China Oil And Gas Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

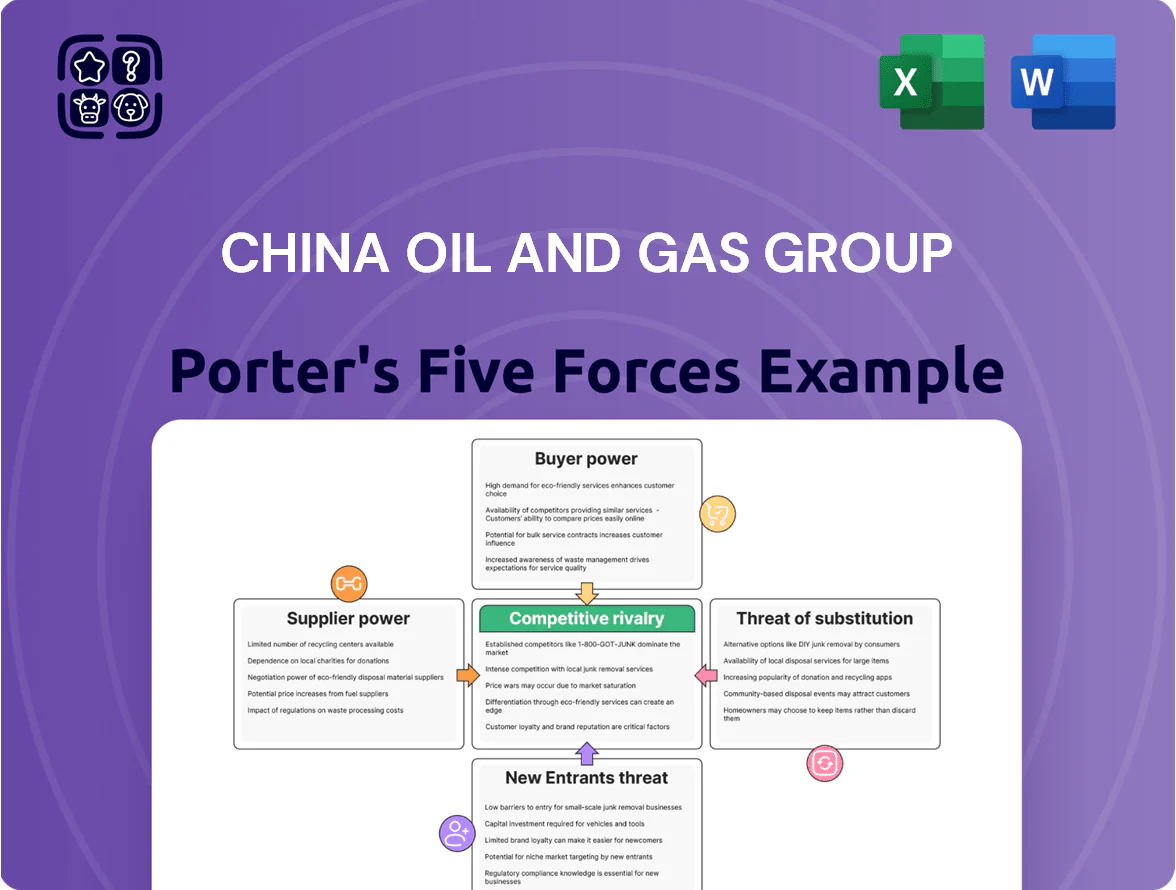

China Oil And Gas Group faces intense supplier leverage for upstream inputs, moderate buyer power in commodity-driven markets, and significant rivalry from state-backed incumbents and private challengers.

Barriers to entry are mixed—high capital intensity deters newcomers, but policy shifts and joint ventures open avenues for competitors; substitutes and regulatory risk add pressure.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China Oil And Gas Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of State Owned Enterprises

PetroChina and Sinopec, state-owned giants controlling ~70–80% of China’s upstream gas production and >75% of trunk pipeline capacity in 2024, dominate supply, leaving China Oil and Gas Group little leverage on price.

Their control of midstream transmission and wholesale procurement lets them set tolls and contract terms; spot volumes for independent buyers fell to ~12% of market share in 2024, shrinking negotiation room.

Specialized Technology and Equipment Costs

Extraction of coalbed methane and shale gas needs niche drilling rigs and frac fleets; worldwide there were about 7 major hydraulic fracturing service providers in 2024, concentrating supply and raising bargaining power for China Oil And Gas Group.

Advanced horizontal-drilling and completion services cost roughly $8–12 million per well in China for shale plays in 2024, so high capex and few vendors give suppliers pricing leverage and influence over project schedules.

Regulatory Control over Resource Allocation

The Chinese government functions as a meta-supplier by controlling exploration licenses and production quotas—Beijing issued 1,024 onshore and offshore exploration permits in 2024 and set crude production guidance of 199 million tonnes in 2025, effectively deciding which firms access blocks; this regulatory gatekeeping makes the state the ultimate arbiter of supply and limits private or smaller integrated firms from bypassing traditional supply chains.

Global Commodity Price Volatility

- Steel price surge: +28% (2021–22)

- Avg LNG spot: ~$30/MMBtu (2022) vs $6 pre-2021

- Imported equipment tied to global indices

- Limits company control over operating costs

Limited Pipeline Infrastructure Access

Access to China’s national pipeline network is essential to move gas from upstream sites to markets; PipeChina’s 2020 reform aimed to open access, but around 60–70% of trunk capacity remains effectively controlled by a few state-linked operators, creating chokepoints.

Those operators can influence timing and volume, raising delivery risk and short-term price exposure for China Oil And Gas Group; in 2024 pipeline throughput constraints contributed to regional gas rationing episodes in Q1.

- National pipeline access required for market delivery

- PipeChina liberalized policy in 2020, but capacity concentrated

- 60–70% trunk capacity tied to few operators

- 2024 Q1 throughput limits caused regional rationing

Suppliers dominate China oil: PetroChina/Sinopec control supply, costs squeeze margins

Suppliers hold strong power: PetroChina/Sinopec control ~70–80% upstream and >75% trunk pipeline (2024), spot sales ~12%, few frack providers (~7 global majors, 2024) and $8–12m/well completions raise capex dependence; govt issues 1,024 exploration permits (2024) and set 199Mt crude guidance (2025), while steel/LNG price swings (steel +28% 2021–22; LNG ~$30/MMBtu 2022) squeeze margins.

| Metric | Value |

|---|---|

| Upstream share | 70–80% (2024) |

| Trunk pipeline | >75% (2024) |

| Spot market | ~12% (2024) |

| Frack providers | ~7 majors (2024) |

| Well cost | $8–12m (2024) |

| Exploration permits | 1,024 (2024) |

| Crude guidance | 199 Mt (2025) |

| Steel price rise | +28% (2021–22) |

| LNG spot | ~$30/MMBtu (2022) |

What is included in the product

Tailored Porter’s Five Forces analysis for China Oil And Gas Group, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape its pricing, profitability, and strategic positioning.

A concise Porter’s Five Forces snapshot for China Oil And Gas Group—ideal for rapid strategic decisions and board briefings, with clear force ratings and remediation actions.

Customers Bargaining Power

Concentration of Industrial Users

A large share of China Oil And Gas Group’s gas sales go to industrial plants and power generators; in 2024 China’s industrial sector consumed about 48% of national gas demand (2024 NBS), so these high-volume buyers can demand volume discounts and long-term lower tariffs.

Government Mandated Pricing for Residential Segments

In China’s residential downstream, provincial governments cap gas tariffs—Beijing, Shanghai, and Guangdong kept city-gate prices within a 5–10% band in 2024—forcing China Oil And Gas Group to absorb spot LNG cost spikes (spot averaged $14/MMBtu in 2024 vs $8/MMBtu in 2020) to avoid social unrest, so end-users gain indirect bargaining power via regulators and squeeze company margins.

Price Sensitivity of Commercial Clients

Commercial clients like hotels and restaurants often spend 5–15% of operating costs on energy; a 2024 IEA/World Bank survey found 38% would switch fuels if gas rose 10% vs competing electricity/LPG. If piped natural gas becomes pricier, customers cut use or buy efficient boilers and heat pumps. That elasticity forces China Oil And Gas Group to keep prices competitive and offer contracts or efficiency incentives to limit churn.

Impact of Economic Deceleration

By end-2025, a 3.2% year-on-year drop in China industrial output would cut corporate fuel demand and boost buyer leverage, letting large industrial clients press for price discounts and longer payment terms.

During slower growth phases, top-50 industrial customers can trim volumes by 12–18%, forcing China Oil And Gas Group to offer flexible contracts or lose share.

Build diversified, flexible portfolios and shorter contract tenors to reduce revenue volatility and limit buyer power.

- 3.2% projected industrial output drop by end-2025

- 12–18% potential volume cuts from major industrial buyers

- Shorter tenors and diversified customers reduce buyer leverage

Growth of Third Party Access and Choice

Market reforms since 2017 let large industrial buyers in China source gas directly from wholesalers; by 2024 roughly 28% of gas sales by volume occurred via spot and direct contracts, up from ~12% in 2018, weakening local distributor lock-in.

Greater price transparency—national trading hubs and published city-gate prices—makes switching easier; procurement teams can compare offers across suppliers, raising buyer bargaining power and pressuring margins for China Oil And Gas Group.

- Direct sourcing share ~28% (2024)

- Spot market growth CAGR ~15% (2018–24)

- Local distributor monopoly erosion—price spreads narrowed ~40% (2019–24)

Industrial buyers wield leverage as spot LNG doubles to $14, direct sourcing rises to 28%

Large industrial buyers (48% of 2024 gas demand) and provincial tariff caps give customers strong leverage; spot LNG averaged $14/MMBtu in 2024 vs $8/MMBtu in 2020, raising margin pressure. Direct sourcing rose to ~28% of volumes by 2024, spot market CAGR ~15% (2018–24), and top-50 clients can cut volumes 12–18% in slowdowns—shorter tenors and customer diversification reduce buyer power.

| Metric | Value |

|---|---|

| Industrial share (2024) | 48% |

| Spot LNG price (2024) | $14/MMBtu |

| Direct sourcing (2024) | 28% |

| Spot market CAGR (2018–24) | ~15% |

| Top-50 volume cut risk | 12–18% |

What You See Is What You Get

China Oil And Gas Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for China Oil And Gas Group you'll receive—no placeholders or mockups, fully formatted and ready for use.

You're viewing the final document; once purchased, you’ll get immediate access to this same file containing the complete competitive assessment and strategic insights.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

China Oil And Gas Group faces intense supplier leverage for upstream inputs, moderate buyer power in commodity-driven markets, and significant rivalry from state-backed incumbents and private challengers.

Barriers to entry are mixed—high capital intensity deters newcomers, but policy shifts and joint ventures open avenues for competitors; substitutes and regulatory risk add pressure.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China Oil And Gas Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of State Owned Enterprises

PetroChina and Sinopec, state-owned giants controlling ~70–80% of China’s upstream gas production and >75% of trunk pipeline capacity in 2024, dominate supply, leaving China Oil and Gas Group little leverage on price.

Their control of midstream transmission and wholesale procurement lets them set tolls and contract terms; spot volumes for independent buyers fell to ~12% of market share in 2024, shrinking negotiation room.

Specialized Technology and Equipment Costs

Extraction of coalbed methane and shale gas needs niche drilling rigs and frac fleets; worldwide there were about 7 major hydraulic fracturing service providers in 2024, concentrating supply and raising bargaining power for China Oil And Gas Group.

Advanced horizontal-drilling and completion services cost roughly $8–12 million per well in China for shale plays in 2024, so high capex and few vendors give suppliers pricing leverage and influence over project schedules.

Regulatory Control over Resource Allocation

The Chinese government functions as a meta-supplier by controlling exploration licenses and production quotas—Beijing issued 1,024 onshore and offshore exploration permits in 2024 and set crude production guidance of 199 million tonnes in 2025, effectively deciding which firms access blocks; this regulatory gatekeeping makes the state the ultimate arbiter of supply and limits private or smaller integrated firms from bypassing traditional supply chains.

Global Commodity Price Volatility

- Steel price surge: +28% (2021–22)

- Avg LNG spot: ~$30/MMBtu (2022) vs $6 pre-2021

- Imported equipment tied to global indices

- Limits company control over operating costs

Limited Pipeline Infrastructure Access

Access to China’s national pipeline network is essential to move gas from upstream sites to markets; PipeChina’s 2020 reform aimed to open access, but around 60–70% of trunk capacity remains effectively controlled by a few state-linked operators, creating chokepoints.

Those operators can influence timing and volume, raising delivery risk and short-term price exposure for China Oil And Gas Group; in 2024 pipeline throughput constraints contributed to regional gas rationing episodes in Q1.

- National pipeline access required for market delivery

- PipeChina liberalized policy in 2020, but capacity concentrated

- 60–70% trunk capacity tied to few operators

- 2024 Q1 throughput limits caused regional rationing

Suppliers dominate China oil: PetroChina/Sinopec control supply, costs squeeze margins

Suppliers hold strong power: PetroChina/Sinopec control ~70–80% upstream and >75% trunk pipeline (2024), spot sales ~12%, few frack providers (~7 global majors, 2024) and $8–12m/well completions raise capex dependence; govt issues 1,024 exploration permits (2024) and set 199Mt crude guidance (2025), while steel/LNG price swings (steel +28% 2021–22; LNG ~$30/MMBtu 2022) squeeze margins.

| Metric | Value |

|---|---|

| Upstream share | 70–80% (2024) |

| Trunk pipeline | >75% (2024) |

| Spot market | ~12% (2024) |

| Frack providers | ~7 majors (2024) |

| Well cost | $8–12m (2024) |

| Exploration permits | 1,024 (2024) |

| Crude guidance | 199 Mt (2025) |

| Steel price rise | +28% (2021–22) |

| LNG spot | ~$30/MMBtu (2022) |

What is included in the product

Tailored Porter’s Five Forces analysis for China Oil And Gas Group, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape its pricing, profitability, and strategic positioning.

A concise Porter’s Five Forces snapshot for China Oil And Gas Group—ideal for rapid strategic decisions and board briefings, with clear force ratings and remediation actions.

Customers Bargaining Power

Concentration of Industrial Users

A large share of China Oil And Gas Group’s gas sales go to industrial plants and power generators; in 2024 China’s industrial sector consumed about 48% of national gas demand (2024 NBS), so these high-volume buyers can demand volume discounts and long-term lower tariffs.

Government Mandated Pricing for Residential Segments

In China’s residential downstream, provincial governments cap gas tariffs—Beijing, Shanghai, and Guangdong kept city-gate prices within a 5–10% band in 2024—forcing China Oil And Gas Group to absorb spot LNG cost spikes (spot averaged $14/MMBtu in 2024 vs $8/MMBtu in 2020) to avoid social unrest, so end-users gain indirect bargaining power via regulators and squeeze company margins.

Price Sensitivity of Commercial Clients

Commercial clients like hotels and restaurants often spend 5–15% of operating costs on energy; a 2024 IEA/World Bank survey found 38% would switch fuels if gas rose 10% vs competing electricity/LPG. If piped natural gas becomes pricier, customers cut use or buy efficient boilers and heat pumps. That elasticity forces China Oil And Gas Group to keep prices competitive and offer contracts or efficiency incentives to limit churn.

Impact of Economic Deceleration

By end-2025, a 3.2% year-on-year drop in China industrial output would cut corporate fuel demand and boost buyer leverage, letting large industrial clients press for price discounts and longer payment terms.

During slower growth phases, top-50 industrial customers can trim volumes by 12–18%, forcing China Oil And Gas Group to offer flexible contracts or lose share.

Build diversified, flexible portfolios and shorter contract tenors to reduce revenue volatility and limit buyer power.

- 3.2% projected industrial output drop by end-2025

- 12–18% potential volume cuts from major industrial buyers

- Shorter tenors and diversified customers reduce buyer leverage

Growth of Third Party Access and Choice

Market reforms since 2017 let large industrial buyers in China source gas directly from wholesalers; by 2024 roughly 28% of gas sales by volume occurred via spot and direct contracts, up from ~12% in 2018, weakening local distributor lock-in.

Greater price transparency—national trading hubs and published city-gate prices—makes switching easier; procurement teams can compare offers across suppliers, raising buyer bargaining power and pressuring margins for China Oil And Gas Group.

- Direct sourcing share ~28% (2024)

- Spot market growth CAGR ~15% (2018–24)

- Local distributor monopoly erosion—price spreads narrowed ~40% (2019–24)

Industrial buyers wield leverage as spot LNG doubles to $14, direct sourcing rises to 28%

Large industrial buyers (48% of 2024 gas demand) and provincial tariff caps give customers strong leverage; spot LNG averaged $14/MMBtu in 2024 vs $8/MMBtu in 2020, raising margin pressure. Direct sourcing rose to ~28% of volumes by 2024, spot market CAGR ~15% (2018–24), and top-50 clients can cut volumes 12–18% in slowdowns—shorter tenors and customer diversification reduce buyer power.

| Metric | Value |

|---|---|

| Industrial share (2024) | 48% |

| Spot LNG price (2024) | $14/MMBtu |

| Direct sourcing (2024) | 28% |

| Spot market CAGR (2018–24) | ~15% |

| Top-50 volume cut risk | 12–18% |

What You See Is What You Get

China Oil And Gas Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for China Oil And Gas Group you'll receive—no placeholders or mockups, fully formatted and ready for use.

You're viewing the final document; once purchased, you’ll get immediate access to this same file containing the complete competitive assessment and strategic insights.