HK Electric Investments Porter's Five Forces Analysis

From Overview to Strategy Blueprint

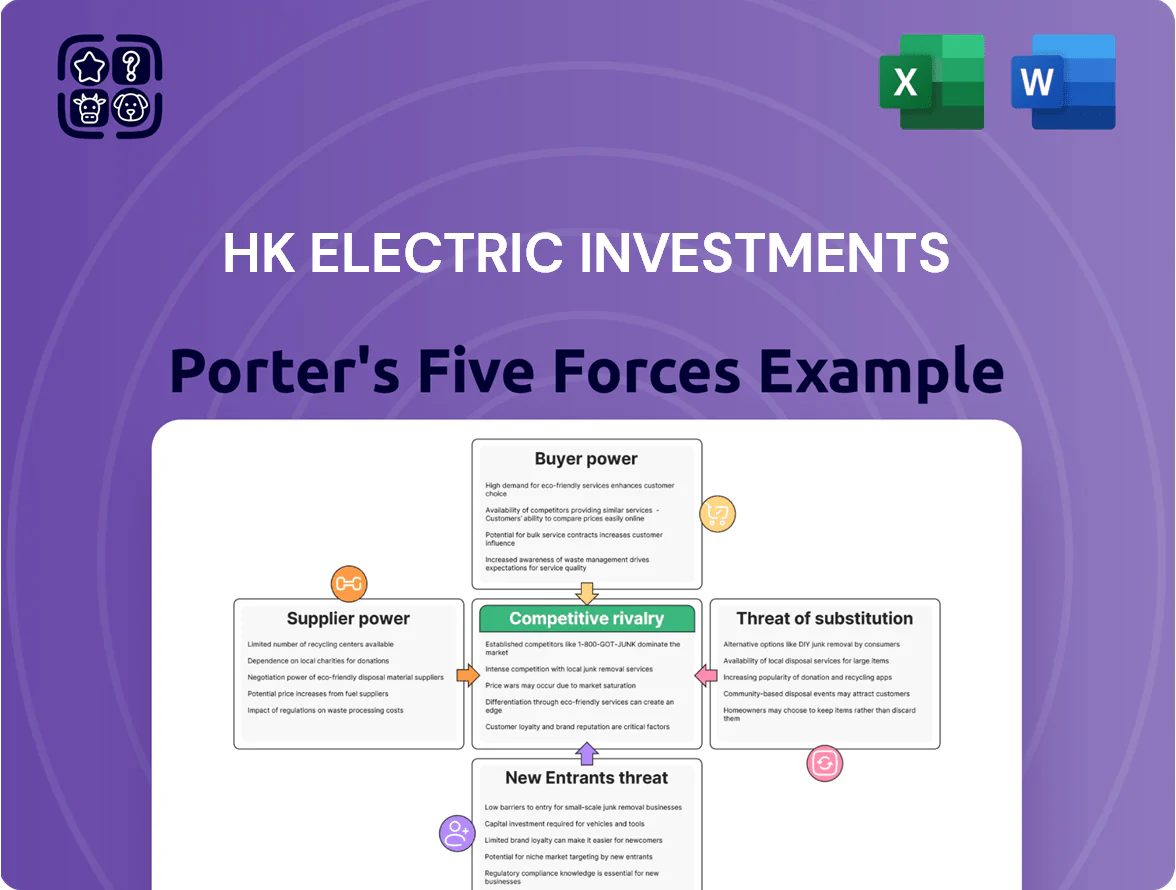

HK Electric Investments faces moderate supplier power and regulatory scrutiny, while customer demand and potential substitutes shape pricing flexibility; competitive rivalry hinges on grid modernization and renewable integration investments.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore HK Electric Investments’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in Global Fuel Markets

HK Electric depends on imported natural gas and coal for Lamma Island plants, sourcing ~85% of fuel needs externally, so it cannot control global spot prices that set base input costs.

In late 2025, Brent-linked gas and coal spikes pushed fuel procurement costs up ~22% year-on-year, raising generation fuel expense and squeezing margins under regulated tariffs.

Limited Natural Gas Infrastructure

HK Electric relies on a few subsea pipelines and a 2024-upgraded offshore LNG terminal, limiting viable gas suppliers to a small set of regional producers and pipeline operators; 2023 import data show >85% of its gas flows via these assets.

Specialized Equipment Procurement

Maintenance and upgrades of HK Electric’s grid and generation units depend on a small set of global firms supplying advanced turbines and smart-grid hardware, giving suppliers strong leverage; in 2024 HK Electric spent ~HKD 3.2bn on capital equipment, much of it vendor-specific.

Technical complexity and certification cycles (often 18–36 months) limit substitutes, so suppliers can demand premium pricing and longer payment terms, squeezing margins on new projects.

HK Electric must keep multi-year, high-value contracts and strategic partnerships—about 60% of recent CAPEX tied to three key vendors—to secure spare parts and firmware support.

Decarbonization and Green Tech Suppliers

- 2024 green capex: HKD 6.1bn (up 35%)

- 2025 large-scale DAC/CCUS vendors: ~8–12 global firms

- Supplier leverage: patents, proprietary processes, long lead times

Long-term Contractual Obligations

- Typical contract length: 10–15 years

- 2024 spot LNG ~40% below 2022 peaks

- Locked volumes limit spot market upside

- Suppliers gain predictable revenue, higher leverage

Supplier leverage squeezes HK Electric: high fuel imports, rising costs, vendor concentration

Suppliers hold strong leverage: HK Electric imports ~85% fuel, signs 10–15y LNG/coal contracts, faced ~22% fuel cost rise in late 2025, and spent HKD 6.1bn on green capex in 2024; vendor concentration (60% CAPEX with 3 vendors, 8–12 global DAC/CCUS firms) raises switching costs and pricing power, pressuring margins.

| Metric | Value |

|---|---|

| Fuel imports | ~85% |

| 2025 fuel cost rise | ~22% |

| 2024 green capex | HKD 6.1bn |

| Key vendors share | ~60% |

| DAC/CCUS firms | 8–12 |

What is included in the product

Tailored exclusively for HK Electric Investments, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats shaping its pricing, profitability, and strategic positioning.

One-sheet Porter's Five Forces for HK Electric Investments—instantly spot regulatory, supplier, and competitive pressures with a clean radar chart and customizable inputs for board-ready slides.

Customers Bargaining Power

Regulated Tariff Mechanisms

The Scheme of Control Agreement with the Hong Kong government caps HK Electric’s allowed return and sets tariff formulas, effectively substituting direct customer bargaining with regulatory oversight; under the current SoC (renewed 2020), allowed return is about 8.99% pre-tax on capital, keeping residential tariffs at HKD 1.244/kWh in 2024 and limiting price volatility.

Geographic Monopoly Constraints

Customers on Hong Kong Island and Lamma Island have no alternative electricity supplier, so buyer power is low and switching is effectively impossible; HK Electric serves about 580,000 accounts and 2.1 million people as of 2024.

That geographic monopoly gives the company pricing control, but public and political scrutiny constrains tariffs—HK Electric’s average tariff was HK$1.305/kWh in 2024 and proposed rises face regulatory pushback.

Regulatory oversight by the Hong Kong Government and the Electricity Ordinance means rate increases must balance company returns and public affordability, limiting exploitative pricing despite captive demand.

Public and Political Sensitivity

Electricity is essential, so any tariff move is politically explosive in Hong Kong; a proposed 2024 tariff rise of 3.5% sparked protests and hearings in the Legislative Council, showing sensitivity to price changes.

Organized consumer groups and >10 LegCo members regularly press HK Electric to justify hikes, linking affordability to social stability and urging audits and subsidy options.

Consequently, HK Electric must publish detailed cost-pass-through analyses and keep ROE targets transparent—its 2023 allowed return on equity was ~8.5%—to gain public and political buy-in.

Commercial Sector Energy Efficiency

Governmental Influence on Strategy

The Hong Kong government functions as the de facto customer representative in Scheme of Control reviews, using its regulatory role to push HK Electric Investments toward higher service standards and green investments without guaranteeing higher returns.

In the 2024 review, regulators asked for accelerated decarbonisation targets aligned with the 2050 net-zero goal, potentially adding HK$5–8 billion capex by 2030, while tariff allowances remained tightly constrained.

This institutional oversight concentrates citizen bargaining power into policy demands, increasing non-price obligations and compressing allowable ROE pressures on the company.

- Government negotiates on behalf of citizens

- 2024 review implied HK$5–8bn extra capex by 2030

- Higher service/green mandates with limited profit relief

HK Electric: Monopoly reach vs regulatory caps, demand cuts and HK$5–8bn decarb cost

Customers have low direct bargaining power due to HK Electric’s geographic monopoly (580,000 accounts, 2.1M people in 2024), but regulatory caps (SoC allowed return ~8.99% pre-tax; avg tariff HK$1.305/kWh in 2024) plus political pressure, large C&I demand reductions (smart BMS cuts 8–12%) and 2024 decarbonisation CAPEX needs (HK$5–8bn by 2030) constrain pricing power.

| Metric | Value (2024) |

|---|---|

| Accounts served | 580,000 |

| Population served | 2.1M |

| Avg tariff | HK$1.305/kWh |

| Allowed return (pre-tax) | ~8.99% |

| C&I demand cut (smart BMS) | 8–12% |

| Decarb CAPEX to 2030 | HK$5–8bn |

Preview Before You Purchase

HK Electric Investments Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of HK Electric Investments you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

HK Electric Investments faces moderate supplier power and regulatory scrutiny, while customer demand and potential substitutes shape pricing flexibility; competitive rivalry hinges on grid modernization and renewable integration investments.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore HK Electric Investments’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in Global Fuel Markets

HK Electric depends on imported natural gas and coal for Lamma Island plants, sourcing ~85% of fuel needs externally, so it cannot control global spot prices that set base input costs.

In late 2025, Brent-linked gas and coal spikes pushed fuel procurement costs up ~22% year-on-year, raising generation fuel expense and squeezing margins under regulated tariffs.

Limited Natural Gas Infrastructure

HK Electric relies on a few subsea pipelines and a 2024-upgraded offshore LNG terminal, limiting viable gas suppliers to a small set of regional producers and pipeline operators; 2023 import data show >85% of its gas flows via these assets.

Specialized Equipment Procurement

Maintenance and upgrades of HK Electric’s grid and generation units depend on a small set of global firms supplying advanced turbines and smart-grid hardware, giving suppliers strong leverage; in 2024 HK Electric spent ~HKD 3.2bn on capital equipment, much of it vendor-specific.

Technical complexity and certification cycles (often 18–36 months) limit substitutes, so suppliers can demand premium pricing and longer payment terms, squeezing margins on new projects.

HK Electric must keep multi-year, high-value contracts and strategic partnerships—about 60% of recent CAPEX tied to three key vendors—to secure spare parts and firmware support.

Decarbonization and Green Tech Suppliers

- 2024 green capex: HKD 6.1bn (up 35%)

- 2025 large-scale DAC/CCUS vendors: ~8–12 global firms

- Supplier leverage: patents, proprietary processes, long lead times

Long-term Contractual Obligations

- Typical contract length: 10–15 years

- 2024 spot LNG ~40% below 2022 peaks

- Locked volumes limit spot market upside

- Suppliers gain predictable revenue, higher leverage

Supplier leverage squeezes HK Electric: high fuel imports, rising costs, vendor concentration

Suppliers hold strong leverage: HK Electric imports ~85% fuel, signs 10–15y LNG/coal contracts, faced ~22% fuel cost rise in late 2025, and spent HKD 6.1bn on green capex in 2024; vendor concentration (60% CAPEX with 3 vendors, 8–12 global DAC/CCUS firms) raises switching costs and pricing power, pressuring margins.

| Metric | Value |

|---|---|

| Fuel imports | ~85% |

| 2025 fuel cost rise | ~22% |

| 2024 green capex | HKD 6.1bn |

| Key vendors share | ~60% |

| DAC/CCUS firms | 8–12 |

What is included in the product

Tailored exclusively for HK Electric Investments, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats shaping its pricing, profitability, and strategic positioning.

One-sheet Porter's Five Forces for HK Electric Investments—instantly spot regulatory, supplier, and competitive pressures with a clean radar chart and customizable inputs for board-ready slides.

Customers Bargaining Power

Regulated Tariff Mechanisms

The Scheme of Control Agreement with the Hong Kong government caps HK Electric’s allowed return and sets tariff formulas, effectively substituting direct customer bargaining with regulatory oversight; under the current SoC (renewed 2020), allowed return is about 8.99% pre-tax on capital, keeping residential tariffs at HKD 1.244/kWh in 2024 and limiting price volatility.

Geographic Monopoly Constraints

Customers on Hong Kong Island and Lamma Island have no alternative electricity supplier, so buyer power is low and switching is effectively impossible; HK Electric serves about 580,000 accounts and 2.1 million people as of 2024.

That geographic monopoly gives the company pricing control, but public and political scrutiny constrains tariffs—HK Electric’s average tariff was HK$1.305/kWh in 2024 and proposed rises face regulatory pushback.

Regulatory oversight by the Hong Kong Government and the Electricity Ordinance means rate increases must balance company returns and public affordability, limiting exploitative pricing despite captive demand.

Public and Political Sensitivity

Electricity is essential, so any tariff move is politically explosive in Hong Kong; a proposed 2024 tariff rise of 3.5% sparked protests and hearings in the Legislative Council, showing sensitivity to price changes.

Organized consumer groups and >10 LegCo members regularly press HK Electric to justify hikes, linking affordability to social stability and urging audits and subsidy options.

Consequently, HK Electric must publish detailed cost-pass-through analyses and keep ROE targets transparent—its 2023 allowed return on equity was ~8.5%—to gain public and political buy-in.

Commercial Sector Energy Efficiency

Governmental Influence on Strategy

The Hong Kong government functions as the de facto customer representative in Scheme of Control reviews, using its regulatory role to push HK Electric Investments toward higher service standards and green investments without guaranteeing higher returns.

In the 2024 review, regulators asked for accelerated decarbonisation targets aligned with the 2050 net-zero goal, potentially adding HK$5–8 billion capex by 2030, while tariff allowances remained tightly constrained.

This institutional oversight concentrates citizen bargaining power into policy demands, increasing non-price obligations and compressing allowable ROE pressures on the company.

- Government negotiates on behalf of citizens

- 2024 review implied HK$5–8bn extra capex by 2030

- Higher service/green mandates with limited profit relief

HK Electric: Monopoly reach vs regulatory caps, demand cuts and HK$5–8bn decarb cost

Customers have low direct bargaining power due to HK Electric’s geographic monopoly (580,000 accounts, 2.1M people in 2024), but regulatory caps (SoC allowed return ~8.99% pre-tax; avg tariff HK$1.305/kWh in 2024) plus political pressure, large C&I demand reductions (smart BMS cuts 8–12%) and 2024 decarbonisation CAPEX needs (HK$5–8bn by 2030) constrain pricing power.

| Metric | Value (2024) |

|---|---|

| Accounts served | 580,000 |

| Population served | 2.1M |

| Avg tariff | HK$1.305/kWh |

| Allowed return (pre-tax) | ~8.99% |

| C&I demand cut (smart BMS) | 8–12% |

| Decarb CAPEX to 2030 | HK$5–8bn |

Preview Before You Purchase

HK Electric Investments Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of HK Electric Investments you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.