Hoffman Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

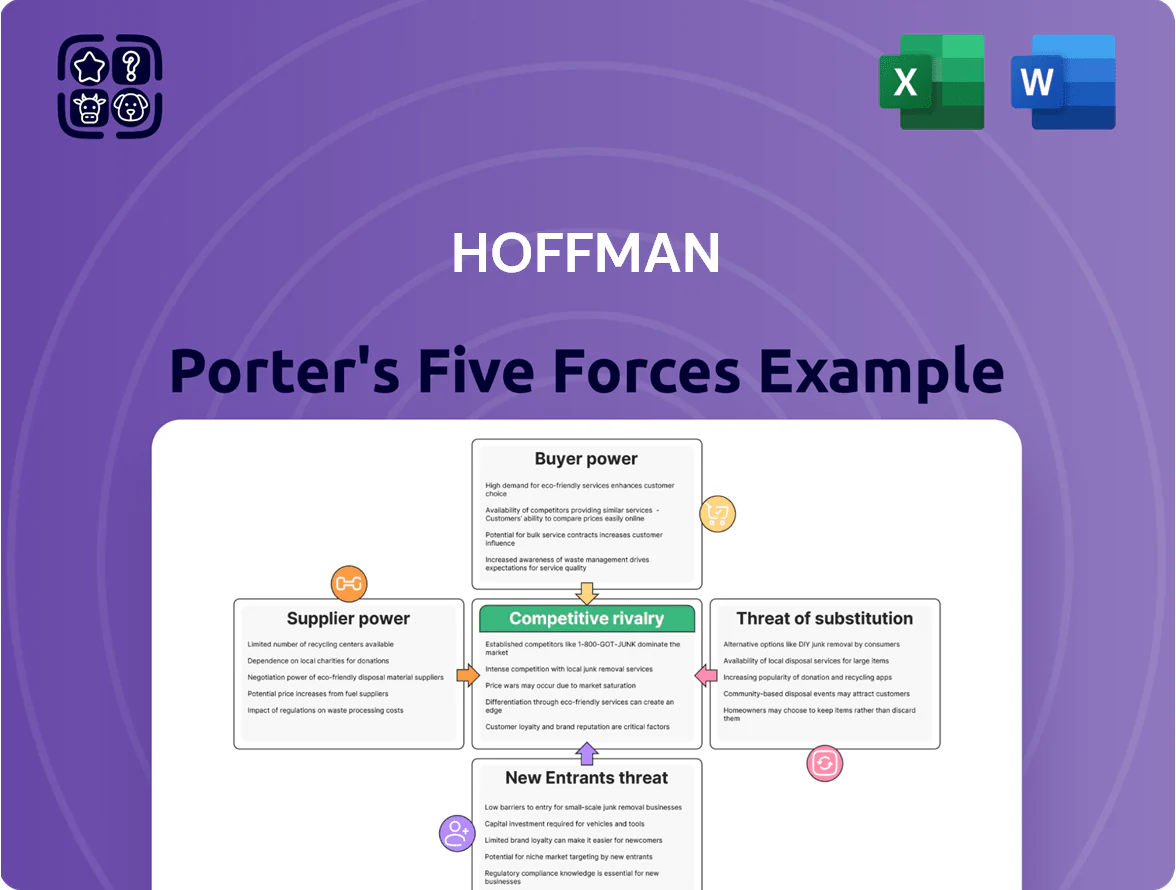

Hoffman’s Five Forces snapshot highlights supplier leverage, buyer pressure, competitive rivalry, threat of new entrants, and substitute risks—framing the core dynamics that shape its strategic options.

This brief preview only scratches the surface; unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights tailored to Hoffman for smarter investment and strategy decisions.

Suppliers Bargaining Power

Specialized Labor Availability

The construction sector in late 2025 faces a 20–25% shortage of highly skilled trades and specialized engineers, giving unions and niche subcontractors strong bargaining power to push wages up 8–15% year-over-year on complex projects.

Hoffman must sustain long-term agreements and referral pipelines with key labor pools; a single two-week crew delay can raise project costs ~1.5–3% and extend timelines, risking penalty clauses and margin erosion.

Raw Material Price Volatility

Suppliers of green steel, low-carbon concrete, and specialty glass hold strong leverage as global supply disruptions pushed green steel premiums up ~35% in 2024 and low-carbon cement shortages tightened availability by an estimated 18% in Europe; tighter environmental rules have demand outstripping supply, letting vendors set prices and lead times. Hoffman must secure multi-year contracts—locking 60–80% of input needs reduces margin volatility and hedges against spot-price spikes that eroded 120–250 bps of gross margin in 2023–2024.

Proprietary Building Technologies

The integration of proprietary building management systems and smart tech gives specialized vendors high bargaining power; 2024 industry data shows 68% of design-build healthcare projects specify vendor-locked platforms. These suppliers deliver unique, hard-to-replace components critical in the design-build phase, raising switching costs and schedule risk. Hoffman frequently faces price pressure—vendor markups can add 4–9% to project budgets—and is often tethered to partner pricing mid-project.

Subcontractor Expertise in Niche Markets

For projects like hyperscale data centers and advanced medical facilities, roughly 20–30 specialist subcontractors globally hold the required certifications and track records, letting them pick projects and charge premiums; market reports from 2025 show specialty labor rates 15–25% above general contractor rates, and Hoffman’s dependence on this elite cohort raises supplier bargaining power, constraining schedule flexibility and increasing margin risk.

- 20–30 global niche subcontractors

- Specialty rates 15–25% premium (2025)

- Higher project selectivity reduces Hoffman’s leverage

- Increased schedule and margin risk

Energy and Logistics Costs

Suppliers of transport and heavy machinery face volatile energy prices and new carbon taxes in 2025, raising diesel and electricity costs by about 12–18% year-over-year in many markets (IEA, 2025); they shift these increases to general contractors via fuel surcharges and 8–20% higher rental rates for specialized equipment.

Hoffman must build supplier-driven cost uplifts into bids for large infrastructure jobs—adding 6–10% contingencies to baseline estimates reduces underquoting risk when energy or carbon levies spike.

- 2025 energy rise: +12–18% (IEA)

- Equipment rental hike: +8–20%

- Recommended contingency: +6–10%

Suppliers' leverage spikes costs—wage, green premiums & energy force 6–10% bid buffers

Suppliers hold high bargaining power: skilled labor shortages (20–25%) push wage inflation 8–15% (2025), green-material premiums rose ~35% (2024) with low-carbon cement availability down ~18% (Europe), vendor-locked tech on 68% of projects increases switching costs, and equipment energy costs +12–18% (IEA, 2025) lead to recommended bid contingencies of 6–10%.

| Metric | Value |

|---|---|

| Skilled shortage | 20–25% |

| Wage inflation | 8–15% |

| Green steel premium | ~35% |

| Low‑carbon cement shortage | ~18% |

| Vendor‑locked projects | 68% |

| Energy cost rise | 12–18% |

| Bid contingency | 6–10% |

What is included in the product

Concise Five Forces assessment tailored to Hoffman, uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats with actionable strategic insights for investor decks and internal planning.

Hoffman Porter’s Five Forces delivers a concise one-sheet that quantifies competitive pressure and highlights where to act—ideal for rapid strategic pivots and investor briefs.

Customers Bargaining Power

Client Concentration in Tech and Healthcare

A significant share of Hoffman’s revenue—about 48% in FY2024—comes from roughly 7 top clients in tech and healthcare, concentrating bargaining power. These firms, with average annual IT budgets >$200M, push for lower rates and bespoke delivery models, pressuring margins. Their option to shift later project phases to rivals creates strong leverage in initial negotiations, often leading to longer payment terms and higher performance penalties. Recent renewals show pricing concessions averaging 6.5% per deal.

Sophisticated Procurement Processes

Institutional clients now use data-driven procurement and third-party consultants—McKinsey estimates 60% of large US institutions employed such consultants in 2024—to audit bids, pushing Hoffman to reveal margins and overheads during RFPs.

This scrutiny, and industry benchmarks showing average construction margin compression to 4–6% in 2024, forces Hoffman to boost cost transparency and cut unit costs to stay competitive.

Demand for Sustainable and LEED Certification

By end-2025, 61% of major corporate and public clients require net-zero targets or LEED Gold+/Platinum, shifting buying power to customers who set green specs.

These demands raise project costs: LEED Platinum premiums average 7–12% and net-zero systems add $40–120/sq ft, so buyers force higher-spec materials and complex builds.

Hoffman must meet these standards to access top-tier contracts worth 20–35% higher margins, so adapting design, supply chains, and reporting is mandatory.

Alternative Project Delivery Options

Clients now pick delivery methods like Integrated Project Delivery (IPD) or Public-Private Partnerships (P3) in roughly 28% of large U.S. infrastructure contracts in 2024, shifting cost and schedule risk to contractors or demanding open-book accounting.

Hoffman must accept collaborative frameworks and risk-transfer terms to win institutional projects; refusal can cut eligible bid pool by an estimated 30% on major public and healthcare procurements.

- 28%: IPD/P3 share of large U.S. deals (2024)

- ~30%: reduction in bid eligibility if Hoffman rejects client frameworks

- Clients often demand open-book financials and shared risk

Low Switching Costs for Future Projects

While mid-project contractor changes are costly, clients face low switching costs for future developments, keeping competition high; industry data shows 42% of clients consider replacing a firm after one major delivery failure (McKinsey 2024).

Hoffman must continually prove value and reliability to retain repeat business; top-tier rivals like Turner and Skanska hold 18–25% national market shares, so a single project failure can shift a client’s entire portfolio to a competitor.

- 42% of clients consider replacing after one failure

- Top rivals hold 18–25% market share

- Low future switching costs sustain perpetual competition

Concentrated clients wield pricing, green & delivery rules—risk of 30% lost bids

Major clients (7 accounts, ~48% FY2024 revenue) exert high bargaining power, driving 6.5% average price concessions and longer payment terms; consultants audit bids (60% usage, 2024) forcing margin disclosure. Green specs (61% require net-zero/LEED by 2025) and delivery choices (28% IPD/P3) shift risk to Hoffman, reducing eligible bids ~30% if refused; switching remains low-cost with 42% clients ready to replace after one failure.

| Metric | Value |

|---|---|

| Top-client revenue share (FY2024) | 48% |

| Price concessions (avg) | 6.5% |

| Consultant use in procurement (2024) | 60% |

| Clients requiring net-zero/LEED by 2025 | 61% |

| IPD/P3 share (large US deals, 2024) | 28% |

| Bid eligibility loss if frameworks refused | ~30% |

| Clients likely to replace after one failure | 42% |

Same Document Delivered

Hoffman Porter's Five Forces Analysis

This preview displays the exact Hoffman Porter Five Forces analysis you'll receive upon purchase—no placeholders or mockups, fully formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Hoffman’s Five Forces snapshot highlights supplier leverage, buyer pressure, competitive rivalry, threat of new entrants, and substitute risks—framing the core dynamics that shape its strategic options.

This brief preview only scratches the surface; unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights tailored to Hoffman for smarter investment and strategy decisions.

Suppliers Bargaining Power

Specialized Labor Availability

The construction sector in late 2025 faces a 20–25% shortage of highly skilled trades and specialized engineers, giving unions and niche subcontractors strong bargaining power to push wages up 8–15% year-over-year on complex projects.

Hoffman must sustain long-term agreements and referral pipelines with key labor pools; a single two-week crew delay can raise project costs ~1.5–3% and extend timelines, risking penalty clauses and margin erosion.

Raw Material Price Volatility

Suppliers of green steel, low-carbon concrete, and specialty glass hold strong leverage as global supply disruptions pushed green steel premiums up ~35% in 2024 and low-carbon cement shortages tightened availability by an estimated 18% in Europe; tighter environmental rules have demand outstripping supply, letting vendors set prices and lead times. Hoffman must secure multi-year contracts—locking 60–80% of input needs reduces margin volatility and hedges against spot-price spikes that eroded 120–250 bps of gross margin in 2023–2024.

Proprietary Building Technologies

The integration of proprietary building management systems and smart tech gives specialized vendors high bargaining power; 2024 industry data shows 68% of design-build healthcare projects specify vendor-locked platforms. These suppliers deliver unique, hard-to-replace components critical in the design-build phase, raising switching costs and schedule risk. Hoffman frequently faces price pressure—vendor markups can add 4–9% to project budgets—and is often tethered to partner pricing mid-project.

Subcontractor Expertise in Niche Markets

For projects like hyperscale data centers and advanced medical facilities, roughly 20–30 specialist subcontractors globally hold the required certifications and track records, letting them pick projects and charge premiums; market reports from 2025 show specialty labor rates 15–25% above general contractor rates, and Hoffman’s dependence on this elite cohort raises supplier bargaining power, constraining schedule flexibility and increasing margin risk.

- 20–30 global niche subcontractors

- Specialty rates 15–25% premium (2025)

- Higher project selectivity reduces Hoffman’s leverage

- Increased schedule and margin risk

Energy and Logistics Costs

Suppliers of transport and heavy machinery face volatile energy prices and new carbon taxes in 2025, raising diesel and electricity costs by about 12–18% year-over-year in many markets (IEA, 2025); they shift these increases to general contractors via fuel surcharges and 8–20% higher rental rates for specialized equipment.

Hoffman must build supplier-driven cost uplifts into bids for large infrastructure jobs—adding 6–10% contingencies to baseline estimates reduces underquoting risk when energy or carbon levies spike.

- 2025 energy rise: +12–18% (IEA)

- Equipment rental hike: +8–20%

- Recommended contingency: +6–10%

Suppliers' leverage spikes costs—wage, green premiums & energy force 6–10% bid buffers

Suppliers hold high bargaining power: skilled labor shortages (20–25%) push wage inflation 8–15% (2025), green-material premiums rose ~35% (2024) with low-carbon cement availability down ~18% (Europe), vendor-locked tech on 68% of projects increases switching costs, and equipment energy costs +12–18% (IEA, 2025) lead to recommended bid contingencies of 6–10%.

| Metric | Value |

|---|---|

| Skilled shortage | 20–25% |

| Wage inflation | 8–15% |

| Green steel premium | ~35% |

| Low‑carbon cement shortage | ~18% |

| Vendor‑locked projects | 68% |

| Energy cost rise | 12–18% |

| Bid contingency | 6–10% |

What is included in the product

Concise Five Forces assessment tailored to Hoffman, uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats with actionable strategic insights for investor decks and internal planning.

Hoffman Porter’s Five Forces delivers a concise one-sheet that quantifies competitive pressure and highlights where to act—ideal for rapid strategic pivots and investor briefs.

Customers Bargaining Power

Client Concentration in Tech and Healthcare

A significant share of Hoffman’s revenue—about 48% in FY2024—comes from roughly 7 top clients in tech and healthcare, concentrating bargaining power. These firms, with average annual IT budgets >$200M, push for lower rates and bespoke delivery models, pressuring margins. Their option to shift later project phases to rivals creates strong leverage in initial negotiations, often leading to longer payment terms and higher performance penalties. Recent renewals show pricing concessions averaging 6.5% per deal.

Sophisticated Procurement Processes

Institutional clients now use data-driven procurement and third-party consultants—McKinsey estimates 60% of large US institutions employed such consultants in 2024—to audit bids, pushing Hoffman to reveal margins and overheads during RFPs.

This scrutiny, and industry benchmarks showing average construction margin compression to 4–6% in 2024, forces Hoffman to boost cost transparency and cut unit costs to stay competitive.

Demand for Sustainable and LEED Certification

By end-2025, 61% of major corporate and public clients require net-zero targets or LEED Gold+/Platinum, shifting buying power to customers who set green specs.

These demands raise project costs: LEED Platinum premiums average 7–12% and net-zero systems add $40–120/sq ft, so buyers force higher-spec materials and complex builds.

Hoffman must meet these standards to access top-tier contracts worth 20–35% higher margins, so adapting design, supply chains, and reporting is mandatory.

Alternative Project Delivery Options

Clients now pick delivery methods like Integrated Project Delivery (IPD) or Public-Private Partnerships (P3) in roughly 28% of large U.S. infrastructure contracts in 2024, shifting cost and schedule risk to contractors or demanding open-book accounting.

Hoffman must accept collaborative frameworks and risk-transfer terms to win institutional projects; refusal can cut eligible bid pool by an estimated 30% on major public and healthcare procurements.

- 28%: IPD/P3 share of large U.S. deals (2024)

- ~30%: reduction in bid eligibility if Hoffman rejects client frameworks

- Clients often demand open-book financials and shared risk

Low Switching Costs for Future Projects

While mid-project contractor changes are costly, clients face low switching costs for future developments, keeping competition high; industry data shows 42% of clients consider replacing a firm after one major delivery failure (McKinsey 2024).

Hoffman must continually prove value and reliability to retain repeat business; top-tier rivals like Turner and Skanska hold 18–25% national market shares, so a single project failure can shift a client’s entire portfolio to a competitor.

- 42% of clients consider replacing after one failure

- Top rivals hold 18–25% market share

- Low future switching costs sustain perpetual competition

Concentrated clients wield pricing, green & delivery rules—risk of 30% lost bids

Major clients (7 accounts, ~48% FY2024 revenue) exert high bargaining power, driving 6.5% average price concessions and longer payment terms; consultants audit bids (60% usage, 2024) forcing margin disclosure. Green specs (61% require net-zero/LEED by 2025) and delivery choices (28% IPD/P3) shift risk to Hoffman, reducing eligible bids ~30% if refused; switching remains low-cost with 42% clients ready to replace after one failure.

| Metric | Value |

|---|---|

| Top-client revenue share (FY2024) | 48% |

| Price concessions (avg) | 6.5% |

| Consultant use in procurement (2024) | 60% |

| Clients requiring net-zero/LEED by 2025 | 61% |

| IPD/P3 share (large US deals, 2024) | 28% |

| Bid eligibility loss if frameworks refused | ~30% |

| Clients likely to replace after one failure | 42% |

Same Document Delivered

Hoffman Porter's Five Forces Analysis

This preview displays the exact Hoffman Porter Five Forces analysis you'll receive upon purchase—no placeholders or mockups, fully formatted and ready for immediate download and use.