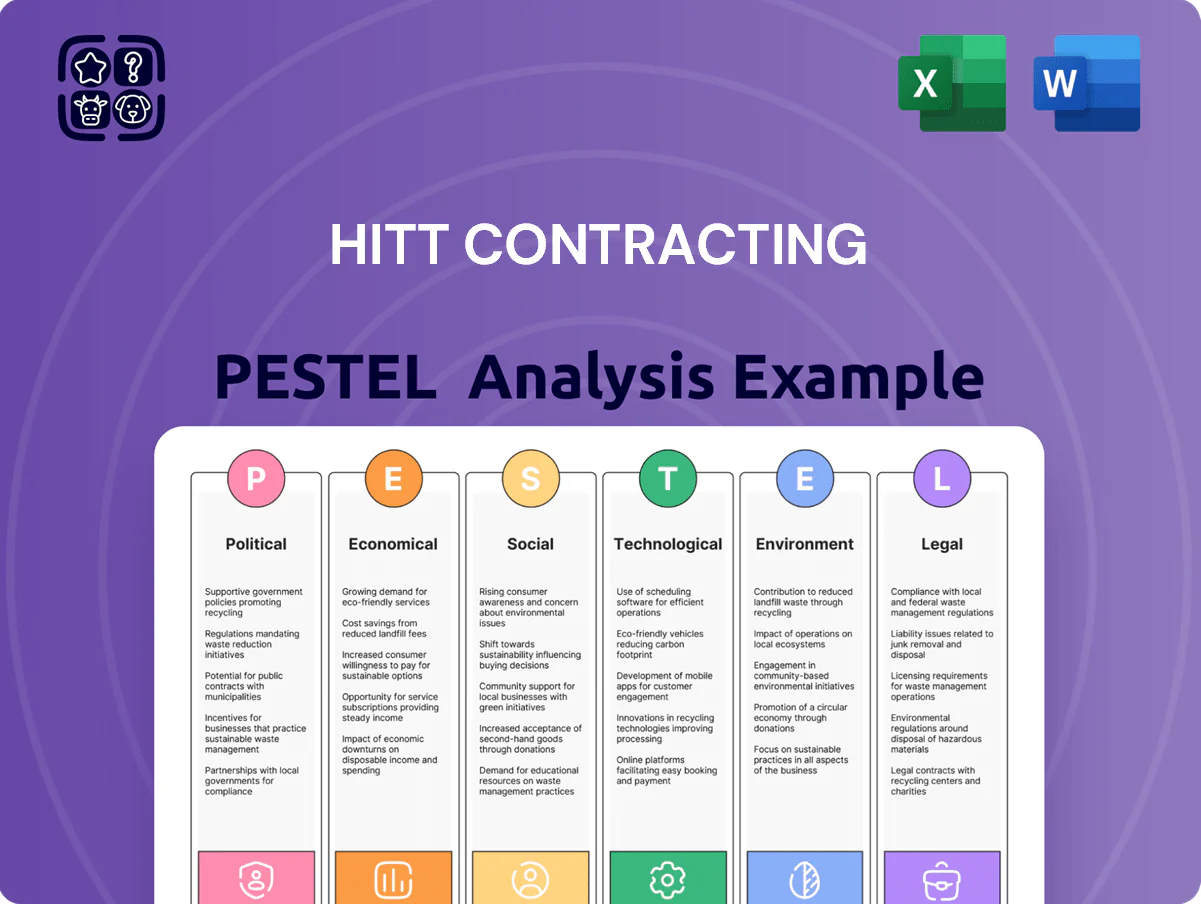

HITT Contracting PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic cycles, and technological advances are reshaping HITT Contracting’s competitive edge—our concise PESTLE highlights key external drivers and risks affecting strategy and margins. Ideal for investors and strategists, the full report delivers deep-dive evidence, actionable recommendations, and editable charts. Purchase now to access the complete analysis and strengthen your decision-making.

Political factors

Federal Infrastructure and Industrial Policy

The continued rollout of the CHIPS and Science Act and the Inflation Reduction Act through 2025 is driving demand for specialized construction, with CHIPS allocating $52.7 billion for semiconductor incentives and IRA-directed clean energy tax credits supporting ~$370 billion in climate investments through 2031; HITT Contracting is positioned to capture projects for fabs and renewable energy facilities. Navigating federal grant compliance and Buy America rules is critical to retain eligibility and avoid clawbacks on projects often exceeding $100M.

Trade Policy and Material Tariffs

Geopolitical tensions and shifting trade alliances in late 2025 have driven US steel prices up ~18% year‑over‑year and aluminum up ~12%, raising material costs for HITT’s commercial builds.

New import tariffs announced in 2025—averaging 7–15% on certain steel/aluminum product lines—force procurement shifts toward domestic suppliers and tariff‑inclusive budgeting.

HITT must continuously monitor US‑China/EU trade relations and freight rates (container rates up ~40% in 2025) to mitigate sudden price spikes and supply disruptions.

Local Zoning and Land Use Regulations

Political shifts in municipal governments across HITT’s national footprint can alter permitting timelines by 20–40%, affecting cash flow and scheduling for the firm’s $1.2B backlog of 2024 projects.

Recent moves toward high-density zoning and urban revitalization in cities like Austin and Denver expand demand in workplace and hospitality segments, with multifamily and commercial permits up 15% year-over-year in 2024.

Proactive engagement with local planning boards cut approval times by an average 30% in HITT pilot projects, proving essential for timely delivery in competitive urban markets.

Government Spending and Budget Stability

Headquartered near Washington, D.C., HITT’s revenue exposure to federal clients makes it vulnerable to budget cycles and the 2018–2025 pattern of 12 short-term continuing resolutions and three shutdowns that have delayed awards and payments; in FY2024 federal discretionary spending was about 1.6 trillion USD, a 2.5% real increase but subject to annual negotiation.

Political gridlock can push contract award timelines out by months, raising working capital needs and DSO for public projects; in 2024 government contractor payment delays averaged 45–60 days in some agencies.

Diversifying into private-sector and state/local work—where HITT had roughly 40% of backlog in 2024—reduces revenue volatility tied to federal budget instability.

- High federal exposure increases cash-flow risk during shutdowns

- FY2024 discretionary budget ~1.6 trillion USD; negotiations still create timing risk

- Average payment delays 45–60 days in 2024 for some agencies

- ~40% backlog from nonfederal clients in 2024 as a diversification hedge

Tax Incentives for Sustainable Development

Legislative focus on carbon reduction has expanded federal and state tax credits—eg, the U.S. 2024 Inflation Reduction Act expansions and 2025 state programs now support up to 30% of qualifying energy-efficiency renovation costs, boosting demand for high-performance interiors and sustainable base buildings.

These incentives push HITT clients toward greener fit-outs; capturing this demand can increase project value by an estimated 5–8% through lifecycle energy savings and tax benefits.

Maximizing credits requires tight integration of HITT’s pre-construction teams with tax consultants to document eligibility, optimize scope, and secure incentives that enhance stakeholder returns.

- Up to 30% tax credits for qualifying renovations (federal/state, 2024–25)

- Potential 5–8% project value uplift via energy savings and incentives

- Requires early pre-construction + tax consultancy alignment

Fed incentives fuel fabs/clean energy but tariffs, materials, permits and payment delays spike project risk

Federal incentive programs (CHIPS $52.7B, IRA ~$370B to 2031) boost demand for fabs/clean energy projects; Buy America/compliance risk on $100M+ contracts; 2024–25 tariffs/up ~7–15% and US steel +18%/aluminum +12% increase material costs; municipal permitting swings (±20–40%) and federal budget volatility (FY2024 discretionary ~$1.6T; avg agency payment delays 45–60 days) raise scheduling and cash‑flow risk.

| Metric | Value |

|---|---|

| CHIPS funding | $52.7B |

| IRA climate spend | ~$370B (to 2031) |

| Steel/aluminum price change (2025) | +18% / +12% |

| Import tariffs (2025) | 7–15% |

| FY2024 discretionary | ~$1.6T |

| Agency payment delays (2024) | 45–60 days |

| Permitting impact | ±20–40% |

What is included in the product

Explores how macro-environmental factors uniquely affect HITT Contracting across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and industry-specific examples to identify threats and opportunities for executives, investors, and strategists.

A concise, PESTLE-segmented summary of HITT Contracting’s external environment that eases meeting prep, supports risk discussions, and can be dropped into slides or shared across teams for quick alignment.

Economic factors

Interest Rate Environment and Capital Costs

By end-2025 Fed rate stabilization—with the federal funds rate forecast near 5.25–5.50%—will cap new commercial construction starts, as CRE lending volumes fell 18% YoY in 2024 and borrowing spreads remain elevated.

Higher capital costs compress developer margins, shifting activity toward renovation and interior fit-outs where ROI timelines are shorter and financing needs are lower.

HITT’s core strength in tenant improvements and interior transformations positions it to gain share; U.S. renovation spending rose 6.4% in 2024, supporting demand for HITT’s services.

Construction Material Price Volatility

Although headline U.S. inflation eased to 3.4% in 2025 YTD, prices for specialized data-center and healthcare components remain elevated—server racks and medical-grade HVAC rose ~12–18% year-on-year through 2024–25. Volatility in copper and semiconductor markets forces HITT to use hedging and early-procurement; forward-buying cut input-cost spikes by ~6–9% on recent projects. Strong vendor partnerships are essential to protect margins amid late-2025 price shocks.

Labor Market Tightness and Wage Growth

The persistent shortage of skilled tradespeople is driving wage growth in construction, with U.S. construction average hourly wages up about 4.8% year-over-year in 2025 and trade-specific premiums reaching 10–15% in major markets; HITT faces higher labor costs and fierce competition for specialists.

Attracting and retaining top talent is an economic imperative for HITT, given industry turnover rates near 25% and longer project delays tied to skill gaps.

Investing in workforce development and internal training—HITT may need to allocate 1–3% of revenue toward upskilling—becomes essential to secure quality, safety, and competitive margins.

Growth of the Data Center Economy

The explosion of AI and cloud computing has made the data center sector a primary economic engine for HITT, with global data center capex estimated at about $200 billion in 2024 and projected to exceed $220 billion in 2025.

Demand for mission-critical facilities remains robust, offering HITT stable revenue less sensitive to GDP cycles—hyperscale vacancy rates stayed below 5% in 2024.

HITT’s reputation in this niche enables it to capture large projects from tech giants, which accounted for roughly 40% of hyperscale spending in 2024, supporting higher-margin, repeatable work.

- Global data center capex ~ $200B (2024), >$220B (2025 est)

- Hyperscale vacancy <5% (2024)

- Tech giants ~40% of hyperscale spend (2024)

Corporate Real Estate Consolidation Trends

Economic shifts to hybrid work cut U.S. office occupancy ~30% vs pre‑pandemic levels, prompting companies to downsize footprints but spend more per sq ft on quality; CBRE reports flight‑to‑quality drove Class A leasing gains of 12% in 2024, favoring high‑end fit‑outs.

For HITT, this increases demand for premium interior services—commercial interiors revenue in 2024 rose industrywide ~8%—making adaptation to consolidation critical for sustaining workplace-sector growth.

- Office occupancy down ~30% (U.S.)

- Class A leasing +12% (2024, CBRE)

- Industry interiors revenue +8% (2024)

- Opportunity: higher spend per sq ft on destination offices

Higher Fed rates pinch CRE starts; data‑center boom and renovations fuel HITT’s premium pipeline

Persistent 5.25–5.50% Fed rates and tighter CRE lending cut new starts; renovation/fit-out demand rose as developers favor shorter-ROI projects. Input-price volatility (server/medical HVAC +12–18% through 2024–25) and labor wage inflation (~4.8% avg; trade premiums 10–15%) squeeze margins, driving hedging, forward-buying, and 1–3% revenue upskilling spend. Data‑center capex ~$200B (2024)→>$220B (2025) and office flight‑to‑quality boost HITT’s premium interiors pipeline.

| Metric | Value |

|---|---|

| Fed funds (end‑2025 est) | 5.25–5.50% |

| Data‑center capex | $200B (2024) → >$220B (2025 est) |

| Server/HVAC price change | +12–18% (2024–25) |

| Construction wages | +4.8% YoY (2025); trade premiums 10–15% |

Preview the Actual Deliverable

HITT Contracting PESTLE Analysis

The preview shown here is the exact HITT Contracting PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic cycles, and technological advances are reshaping HITT Contracting’s competitive edge—our concise PESTLE highlights key external drivers and risks affecting strategy and margins. Ideal for investors and strategists, the full report delivers deep-dive evidence, actionable recommendations, and editable charts. Purchase now to access the complete analysis and strengthen your decision-making.

Political factors

Federal Infrastructure and Industrial Policy

The continued rollout of the CHIPS and Science Act and the Inflation Reduction Act through 2025 is driving demand for specialized construction, with CHIPS allocating $52.7 billion for semiconductor incentives and IRA-directed clean energy tax credits supporting ~$370 billion in climate investments through 2031; HITT Contracting is positioned to capture projects for fabs and renewable energy facilities. Navigating federal grant compliance and Buy America rules is critical to retain eligibility and avoid clawbacks on projects often exceeding $100M.

Trade Policy and Material Tariffs

Geopolitical tensions and shifting trade alliances in late 2025 have driven US steel prices up ~18% year‑over‑year and aluminum up ~12%, raising material costs for HITT’s commercial builds.

New import tariffs announced in 2025—averaging 7–15% on certain steel/aluminum product lines—force procurement shifts toward domestic suppliers and tariff‑inclusive budgeting.

HITT must continuously monitor US‑China/EU trade relations and freight rates (container rates up ~40% in 2025) to mitigate sudden price spikes and supply disruptions.

Local Zoning and Land Use Regulations

Political shifts in municipal governments across HITT’s national footprint can alter permitting timelines by 20–40%, affecting cash flow and scheduling for the firm’s $1.2B backlog of 2024 projects.

Recent moves toward high-density zoning and urban revitalization in cities like Austin and Denver expand demand in workplace and hospitality segments, with multifamily and commercial permits up 15% year-over-year in 2024.

Proactive engagement with local planning boards cut approval times by an average 30% in HITT pilot projects, proving essential for timely delivery in competitive urban markets.

Government Spending and Budget Stability

Headquartered near Washington, D.C., HITT’s revenue exposure to federal clients makes it vulnerable to budget cycles and the 2018–2025 pattern of 12 short-term continuing resolutions and three shutdowns that have delayed awards and payments; in FY2024 federal discretionary spending was about 1.6 trillion USD, a 2.5% real increase but subject to annual negotiation.

Political gridlock can push contract award timelines out by months, raising working capital needs and DSO for public projects; in 2024 government contractor payment delays averaged 45–60 days in some agencies.

Diversifying into private-sector and state/local work—where HITT had roughly 40% of backlog in 2024—reduces revenue volatility tied to federal budget instability.

- High federal exposure increases cash-flow risk during shutdowns

- FY2024 discretionary budget ~1.6 trillion USD; negotiations still create timing risk

- Average payment delays 45–60 days in 2024 for some agencies

- ~40% backlog from nonfederal clients in 2024 as a diversification hedge

Tax Incentives for Sustainable Development

Legislative focus on carbon reduction has expanded federal and state tax credits—eg, the U.S. 2024 Inflation Reduction Act expansions and 2025 state programs now support up to 30% of qualifying energy-efficiency renovation costs, boosting demand for high-performance interiors and sustainable base buildings.

These incentives push HITT clients toward greener fit-outs; capturing this demand can increase project value by an estimated 5–8% through lifecycle energy savings and tax benefits.

Maximizing credits requires tight integration of HITT’s pre-construction teams with tax consultants to document eligibility, optimize scope, and secure incentives that enhance stakeholder returns.

- Up to 30% tax credits for qualifying renovations (federal/state, 2024–25)

- Potential 5–8% project value uplift via energy savings and incentives

- Requires early pre-construction + tax consultancy alignment

Fed incentives fuel fabs/clean energy but tariffs, materials, permits and payment delays spike project risk

Federal incentive programs (CHIPS $52.7B, IRA ~$370B to 2031) boost demand for fabs/clean energy projects; Buy America/compliance risk on $100M+ contracts; 2024–25 tariffs/up ~7–15% and US steel +18%/aluminum +12% increase material costs; municipal permitting swings (±20–40%) and federal budget volatility (FY2024 discretionary ~$1.6T; avg agency payment delays 45–60 days) raise scheduling and cash‑flow risk.

| Metric | Value |

|---|---|

| CHIPS funding | $52.7B |

| IRA climate spend | ~$370B (to 2031) |

| Steel/aluminum price change (2025) | +18% / +12% |

| Import tariffs (2025) | 7–15% |

| FY2024 discretionary | ~$1.6T |

| Agency payment delays (2024) | 45–60 days |

| Permitting impact | ±20–40% |

What is included in the product

Explores how macro-environmental factors uniquely affect HITT Contracting across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and industry-specific examples to identify threats and opportunities for executives, investors, and strategists.

A concise, PESTLE-segmented summary of HITT Contracting’s external environment that eases meeting prep, supports risk discussions, and can be dropped into slides or shared across teams for quick alignment.

Economic factors

Interest Rate Environment and Capital Costs

By end-2025 Fed rate stabilization—with the federal funds rate forecast near 5.25–5.50%—will cap new commercial construction starts, as CRE lending volumes fell 18% YoY in 2024 and borrowing spreads remain elevated.

Higher capital costs compress developer margins, shifting activity toward renovation and interior fit-outs where ROI timelines are shorter and financing needs are lower.

HITT’s core strength in tenant improvements and interior transformations positions it to gain share; U.S. renovation spending rose 6.4% in 2024, supporting demand for HITT’s services.

Construction Material Price Volatility

Although headline U.S. inflation eased to 3.4% in 2025 YTD, prices for specialized data-center and healthcare components remain elevated—server racks and medical-grade HVAC rose ~12–18% year-on-year through 2024–25. Volatility in copper and semiconductor markets forces HITT to use hedging and early-procurement; forward-buying cut input-cost spikes by ~6–9% on recent projects. Strong vendor partnerships are essential to protect margins amid late-2025 price shocks.

Labor Market Tightness and Wage Growth

The persistent shortage of skilled tradespeople is driving wage growth in construction, with U.S. construction average hourly wages up about 4.8% year-over-year in 2025 and trade-specific premiums reaching 10–15% in major markets; HITT faces higher labor costs and fierce competition for specialists.

Attracting and retaining top talent is an economic imperative for HITT, given industry turnover rates near 25% and longer project delays tied to skill gaps.

Investing in workforce development and internal training—HITT may need to allocate 1–3% of revenue toward upskilling—becomes essential to secure quality, safety, and competitive margins.

Growth of the Data Center Economy

The explosion of AI and cloud computing has made the data center sector a primary economic engine for HITT, with global data center capex estimated at about $200 billion in 2024 and projected to exceed $220 billion in 2025.

Demand for mission-critical facilities remains robust, offering HITT stable revenue less sensitive to GDP cycles—hyperscale vacancy rates stayed below 5% in 2024.

HITT’s reputation in this niche enables it to capture large projects from tech giants, which accounted for roughly 40% of hyperscale spending in 2024, supporting higher-margin, repeatable work.

- Global data center capex ~ $200B (2024), >$220B (2025 est)

- Hyperscale vacancy <5% (2024)

- Tech giants ~40% of hyperscale spend (2024)

Corporate Real Estate Consolidation Trends

Economic shifts to hybrid work cut U.S. office occupancy ~30% vs pre‑pandemic levels, prompting companies to downsize footprints but spend more per sq ft on quality; CBRE reports flight‑to‑quality drove Class A leasing gains of 12% in 2024, favoring high‑end fit‑outs.

For HITT, this increases demand for premium interior services—commercial interiors revenue in 2024 rose industrywide ~8%—making adaptation to consolidation critical for sustaining workplace-sector growth.

- Office occupancy down ~30% (U.S.)

- Class A leasing +12% (2024, CBRE)

- Industry interiors revenue +8% (2024)

- Opportunity: higher spend per sq ft on destination offices

Higher Fed rates pinch CRE starts; data‑center boom and renovations fuel HITT’s premium pipeline

Persistent 5.25–5.50% Fed rates and tighter CRE lending cut new starts; renovation/fit-out demand rose as developers favor shorter-ROI projects. Input-price volatility (server/medical HVAC +12–18% through 2024–25) and labor wage inflation (~4.8% avg; trade premiums 10–15%) squeeze margins, driving hedging, forward-buying, and 1–3% revenue upskilling spend. Data‑center capex ~$200B (2024)→>$220B (2025) and office flight‑to‑quality boost HITT’s premium interiors pipeline.

| Metric | Value |

|---|---|

| Fed funds (end‑2025 est) | 5.25–5.50% |

| Data‑center capex | $200B (2024) → >$220B (2025 est) |

| Server/HVAC price change | +12–18% (2024–25) |

| Construction wages | +4.8% YoY (2025); trade premiums 10–15% |

Preview the Actual Deliverable

HITT Contracting PESTLE Analysis

The preview shown here is the exact HITT Contracting PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.