Hirogin Holdings SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Hirogin Holdings shows resilient regional market reach and diversified financial services, tempered by heavy regulation and exposure to interest-rate cycles; its growth hinges on digital transformation and cross-border expansion. Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

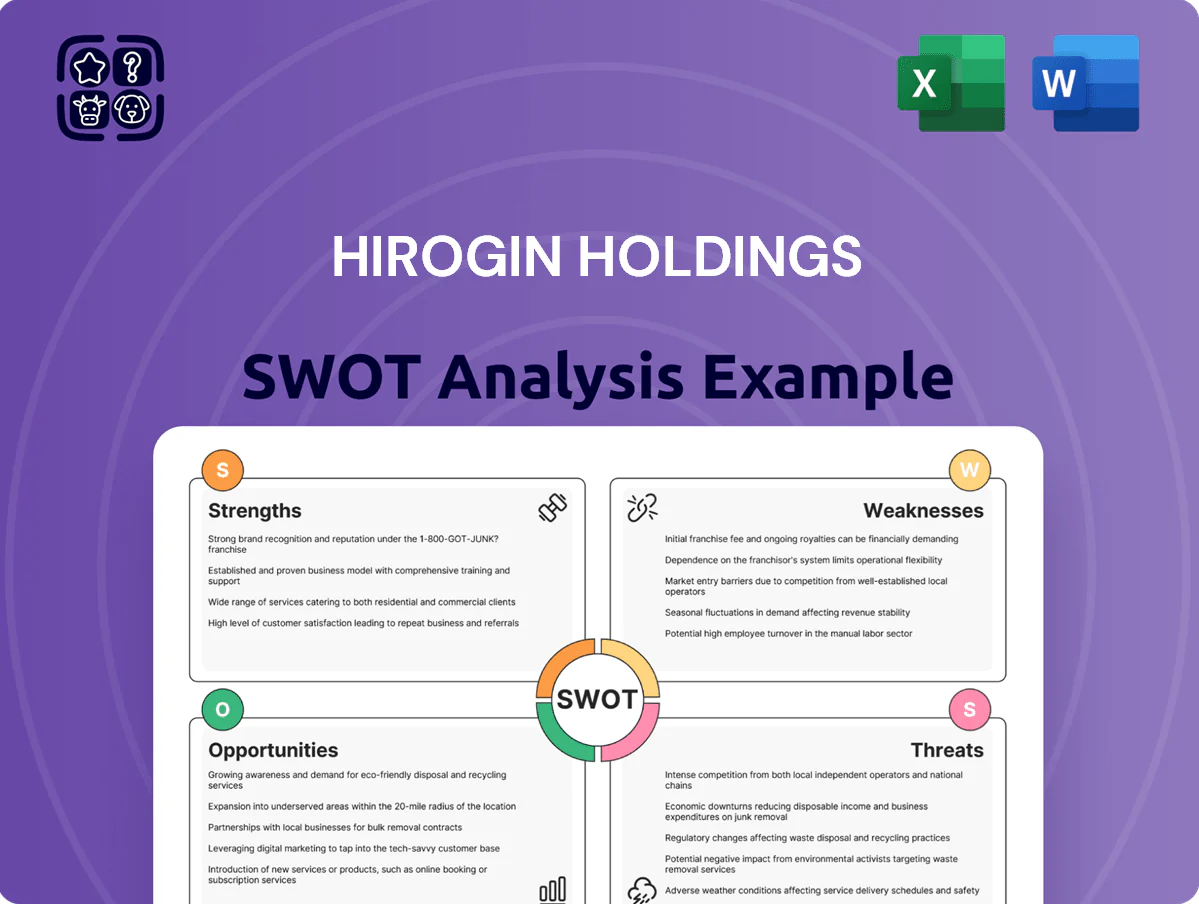

Strengths

Dominant Regional Market Share

Hirogin Holdings controls roughly 45% of Hiroshima Prefecture’s deposits (about ¥1.2 trillion as of FY2024), making it the primary bank for many local firms and 290,000+ households; that scale gives a stable, low-cost deposit base.

Deep local knowledge—branch network density of 1 branch per 15,000 residents—boosts credit quality and product fit, lowering default rates compared with national peers.

Proximity drives high loyalty: 70%+ of SMEs use Hirogin as main bank, creating strong switching costs and meaningful barriers to entry for national banks.

Diversified Financial Service Portfolio

Hirogin Holdings runs banking plus leasing, securities, and credit-card arms, which in FY2024 produced about ¥62.3bn in non-interest income—roughly 38% of total revenue—helping diversify cash flow beyond net interest margin pressures.

Strong Ties to Manufacturing Sector

The group maintains deep ties with regional industrial leaders, notably in automotive and shipbuilding, supporting roughly ¥320 billion in corporate loans and ¥85 billion in trade finance lines as of Q4 2025.

Solid Capital Adequacy Ratios

Hirogin Holdings posts CET1 (common equity tier 1) around 12.5% and total capital ratio near 15% as of FY2024, comfortably above Japan’s minimums and providing a buffer against shocks.

These ratios fund steady dividends and buybacks while enabling JPY 120–150 billion planned digital and regional investments through 2026; a strong balance sheet boosts investor confidence and strategic flexibility.

- CET1 ~12.5%

- Total capital ~15%

- Planned investments JPY 120–150bn

- Supports dividends, buybacks, resilience

Advanced Digital Transformation Progress

- 68% active customers using digital channels by end-2025

- 54% increase in e-transactions YoY (2025)

- 38% drop in branch visits

- JPY 12.4 billion OPEX savings in 2025

- 11% reduction in operating costs

Hirogin: Dominant Hiroshima bank—45% deposits, strong SME franchise, digital surge

Hirogin controls ~45% of Hiroshima deposits (≈¥1.2tn FY2024), 290k+ households; CET1 ~12.5% and total capital ~15% (FY2024), planned JPY120–150bn investments to 2026; digital users 68% (end‑2025), e-transactions +54% YoY, OPEX savings JPY12.4bn (2025); strong SME share (70%+ main‑bank) and ¥320bn corporate loan exposure to local industries.

| Metric | Value |

|---|---|

| Deposits share | 45% (¥1.2tn) |

| CET1 | 12.5% |

| Digital users | 68% |

What is included in the product

Provides a concise SWOT overview of Hirogin Holdings by mapping internal strengths and weaknesses against external opportunities and threats to clarify strategic priorities and competitive positioning.

Provides a concise Hirogin Holdings SWOT snapshot for rapid strategic alignment and clear stakeholder briefings.

Weaknesses

High Geographic Concentration

The group's assets and over 80% of net loans are tied to Hiroshima and nearby prefectures, so a local recession would cut loan demand and push NPLs higher across Hirogin Holdings.

In 2024 Hiroshima GDP fell 1.2% year-on-year and regional household income slipped 0.9%, showing how quickly revenues can shrink when the local economy weakens.

Elevated Operating Cost Structure

Hirogin’s legacy branch network and headcount keep its 2025 cost-to-income ratio near 62%, versus 48–52% for larger national peers, squeezing net interest margins and ROE. Maintaining rural branches supports financial inclusion but cuts branch-level ROA by an estimated 60–80 bps. Planned branch rationalizations hit delays from local opposition, slowing targeted annual overhead cuts of ¥6–8bn.

Dependency on Specific Industrial Cycles

The bank’s loan book is heavily concentrated in manufacturing and automotive supply chains, exposing it to global trade shifts and industrial transitions; 62% of corporate loans were to these sectors as of FY2024, up from 55% in 2021.

If regional industries face structural disruption—like the EV shift—nonperforming loans could rise quickly; Japan’s auto parts demand fell 8% YoY in Q3 2024, a warning sign.

This sector-specific exposure needs continuous monitoring and proactive risk controls—stress tests, concentration limits, and quarterly reviews—to prevent large loan losses.

Limited Non-Interest Income Growth

- 68% operating income from lending

- Non-interest ratio 32% in 2024

- Fee-income growth 4.2% YoY (2024)

- Peer fee growth ~12% YoY

Slow International Expansion

Hirogin Holdings lags larger peers in overseas presence, with international revenue under 8% of consolidated net sales in FY2024, limiting access to high-growth Asia-Pacific and cross-border fee income.

This domestic focus ties growth to Japan’s ~0.5% GDP trend in 2024, reducing diversification and hindering support for clients expanding abroad.

- International revenue <8% (FY2024)

- Missed cross-border fees

- Exposure to Japan’s ~0.5% GDP (2024)

Hirogin risk: regional slump, auto exposure and bloated costs squeeze margins

Hirogin is highly regional: 80%+ net loans tied to Hiroshima area, so local GDP (-1.2% in 2024) and household income (-0.9% 2024) sharply affect NPLs and loan demand; 62% of corporate loans are manufacturing/auto supply chains, vulnerable to trade and EV shifts (auto parts demand -8% YoY Q3 2024). Cost base is high: 2025 C/I ~62% vs peers 48–52%, ROA hit by rural branches; 68% of FY2024 operating income from lending; fee income growth 4.2% (2024) vs peer ~12%; international revenue <8% (FY2024).

| Metric | Value |

|---|---|

| Regional loan share | 80%+ |

| Hiroshima GDP 2024 | -1.2% YoY |

| Cost-to-income (2025) | ~62% |

| Corp loans to auto/manuf | 62% (FY2024) |

| Fee income growth 2024 | 4.2% YoY |

| International revenue FY2024 | <8% |

Preview Before You Purchase

Hirogin Holdings SWOT Analysis

This is the actual Hirogin Holdings SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is pulled directly from the full, editable report and the complete version is unlocked after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Hirogin Holdings shows resilient regional market reach and diversified financial services, tempered by heavy regulation and exposure to interest-rate cycles; its growth hinges on digital transformation and cross-border expansion. Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

Dominant Regional Market Share

Hirogin Holdings controls roughly 45% of Hiroshima Prefecture’s deposits (about ¥1.2 trillion as of FY2024), making it the primary bank for many local firms and 290,000+ households; that scale gives a stable, low-cost deposit base.

Deep local knowledge—branch network density of 1 branch per 15,000 residents—boosts credit quality and product fit, lowering default rates compared with national peers.

Proximity drives high loyalty: 70%+ of SMEs use Hirogin as main bank, creating strong switching costs and meaningful barriers to entry for national banks.

Diversified Financial Service Portfolio

Hirogin Holdings runs banking plus leasing, securities, and credit-card arms, which in FY2024 produced about ¥62.3bn in non-interest income—roughly 38% of total revenue—helping diversify cash flow beyond net interest margin pressures.

Strong Ties to Manufacturing Sector

The group maintains deep ties with regional industrial leaders, notably in automotive and shipbuilding, supporting roughly ¥320 billion in corporate loans and ¥85 billion in trade finance lines as of Q4 2025.

Solid Capital Adequacy Ratios

Hirogin Holdings posts CET1 (common equity tier 1) around 12.5% and total capital ratio near 15% as of FY2024, comfortably above Japan’s minimums and providing a buffer against shocks.

These ratios fund steady dividends and buybacks while enabling JPY 120–150 billion planned digital and regional investments through 2026; a strong balance sheet boosts investor confidence and strategic flexibility.

- CET1 ~12.5%

- Total capital ~15%

- Planned investments JPY 120–150bn

- Supports dividends, buybacks, resilience

Advanced Digital Transformation Progress

- 68% active customers using digital channels by end-2025

- 54% increase in e-transactions YoY (2025)

- 38% drop in branch visits

- JPY 12.4 billion OPEX savings in 2025

- 11% reduction in operating costs

Hirogin: Dominant Hiroshima bank—45% deposits, strong SME franchise, digital surge

Hirogin controls ~45% of Hiroshima deposits (≈¥1.2tn FY2024), 290k+ households; CET1 ~12.5% and total capital ~15% (FY2024), planned JPY120–150bn investments to 2026; digital users 68% (end‑2025), e-transactions +54% YoY, OPEX savings JPY12.4bn (2025); strong SME share (70%+ main‑bank) and ¥320bn corporate loan exposure to local industries.

| Metric | Value |

|---|---|

| Deposits share | 45% (¥1.2tn) |

| CET1 | 12.5% |

| Digital users | 68% |

What is included in the product

Provides a concise SWOT overview of Hirogin Holdings by mapping internal strengths and weaknesses against external opportunities and threats to clarify strategic priorities and competitive positioning.

Provides a concise Hirogin Holdings SWOT snapshot for rapid strategic alignment and clear stakeholder briefings.

Weaknesses

High Geographic Concentration

The group's assets and over 80% of net loans are tied to Hiroshima and nearby prefectures, so a local recession would cut loan demand and push NPLs higher across Hirogin Holdings.

In 2024 Hiroshima GDP fell 1.2% year-on-year and regional household income slipped 0.9%, showing how quickly revenues can shrink when the local economy weakens.

Elevated Operating Cost Structure

Hirogin’s legacy branch network and headcount keep its 2025 cost-to-income ratio near 62%, versus 48–52% for larger national peers, squeezing net interest margins and ROE. Maintaining rural branches supports financial inclusion but cuts branch-level ROA by an estimated 60–80 bps. Planned branch rationalizations hit delays from local opposition, slowing targeted annual overhead cuts of ¥6–8bn.

Dependency on Specific Industrial Cycles

The bank’s loan book is heavily concentrated in manufacturing and automotive supply chains, exposing it to global trade shifts and industrial transitions; 62% of corporate loans were to these sectors as of FY2024, up from 55% in 2021.

If regional industries face structural disruption—like the EV shift—nonperforming loans could rise quickly; Japan’s auto parts demand fell 8% YoY in Q3 2024, a warning sign.

This sector-specific exposure needs continuous monitoring and proactive risk controls—stress tests, concentration limits, and quarterly reviews—to prevent large loan losses.

Limited Non-Interest Income Growth

- 68% operating income from lending

- Non-interest ratio 32% in 2024

- Fee-income growth 4.2% YoY (2024)

- Peer fee growth ~12% YoY

Slow International Expansion

Hirogin Holdings lags larger peers in overseas presence, with international revenue under 8% of consolidated net sales in FY2024, limiting access to high-growth Asia-Pacific and cross-border fee income.

This domestic focus ties growth to Japan’s ~0.5% GDP trend in 2024, reducing diversification and hindering support for clients expanding abroad.

- International revenue <8% (FY2024)

- Missed cross-border fees

- Exposure to Japan’s ~0.5% GDP (2024)

Hirogin risk: regional slump, auto exposure and bloated costs squeeze margins

Hirogin is highly regional: 80%+ net loans tied to Hiroshima area, so local GDP (-1.2% in 2024) and household income (-0.9% 2024) sharply affect NPLs and loan demand; 62% of corporate loans are manufacturing/auto supply chains, vulnerable to trade and EV shifts (auto parts demand -8% YoY Q3 2024). Cost base is high: 2025 C/I ~62% vs peers 48–52%, ROA hit by rural branches; 68% of FY2024 operating income from lending; fee income growth 4.2% (2024) vs peer ~12%; international revenue <8% (FY2024).

| Metric | Value |

|---|---|

| Regional loan share | 80%+ |

| Hiroshima GDP 2024 | -1.2% YoY |

| Cost-to-income (2025) | ~62% |

| Corp loans to auto/manuf | 62% (FY2024) |

| Fee income growth 2024 | 4.2% YoY |

| International revenue FY2024 | <8% |

Preview Before You Purchase

Hirogin Holdings SWOT Analysis

This is the actual Hirogin Holdings SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is pulled directly from the full, editable report and the complete version is unlocked after payment.