Hillenbrand Boston Consulting Group Matrix

Download Your Competitive Advantage

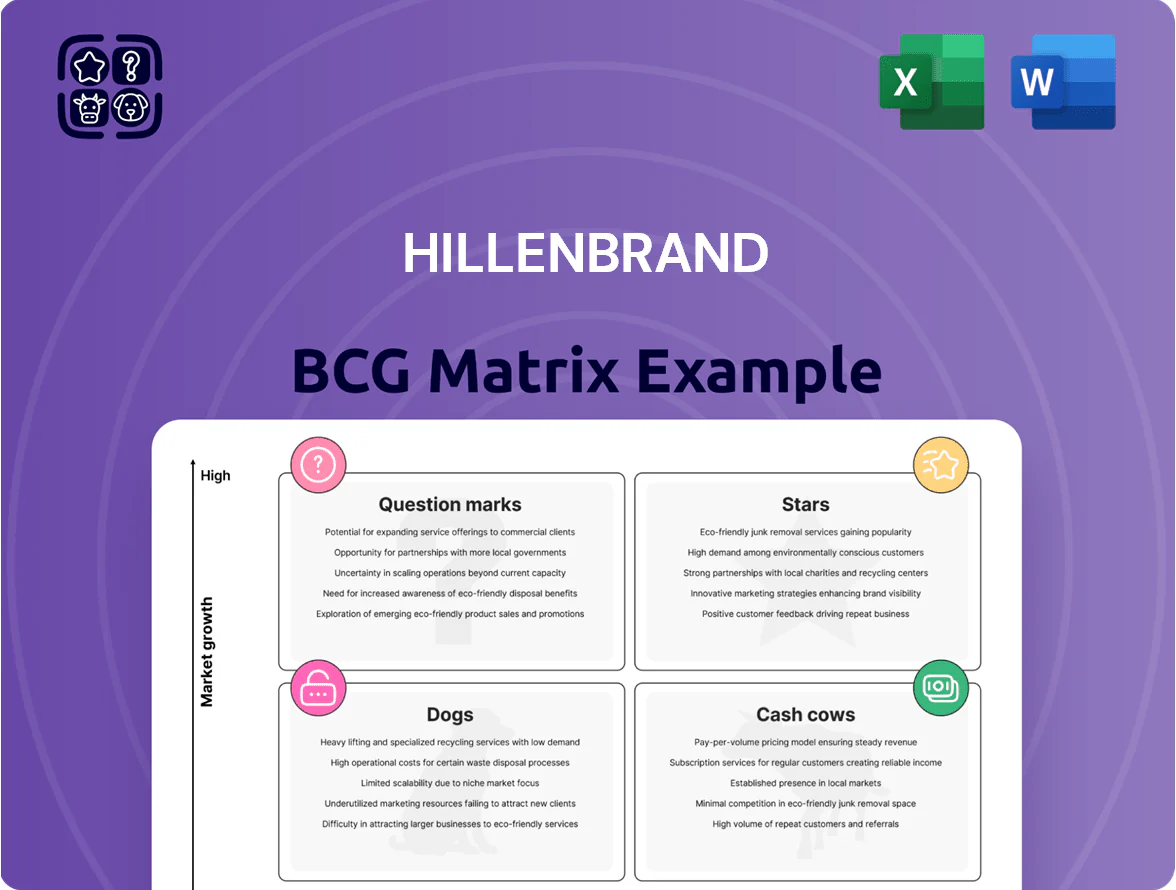

The Hillenbrand BCG Matrix snapshot highlights where its product lines likely sit—identifying potential Stars in high-growth segments, Cash Cows funding operations, Dogs that may be phased out, and Question Marks needing investment decisions. This concise preview points to strategic reallocation opportunities and risk areas as market dynamics shift. Get the full BCG Matrix report to see quadrant-by-quadrant placements, data-driven recommendations, and actionable steps for capital allocation and portfolio optimization—purchase now for Word and Excel deliverables.

Stars

Food and Nutrition Processing Systems

Hillenbrand boosted its Food and Nutrition Processing Systems via the 2023 purchase of Schenck Process Food and Performance Materials, positioning it as a BCG high-growth leader; the deal added roughly $350–400M in addressable revenue capacity.

The processed and convenience food market is growing >5% CAGR to 2025, driven by urbanization and stricter hygiene rules, supporting sustained demand.

The unit holds high market share in extrusion and milling tech for plant-based proteins and pet food, driving strong margins but needing ongoing R&D—Hillenbrand’s segment R&D spend rose to about 3–4% of segment sales in 2024 to defend against global rivals.

Circular Economy and Recycling Technologies

This product line centers on high-capacity recycling systems, notably the Herbold Meckesheim brand, targeting surging demand for post-consumer resin processing.

As of late 2025, the global recycled plastics market is growing ~8% annually; Hillenbrand leads in engineered systems for chemical and mechanical recycling of PET and other polymers.

Sustained capex is required to match fast evolution in sustainable packaging and material science; 2024–25 order intake for recycling equipment rose ~15% year-over-year, showing momentum.

Advanced Process Solutions Aftermarket Services

The Advanced Process Solutions aftermarket is a star for Hillenbrand (Coperion/Schenck) driven by a global installed base worth an estimated $3.2bn in serviceable equipment; aftermarket now delivers ~40% gross margins and grew ~12% CAGR 2019–2024 as customers modernize for energy efficiency and automation.

Industry 4.0 and predictive maintenance have pushed parts & service into high-share growth: parts recurring revenue rose to ~48% of APS service sales in 2024, with digital service platform subscriptions hitting $24m ARR and global service centers expanding to 65 locations to capture further share.

Sustainable Packaging Equipment

Hillenbrand’s Sustainable Packaging Equipment supplies extrusion and compounding systems for biodegradable and recyclable polymers, critical to packaging makers shifting from fossil-based plastics.

Industry outlook: sustainable packaging is forecast above 300 billion dollars by 2026 (market research consensus), placing this unit in a high-growth sector with a strong competitive moat.

Hillenbrand’s tech handles complex biopolymers, giving first-mover edge in emerging markets and supporting pricing power and share gains.

It remains a star: consuming cash to scale quickly while keeping a dominant tech position during industry transformation.

- Market >$300B by 2026

- Mission-critical extrusion/compounding tech

- First-mover on complex biopolymers

- High growth, cash-hungry scaling

Health and Pharmaceutical Processing Equipment

Hillenbrand’s Linxis Group and Coperion brands hold a strong position in pharmaceutical and health-grade processing equipment, supplying regulated machinery for drug manufacturing and medical plastics; pharma equipment demand grew ~6–8% CAGR 2019–2024 versus ~2–3% for general industrials (IMS Health, OECD-based estimates).

The niche needs high-spec machines, strict regulatory compliance, and dedicated sales/support teams, raising gross margins but increasing service costs and working capital needs.

Given aging populations and rising healthcare spend—global health expenditure reached ~12% of GDP in 2023—this segment offers durable growth and leadership potential for Hillenbrand over the next decade.

- High growth: ~6–8% CAGR (2019–2024)

- Higher margins; higher service cost

- Requires regulatory expertise, dedicated sales

- Strong long-term leadership opportunity

Hillenbrand Stars: High-Margin Aftermarket, $3.2B Base, Recycling Orders +15% YoY

Hillenbrand’s Stars (Coperion/Schenck/Linxis/Herbold) are high-share units in fast-growing segments (processed foods, recycled plastics, sustainable packaging, pharma equipment), showing 6–8%–8%+ CAGR, ~40% gross margins in aftermarket, ~$3.2bn serviceable installed base, $350–400M added addressable revenue (Schenck 2023), and 2024–25 recycling order intake +15% YoY.

| Metric | Value (latest) |

|---|---|

| CAGR (segments) | 6–8% / ~8% |

| Aftermarket gross margin | ~40% |

| Serviceable installed base | $3.2bn |

| Schenck addl. revenue capacity | $350–400M |

| Recycling order intake | +15% YoY (2024–25) |

What is included in the product

BCG Matrix analysis of Hillenbrand’s units: strategic guidance for Stars, Cash Cows, Question Marks, and Dogs—invest, hold, or divest based on trends.

One-page Hillenbrand BCG Matrix placing each unit in a clear quadrant for quick strategic decisions

Cash Cows

Coperion Compounding and Extrusion Systems

Coperion Compounding and Extrusion Systems is the global leader in compounding for plastics and chemicals, holding an estimated 30–40% market share in a mature sector that grew low single digits (≈2–4% CAGR) through 2025.

By 2025 Coperion produced roughly 70–80% of Hillenbrand’s free cash flow, with EBITDA margins near 20% and capex-to-sales below 3%, so it funds M&A into growth pockets.

Its low maintenance capex and steady margins make Coperion the cash cow of Advanced Process Solutions, underpinning stability during Hillenbrand’s private-equity transition.

Rotex Industrial Separation Equipment

Rotex Industrial Separation Equipment is a dominant brand in screening for minerals, fertilizers and chemicals, holding estimated market shares of 30–40% in North America and ~25% in Europe (2024 industry estimates) due to decades-long durability reputation and aftermarket service contracts.

Market growth for basic industrial separation is muted at ~2% CAGR (2021–24); yet Rotex delivers steady EBITDA margins near 25% and predictable aftermarket revenue, letting Hillenbrand use cash flows to pay down corporate net debt (Hillenbrand net leverage 1.9x at 2024 year-end) and fund investments in higher-growth units.

Milacron Hot Runner Systems (Mold-Masters)

After divesting cyclical injection molding machinery in 2023, Hillenbrand kept high-margin Mold-Masters (Milacron Hot Runner Systems) inside MTS; the unit reported ~USD 220m revenue in 2024 and ~28% adjusted EBITDA margin, reflecting strong cash generation.

Mold-Masters leads global melt-delivery and control systems in a mature market; high share, low capex vs heavy presses, and recurring service sales make it a classic cash cow.

Stable demand from medical and automotive—combined end-market exposure ~60% of sales in 2024—provides predictable cash flow that funds Hillenbrand’s growth and dividends.

Bulk Material Handling Systems

Hillenbrand’s Bulk Material Handling Systems serve mature sectors—mining, cement, heavy manufacturing—providing conveyors, feeders and weighing systems; these end markets grew ~1–2% annually 2020–2024, so revenue growth is low but predictable.

Established market share and recurring replacement orders plus system upgrades yield high gross margins (mid-30s% reported by Hillenbrand in FY2024) and low promo spend, producing steady free cash flow that funds the company’s pivot to food and recycling.

Here’s the quick math: FY2024 segment operating margin ~32%, recurring aftermarket ≈45% of segment revenue, and cash conversion supports Hillenbrand’s 2025 capex shift toward growth areas.

- Serves low-growth, capital-intensive industries

- High margins (mid-30s%) and low marketing cost

- Aftermarket ≈45% of segment sales—stable revenue

- Funds strategic shift to food and recycling via steady cash

Legacy Industrial Compounding Solutions

Hillenbrand’s Legacy Industrial Compounding Solutions serve a mature, low-growth global polyolefin and engineering plastics market (≈1–2% CAGR). With leading share and plants in Germany and the U.S., these lines deliver high margins—Hillenbrand reported segment EBITDA margin ~22% in 2024—generating steady cash to fund integration of recent food-processing and sustainable-tech purchases.

- Market growth 1–2% CAGR

- Segment EBITDA margin ≈22% (2024)

- Manufacturing footprint: Germany, U.S.

- Low marketing spend; industry-standard systems

- Cash funds M&A integration (food, sustainability)

Hillenbrand cash cows drive 70–80% FCF, 20–32% EBITDA; fueling debt paydown & M&A

Coperion, Rotex, Mold-Masters and Bulk Handling are Hillenbrand cash cows—high share in mature markets, FY2024 EBITDA margins 20–28%, aftermarket ~45%, capex-to-sales <3%, and together supplied ~70–80% of free cash flow used for debt reduction (net leverage 1.9x YE2024) and M&A.

| Unit | 2024 Rev (USD) | EBITDA% | Aftermarket% |

|---|---|---|---|

| Coperion | ~1.1bn | ~20% | — |

| Mold-Masters | 220m | 28% | — |

| Rotex | ~250m | 25% | — |

| Bulk | ~300m | 32% | 45% |

What You See Is What You Get

Hillenbrand BCG Matrix

The file you're previewing on this page is the exact Hillenbrand BCG Matrix report you'll receive after purchase—no watermarks, no demo elements, just the fully formatted, ready-to-use strategic analysis tailored for portfolio clarity and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

The Hillenbrand BCG Matrix snapshot highlights where its product lines likely sit—identifying potential Stars in high-growth segments, Cash Cows funding operations, Dogs that may be phased out, and Question Marks needing investment decisions. This concise preview points to strategic reallocation opportunities and risk areas as market dynamics shift. Get the full BCG Matrix report to see quadrant-by-quadrant placements, data-driven recommendations, and actionable steps for capital allocation and portfolio optimization—purchase now for Word and Excel deliverables.

Stars

Food and Nutrition Processing Systems

Hillenbrand boosted its Food and Nutrition Processing Systems via the 2023 purchase of Schenck Process Food and Performance Materials, positioning it as a BCG high-growth leader; the deal added roughly $350–400M in addressable revenue capacity.

The processed and convenience food market is growing >5% CAGR to 2025, driven by urbanization and stricter hygiene rules, supporting sustained demand.

The unit holds high market share in extrusion and milling tech for plant-based proteins and pet food, driving strong margins but needing ongoing R&D—Hillenbrand’s segment R&D spend rose to about 3–4% of segment sales in 2024 to defend against global rivals.

Circular Economy and Recycling Technologies

This product line centers on high-capacity recycling systems, notably the Herbold Meckesheim brand, targeting surging demand for post-consumer resin processing.

As of late 2025, the global recycled plastics market is growing ~8% annually; Hillenbrand leads in engineered systems for chemical and mechanical recycling of PET and other polymers.

Sustained capex is required to match fast evolution in sustainable packaging and material science; 2024–25 order intake for recycling equipment rose ~15% year-over-year, showing momentum.

Advanced Process Solutions Aftermarket Services

The Advanced Process Solutions aftermarket is a star for Hillenbrand (Coperion/Schenck) driven by a global installed base worth an estimated $3.2bn in serviceable equipment; aftermarket now delivers ~40% gross margins and grew ~12% CAGR 2019–2024 as customers modernize for energy efficiency and automation.

Industry 4.0 and predictive maintenance have pushed parts & service into high-share growth: parts recurring revenue rose to ~48% of APS service sales in 2024, with digital service platform subscriptions hitting $24m ARR and global service centers expanding to 65 locations to capture further share.

Sustainable Packaging Equipment

Hillenbrand’s Sustainable Packaging Equipment supplies extrusion and compounding systems for biodegradable and recyclable polymers, critical to packaging makers shifting from fossil-based plastics.

Industry outlook: sustainable packaging is forecast above 300 billion dollars by 2026 (market research consensus), placing this unit in a high-growth sector with a strong competitive moat.

Hillenbrand’s tech handles complex biopolymers, giving first-mover edge in emerging markets and supporting pricing power and share gains.

It remains a star: consuming cash to scale quickly while keeping a dominant tech position during industry transformation.

- Market >$300B by 2026

- Mission-critical extrusion/compounding tech

- First-mover on complex biopolymers

- High growth, cash-hungry scaling

Health and Pharmaceutical Processing Equipment

Hillenbrand’s Linxis Group and Coperion brands hold a strong position in pharmaceutical and health-grade processing equipment, supplying regulated machinery for drug manufacturing and medical plastics; pharma equipment demand grew ~6–8% CAGR 2019–2024 versus ~2–3% for general industrials (IMS Health, OECD-based estimates).

The niche needs high-spec machines, strict regulatory compliance, and dedicated sales/support teams, raising gross margins but increasing service costs and working capital needs.

Given aging populations and rising healthcare spend—global health expenditure reached ~12% of GDP in 2023—this segment offers durable growth and leadership potential for Hillenbrand over the next decade.

- High growth: ~6–8% CAGR (2019–2024)

- Higher margins; higher service cost

- Requires regulatory expertise, dedicated sales

- Strong long-term leadership opportunity

Hillenbrand Stars: High-Margin Aftermarket, $3.2B Base, Recycling Orders +15% YoY

Hillenbrand’s Stars (Coperion/Schenck/Linxis/Herbold) are high-share units in fast-growing segments (processed foods, recycled plastics, sustainable packaging, pharma equipment), showing 6–8%–8%+ CAGR, ~40% gross margins in aftermarket, ~$3.2bn serviceable installed base, $350–400M added addressable revenue (Schenck 2023), and 2024–25 recycling order intake +15% YoY.

| Metric | Value (latest) |

|---|---|

| CAGR (segments) | 6–8% / ~8% |

| Aftermarket gross margin | ~40% |

| Serviceable installed base | $3.2bn |

| Schenck addl. revenue capacity | $350–400M |

| Recycling order intake | +15% YoY (2024–25) |

What is included in the product

BCG Matrix analysis of Hillenbrand’s units: strategic guidance for Stars, Cash Cows, Question Marks, and Dogs—invest, hold, or divest based on trends.

One-page Hillenbrand BCG Matrix placing each unit in a clear quadrant for quick strategic decisions

Cash Cows

Coperion Compounding and Extrusion Systems

Coperion Compounding and Extrusion Systems is the global leader in compounding for plastics and chemicals, holding an estimated 30–40% market share in a mature sector that grew low single digits (≈2–4% CAGR) through 2025.

By 2025 Coperion produced roughly 70–80% of Hillenbrand’s free cash flow, with EBITDA margins near 20% and capex-to-sales below 3%, so it funds M&A into growth pockets.

Its low maintenance capex and steady margins make Coperion the cash cow of Advanced Process Solutions, underpinning stability during Hillenbrand’s private-equity transition.

Rotex Industrial Separation Equipment

Rotex Industrial Separation Equipment is a dominant brand in screening for minerals, fertilizers and chemicals, holding estimated market shares of 30–40% in North America and ~25% in Europe (2024 industry estimates) due to decades-long durability reputation and aftermarket service contracts.

Market growth for basic industrial separation is muted at ~2% CAGR (2021–24); yet Rotex delivers steady EBITDA margins near 25% and predictable aftermarket revenue, letting Hillenbrand use cash flows to pay down corporate net debt (Hillenbrand net leverage 1.9x at 2024 year-end) and fund investments in higher-growth units.

Milacron Hot Runner Systems (Mold-Masters)

After divesting cyclical injection molding machinery in 2023, Hillenbrand kept high-margin Mold-Masters (Milacron Hot Runner Systems) inside MTS; the unit reported ~USD 220m revenue in 2024 and ~28% adjusted EBITDA margin, reflecting strong cash generation.

Mold-Masters leads global melt-delivery and control systems in a mature market; high share, low capex vs heavy presses, and recurring service sales make it a classic cash cow.

Stable demand from medical and automotive—combined end-market exposure ~60% of sales in 2024—provides predictable cash flow that funds Hillenbrand’s growth and dividends.

Bulk Material Handling Systems

Hillenbrand’s Bulk Material Handling Systems serve mature sectors—mining, cement, heavy manufacturing—providing conveyors, feeders and weighing systems; these end markets grew ~1–2% annually 2020–2024, so revenue growth is low but predictable.

Established market share and recurring replacement orders plus system upgrades yield high gross margins (mid-30s% reported by Hillenbrand in FY2024) and low promo spend, producing steady free cash flow that funds the company’s pivot to food and recycling.

Here’s the quick math: FY2024 segment operating margin ~32%, recurring aftermarket ≈45% of segment revenue, and cash conversion supports Hillenbrand’s 2025 capex shift toward growth areas.

- Serves low-growth, capital-intensive industries

- High margins (mid-30s%) and low marketing cost

- Aftermarket ≈45% of segment sales—stable revenue

- Funds strategic shift to food and recycling via steady cash

Legacy Industrial Compounding Solutions

Hillenbrand’s Legacy Industrial Compounding Solutions serve a mature, low-growth global polyolefin and engineering plastics market (≈1–2% CAGR). With leading share and plants in Germany and the U.S., these lines deliver high margins—Hillenbrand reported segment EBITDA margin ~22% in 2024—generating steady cash to fund integration of recent food-processing and sustainable-tech purchases.

- Market growth 1–2% CAGR

- Segment EBITDA margin ≈22% (2024)

- Manufacturing footprint: Germany, U.S.

- Low marketing spend; industry-standard systems

- Cash funds M&A integration (food, sustainability)

Hillenbrand cash cows drive 70–80% FCF, 20–32% EBITDA; fueling debt paydown & M&A

Coperion, Rotex, Mold-Masters and Bulk Handling are Hillenbrand cash cows—high share in mature markets, FY2024 EBITDA margins 20–28%, aftermarket ~45%, capex-to-sales <3%, and together supplied ~70–80% of free cash flow used for debt reduction (net leverage 1.9x YE2024) and M&A.

| Unit | 2024 Rev (USD) | EBITDA% | Aftermarket% |

|---|---|---|---|

| Coperion | ~1.1bn | ~20% | — |

| Mold-Masters | 220m | 28% | — |

| Rotex | ~250m | 25% | — |

| Bulk | ~300m | 32% | 45% |

What You See Is What You Get

Hillenbrand BCG Matrix

The file you're previewing on this page is the exact Hillenbrand BCG Matrix report you'll receive after purchase—no watermarks, no demo elements, just the fully formatted, ready-to-use strategic analysis tailored for portfolio clarity and decision-making.