Hillenbrand SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Hillenbrand’s diversified manufacturing footprint and aftermarket services drive steady cash flow, but exposure to cyclical end markets and integration risks warrant close monitoring; our full SWOT unpacks these dynamics with data-backed insight. Purchase the complete SWOT analysis to receive a professionally formatted Word report and editable Excel tools—ideal for investors, strategists, and advisors seeking actionable, presentation-ready intelligence.

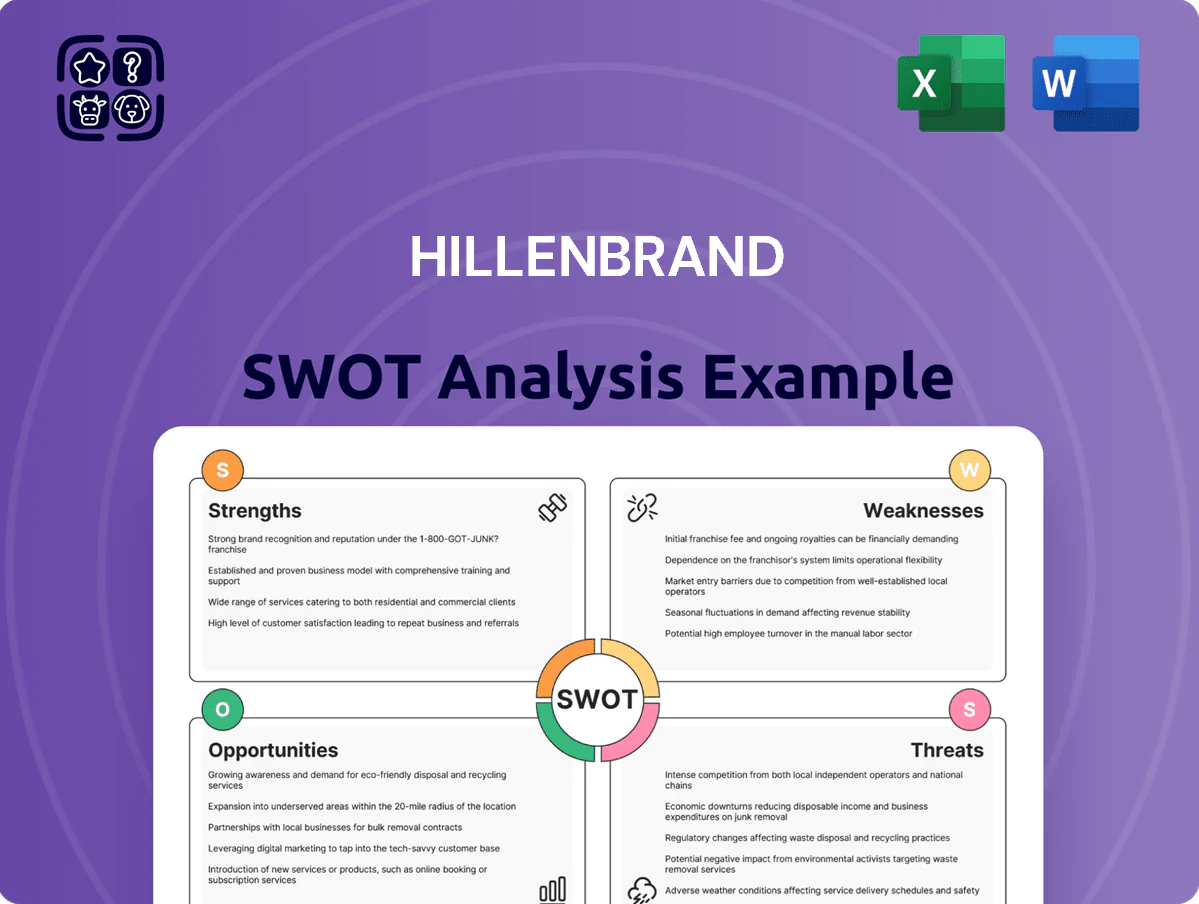

Strengths

Market Leadership in Highly Engineered Solutions

Hillenbrand holds global leadership via Coperion and Milacron, which together served >70 markets and accounted for roughly 55% of FY2024 industrial equipment revenue, anchoring its position in extrusion and injection molding technology.

These high‑engineering products are hard for low‑cost rivals to copy, enabling price premiums and gross margins ~18–20% in 2024 versus 12–14% for commodity peers.

Technical leadership builds strong customer loyalty and a recurring aftermarket and services business that generated about $420 million in FY2024 revenue, roughly 20% of segment sales.

The Hillenbrand Operating Model

The Hillenbrand Operating Model drives continuous improvement through lean manufacturing, strategic procurement, and talent development, lifting adjusted operating margin by about 180 basis points from 2019–2024 and improving free cash flow conversion to roughly 25% in FY2024; standardized tools speed integration of acquisitions (e.g., the 2021 purchase of Diversey-related assets) and trimmed integration time by an estimated 30%, boosting segment efficiency across the portfolio.

Diversified Industrial End Markets

Hillenbrand shifted from death care to industrials, now serving food, pharma, and recycling; by 2024 industrial revenue made up ~98% of sales, cutting legacy exposure.

Diversified end markets lower single-industry risk—food and pharma demand limited cyclicality, recycling benefits from steady commodity-driven tailwinds.

The split between Advanced Process Solutions and Molding Technology Solutions (2024 pro forma revenue ~$2.3B and $1.1B respectively) gives balanced cash flow for long-term growth.

Extensive Global Service Footprint

With operations in over 40 countries, Hillenbrand supports a large installed base that drives recurring revenue from parts, maintenance, and field service—services made up about 35% of 2024 revenue (Hillenbrand Inc. 2024 10-K).

This global footprint lets Hillenbrand serve multinational clients consistently, a clear edge versus regional competitors and helps stabilize cash flow when capital-equipment orders dip.

- 40+ countries global presence

- Installed base fuels recurring service revenue (~35% of 2024 sales)

- Supports multinational customers in-market

- Service mix cushions capital-sales cyclicality

Focus on Sustainability and Innovation

Hillenbrand has become a key enabler of the circular economy by commercializing advanced plastics recycling equipment that processed over 120 kilotonnes of post-consumer resin in 2024, meeting rising demand from global recycled-content mandates.

Its machines are critical for high-growth recycled-materials processing, a market growing ~8–10% CAGR to 2030, and Hillenbrand’s continued R&D spend—about $45 million in 2024—keeps it ahead on energy-efficient, waste-reducing solutions.

These strengths support higher-margin aftermarket sales and customer stickiness as regulators push 2025–2030 recycled-content targets across EU and US supply chains.

- Processed ~120 kt post-consumer resin (2024)

- R&D spend ~$45M (2024)

- Recycled-materials market +8–10% CAGR to 2030

- Supports EU/US recycled-content mandates 2025–2030

Market‑leading extrusion/injection firm: $3.4B pro‑forma, high margins & $420M aftermarket

Market leader in extrusion/injection (Coperion, Milacron) — FY2024 industrial revenue split ~68/32; higher gross margin ~18–20% vs peers 12–14%; recurring service/backlog ~35% of sales (~$420M aftermarket); global footprint 40+ countries; FY2024 R&D ~$45M; processed ~120 kt post‑consumer resin (2024); pro forma 2024 revenue APS ~$2.3B, MTS ~$1.1B.

What is included in the product

Delivers a strategic overview of Hillenbrand’s internal strengths and weaknesses alongside external opportunities and threats, mapping key growth drivers, operational gaps, and market risks that shape the company’s competitive position.

Delivers a concise Hillenbrand SWOT matrix for rapid strategic alignment, ideal for executives needing a clear snapshot of strengths, weaknesses, opportunities, and threats.

Weaknesses

Significant Debt from Strategic Acquisitions

The aggressive acquisition push left Hillenbrand Inc. with long-term debt of about $1.9 billion as of 2025 Q4, pushing net leverage to roughly 3.2x EBITDA; that scale boosts capabilities but raises interest-service costs that constrain capex and R&D.

Management must prioritize rapid deleveraging—paydown or cash-flow improvements—to restore flexibility while rates average above 5% in 2025; otherwise refinancing risk and reduced investment optionality rise.

Cyclical Sensitivity of Capital Equipment

Complexity in Integrating Large Scale Acquisitions

The rapid acquisitions such as the 2023 Schenck Process Food and Performance Materials deal add integration risk: combining cultures, ERP platforms, and supply chains can cause operational downtime and drove Hillenbrand’s 2024 restructuring charge of $72 million.

If synergies lag, Hillenbrand may miss its $60–80 million annual run-rate target for 2025, hurting EBITDA margins and investor confidence; integration overruns historically raise costs by ~10–25% in comparable M&A cases.

Exposure to Volatile Raw Material Costs

Hillenbrand, as a heavy-equipment maker, is exposed to volatile steel and aluminum markets; LTM 2025 US hot-rolled coil price swings of ±20% amplify input-cost risk.

The firm uses surcharges and repricing, but typical contract lag of 30–90 days means sudden raw-material or energy spikes—like mid-2024 +35% steel jump—can squeeze margins on fixed-price orders.

- High sensitivity to steel/aluminum price swings (±20–35% recent moves)

- Pricing lag 30–90 days delays cost recovery

- Fixed-price contracts magnify margin compression risk

Reliance on Global Trade and Supply Chains

The company’s global manufacturing and distribution model makes Hillenbrand (NYSE: HI) vulnerable to international logistics disruptions; 2024 supply-chain delays raised lead times by ~12% for industrial products, per management commentary.

Geopolitical tensions and tariff shifts can raise component costs—Hillenbrand warned a 3–5% input-cost swing could cut 2025 margins by ~80–200bps.

Complex supplier networks increase exposure to regional economic instability and require higher working capital and inventory buffers.

- 12% longer lead times in 2024

- 3–5% input-cost swing → 80–200bps margin hit

- Higher working capital, inventory buffers

Hillenbrand: Heavy Debt, Cyclical Capex Risk, Margin Pressure from Raw-Material Swings

The aggressive acquisition push left Hillenbrand (NYSE: HI) with ~$1.9B long-term debt (2025 Q4), ~3.2x net leverage, raising interest service costs and constraining capex/R&D; high capital-equipment exposure (≈62% of 2024 sales) drives cyclicality (Q3 2023 EPS -28% YoY); integration/reshaping costs (2024 restructuring $72M) risk missing $60–80M synergy target; raw-material swings ±20–35% and 30–90d pricing lag squeeze margins.

| Metric | Value |

|---|---|

| Long-term debt (2025 Q4) | $1.9B |

| Net leverage | ~3.2x EBITDA |

| Capital-equipment sales (2024) | ≈62% |

| Restructuring charge (2024) | $72M |

| Synergy target (2025) | $60–80M |

| Steel/aluminum price moves (LTM 2025) | ±20–35% |

| Pricing lag | 30–90 days |

Same Document Delivered

Hillenbrand SWOT Analysis

This is the actual Hillenbrand SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and the complete, editable version becomes available immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Hillenbrand’s diversified manufacturing footprint and aftermarket services drive steady cash flow, but exposure to cyclical end markets and integration risks warrant close monitoring; our full SWOT unpacks these dynamics with data-backed insight. Purchase the complete SWOT analysis to receive a professionally formatted Word report and editable Excel tools—ideal for investors, strategists, and advisors seeking actionable, presentation-ready intelligence.

Strengths

Market Leadership in Highly Engineered Solutions

Hillenbrand holds global leadership via Coperion and Milacron, which together served >70 markets and accounted for roughly 55% of FY2024 industrial equipment revenue, anchoring its position in extrusion and injection molding technology.

These high‑engineering products are hard for low‑cost rivals to copy, enabling price premiums and gross margins ~18–20% in 2024 versus 12–14% for commodity peers.

Technical leadership builds strong customer loyalty and a recurring aftermarket and services business that generated about $420 million in FY2024 revenue, roughly 20% of segment sales.

The Hillenbrand Operating Model

The Hillenbrand Operating Model drives continuous improvement through lean manufacturing, strategic procurement, and talent development, lifting adjusted operating margin by about 180 basis points from 2019–2024 and improving free cash flow conversion to roughly 25% in FY2024; standardized tools speed integration of acquisitions (e.g., the 2021 purchase of Diversey-related assets) and trimmed integration time by an estimated 30%, boosting segment efficiency across the portfolio.

Diversified Industrial End Markets

Hillenbrand shifted from death care to industrials, now serving food, pharma, and recycling; by 2024 industrial revenue made up ~98% of sales, cutting legacy exposure.

Diversified end markets lower single-industry risk—food and pharma demand limited cyclicality, recycling benefits from steady commodity-driven tailwinds.

The split between Advanced Process Solutions and Molding Technology Solutions (2024 pro forma revenue ~$2.3B and $1.1B respectively) gives balanced cash flow for long-term growth.

Extensive Global Service Footprint

With operations in over 40 countries, Hillenbrand supports a large installed base that drives recurring revenue from parts, maintenance, and field service—services made up about 35% of 2024 revenue (Hillenbrand Inc. 2024 10-K).

This global footprint lets Hillenbrand serve multinational clients consistently, a clear edge versus regional competitors and helps stabilize cash flow when capital-equipment orders dip.

- 40+ countries global presence

- Installed base fuels recurring service revenue (~35% of 2024 sales)

- Supports multinational customers in-market

- Service mix cushions capital-sales cyclicality

Focus on Sustainability and Innovation

Hillenbrand has become a key enabler of the circular economy by commercializing advanced plastics recycling equipment that processed over 120 kilotonnes of post-consumer resin in 2024, meeting rising demand from global recycled-content mandates.

Its machines are critical for high-growth recycled-materials processing, a market growing ~8–10% CAGR to 2030, and Hillenbrand’s continued R&D spend—about $45 million in 2024—keeps it ahead on energy-efficient, waste-reducing solutions.

These strengths support higher-margin aftermarket sales and customer stickiness as regulators push 2025–2030 recycled-content targets across EU and US supply chains.

- Processed ~120 kt post-consumer resin (2024)

- R&D spend ~$45M (2024)

- Recycled-materials market +8–10% CAGR to 2030

- Supports EU/US recycled-content mandates 2025–2030

Market‑leading extrusion/injection firm: $3.4B pro‑forma, high margins & $420M aftermarket

Market leader in extrusion/injection (Coperion, Milacron) — FY2024 industrial revenue split ~68/32; higher gross margin ~18–20% vs peers 12–14%; recurring service/backlog ~35% of sales (~$420M aftermarket); global footprint 40+ countries; FY2024 R&D ~$45M; processed ~120 kt post‑consumer resin (2024); pro forma 2024 revenue APS ~$2.3B, MTS ~$1.1B.

What is included in the product

Delivers a strategic overview of Hillenbrand’s internal strengths and weaknesses alongside external opportunities and threats, mapping key growth drivers, operational gaps, and market risks that shape the company’s competitive position.

Delivers a concise Hillenbrand SWOT matrix for rapid strategic alignment, ideal for executives needing a clear snapshot of strengths, weaknesses, opportunities, and threats.

Weaknesses

Significant Debt from Strategic Acquisitions

The aggressive acquisition push left Hillenbrand Inc. with long-term debt of about $1.9 billion as of 2025 Q4, pushing net leverage to roughly 3.2x EBITDA; that scale boosts capabilities but raises interest-service costs that constrain capex and R&D.

Management must prioritize rapid deleveraging—paydown or cash-flow improvements—to restore flexibility while rates average above 5% in 2025; otherwise refinancing risk and reduced investment optionality rise.

Cyclical Sensitivity of Capital Equipment

Complexity in Integrating Large Scale Acquisitions

The rapid acquisitions such as the 2023 Schenck Process Food and Performance Materials deal add integration risk: combining cultures, ERP platforms, and supply chains can cause operational downtime and drove Hillenbrand’s 2024 restructuring charge of $72 million.

If synergies lag, Hillenbrand may miss its $60–80 million annual run-rate target for 2025, hurting EBITDA margins and investor confidence; integration overruns historically raise costs by ~10–25% in comparable M&A cases.

Exposure to Volatile Raw Material Costs

Hillenbrand, as a heavy-equipment maker, is exposed to volatile steel and aluminum markets; LTM 2025 US hot-rolled coil price swings of ±20% amplify input-cost risk.

The firm uses surcharges and repricing, but typical contract lag of 30–90 days means sudden raw-material or energy spikes—like mid-2024 +35% steel jump—can squeeze margins on fixed-price orders.

- High sensitivity to steel/aluminum price swings (±20–35% recent moves)

- Pricing lag 30–90 days delays cost recovery

- Fixed-price contracts magnify margin compression risk

Reliance on Global Trade and Supply Chains

The company’s global manufacturing and distribution model makes Hillenbrand (NYSE: HI) vulnerable to international logistics disruptions; 2024 supply-chain delays raised lead times by ~12% for industrial products, per management commentary.

Geopolitical tensions and tariff shifts can raise component costs—Hillenbrand warned a 3–5% input-cost swing could cut 2025 margins by ~80–200bps.

Complex supplier networks increase exposure to regional economic instability and require higher working capital and inventory buffers.

- 12% longer lead times in 2024

- 3–5% input-cost swing → 80–200bps margin hit

- Higher working capital, inventory buffers

Hillenbrand: Heavy Debt, Cyclical Capex Risk, Margin Pressure from Raw-Material Swings

The aggressive acquisition push left Hillenbrand (NYSE: HI) with ~$1.9B long-term debt (2025 Q4), ~3.2x net leverage, raising interest service costs and constraining capex/R&D; high capital-equipment exposure (≈62% of 2024 sales) drives cyclicality (Q3 2023 EPS -28% YoY); integration/reshaping costs (2024 restructuring $72M) risk missing $60–80M synergy target; raw-material swings ±20–35% and 30–90d pricing lag squeeze margins.

| Metric | Value |

|---|---|

| Long-term debt (2025 Q4) | $1.9B |

| Net leverage | ~3.2x EBITDA |

| Capital-equipment sales (2024) | ≈62% |

| Restructuring charge (2024) | $72M |

| Synergy target (2025) | $60–80M |

| Steel/aluminum price moves (LTM 2025) | ±20–35% |

| Pricing lag | 30–90 days |

Same Document Delivered

Hillenbrand SWOT Analysis

This is the actual Hillenbrand SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and the complete, editable version becomes available immediately after checkout.