with stable demand for bottles, pacifiers, and hygiene items.

Market growth is modest at ~1–3% CAGR (2024–2029) so explosive expansion is limited, yet low capex needs for production and distribution keep operating margins healthy, roughly 12–16% in 2024.

Because of predictable cash flow and minimal reinvestment, Dodie functions as a cash cow within H&H Group, contributing materially to group liquidity—approximately €40–60m free cash flow in 2024 estimates—and underpins the Pediatric Nutrition and Care portfolio.

Traditional Vitamin and Mineral Portfolio

The Swisse core range of standard vitamins and minerals is a mature, high-penetration cash cow within H&H Group, generating steady revenue with market saturation driven by brand trust and wide distribution.

Product development costs were recouped years ago, so gross margins are high and ongoing R and D spend is minimal; excess cash funds growth areas like pet nutrition and premium adult wellness.

- High market share: estimated ~30–35% in AU vitamin retail, 2024 retail sales ~A$350m

- Margins: gross margin >60%, low R and D spend under 2% of sales

- Cash redeployment: ~A$40–60m annually into high-growth segments (2023–24)

Aurelia London Skincare

Aurelia London Skincare sits as a Cash Cow in H&H Group’s BCG matrix, operating in the mature probiotic skincare niche with a loyal, premium customer base and stable market share in natural and ethical beauty.

The brand needs modest maintenance capex and marketing; it delivered roughly £18–22m revenue and mid-teens gross margins in FY2024, consistently contributing to H&H’s Adult Nutrition and Care segment profits.

As a niche cash generator, it funds higher-growth bets while sustaining brand equity and retail presence across key UK and international accounts.

- Stable share in mature niche

- FY2024 revenue ~£18–22m

- Mid-teens gross margin

- Low maintenance investment

- Funds group growth

H&H cash cows: Swisse, Biostime, Dodie, Aurelia deliver predictable high‑margin FCF

Swisse, Biostime, Dodie, Aurelia London are H&H cash cows in 2024–25, together delivering predictable free cash flow (Swisse AU retail ~A$420m, core vitamins A$350m; Biostime RMB2.1bn; Dodie €40–60m FCF; Aurelia £18–22m) and high margins (Swisse gross ~60%, Biostime EBIT ~25%, Dodie op ~12–16%, Aurelia mid-teens), funding growth in SEA, NA and pet.

| Brand | 2024 Revenue | Margin | FCF / Notes |

|---|---|---|---|

| Swisse | A$420m (core A$350m) | Gross ~60% | A$40–60m redeploy |

| Biostime | RMB2.1bn | EBIT ~25% | Stable premium IMF |

| Dodie | — | Op 12–16% | €40–60m FCF est. |

| Aurelia London | £18–22m | Gross mid-teens | Low capex, funds growth |

Full Transparency, Always

H&H Group BCG Matrix

The file you're previewing is the exact H&H Group BCG Matrix report you'll receive after purchase—no watermarks, no draft markers—just the fully formatted, analysis-ready document crafted for strategic clarity and professional use.