Hilton Grand Vacations PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

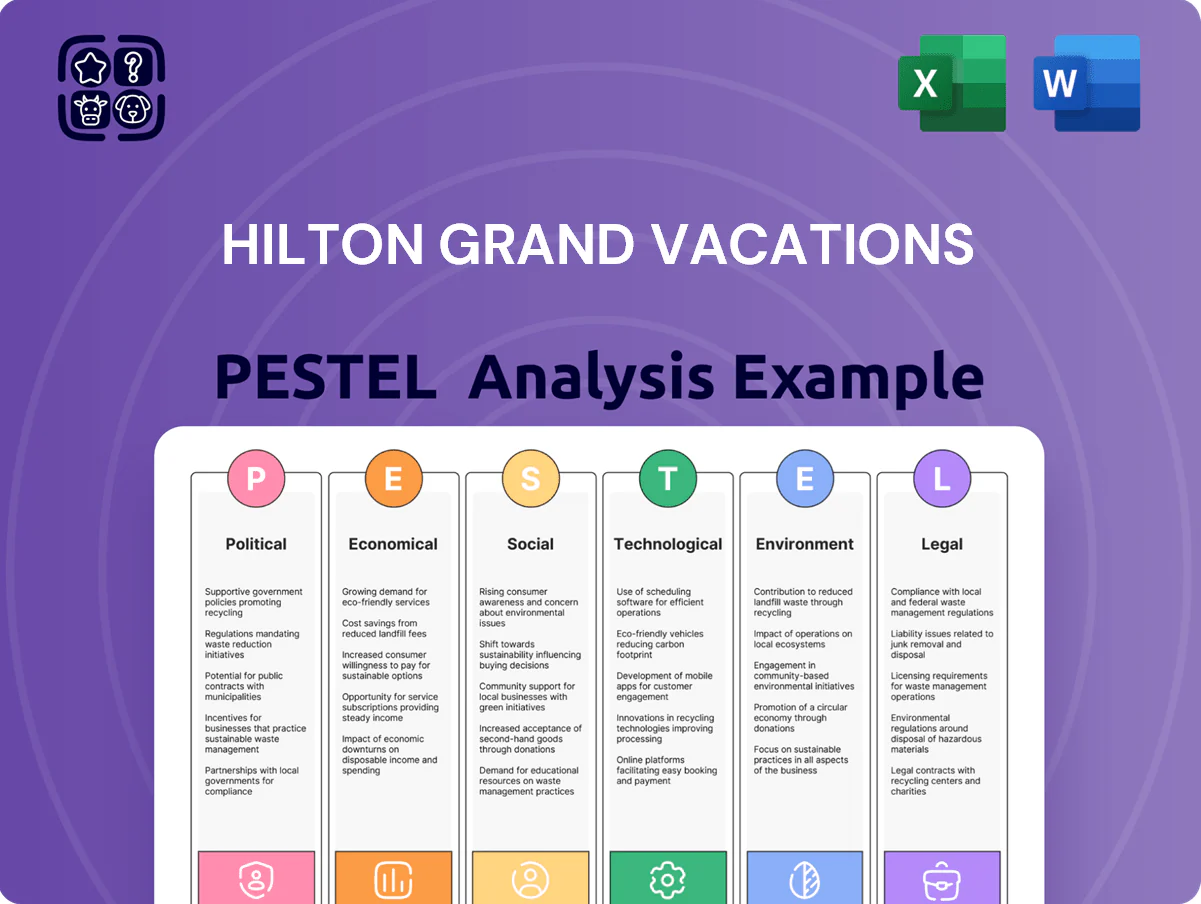

Unlock strategic clarity with our focused PESTLE Analysis of Hilton Grand Vacations—revealing how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape performance and growth opportunities; buy the full report for an actionable, fully editable breakdown to inform investments, strategy, and pitch-ready recommendations.

Political factors

Geopolitical Stability in Key Markets

Hilton Grand Vacations expansion into Japan and Europe exposes it to regional political shifts; in FY2024 international revenue represented about 18% of total revenue, making stability in these markets material to operations.

Political unrest or diplomatic changes can reduce cross-border travel for its ~460,000 members; after COVID, international arrivals to Japan fell 70% in 2020 but recovered to 50% of 2019 levels by 2023, showing sensitivity to geopolitics.

Maintaining a geographically diverse portfolio—North America, Europe, Asia—helps HGV dilute localized political volatility risk, as no single region accounts for more than ~40% of its room inventory.

Tourism Promotion and Incentive Policies

Government-led tourism initiatives boost Hilton Grand Vacations’ U.S. and Asia-Pacific resorts; U.S. Travel Association reported domestic travel spending rose to $1.3 trillion in 2023, while UNWTO noted Asia-Pacific arrivals recovered to ~75% of 2019 levels in 2024, supporting demand.

International Trade and Visa Regulations

Changes in visa rules and trade deals can alter traveler flows to Hilton Grand Vacations resorts; e.g., U.S. travel visa approvals dropped 8% in 2024 vs 2023, tightening visitor pools to destinations like Hawaii where international arrivals fell 6% Y/Y. Stricter immigration limits could reduce demand for timeshare sales from overseas buyers. Management must track trade policy shifts that raised construction import costs—steel and lumber import prices rose ~12% in 2024—impacting new development budgets.

Corporate Taxation and Fiscal Policies

Potential shifts in US federal corporate tax rates or changes in tax treatment for real estate and interest income can materially affect HGV’s net margins; a 1 percentage-point rise in effective tax rate would reduce 2025 adjusted EPS by an estimated mid-single-digit percentage given 2024 tax-effective margins (HGV reported $1.02bn EBITDA in FY2024).

As a capital-intensive business that earned roughly $200–250m annually from financing-related net interest and fees in 2023–2024, HGV is sensitive to fiscal measures that tighten consumer credit or raise corporate borrowing costs, which could compress financing revenue and raise funding expenses.

Adapting to evolving tax regimes across jurisdictions—where statutory rates range from the US federal 21% plus state levies to overseas rates exceeding 25%—is essential for efficient capital allocation, transfer pricing, and optimizing blended tax rates.

- 2024 EBITDA $1.02bn; financing income ~$200–250m

- US federal tax baseline 21%; some jurisdictions >25%

- 1ppt tax rise → mid-single-digit EPS hit (est.)

- High sensitivity to consumer credit and corporate debt costs

Political Influence on Infrastructure Development

The success of Hilton Grand Vacations resorts relies on local infrastructure—airports, roads, utilities—often controlled by political entities; in 2024, destinations with upgraded airports saw 12–18% higher RevPAR for resort-class properties.

Political support for infrastructure projects, such as Florida’s $2.3bn tourism infrastructure allocations in 2024, improves accessibility and HGV property values.

Conversely, political neglect or corruption can cause deteriorating services, lowering occupancy and guest satisfaction.

- Infrastructure upgrades correlate with 12–18% higher RevPAR

- Florida allocated $2.3bn to tourism infrastructure in 2024

- Neglect/corruption reduces occupancy and guest satisfaction

Hilton Grand Vacations: Political risks and trade shifts threaten international revenue and margins

Hilton Grand Vacations faces material political risk from international market shifts—FY2024 international revenue ~18%—making stability in Japan/Europe critical. Visa, trade, and infrastructure policies affect arrivals and costs; e.g., U.S. travel visa approvals −8% in 2024, steel/lumber import prices +12% in 2024. Fiscal/tax changes (US baseline 21%) and credit policy also directly impact margins and financing income (~$200–250m in 2023–24).

| Metric | 2023–24 |

|---|---|

| Intl revenue share | ~18% |

| EBITDA | $1.02bn (2024) |

| Financing income | $200–250m |

| Visa approvals Y/Y | −8% (2024) |

| Import prices (steel/lumber) | +12% (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely affect Hilton Grand Vacations, with data-driven trends and region-specific examples to identify risks, opportunities, and strategic actions for executives, investors, and planners.

A concise PESTLE snapshot for Hilton Grand Vacations that clearly segments political, economic, social, technological, legal, and environmental factors—ideal for quick sharing in presentations or team discussions to align on external risks and opportunity areas.

Economic factors

Interest Rate Volatility

Hilton Grand Vacations finances many vacation ownership purchases, so the Fed's rise to a 5.25–5.50% policy rate in 2024 raised its cost of funding and pressured net interest income; higher rates also cooled consumer loan demand, contributing to a 2024 YTD slowdown in sales growth versus 2023. A 100 bp move can materially widen spread compression on its loan book, making monitoring Fed guidance essential for forecasting sales volume and managing loan-margin risk.

Consumer Discretionary Income Trends

As a luxury leisure product, Hilton Grand Vacations relies on upper-middle-income disposable income; US real disposable personal income rose 1.1% year-over-year in 2024, supporting demand among its core demographic.

Economic downturns or falling consumer confidence—consumer confidence fell to 88.7 in Dec 2024—can defer purchases and increase defaults on vacation-ownership loans, which HGV reported as elevated delinquency trends in 2024.

HGV monitors indicators like GDP growth (2.5% in 2024) and unemployment (3.7% avg 2024) to adjust pricing and inventory allocation, using dynamic pricing and resale channel expansion to mitigate demand swings.

Inflation and Rising Operating Costs

Persistent inflation raises HGV's resort operating costs—labor, utilities, maintenance—pushing annual owner fees higher; US CPI was 3.4% in 2024 and many utility costs rose double digits in 2023–24, squeezing margins. Significant fee hikes that outpace household income growth (median US household income fell 0.5% real in 2023) risk owner dissatisfaction and higher delinquency rates, already a concern in times of rate stress. HGV must adopt cost-saving tech—energy-efficient systems, predictive maintenance, centralized procurement—and lean management to limit fee increases and protect membership retention.

Credit Market Accessibility

The ability of Hilton Grand Vacations to securitize its vacation ownership notes underpins liquidity and capital structure; in 2024 HGV issued over $1.0 billion of securitized notes, enabling refinance and development funding.

Healthy credit markets—US investment-grade spreads tightening to ~120 bps in 2024—allow efficient capital recycling for resort projects and acquisitions, while a credit tightening could raise funding costs and limit access.

Restricted credit availability would pressure HGV’s leverage management given net debt/EBITDA around 3.5x (2024), complicating growth finance and debt servicing.

- 2024 securitizations: >$1.0B

- 2024 net debt/EBITDA: ~3.5x

- IG spreads 2024: ~120 bps

Foreign Exchange Rate Fluctuations

With operations in over 100 countries, Hilton Grand Vacations faces currency risk that can swing reported international revenues and increase overseas operating costs; in 2024 nearly 18% of net vacation ownership revenue was from non-US markets, amplifying translation exposure.

A strong US dollar can deter international members—Japan accounts for about 6% of owner base—and may reduce bookings and resale activity in key markets.

HGV employs forward contracts, currency swaps and natural hedges; as of FY2024 the company reported hedging coverage for a significant portion of short‑term foreign cash flows to stabilize EBITDA against FX volatility.

- Global exposure: >100 countries; ~18% non‑US vacation revenue (2024)

- Market risk: Japan ~6% of owners; sensitive to USD strength

- Risk management: forwards, swaps, natural hedges; FY2024 hedging program covers major short‑term FX flows

Higher rates squeeze HGV: $1B+ securitizations, 3.5x net debt/EBITDA, US consumer drag

Higher rates (Fed 5.25–5.50% in 2024) raised funding costs and cooled sales; HGV issued >$1.0B securitizations in 2024 and had net debt/EBITDA ~3.5x. US CPI 3.4% and real median household income down 0.5% pressured owner fees and defaults; consumer confidence 88.7 (Dec 2024) and GDP growth 2.5% guided pricing/inventory. FX risk: ~18% non‑US revenue, Japan ~6% owners; hedges cover major short‑term flows.

| Metric | 2024 |

|---|---|

| Fed policy rate | 5.25–5.50% |

| Securitizations | >$1.0B |

| Net debt/EBITDA | ~3.5x |

| US CPI | 3.4% |

| Consumer confidence | 88.7 (Dec) |

| Non‑US revenue | ~18% |

Full Version Awaits

Hilton Grand Vacations PESTLE Analysis

The preview shown here is the exact Hilton Grand Vacations PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our focused PESTLE Analysis of Hilton Grand Vacations—revealing how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape performance and growth opportunities; buy the full report for an actionable, fully editable breakdown to inform investments, strategy, and pitch-ready recommendations.

Political factors

Geopolitical Stability in Key Markets

Hilton Grand Vacations expansion into Japan and Europe exposes it to regional political shifts; in FY2024 international revenue represented about 18% of total revenue, making stability in these markets material to operations.

Political unrest or diplomatic changes can reduce cross-border travel for its ~460,000 members; after COVID, international arrivals to Japan fell 70% in 2020 but recovered to 50% of 2019 levels by 2023, showing sensitivity to geopolitics.

Maintaining a geographically diverse portfolio—North America, Europe, Asia—helps HGV dilute localized political volatility risk, as no single region accounts for more than ~40% of its room inventory.

Tourism Promotion and Incentive Policies

Government-led tourism initiatives boost Hilton Grand Vacations’ U.S. and Asia-Pacific resorts; U.S. Travel Association reported domestic travel spending rose to $1.3 trillion in 2023, while UNWTO noted Asia-Pacific arrivals recovered to ~75% of 2019 levels in 2024, supporting demand.

International Trade and Visa Regulations

Changes in visa rules and trade deals can alter traveler flows to Hilton Grand Vacations resorts; e.g., U.S. travel visa approvals dropped 8% in 2024 vs 2023, tightening visitor pools to destinations like Hawaii where international arrivals fell 6% Y/Y. Stricter immigration limits could reduce demand for timeshare sales from overseas buyers. Management must track trade policy shifts that raised construction import costs—steel and lumber import prices rose ~12% in 2024—impacting new development budgets.

Corporate Taxation and Fiscal Policies

Potential shifts in US federal corporate tax rates or changes in tax treatment for real estate and interest income can materially affect HGV’s net margins; a 1 percentage-point rise in effective tax rate would reduce 2025 adjusted EPS by an estimated mid-single-digit percentage given 2024 tax-effective margins (HGV reported $1.02bn EBITDA in FY2024).

As a capital-intensive business that earned roughly $200–250m annually from financing-related net interest and fees in 2023–2024, HGV is sensitive to fiscal measures that tighten consumer credit or raise corporate borrowing costs, which could compress financing revenue and raise funding expenses.

Adapting to evolving tax regimes across jurisdictions—where statutory rates range from the US federal 21% plus state levies to overseas rates exceeding 25%—is essential for efficient capital allocation, transfer pricing, and optimizing blended tax rates.

- 2024 EBITDA $1.02bn; financing income ~$200–250m

- US federal tax baseline 21%; some jurisdictions >25%

- 1ppt tax rise → mid-single-digit EPS hit (est.)

- High sensitivity to consumer credit and corporate debt costs

Political Influence on Infrastructure Development

The success of Hilton Grand Vacations resorts relies on local infrastructure—airports, roads, utilities—often controlled by political entities; in 2024, destinations with upgraded airports saw 12–18% higher RevPAR for resort-class properties.

Political support for infrastructure projects, such as Florida’s $2.3bn tourism infrastructure allocations in 2024, improves accessibility and HGV property values.

Conversely, political neglect or corruption can cause deteriorating services, lowering occupancy and guest satisfaction.

- Infrastructure upgrades correlate with 12–18% higher RevPAR

- Florida allocated $2.3bn to tourism infrastructure in 2024

- Neglect/corruption reduces occupancy and guest satisfaction

Hilton Grand Vacations: Political risks and trade shifts threaten international revenue and margins

Hilton Grand Vacations faces material political risk from international market shifts—FY2024 international revenue ~18%—making stability in Japan/Europe critical. Visa, trade, and infrastructure policies affect arrivals and costs; e.g., U.S. travel visa approvals −8% in 2024, steel/lumber import prices +12% in 2024. Fiscal/tax changes (US baseline 21%) and credit policy also directly impact margins and financing income (~$200–250m in 2023–24).

| Metric | 2023–24 |

|---|---|

| Intl revenue share | ~18% |

| EBITDA | $1.02bn (2024) |

| Financing income | $200–250m |

| Visa approvals Y/Y | −8% (2024) |

| Import prices (steel/lumber) | +12% (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely affect Hilton Grand Vacations, with data-driven trends and region-specific examples to identify risks, opportunities, and strategic actions for executives, investors, and planners.

A concise PESTLE snapshot for Hilton Grand Vacations that clearly segments political, economic, social, technological, legal, and environmental factors—ideal for quick sharing in presentations or team discussions to align on external risks and opportunity areas.

Economic factors

Interest Rate Volatility

Hilton Grand Vacations finances many vacation ownership purchases, so the Fed's rise to a 5.25–5.50% policy rate in 2024 raised its cost of funding and pressured net interest income; higher rates also cooled consumer loan demand, contributing to a 2024 YTD slowdown in sales growth versus 2023. A 100 bp move can materially widen spread compression on its loan book, making monitoring Fed guidance essential for forecasting sales volume and managing loan-margin risk.

Consumer Discretionary Income Trends

As a luxury leisure product, Hilton Grand Vacations relies on upper-middle-income disposable income; US real disposable personal income rose 1.1% year-over-year in 2024, supporting demand among its core demographic.

Economic downturns or falling consumer confidence—consumer confidence fell to 88.7 in Dec 2024—can defer purchases and increase defaults on vacation-ownership loans, which HGV reported as elevated delinquency trends in 2024.

HGV monitors indicators like GDP growth (2.5% in 2024) and unemployment (3.7% avg 2024) to adjust pricing and inventory allocation, using dynamic pricing and resale channel expansion to mitigate demand swings.

Inflation and Rising Operating Costs

Persistent inflation raises HGV's resort operating costs—labor, utilities, maintenance—pushing annual owner fees higher; US CPI was 3.4% in 2024 and many utility costs rose double digits in 2023–24, squeezing margins. Significant fee hikes that outpace household income growth (median US household income fell 0.5% real in 2023) risk owner dissatisfaction and higher delinquency rates, already a concern in times of rate stress. HGV must adopt cost-saving tech—energy-efficient systems, predictive maintenance, centralized procurement—and lean management to limit fee increases and protect membership retention.

Credit Market Accessibility

The ability of Hilton Grand Vacations to securitize its vacation ownership notes underpins liquidity and capital structure; in 2024 HGV issued over $1.0 billion of securitized notes, enabling refinance and development funding.

Healthy credit markets—US investment-grade spreads tightening to ~120 bps in 2024—allow efficient capital recycling for resort projects and acquisitions, while a credit tightening could raise funding costs and limit access.

Restricted credit availability would pressure HGV’s leverage management given net debt/EBITDA around 3.5x (2024), complicating growth finance and debt servicing.

- 2024 securitizations: >$1.0B

- 2024 net debt/EBITDA: ~3.5x

- IG spreads 2024: ~120 bps

Foreign Exchange Rate Fluctuations

With operations in over 100 countries, Hilton Grand Vacations faces currency risk that can swing reported international revenues and increase overseas operating costs; in 2024 nearly 18% of net vacation ownership revenue was from non-US markets, amplifying translation exposure.

A strong US dollar can deter international members—Japan accounts for about 6% of owner base—and may reduce bookings and resale activity in key markets.

HGV employs forward contracts, currency swaps and natural hedges; as of FY2024 the company reported hedging coverage for a significant portion of short‑term foreign cash flows to stabilize EBITDA against FX volatility.

- Global exposure: >100 countries; ~18% non‑US vacation revenue (2024)

- Market risk: Japan ~6% of owners; sensitive to USD strength

- Risk management: forwards, swaps, natural hedges; FY2024 hedging program covers major short‑term FX flows

Higher rates squeeze HGV: $1B+ securitizations, 3.5x net debt/EBITDA, US consumer drag

Higher rates (Fed 5.25–5.50% in 2024) raised funding costs and cooled sales; HGV issued >$1.0B securitizations in 2024 and had net debt/EBITDA ~3.5x. US CPI 3.4% and real median household income down 0.5% pressured owner fees and defaults; consumer confidence 88.7 (Dec 2024) and GDP growth 2.5% guided pricing/inventory. FX risk: ~18% non‑US revenue, Japan ~6% owners; hedges cover major short‑term flows.

| Metric | 2024 |

|---|---|

| Fed policy rate | 5.25–5.50% |

| Securitizations | >$1.0B |

| Net debt/EBITDA | ~3.5x |

| US CPI | 3.4% |

| Consumer confidence | 88.7 (Dec) |

| Non‑US revenue | ~18% |

Full Version Awaits

Hilton Grand Vacations PESTLE Analysis

The preview shown here is the exact Hilton Grand Vacations PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.