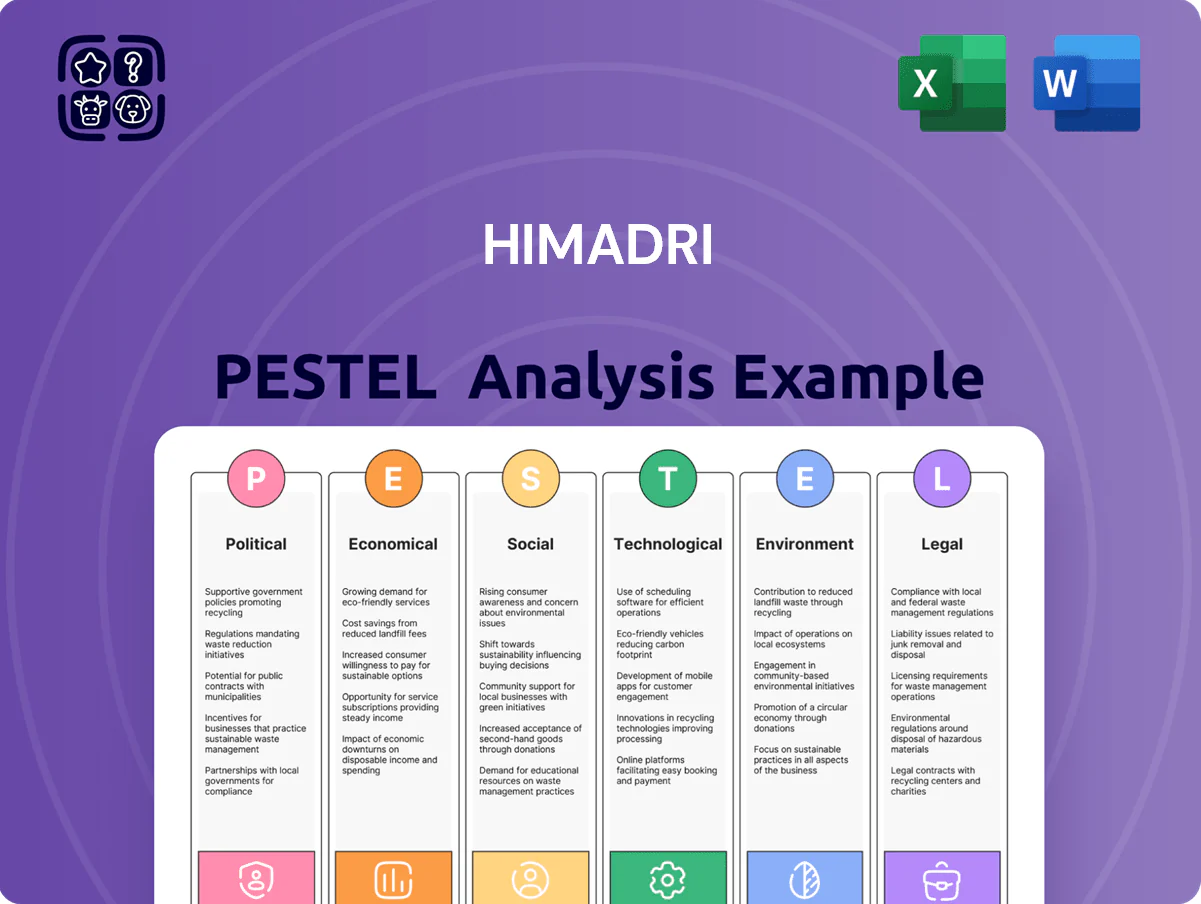

Himadri PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and emerging technologies are reshaping Himadri’s strategic landscape in our concise PESTLE snapshot—perfect for investors and strategists seeking a competitive edge. Purchase the full PESTLE analysis to access detailed risk assessments, regulatory impacts, and actionable insights tailored to Himadri, ready for immediate use in reports and decision-making.

Political factors

Government EV Policy and PLI Schemes

The Indian government’s updated EV subsidy frameworks and tax incentives continue to propel Himadri’s battery materials segment, with EV sales rising 75% YoY to ~1.3 million units in 2024 boosting domestic demand for battery feedstock. Himadri’s participation in the ACC Production Linked Incentive scheme offers fiscal support—up to 20–25% capex-linked incentives—improving margins and scale economics. These measures aim to cut cell import dependency (imports fell ~18% in 2024) and target India as a green manufacturing hub by end-2025.

Geopolitical Trade Dynamics and Tariffs

Fluctuating trade relations between China, the EU and the US have widened specialty chemicals tariffs variability, affecting Himadri’s export-import parity; global chemical trade tensions rose 12% in tariff measures in 2024, squeezing margins. Changes in import duties on coal tar and anthracite from Indonesia and Australia—key sources accounting for ~40% of Himadri’s feedstock—can raise raw material costs by 6–10%. Himadri must hedge supplier mix and use long-term contracts to preserve competitiveness and supply stability.

Strategic Make in India Initiatives

The national Make in India push and Atmanirbhar Bharat drive target boosting local manufacturing of high-tech materials, increasing procurement from domestic suppliers by an estimated 12–15% in government infrastructure projects in 2024–25; Himadri’s production of carbon and graphite electrode feedstock aligns with this policy and supports aluminum and steel sectors.

Global Environmental Accords and Agreements

As a global player, Himadri is constrained by international climate commitments like the Paris Agreement that drive national policy; India targets a 45% emissions intensity reduction by 2030 from 2005 levels, pushing chemical firms toward lower-carbon processes.

India's tightening rules on carbon and hazardous waste—reflected in the 2023 amendment to the Hazardous and Other Waste Rules and rising carbon pricing discussion—force Himadri to invest in cleaner tech and waste treatment to retain operational permits.

These political mandates affect capital allocation: Himadri may need CAPEX increases—industry estimates suggest 5–10% higher upfront costs—to meet compliance, altering long-term plant strategy and permitting timelines.

- Paris-driven national targets: 45% emissions intensity cut by 2030

- 2023 hazardous waste rule tightening raises compliance costs

- Estimated 5–10% higher CAPEX for cleaner technologies

Regional Stability and Industrial Zoning

Political stability in West Bengal, Odisha and Gujarat—where Himadri has major plants—is critical: state GDP growth ranged 6–8% in 2024–25, supporting industrial expansion but exposing projects to regional policy shifts.

State rules on land acquisition, labor and industrial power tariffs (industrial tariff spread 2024: Gujarat 7–8 INR/kWh, West Bengal 6–7 INR/kWh) directly affect capex and operating margins for new facilities.

Maintaining strong local government relations reduced permit delays by an estimated 20–30% in recent Himadri expansions, enabling faster scaling and lower holding costs.

- Key states: West Bengal, Odisha, Gujarat

- State GDP growth 2024–25: ~6–8%

- Industrial power tariffs (2024): Gujarat 7–8 INR/kWh, West Bengal 6–7 INR/kWh

- Permit delay reduction via local engagement: ~20–30%

EV incentives lift battery demand but tariffs, feedstock & emissions rules squeeze margins

Favourable EV incentives and PLI support boost battery-material demand (EV sales ~1.3m in 2024; imports of cells down ~18%), while trade tariffs (+12% tariff measures in 2024) and feedstock duty shifts (Indonesia/Australia sources ~40% of feedstock) raise cost volatility; stricter waste/carbon rules and 45% emissions-intensity target by 2030 force 5–10% higher CAPEX for cleaner tech; state policy, tariffs and permit management affect margins and timelines.

| Metric | 2024/25 |

|---|---|

| EV sales | ~1.3m units |

| Cell imports change | -18% |

| Trade tariff measures | +12% |

| Feedstock from ID/AU | ~40% |

| CAPEX rise for compliance | 5–10% |

| Emissions-intensity target | -45% by 2030 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Himadri, with data-backed trends and region-specific examples to identify risks and opportunities for executives and investors.

Summarizes Himadri’s PESTLE findings into a concise, shareable format that’s easy to drop into presentations or strategy sessions, visually segmented by category for rapid interpretation and quick team alignment.

Economic factors

Volatility in Raw Material Pricing

Himadri’s profitability remains highly sensitive to global coal tar and crude-derivative prices, which rose ~18% YoY in 2024 for coal tar and showed Brent crude averaging $84/bbl in 2024–2025, amplifying feedstock cost pressure.

Commodity-driven cost increases risk margin compression if pass-through to customers is limited; Himadri reported EBITDA margin volatility between 9–13% in 2023–2024.

Maintaining stability through end-2025 requires sophisticated procurement, volume-flexible contracts and hedging; as of 2025 management cited covering ~40% of exposure via long-term contracts and derivatives.

Growth of the Infrastructure and Aluminum Sectors

Demand for coal tar pitch, key to Himadri, tracks aluminum and graphite electrode output tied to infrastructure spending; global infrastructure investment reached about USD 4.5 trillion in 2024, supporting higher aluminium production (global primary aluminium up ~2% to 68.1 Mt in 2024) and electrode demand. Rapid urbanization in India and Southeast Asia lifted construction activity—India’s nominal GDP growth ~7.4% in FY2024—boosting material consumption for Himadri. A slowdown in capital-intensive sectors could reduce offtake and pressure traditional revenue streams, given Himadri’s exposure to these industries.

Interest Rate Environment and Capital Expenditure

The RBI's repo rate at 6.50% (Feb 2025) raises borrowing costs for Himadri's expansion in advanced carbon materials; higher rates lift interest expense and can delay capex on projects costing several hundred crore INR. Maintaining a conservative net debt/equity (Himadri reported 0.42 in FY2024) is crucial to secure financing without excessive dilution. Higher global rates also push up USD-linked loan servicing for exports and technology imports.

Currency Fluctuations and Export Competitiveness

As a major exporter, Himadri's revenue realization shifts with INR moves versus USD/EUR; INR strengthened ~3.4% vs USD in 2024, compressing dollar-denominated revenue when converted to INR unless hedged.

Currency volatility alters export price competitiveness and imported raw-material costs—e.g., a 5% INR depreciation in 2024 would raise imported coal/chemicals costs materially and improve USD sales margins.

Effective FX risk management—forward contracts, options, and natural hedges—remains essential to stabilize margins amid average daily INR-USD volatility of ~0.6% in 2024.

- INR vs USD: +3.4% (2024)

- Avg daily INR-USD vol: ~0.6% (2024)

- 5% INR move materially impacts import costs and export margins

- Hedging tools: forwards, options, natural hedges

Energy Costs and Operational Efficiency

The energy-intensive chemical processes of Himadri make margins sensitive to industrial power and fuel rates; India industrial electricity average rose ~6% y/y in 2024 and Brent-linked fuel volatility pushed input costs up, impacting carbon black and specialty oil unit economics.

Rising energy costs in 2024–25 spur capex in captive power and waste-heat recovery; Himadri disclosed ~₹1.2–1.5 bn annual energy-related savings potential from efficiency projects and continuous process optimization to defend low-cost producer status.

- Industrial electricity +6% y/y (2024)

- Estimated energy-related savings potential ~₹1.2–1.5 bn

- Capex focus: captive power, waste-heat recovery, energy-efficient tech

- Objective: continuous process optimization to reduce unit costs

Himadri margins squeezed by commodity, FX and funding headwinds; ₹1.2–1.5bn savings upside

Himadri faces commodity-driven margin risk: coal tar +18% YoY (2024), Brent ~84$/bbl (2024–25); EBITDA margin 9–13% (2023–24). FX: INR +3.4% vs USD (2024), avg daily vol ~0.6%; ~40% exposure hedged (2025). RBI repo 6.50% (Feb 2025) raises funding costs; net debt/equity 0.42 (FY2024). Energy costs +6% y/y (2024); estimated savings potential ₹1.2–1.5 bn.

| Metric | Value |

|---|---|

| Coal tar YoY (2024) | +18% |

| Brent | $84/bbl |

| INR vs USD (2024) | +3.4% |

| Repo rate (Feb 2025) | 6.50% |

| Net D/E (FY2024) | 0.42 |

| Energy cost rise (2024) | +6% |

| Energy savings potential | ₹1.2–1.5 bn |

Full Version Awaits

Himadri PESTLE Analysis

The preview shown here is the exact Himadri PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and emerging technologies are reshaping Himadri’s strategic landscape in our concise PESTLE snapshot—perfect for investors and strategists seeking a competitive edge. Purchase the full PESTLE analysis to access detailed risk assessments, regulatory impacts, and actionable insights tailored to Himadri, ready for immediate use in reports and decision-making.

Political factors

Government EV Policy and PLI Schemes

The Indian government’s updated EV subsidy frameworks and tax incentives continue to propel Himadri’s battery materials segment, with EV sales rising 75% YoY to ~1.3 million units in 2024 boosting domestic demand for battery feedstock. Himadri’s participation in the ACC Production Linked Incentive scheme offers fiscal support—up to 20–25% capex-linked incentives—improving margins and scale economics. These measures aim to cut cell import dependency (imports fell ~18% in 2024) and target India as a green manufacturing hub by end-2025.

Geopolitical Trade Dynamics and Tariffs

Fluctuating trade relations between China, the EU and the US have widened specialty chemicals tariffs variability, affecting Himadri’s export-import parity; global chemical trade tensions rose 12% in tariff measures in 2024, squeezing margins. Changes in import duties on coal tar and anthracite from Indonesia and Australia—key sources accounting for ~40% of Himadri’s feedstock—can raise raw material costs by 6–10%. Himadri must hedge supplier mix and use long-term contracts to preserve competitiveness and supply stability.

Strategic Make in India Initiatives

The national Make in India push and Atmanirbhar Bharat drive target boosting local manufacturing of high-tech materials, increasing procurement from domestic suppliers by an estimated 12–15% in government infrastructure projects in 2024–25; Himadri’s production of carbon and graphite electrode feedstock aligns with this policy and supports aluminum and steel sectors.

Global Environmental Accords and Agreements

As a global player, Himadri is constrained by international climate commitments like the Paris Agreement that drive national policy; India targets a 45% emissions intensity reduction by 2030 from 2005 levels, pushing chemical firms toward lower-carbon processes.

India's tightening rules on carbon and hazardous waste—reflected in the 2023 amendment to the Hazardous and Other Waste Rules and rising carbon pricing discussion—force Himadri to invest in cleaner tech and waste treatment to retain operational permits.

These political mandates affect capital allocation: Himadri may need CAPEX increases—industry estimates suggest 5–10% higher upfront costs—to meet compliance, altering long-term plant strategy and permitting timelines.

- Paris-driven national targets: 45% emissions intensity cut by 2030

- 2023 hazardous waste rule tightening raises compliance costs

- Estimated 5–10% higher CAPEX for cleaner technologies

Regional Stability and Industrial Zoning

Political stability in West Bengal, Odisha and Gujarat—where Himadri has major plants—is critical: state GDP growth ranged 6–8% in 2024–25, supporting industrial expansion but exposing projects to regional policy shifts.

State rules on land acquisition, labor and industrial power tariffs (industrial tariff spread 2024: Gujarat 7–8 INR/kWh, West Bengal 6–7 INR/kWh) directly affect capex and operating margins for new facilities.

Maintaining strong local government relations reduced permit delays by an estimated 20–30% in recent Himadri expansions, enabling faster scaling and lower holding costs.

- Key states: West Bengal, Odisha, Gujarat

- State GDP growth 2024–25: ~6–8%

- Industrial power tariffs (2024): Gujarat 7–8 INR/kWh, West Bengal 6–7 INR/kWh

- Permit delay reduction via local engagement: ~20–30%

EV incentives lift battery demand but tariffs, feedstock & emissions rules squeeze margins

Favourable EV incentives and PLI support boost battery-material demand (EV sales ~1.3m in 2024; imports of cells down ~18%), while trade tariffs (+12% tariff measures in 2024) and feedstock duty shifts (Indonesia/Australia sources ~40% of feedstock) raise cost volatility; stricter waste/carbon rules and 45% emissions-intensity target by 2030 force 5–10% higher CAPEX for cleaner tech; state policy, tariffs and permit management affect margins and timelines.

| Metric | 2024/25 |

|---|---|

| EV sales | ~1.3m units |

| Cell imports change | -18% |

| Trade tariff measures | +12% |

| Feedstock from ID/AU | ~40% |

| CAPEX rise for compliance | 5–10% |

| Emissions-intensity target | -45% by 2030 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Himadri, with data-backed trends and region-specific examples to identify risks and opportunities for executives and investors.

Summarizes Himadri’s PESTLE findings into a concise, shareable format that’s easy to drop into presentations or strategy sessions, visually segmented by category for rapid interpretation and quick team alignment.

Economic factors

Volatility in Raw Material Pricing

Himadri’s profitability remains highly sensitive to global coal tar and crude-derivative prices, which rose ~18% YoY in 2024 for coal tar and showed Brent crude averaging $84/bbl in 2024–2025, amplifying feedstock cost pressure.

Commodity-driven cost increases risk margin compression if pass-through to customers is limited; Himadri reported EBITDA margin volatility between 9–13% in 2023–2024.

Maintaining stability through end-2025 requires sophisticated procurement, volume-flexible contracts and hedging; as of 2025 management cited covering ~40% of exposure via long-term contracts and derivatives.

Growth of the Infrastructure and Aluminum Sectors

Demand for coal tar pitch, key to Himadri, tracks aluminum and graphite electrode output tied to infrastructure spending; global infrastructure investment reached about USD 4.5 trillion in 2024, supporting higher aluminium production (global primary aluminium up ~2% to 68.1 Mt in 2024) and electrode demand. Rapid urbanization in India and Southeast Asia lifted construction activity—India’s nominal GDP growth ~7.4% in FY2024—boosting material consumption for Himadri. A slowdown in capital-intensive sectors could reduce offtake and pressure traditional revenue streams, given Himadri’s exposure to these industries.

Interest Rate Environment and Capital Expenditure

The RBI's repo rate at 6.50% (Feb 2025) raises borrowing costs for Himadri's expansion in advanced carbon materials; higher rates lift interest expense and can delay capex on projects costing several hundred crore INR. Maintaining a conservative net debt/equity (Himadri reported 0.42 in FY2024) is crucial to secure financing without excessive dilution. Higher global rates also push up USD-linked loan servicing for exports and technology imports.

Currency Fluctuations and Export Competitiveness

As a major exporter, Himadri's revenue realization shifts with INR moves versus USD/EUR; INR strengthened ~3.4% vs USD in 2024, compressing dollar-denominated revenue when converted to INR unless hedged.

Currency volatility alters export price competitiveness and imported raw-material costs—e.g., a 5% INR depreciation in 2024 would raise imported coal/chemicals costs materially and improve USD sales margins.

Effective FX risk management—forward contracts, options, and natural hedges—remains essential to stabilize margins amid average daily INR-USD volatility of ~0.6% in 2024.

- INR vs USD: +3.4% (2024)

- Avg daily INR-USD vol: ~0.6% (2024)

- 5% INR move materially impacts import costs and export margins

- Hedging tools: forwards, options, natural hedges

Energy Costs and Operational Efficiency

The energy-intensive chemical processes of Himadri make margins sensitive to industrial power and fuel rates; India industrial electricity average rose ~6% y/y in 2024 and Brent-linked fuel volatility pushed input costs up, impacting carbon black and specialty oil unit economics.

Rising energy costs in 2024–25 spur capex in captive power and waste-heat recovery; Himadri disclosed ~₹1.2–1.5 bn annual energy-related savings potential from efficiency projects and continuous process optimization to defend low-cost producer status.

- Industrial electricity +6% y/y (2024)

- Estimated energy-related savings potential ~₹1.2–1.5 bn

- Capex focus: captive power, waste-heat recovery, energy-efficient tech

- Objective: continuous process optimization to reduce unit costs

Himadri margins squeezed by commodity, FX and funding headwinds; ₹1.2–1.5bn savings upside

Himadri faces commodity-driven margin risk: coal tar +18% YoY (2024), Brent ~84$/bbl (2024–25); EBITDA margin 9–13% (2023–24). FX: INR +3.4% vs USD (2024), avg daily vol ~0.6%; ~40% exposure hedged (2025). RBI repo 6.50% (Feb 2025) raises funding costs; net debt/equity 0.42 (FY2024). Energy costs +6% y/y (2024); estimated savings potential ₹1.2–1.5 bn.

| Metric | Value |

|---|---|

| Coal tar YoY (2024) | +18% |

| Brent | $84/bbl |

| INR vs USD (2024) | +3.4% |

| Repo rate (Feb 2025) | 6.50% |

| Net D/E (FY2024) | 0.42 |

| Energy cost rise (2024) | +6% |

| Energy savings potential | ₹1.2–1.5 bn |

Full Version Awaits

Himadri PESTLE Analysis

The preview shown here is the exact Himadri PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.