H&H Group PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Uncover how political shifts, economic headwinds, and evolving consumer trends are reshaping H&H Group’s prospects—our concise PESTLE snapshot highlights key external risks and opportunities to inform smarter decisions; purchase the full PESTLE for a detailed, actionable report you can download and deploy immediately.

Political factors

Geopolitical trade relations

Trade dynamics between China, Australia and the US materially affect H&H Group; in FY2024 ~63% of revenue came from China while Australia hosts major production, so tariff shifts alter landed costs for Swisse and Biostime and can swing gross margins by several percentage points.

Recent China-Australia tensions and US-China trade measures raised compliance costs and logistics premiums—container rates spiked 40% in 2023—pressuring supply-chain predictability for H&H.

Management is diversifying manufacturing beyond Australia and China and reported CAPEX of HKD 820m in 2024 to expand Southeast Asian capacity, while prioritizing local government engagement to mitigate tariff and access risks.

Regulatory registration policies

The Chinese government tightened infant formula registration via the State Administration for Market Regulation, raising technical and safety criteria; H&H Group must ensure Biostime meets evolving national standards to retain mainland licenses. Non-compliance risks major Pediatric Nutrition revenue—China accounted for about 45% of H&H’s FY2024 revenue (≈HKD 5.9bn), so regulatory loss could be material. A proactive government affairs strategy and monitoring of local legislative cycles are therefore essential.

Government health initiatives

National health agendas like Healthy China 2030, targeting a 30% reduction in major chronic disease burden by 2030, create a supportive political backdrop for H&H Group’s Adult Nutrition and Care segment.

Global shifts toward preventative healthcare—governments aiming to cut long‑term care costs (OECD estimates prevention could save up to 10% of health spending)—align with H&H’s wellness mission.

Positioning supplements as public‑health tools may unlock favorable policies and institutional procurement, supporting partnerships and revenue visibility.

Political alignment stabilizes long‑term growth across mature and emerging markets, aiding H&H’s FY2024–25 expansion plans and margin targets.

Global food security and sovereignty

Rising political emphasis on food security is prompting protectionist policies; in 2024 over 40 countries introduced measures favoring domestic food production, affecting global nutritional supply chains.

Regions now incentivize local sourcing—e.g., EU and Brazil support domestic milk and pet-food ingredient procurement—reducing import reliance and raising input-cost risk for H&H.

H&H must balance global sourcing with local investment: strategic localization of select production lines (estimated capex of 5–10% of annual manufacturing spend) can hedge sovereignty-driven legislation.

- Protectionism rising: 40+ countries (2024) with food-security measures

- Local sourcing incentives in EU/Brazil target milk and pet ingredients

- H&H should localize select lines; capex ~5–10% manufacturing spend

Economic stability in key markets

Political stability in the Eurozone and Southeast Asia influences H&H Group’s consumer demand and operations; Eurozone GDP growth slowed to 0.7% in 2024 while ASEAN combined growth was ~4.5%, affecting regional sales forecasts.

Conflicts raise logistics disruption risk and insurance costs—global marine insurance rates rose ~18% in 2024—prompting higher security spend and supply-chain resilience measures.

The group actively monitors political risk to reallocate marketing and cut inventory exposure; stable markets enable predictable capex and 3–5 year strategic planning.

- Eurozone GDP 2024: 0.7%

- ASEAN GDP 2024: ~4.5%

- Marine insurance rates increase 2024: ~18%

- Adjustments: marketing, inventory, security, capex horizon 3–5 years

H&H margins squeezed as trade tensions, tariffs and China rules force HKD820m localization

Political risks—trade tensions, tariff shifts and tightened Chinese infant‑formula rules—directly affect H&H’s margins and China revenue (FY2024 China ≈63% group revenue; Pediatric Nutrition ≈45%, ~HKD5.9bn). Rising protectionism (40+ countries, 2024) and higher logistics/insurance costs (container +40% in 2023; marine insurance +18% in 2024) drive localization capex (HKD820m FY2024).

| Metric | 2023–24 |

|---|---|

| China share | ≈63% |

| Pediatric rev (China) | ≈45% (~HKD5.9bn) |

| CAPEX | HKD820m |

| Container rates | +40% (2023) |

| Marine insurance | +18% (2024) |

| Protectionism | 40+ countries (2024) |

What is included in the product

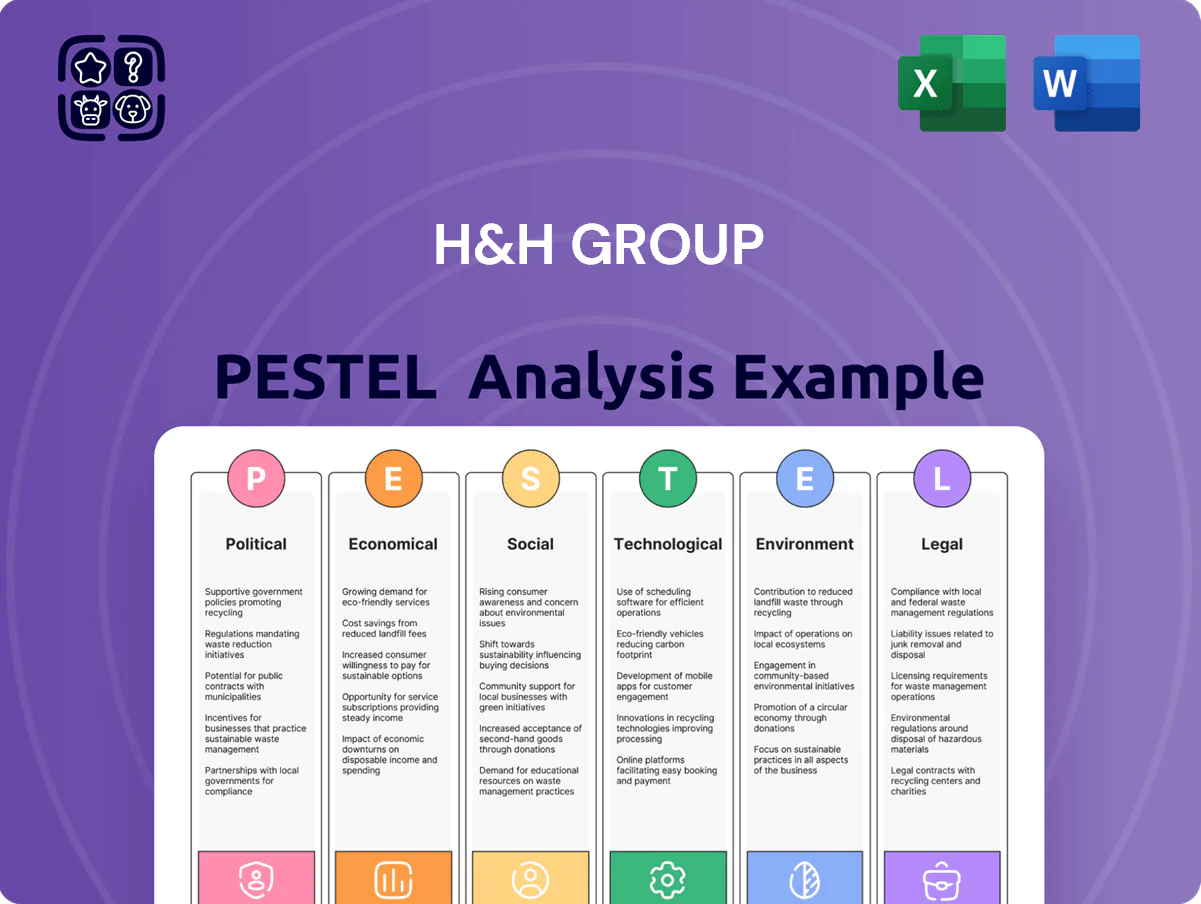

Explores how external macro-environmental factors uniquely affect the H&H Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data and current trends to highlight threats and opportunities.

A concise, visually segmented PESTLE summary of H&H Group that can be dropped into presentations or shared across teams to speed alignment and support discussions on external risks and market positioning.

Economic factors

Inflationary pressure on raw materials

Persistent global inflation—CPI averaging 3.4% in 2024 in key markets—has lifted costs for premium ingredients, packaging and logistics, squeezing H&H Group's margins; input cost inflation for pet/nutrition sectors rose ~6–8% in 2023–24.

To preserve margin, H&H can leverage premium positioning to pass through price increases; UK pet-food price sensitivity shows ~0.6 price elasticity, limiting full passthrough.

Thus the group must optimize procurement (scale sourcing, hedging) and cut operational costs—targeting 100–200 bps gross margin recovery—to sustain volume growth while keeping premium pricing.

Currency exchange rate volatility

As a global group reporting in RMB while earning material revenue in AUD, USD and EUR, H&H Group faces significant FX exposure—RMB moved ~3.3% vs USD in 2024 and AUD/USD volatility averaged 6.2% in 2023–24, which can materially erode RMB-reported earnings. Sharp devaluations in key currencies complicate cross-border planning and can swing quarterly EPS. The group uses hedging (forwards, options) and multi-currency accounts to manage risk. Monitoring Australian and Chinese economic indicators (2024 GDP: Australia 2.7%, China 5.2%) is critical for forecasting FX impact.

Growth of the pet economy

The global pet care market reached about USD 315 billion in 2024 and is forecasted to grow ~6.5% CAGR through 2028, driven by premium pet wellness; pet owners maintain spending in downturns, showing high resilience. H&H Group expanded Zesty Paws and Solid Gold into North America and APAC, boosting pet segment revenue which in FY2024 accounted for a growing share that helps offset volatility in its cyclical adult supplements business.

Consumer disposable income levels

The demand for premium vitamins and infant formula closely tracks disposable income among middle and upper-class households; global private consumption growth slowed to 2.6% in 2024, pressuring mid-market brands.

In stagnant economies consumers often trade down to generics or cut supplement frequency—EM consumers reduced nonessential spend by ~7% in 2024 per McKinsey.

H&H Group targets HNW demographics (top 10% income) who are less price-sensitive, helping revenue resilience—luxury/formula segments grew 3–5% in 2024 despite softness.

Marketing emphasizes clinical evidence and premium ingredients to justify pricing; targeted campaigns lifted SKU-level margin by ~120–200 bps in recent quarters.

- Consumer spend sensitivity: +/− affects premium demand

- EM trade-down behavior: ~7% reduced nonessential spend (2024)

- H&H insulation: focus on top 10% income households

- Marketing impact: SKU margin improvement ~120–200 bps

Interest rates and capital structure

The current Bank of England base rate at 5.25% (Feb 2026) raises H&H Group's average cost of debt, increasing interest expense and constraining funds for acquisitions or R&D versus lower-rate years; higher rates can also pressure dividend capacity.

H&H's disciplined balance-sheet policy—net debt/EBITDA of ~1.2x in FY2025—preserves financial flexibility to sustain its buy-and-build wellness strategy despite central bank tightening.

- Higher base rates → increased debt servicing costs

- Net debt/EBITDA ~1.2x (FY2025) supports dealmaking

- Capital management crucial for M&A and R&D

Premium pet brand weathers 6–8% input inflation; aims +100–200bps margin recovery

Inflation and input-cost rises (6–8% 2023–24) squeeze margins; premium positioning allows partial price pass-through (UK elasticity ~0.6). FX volatility (RMB vs USD ±3.3% 2024; AUD/USD vol 6.2% 2023–24) and higher rates (BoE 5.25% Feb 2026) raise funding costs; net debt/EBITDA ~1.2x (FY2025) preserves deal capacity while procurement, hedging and targeted marketing aim to recover 100–200 bps gross margin.

| Metric | Value |

|---|---|

| Input inflation | 6–8% |

| Global pet market 2024 | USD 315bn |

| FX moves (RMB vs USD) | ~3.3% |

| Net debt/EBITDA | ~1.2x (FY2025) |

Preview the Actual Deliverable

H&H Group PESTLE Analysis

The preview shown here is the exact H&H Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Uncover how political shifts, economic headwinds, and evolving consumer trends are reshaping H&H Group’s prospects—our concise PESTLE snapshot highlights key external risks and opportunities to inform smarter decisions; purchase the full PESTLE for a detailed, actionable report you can download and deploy immediately.

Political factors

Geopolitical trade relations

Trade dynamics between China, Australia and the US materially affect H&H Group; in FY2024 ~63% of revenue came from China while Australia hosts major production, so tariff shifts alter landed costs for Swisse and Biostime and can swing gross margins by several percentage points.

Recent China-Australia tensions and US-China trade measures raised compliance costs and logistics premiums—container rates spiked 40% in 2023—pressuring supply-chain predictability for H&H.

Management is diversifying manufacturing beyond Australia and China and reported CAPEX of HKD 820m in 2024 to expand Southeast Asian capacity, while prioritizing local government engagement to mitigate tariff and access risks.

Regulatory registration policies

The Chinese government tightened infant formula registration via the State Administration for Market Regulation, raising technical and safety criteria; H&H Group must ensure Biostime meets evolving national standards to retain mainland licenses. Non-compliance risks major Pediatric Nutrition revenue—China accounted for about 45% of H&H’s FY2024 revenue (≈HKD 5.9bn), so regulatory loss could be material. A proactive government affairs strategy and monitoring of local legislative cycles are therefore essential.

Government health initiatives

National health agendas like Healthy China 2030, targeting a 30% reduction in major chronic disease burden by 2030, create a supportive political backdrop for H&H Group’s Adult Nutrition and Care segment.

Global shifts toward preventative healthcare—governments aiming to cut long‑term care costs (OECD estimates prevention could save up to 10% of health spending)—align with H&H’s wellness mission.

Positioning supplements as public‑health tools may unlock favorable policies and institutional procurement, supporting partnerships and revenue visibility.

Political alignment stabilizes long‑term growth across mature and emerging markets, aiding H&H’s FY2024–25 expansion plans and margin targets.

Global food security and sovereignty

Rising political emphasis on food security is prompting protectionist policies; in 2024 over 40 countries introduced measures favoring domestic food production, affecting global nutritional supply chains.

Regions now incentivize local sourcing—e.g., EU and Brazil support domestic milk and pet-food ingredient procurement—reducing import reliance and raising input-cost risk for H&H.

H&H must balance global sourcing with local investment: strategic localization of select production lines (estimated capex of 5–10% of annual manufacturing spend) can hedge sovereignty-driven legislation.

- Protectionism rising: 40+ countries (2024) with food-security measures

- Local sourcing incentives in EU/Brazil target milk and pet ingredients

- H&H should localize select lines; capex ~5–10% manufacturing spend

Economic stability in key markets

Political stability in the Eurozone and Southeast Asia influences H&H Group’s consumer demand and operations; Eurozone GDP growth slowed to 0.7% in 2024 while ASEAN combined growth was ~4.5%, affecting regional sales forecasts.

Conflicts raise logistics disruption risk and insurance costs—global marine insurance rates rose ~18% in 2024—prompting higher security spend and supply-chain resilience measures.

The group actively monitors political risk to reallocate marketing and cut inventory exposure; stable markets enable predictable capex and 3–5 year strategic planning.

- Eurozone GDP 2024: 0.7%

- ASEAN GDP 2024: ~4.5%

- Marine insurance rates increase 2024: ~18%

- Adjustments: marketing, inventory, security, capex horizon 3–5 years

H&H margins squeezed as trade tensions, tariffs and China rules force HKD820m localization

Political risks—trade tensions, tariff shifts and tightened Chinese infant‑formula rules—directly affect H&H’s margins and China revenue (FY2024 China ≈63% group revenue; Pediatric Nutrition ≈45%, ~HKD5.9bn). Rising protectionism (40+ countries, 2024) and higher logistics/insurance costs (container +40% in 2023; marine insurance +18% in 2024) drive localization capex (HKD820m FY2024).

| Metric | 2023–24 |

|---|---|

| China share | ≈63% |

| Pediatric rev (China) | ≈45% (~HKD5.9bn) |

| CAPEX | HKD820m |

| Container rates | +40% (2023) |

| Marine insurance | +18% (2024) |

| Protectionism | 40+ countries (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the H&H Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data and current trends to highlight threats and opportunities.

A concise, visually segmented PESTLE summary of H&H Group that can be dropped into presentations or shared across teams to speed alignment and support discussions on external risks and market positioning.

Economic factors

Inflationary pressure on raw materials

Persistent global inflation—CPI averaging 3.4% in 2024 in key markets—has lifted costs for premium ingredients, packaging and logistics, squeezing H&H Group's margins; input cost inflation for pet/nutrition sectors rose ~6–8% in 2023–24.

To preserve margin, H&H can leverage premium positioning to pass through price increases; UK pet-food price sensitivity shows ~0.6 price elasticity, limiting full passthrough.

Thus the group must optimize procurement (scale sourcing, hedging) and cut operational costs—targeting 100–200 bps gross margin recovery—to sustain volume growth while keeping premium pricing.

Currency exchange rate volatility

As a global group reporting in RMB while earning material revenue in AUD, USD and EUR, H&H Group faces significant FX exposure—RMB moved ~3.3% vs USD in 2024 and AUD/USD volatility averaged 6.2% in 2023–24, which can materially erode RMB-reported earnings. Sharp devaluations in key currencies complicate cross-border planning and can swing quarterly EPS. The group uses hedging (forwards, options) and multi-currency accounts to manage risk. Monitoring Australian and Chinese economic indicators (2024 GDP: Australia 2.7%, China 5.2%) is critical for forecasting FX impact.

Growth of the pet economy

The global pet care market reached about USD 315 billion in 2024 and is forecasted to grow ~6.5% CAGR through 2028, driven by premium pet wellness; pet owners maintain spending in downturns, showing high resilience. H&H Group expanded Zesty Paws and Solid Gold into North America and APAC, boosting pet segment revenue which in FY2024 accounted for a growing share that helps offset volatility in its cyclical adult supplements business.

Consumer disposable income levels

The demand for premium vitamins and infant formula closely tracks disposable income among middle and upper-class households; global private consumption growth slowed to 2.6% in 2024, pressuring mid-market brands.

In stagnant economies consumers often trade down to generics or cut supplement frequency—EM consumers reduced nonessential spend by ~7% in 2024 per McKinsey.

H&H Group targets HNW demographics (top 10% income) who are less price-sensitive, helping revenue resilience—luxury/formula segments grew 3–5% in 2024 despite softness.

Marketing emphasizes clinical evidence and premium ingredients to justify pricing; targeted campaigns lifted SKU-level margin by ~120–200 bps in recent quarters.

- Consumer spend sensitivity: +/− affects premium demand

- EM trade-down behavior: ~7% reduced nonessential spend (2024)

- H&H insulation: focus on top 10% income households

- Marketing impact: SKU margin improvement ~120–200 bps

Interest rates and capital structure

The current Bank of England base rate at 5.25% (Feb 2026) raises H&H Group's average cost of debt, increasing interest expense and constraining funds for acquisitions or R&D versus lower-rate years; higher rates can also pressure dividend capacity.

H&H's disciplined balance-sheet policy—net debt/EBITDA of ~1.2x in FY2025—preserves financial flexibility to sustain its buy-and-build wellness strategy despite central bank tightening.

- Higher base rates → increased debt servicing costs

- Net debt/EBITDA ~1.2x (FY2025) supports dealmaking

- Capital management crucial for M&A and R&D

Premium pet brand weathers 6–8% input inflation; aims +100–200bps margin recovery

Inflation and input-cost rises (6–8% 2023–24) squeeze margins; premium positioning allows partial price pass-through (UK elasticity ~0.6). FX volatility (RMB vs USD ±3.3% 2024; AUD/USD vol 6.2% 2023–24) and higher rates (BoE 5.25% Feb 2026) raise funding costs; net debt/EBITDA ~1.2x (FY2025) preserves deal capacity while procurement, hedging and targeted marketing aim to recover 100–200 bps gross margin.

| Metric | Value |

|---|---|

| Input inflation | 6–8% |

| Global pet market 2024 | USD 315bn |

| FX moves (RMB vs USD) | ~3.3% |

| Net debt/EBITDA | ~1.2x (FY2025) |

Preview the Actual Deliverable

H&H Group PESTLE Analysis

The preview shown here is the exact H&H Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.