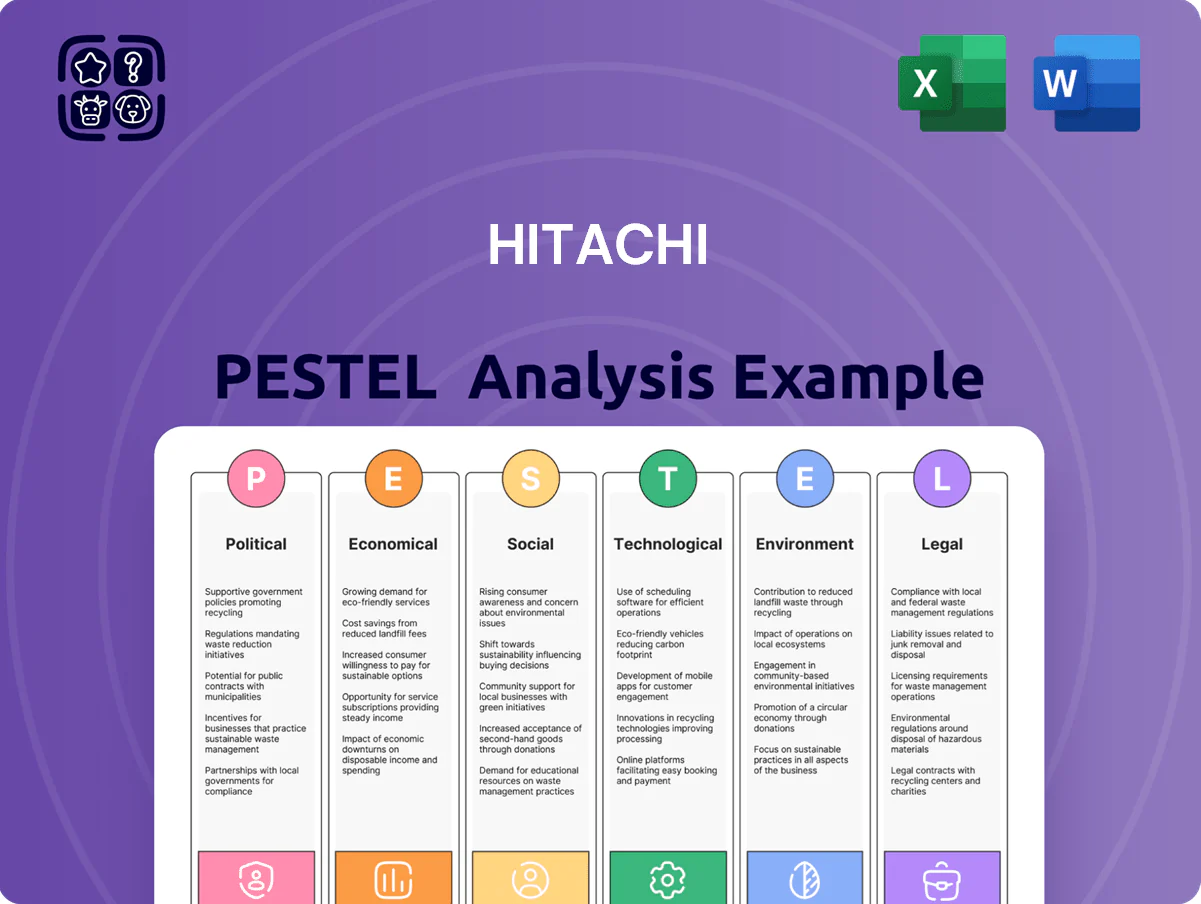

Hitachi PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our concise PESTLE Analysis of Hitachi—explore how political shifts, economic trends, social changes, technological innovation, legal risks, and environmental pressures are reshaping its outlook; buy the full analysis to access ready-to-use, expert insights and actionable recommendations for investors, consultants, and strategists.

Political factors

Geopolitical instability and supply chain security

Ongoing US-China tensions force Hitachi to diversify supply chains and manufacturing hubs; by Q3 2025 the company reported shifting 12% of component sourcing away from China and expanding production in Southeast Asia and Japan to reduce exposure.

Export controls on semiconductors and AI-related tech require Hitachi to secure export licenses and adapt contracts across 30+ countries while keeping projects aligned with regional security alliances like the Quad and EU frameworks.

Maintaining compliance in digital infrastructure deals has increased compliance costs by an estimated 4–6% of capex in 2024–25, necessitating a flexible geographic footprint to mitigate sudden trade barriers or sanctions.

Governmental focus on digital transformation

Japan's Society 5.0 and EU digital recovery funds, plus Southeast Asia's $100B+ smart city pipelines, create strong tailwinds for Hitachi's IT/OT integration; Lumada targets these state-backed markets, supporting Hitachi's ¥8.5T FY2024 order backlog and recurring revenue growth.

Global energy policy shifts

As countries push for net-zero, mandates boosting renewables and nuclear expansion directly increase demand for Hitachi Energy and Hitachi-GE Nuclear, with global clean energy investment reaching $1.7 trillion in 2023 and expected to grow in 2024–25.

Hitachi gains from subsidies—e.g., EU and US allocations for green hydrogen and carbon capture (US IRA commitments of $369bn energy-related tax credits through 2031)—supporting its H2 and CCUS projects.

Revived nuclear programs in UK, Japan and Poland add pipeline value; Hitachi's EDF/UK opportunities align with ~£160bn planned UK nuclear investments to 2050.

Political stability in energy-dependent markets remains vital for Hitachi’s long-term capital-intensive projects, where financing and permits determine ROI and project timelines.

Regional infrastructure investment acts

Major legislative packages such as the US Infrastructure Investment and Jobs Act (USD 1.2 trillion, 2021) and the European Green Deal (EUR 1 trillion mobilization aim) boost demand for Hitachi’s mobility and industrial solutions by funding rail projects and grid upgrades where Hitachi holds marketable expertise.

These policies allocate billions for rail and power: the US bill includes USD 66 billion for rail and tens of billions for grid modernization; EU recovery and Green Deal funding channels similarly prioritize electrification and smart grids, aligning with Hitachi Energy and Hitachi Rail offerings.

Navigating local content and Buy America/Buy European rules—often requiring domestic manufacturing or sourcing—remains a strategic priority to secure contracts and protect market share amid competitive bidding.

- US IIJA: USD 66B rail, large grid funding

- EU Green Deal: ~EUR 1T mobilization

- Policy-driven demand for rail, grid, electrification

- Local content rules critical for contract eligibility

Data sovereignty and localization laws

Rising data sovereignty laws force Hitachi to localize cloud and digital services, reshaping deployment: over 60% of G20 countries tightened data localization rules by 2024, raising compliance costs and CAPEX for regional data centers.

Hitachi must redesign software and edge architectures to meet differing standards—noncompliance risks losing access to government and enterprise tenders worth billions; Japan’s public-sector IT contracts exceeded ¥3.5 trillion in 2023.

Geopolitics, green subsidies fuel Hitachi’s ¥8.5T backlog as supply shifts 12%

Geopolitical tensions (US-China) and export controls raised compliance costs ~4–6% of capex (2024–25) and pushed Hitachi to shift 12% sourcing from China, expanding SE Asia/Japan production; state funds (Japan Society 5.0, EU digital recovery, SE Asia $100B smart-city pipelines) and green subsidies (US IRA $369B energy credits) drive demand for Hitachi Energy, Rail and Lumada, supporting ¥8.5T FY2024 order backlog.

| Metric | Value |

|---|---|

| Sourcing shifted from China | 12% |

| Capex compliance impact (2024–25) | 4–6% |

| Hitachi FY2024 order backlog | ¥8.5T |

| Global clean energy investment (2023) | $1.7T |

| US IRA energy tax credits | $369B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Hitachi across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and industry trends to identify threats and opportunities.

A concise, visually segmented Hitachi PESTLE summary that relieves meeting prep pain by highlighting key external risks and opportunities for quick inclusion in presentations or strategy sessions.

Economic factors

Interest rate fluctuations and capital costs

The global shift in central bank policies through 2025 pushed average OECD policy rates up ~100–150bps versus 2023, raising borrowing costs for large-scale infrastructure; 10‑yr government yields rose to ~3.5–4.0% in major markets, tightening project finance. Higher rates have already prompted reported delays in energy and mobility CAPEX—project pipeline slowdowns of 10–20% in some regions—pressuring Hitachi to optimize its debt mix. Hitachi must actively manage its ¥/USD debt profile, hedges and pricing to protect EBITDA margins (Hitachi reported ¥1.3tn EBITDA in FY2024) amid volatile rates.

Currency exchange rate volatility

As a Japanese multinational, Hitachi’s FY2024 revenue mix—roughly 55% from overseas—makes it highly sensitive to JPY/USD and JPY/EUR moves; JPY weakened ~6% vs USD in 2023-24, bolstering export competitiveness but raising imported energy/raw material costs by similar percentages.

Hitachi reported a ¥50.5bn FX loss in FY2024; the firm uses forward hedges and natural hedges through ¥1.2tn localized overseas capital expenditure to limit consolidated profit volatility.

Inflationary pressure on operational costs

Persistent inflation in labor and material costs—Japan CPI rose 3.1% in 2024 and global steel prices averaged up 12% YoY—forces Hitachi to drive productivity and pricing measures to protect margins.

Hitachi is investing in automation and digital twins across operations; its FY2024 capex rose to ¥620bn to boost efficiency and offset input-cost inflation.

Maintaining profitability hinges on passing costs to customers without ceding share to lower-cost rivals, with Hitachi targeting double-digit productivity gains to do so.

Economic growth trends in emerging markets

Hitachi’s strategy targets Southeast Asia and India where middle-class households are projected to reach 2.8bn by 2030, driving demand for smart life solutions, transit systems, and power infrastructure; ASEAN GDP grew 4.5% in 2023 while India expanded ~7.2% in FY2023–24, supporting project pipelines.

Exposure raises risks from cyclical slowdowns and sovereign or banking liquidity strains—IMF warned of emerging-market debt stress with external financing needs of $2.4tn in 2024–25 for low-income countries.

- Market growth: ASEAN 4.5% (2023), India ~7.2% (FY23–24)

- Demand drivers: rising middle class to 2030 (~2.8bn)

- Revenue opportunity: infrastructure & smart systems

- Risks: economic cycles, EM liquidity needs ~$2.4tn (2024–25)

Global semiconductor and component availability

The global semiconductor shortage trimmed global chip supply by an estimated 10–15% in 2024, keeping prices elevated; Hitachi’s products—from industrial robots to railway signaling—are exposed to this volatility because advanced ICs comprise a growing share of BOM costs.

Hitachi mitigates risk via strategic inventory and multi-year supplier contracts; in FY2024 the company reported inventory days around 85, underscoring emphasis on buffer stocks to protect manufacturing throughput.

- 10–15% global chip shortfall in 2024

- Hitachi FY2024 inventory ≈85 days

- High-tech BOM share rising, increasing vulnerability

- Long-term supplier contracts and buffer inventory are key safeguards

Higher rates squeeze Hitachi's ¥1.3tn EBITDA; JPY weakness aids exports, boosts costs

Higher global rates (10y ~3.5–4.0%) and OECD policy rates +100–150bps to 2025 raise project financing costs, pressuring Hitachi’s ¥1.3tn FY2024 EBITDA and prompting ¥/USD hedge and debt-mix actions; JPY weakened ~6% vs USD (2023–24) aiding exports but adding ~6% input cost pressure.

FY2024: revenue 55% overseas, capex ¥620bn, inventory ~85 days; ASEAN GDP +4.5% (2023), India +7.2% (FY23–24); EM external financing needs ~$2.4tn (2024–25).

| Metric | Value |

|---|---|

| EBITDA FY2024 | ¥1.3tn |

| Capex FY2024 | ¥620bn |

| Inventory days | ~85 |

| Overseas revenue | ~55% |

| JPY vs USD (2023–24) | -6% |

| ASEAN GDP (2023) | +4.5% |

| India GDP (FY23–24) | +7.2% |

| EM financing need (2024–25) | $2.4tn |

Full Version Awaits

Hitachi PESTLE Analysis

The preview shown here is the exact Hitachi PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our concise PESTLE Analysis of Hitachi—explore how political shifts, economic trends, social changes, technological innovation, legal risks, and environmental pressures are reshaping its outlook; buy the full analysis to access ready-to-use, expert insights and actionable recommendations for investors, consultants, and strategists.

Political factors

Geopolitical instability and supply chain security

Ongoing US-China tensions force Hitachi to diversify supply chains and manufacturing hubs; by Q3 2025 the company reported shifting 12% of component sourcing away from China and expanding production in Southeast Asia and Japan to reduce exposure.

Export controls on semiconductors and AI-related tech require Hitachi to secure export licenses and adapt contracts across 30+ countries while keeping projects aligned with regional security alliances like the Quad and EU frameworks.

Maintaining compliance in digital infrastructure deals has increased compliance costs by an estimated 4–6% of capex in 2024–25, necessitating a flexible geographic footprint to mitigate sudden trade barriers or sanctions.

Governmental focus on digital transformation

Japan's Society 5.0 and EU digital recovery funds, plus Southeast Asia's $100B+ smart city pipelines, create strong tailwinds for Hitachi's IT/OT integration; Lumada targets these state-backed markets, supporting Hitachi's ¥8.5T FY2024 order backlog and recurring revenue growth.

Global energy policy shifts

As countries push for net-zero, mandates boosting renewables and nuclear expansion directly increase demand for Hitachi Energy and Hitachi-GE Nuclear, with global clean energy investment reaching $1.7 trillion in 2023 and expected to grow in 2024–25.

Hitachi gains from subsidies—e.g., EU and US allocations for green hydrogen and carbon capture (US IRA commitments of $369bn energy-related tax credits through 2031)—supporting its H2 and CCUS projects.

Revived nuclear programs in UK, Japan and Poland add pipeline value; Hitachi's EDF/UK opportunities align with ~£160bn planned UK nuclear investments to 2050.

Political stability in energy-dependent markets remains vital for Hitachi’s long-term capital-intensive projects, where financing and permits determine ROI and project timelines.

Regional infrastructure investment acts

Major legislative packages such as the US Infrastructure Investment and Jobs Act (USD 1.2 trillion, 2021) and the European Green Deal (EUR 1 trillion mobilization aim) boost demand for Hitachi’s mobility and industrial solutions by funding rail projects and grid upgrades where Hitachi holds marketable expertise.

These policies allocate billions for rail and power: the US bill includes USD 66 billion for rail and tens of billions for grid modernization; EU recovery and Green Deal funding channels similarly prioritize electrification and smart grids, aligning with Hitachi Energy and Hitachi Rail offerings.

Navigating local content and Buy America/Buy European rules—often requiring domestic manufacturing or sourcing—remains a strategic priority to secure contracts and protect market share amid competitive bidding.

- US IIJA: USD 66B rail, large grid funding

- EU Green Deal: ~EUR 1T mobilization

- Policy-driven demand for rail, grid, electrification

- Local content rules critical for contract eligibility

Data sovereignty and localization laws

Rising data sovereignty laws force Hitachi to localize cloud and digital services, reshaping deployment: over 60% of G20 countries tightened data localization rules by 2024, raising compliance costs and CAPEX for regional data centers.

Hitachi must redesign software and edge architectures to meet differing standards—noncompliance risks losing access to government and enterprise tenders worth billions; Japan’s public-sector IT contracts exceeded ¥3.5 trillion in 2023.

Geopolitics, green subsidies fuel Hitachi’s ¥8.5T backlog as supply shifts 12%

Geopolitical tensions (US-China) and export controls raised compliance costs ~4–6% of capex (2024–25) and pushed Hitachi to shift 12% sourcing from China, expanding SE Asia/Japan production; state funds (Japan Society 5.0, EU digital recovery, SE Asia $100B smart-city pipelines) and green subsidies (US IRA $369B energy credits) drive demand for Hitachi Energy, Rail and Lumada, supporting ¥8.5T FY2024 order backlog.

| Metric | Value |

|---|---|

| Sourcing shifted from China | 12% |

| Capex compliance impact (2024–25) | 4–6% |

| Hitachi FY2024 order backlog | ¥8.5T |

| Global clean energy investment (2023) | $1.7T |

| US IRA energy tax credits | $369B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Hitachi across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and industry trends to identify threats and opportunities.

A concise, visually segmented Hitachi PESTLE summary that relieves meeting prep pain by highlighting key external risks and opportunities for quick inclusion in presentations or strategy sessions.

Economic factors

Interest rate fluctuations and capital costs

The global shift in central bank policies through 2025 pushed average OECD policy rates up ~100–150bps versus 2023, raising borrowing costs for large-scale infrastructure; 10‑yr government yields rose to ~3.5–4.0% in major markets, tightening project finance. Higher rates have already prompted reported delays in energy and mobility CAPEX—project pipeline slowdowns of 10–20% in some regions—pressuring Hitachi to optimize its debt mix. Hitachi must actively manage its ¥/USD debt profile, hedges and pricing to protect EBITDA margins (Hitachi reported ¥1.3tn EBITDA in FY2024) amid volatile rates.

Currency exchange rate volatility

As a Japanese multinational, Hitachi’s FY2024 revenue mix—roughly 55% from overseas—makes it highly sensitive to JPY/USD and JPY/EUR moves; JPY weakened ~6% vs USD in 2023-24, bolstering export competitiveness but raising imported energy/raw material costs by similar percentages.

Hitachi reported a ¥50.5bn FX loss in FY2024; the firm uses forward hedges and natural hedges through ¥1.2tn localized overseas capital expenditure to limit consolidated profit volatility.

Inflationary pressure on operational costs

Persistent inflation in labor and material costs—Japan CPI rose 3.1% in 2024 and global steel prices averaged up 12% YoY—forces Hitachi to drive productivity and pricing measures to protect margins.

Hitachi is investing in automation and digital twins across operations; its FY2024 capex rose to ¥620bn to boost efficiency and offset input-cost inflation.

Maintaining profitability hinges on passing costs to customers without ceding share to lower-cost rivals, with Hitachi targeting double-digit productivity gains to do so.

Economic growth trends in emerging markets

Hitachi’s strategy targets Southeast Asia and India where middle-class households are projected to reach 2.8bn by 2030, driving demand for smart life solutions, transit systems, and power infrastructure; ASEAN GDP grew 4.5% in 2023 while India expanded ~7.2% in FY2023–24, supporting project pipelines.

Exposure raises risks from cyclical slowdowns and sovereign or banking liquidity strains—IMF warned of emerging-market debt stress with external financing needs of $2.4tn in 2024–25 for low-income countries.

- Market growth: ASEAN 4.5% (2023), India ~7.2% (FY23–24)

- Demand drivers: rising middle class to 2030 (~2.8bn)

- Revenue opportunity: infrastructure & smart systems

- Risks: economic cycles, EM liquidity needs ~$2.4tn (2024–25)

Global semiconductor and component availability

The global semiconductor shortage trimmed global chip supply by an estimated 10–15% in 2024, keeping prices elevated; Hitachi’s products—from industrial robots to railway signaling—are exposed to this volatility because advanced ICs comprise a growing share of BOM costs.

Hitachi mitigates risk via strategic inventory and multi-year supplier contracts; in FY2024 the company reported inventory days around 85, underscoring emphasis on buffer stocks to protect manufacturing throughput.

- 10–15% global chip shortfall in 2024

- Hitachi FY2024 inventory ≈85 days

- High-tech BOM share rising, increasing vulnerability

- Long-term supplier contracts and buffer inventory are key safeguards

Higher rates squeeze Hitachi's ¥1.3tn EBITDA; JPY weakness aids exports, boosts costs

Higher global rates (10y ~3.5–4.0%) and OECD policy rates +100–150bps to 2025 raise project financing costs, pressuring Hitachi’s ¥1.3tn FY2024 EBITDA and prompting ¥/USD hedge and debt-mix actions; JPY weakened ~6% vs USD (2023–24) aiding exports but adding ~6% input cost pressure.

FY2024: revenue 55% overseas, capex ¥620bn, inventory ~85 days; ASEAN GDP +4.5% (2023), India +7.2% (FY23–24); EM external financing needs ~$2.4tn (2024–25).

| Metric | Value |

|---|---|

| EBITDA FY2024 | ¥1.3tn |

| Capex FY2024 | ¥620bn |

| Inventory days | ~85 |

| Overseas revenue | ~55% |

| JPY vs USD (2023–24) | -6% |

| ASEAN GDP (2023) | +4.5% |

| India GDP (FY23–24) | +7.2% |

| EM financing need (2024–25) | $2.4tn |

Full Version Awaits

Hitachi PESTLE Analysis

The preview shown here is the exact Hitachi PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.