Holder Construction PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE Analysis of Holder Construction—spot regulatory risks, technological shifts, and environmental pressures shaping the firm’s future. Tailored for investors, consultants, and executives, this concise report turns external trends into actionable strategy. Purchase the full version to access the complete, editable analysis and make faster, smarter decisions.

Political factors

Federal Infrastructure Funding

Federal infrastructure allocations through FY2024–2026 channel over $120B toward aviation and public facilities modernization, sustaining a predictable project pipeline for Holder Construction in airport and higher-education builds.

Holder’s aviation and campus portfolios align with USDOT and IIJA-driven priorities, positioning the firm for a growing share of $45B+ in planned FAA airport grants and related P3 opportunities.

Strategic alignment with national goals enhances Holder’s competitiveness for multi-year public-private partnerships, supporting revenue stability amid anticipated federal capital spending through 2026.

Data Center Zoning and Regulation

As U.S. data center power demand rose ~8% in 2024 and states like New York and California tightened energy and siting rules, Holder Construction faces stricter zoning and energy-use mandates that affect site selection and capex timing; community opposition over land and grid strain now delays projects by months on average. Proactive engagement with local officials and utilities is essential to secure permits and protect Holder’s leadership in mission-critical builds.

Trade Policies and Material Tariffs

Ongoing US trade negotiations and tariffs—including current steel tariffs around 25% and a 2024 spike in imported specialty components costs of roughly 12%—force Holder to adjust procurement across national projects; monitoring shifts in US-China and US-EU relations is essential to avoid abrupt cost increases or 2024 supply delays that affected 8–10% of construction schedules. Developing domestic supplier hubs and flexible contracts (e.g., index-linked pricing, 30–60 day lead clauses) can shield project budgets from geopolitical volatility.

Public Sector Educational Budgeting

State-level shifts in higher education funding directly affect campus expansion and renovation volumes; U.S. state appropriations for higher education fell 3.1% per FTE from 2008–2022 but rebounded in 2023–24 with a median 4% increase, influencing Holder Construction’s project pipeline.

Holder monitors legislative sessions and budget hearings because institutional capital plans depend on these allocations; targeting states with FY2024 higher-ed capital increases (e.g., CA, NY, TX) improves bid win probability.

- State appropriation trends: +4% median FY2023–24

- Key targets: CA, NY, TX with major capital plans

- Legislative sessions drive project timing and volume

Safety and Labor Legislation

Federal and state agendas tightened worker-rights and site-safety rules through 2024–2025, with OSHA and several states issuing new heat-illness prevention mandates; construction heat-related citations rose 22% in 2024, pressuring Holder to update protocols and training.

New apprentice-ratio regulations in CA and WA require firms to document ratios on projects—affecting labor cost profiles; Holder must adjust subcontractor contracts and payroll forecasting to absorb a projected 1–2% margin impact.

Proactively aligning compliance reduces violation risk and protects Holder’s reputation—companies with strong safety records saw insurance premium discounts up to 10% in 2024, underscoring financial incentives to lead on safety.

- Heat-illness citations +22% (2024)

- Estimated margin impact from apprentice ratios 1–2%

- Safety-led insurance premium reductions up to 10%

FAA $45B+ pipeline and $120B infrastructure drive work amid tariffs, supply and safety costs

Federal infrastructure funding (FY2024–26) and $45B+ FAA grant pipeline secure predictable airport/campus work; state higher-ed capital up ~4% FY2023–24 (CA, NY, TX) boosting bids. Trade tariffs (steel ~25%, specialty imports +12% in 2024) and 8–10% schedule impacts from 2024 supply disruptions raise procurement risk; domestic sourcing mitigates. OSHA/state heat rules (heat citations +22% 2024) and CA/WA apprentice ratios (1–2% margin hit) require compliance investment to protect margins and insurance discounts (~10%).

| Metric | Value |

|---|---|

| FAA grant pipeline | $45B+ |

| Infrastructure funding FY24–26 | $120B+ |

| State higher-ed capital change FY23–24 | +4% (median) |

| Steel tariffs (2024) | ~25% |

| Specialty import cost spike (2024) | +12% |

| Supply-driven schedule impacts (2024) | 8–10% |

| Heat-related citations (2024) | +22% |

| Apprentice-ratio margin impact | 1–2% |

| Insurance premium reduction (safety leaders) | up to 10% |

What is included in the product

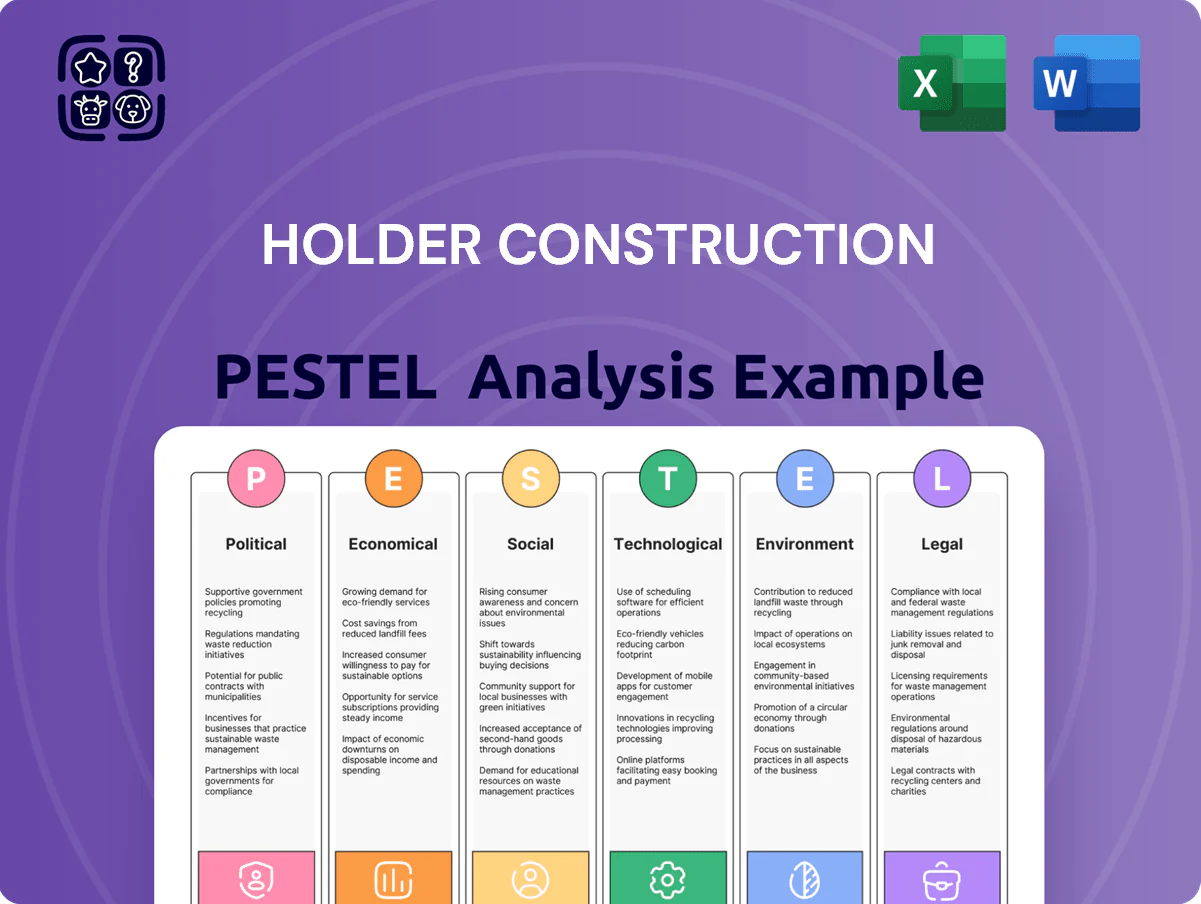

Explores how macro-environmental forces uniquely affect Holder Construction across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, consultants, and investors.

Provides a clean, visually segmented PESTLE summary for Holder Construction that’s easy to drop into presentations or share across teams, helping stakeholders quickly assess external risks and market positioning.

Economic factors

Interest Rate Environment

By end-2025 U.S. policy rates settled near 5.25–5.50%, but elevated borrowing costs keep cost of capital top concern for hospitality and corporate real estate clients; higher rates in 2024–25 pushed CRE transaction volumes down ~30% YoY in some markets.

For Holder, rate-driven delays or scope cuts mean demand for efficient preconstruction rises; providing value-engineered designs can preserve ROI amid 6–8% construction financing spreads.

Accurate cost forecasting—within +/-3% on recent midmarket projects—remains a key competitive advantage in winning fee-based early-stage work.

Skilled Labor Market Dynamics

The US construction sector faced a 2024 skilled labor shortfall of about 430,000 workers, pushing craft wages up roughly 6–8% year-over-year; Holder must expand apprenticeship and retention programs to secure talent and meet schedules.

Rising labor costs and a 2023–24 subcontractor margin squeeze (average gross margins down ~1.5–2 ppt) force Holder to deepen subcontractor partnerships and training investments to protect quality delivery.

Labor inflation requires Holder to adopt data-driven estimating and HR analytics—companies using AI-enabled estimating report up to 10% better margin accuracy, critical to preserving Holder’s project profitability.

Material Price Volatility

Fluctuations in prices for concrete, copper and data-center equipment—cement up ~18% and copper up ~22% 2022–2024—have forced Holder to increase agile supply-chain measures to protect margins.

By end-2025 Holder expanded early procurement and warehousing for long-lead items, covering an estimated 40–55% of project needs to lock prices and reduce exposure.

This economic pressure raises the preconstruction phase’s value: detailed cost modeling and procurement sequencing have lowered bid-to-complete variance by roughly 6–9 percentage points on complex builds.

Corporate Real Estate Demand

The shift to hybrid work cut U.S. downtown office occupancy to about 62% in 2024, driving Holder toward adaptive reuse and high-tech renovations to capture demand for flexible, collaborative spaces and build upgrades that command 10–20% higher rent premiums.

Commercial construction starts fell 8% year-over-year in 2024, so Holder is diversifying into healthcare and mission-critical facilities—sectors with projected CAGR >4% and lower vacancy volatility.

Monitoring metro office vacancy rates (national office vacancy ~17% in 2024) and corporate CAPEX trends—S&P 500 CAPEX down ~3% in 2024—remains vital for Holder’s long-term site selection and backlog management.

- Adaptation: focus on adaptive reuse, tech retrofits

- Diversification: healthcare, data centers, life sciences

- Metrics: track vacancy ~17%, occupancy ~62%, CAPEX trends

Energy Infrastructure Costs

Rising wholesale U.S. electricity prices rose ~12% in 2022–2024 in many markets, increasing operational costs for facilities Holder builds, notably data centers where energy is ~50%+ of OPEX.

Clients demand energy-efficient designs—PUE targets ≤1.2—to reduce total cost of ownership amid volatile natural gas and power markets.

Holder’s sustainable, high-performance delivery attracts institutional investors seeking lower lifecycle costs and ESG-aligned returns.

- U.S. electricity +12% (2022–2024)

- Data center energy ≈50%+ OPEX

- PUE target ≤1.2

- Investor demand for ESG infrastructure rising

Higher rates, squeezed CRE & rising input costs push preconstruction value plays—Holder boosts procurement

Higher 2024–25 rates (Fed 5.25–5.50%) and CRE volume down ~30% shifted demand to value-engineered preconstruction; labor shortfall ~430k raised wages 6–8%; cement +18%, copper +22% (2022–24); electricity +12% (2022–24); Holder expanded early procurement to cover 40–55% of long-lead items and targets PUE ≤1.2 for energy-sensitive builds.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| CRE volume change | ≈-30% YoY |

| Labor gap | ≈430,000 workers |

| Wage inflation | 6–8% |

| Cement / Copper | +18% / +22% |

| Electricity | +12% |

| Procurement cover | 40–55% |

| PUE target | ≤1.2 |

What You See Is What You Get

Holder Construction PESTLE Analysis

The preview shown here is the exact Holder Construction PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE Analysis of Holder Construction—spot regulatory risks, technological shifts, and environmental pressures shaping the firm’s future. Tailored for investors, consultants, and executives, this concise report turns external trends into actionable strategy. Purchase the full version to access the complete, editable analysis and make faster, smarter decisions.

Political factors

Federal Infrastructure Funding

Federal infrastructure allocations through FY2024–2026 channel over $120B toward aviation and public facilities modernization, sustaining a predictable project pipeline for Holder Construction in airport and higher-education builds.

Holder’s aviation and campus portfolios align with USDOT and IIJA-driven priorities, positioning the firm for a growing share of $45B+ in planned FAA airport grants and related P3 opportunities.

Strategic alignment with national goals enhances Holder’s competitiveness for multi-year public-private partnerships, supporting revenue stability amid anticipated federal capital spending through 2026.

Data Center Zoning and Regulation

As U.S. data center power demand rose ~8% in 2024 and states like New York and California tightened energy and siting rules, Holder Construction faces stricter zoning and energy-use mandates that affect site selection and capex timing; community opposition over land and grid strain now delays projects by months on average. Proactive engagement with local officials and utilities is essential to secure permits and protect Holder’s leadership in mission-critical builds.

Trade Policies and Material Tariffs

Ongoing US trade negotiations and tariffs—including current steel tariffs around 25% and a 2024 spike in imported specialty components costs of roughly 12%—force Holder to adjust procurement across national projects; monitoring shifts in US-China and US-EU relations is essential to avoid abrupt cost increases or 2024 supply delays that affected 8–10% of construction schedules. Developing domestic supplier hubs and flexible contracts (e.g., index-linked pricing, 30–60 day lead clauses) can shield project budgets from geopolitical volatility.

Public Sector Educational Budgeting

State-level shifts in higher education funding directly affect campus expansion and renovation volumes; U.S. state appropriations for higher education fell 3.1% per FTE from 2008–2022 but rebounded in 2023–24 with a median 4% increase, influencing Holder Construction’s project pipeline.

Holder monitors legislative sessions and budget hearings because institutional capital plans depend on these allocations; targeting states with FY2024 higher-ed capital increases (e.g., CA, NY, TX) improves bid win probability.

- State appropriation trends: +4% median FY2023–24

- Key targets: CA, NY, TX with major capital plans

- Legislative sessions drive project timing and volume

Safety and Labor Legislation

Federal and state agendas tightened worker-rights and site-safety rules through 2024–2025, with OSHA and several states issuing new heat-illness prevention mandates; construction heat-related citations rose 22% in 2024, pressuring Holder to update protocols and training.

New apprentice-ratio regulations in CA and WA require firms to document ratios on projects—affecting labor cost profiles; Holder must adjust subcontractor contracts and payroll forecasting to absorb a projected 1–2% margin impact.

Proactively aligning compliance reduces violation risk and protects Holder’s reputation—companies with strong safety records saw insurance premium discounts up to 10% in 2024, underscoring financial incentives to lead on safety.

- Heat-illness citations +22% (2024)

- Estimated margin impact from apprentice ratios 1–2%

- Safety-led insurance premium reductions up to 10%

FAA $45B+ pipeline and $120B infrastructure drive work amid tariffs, supply and safety costs

Federal infrastructure funding (FY2024–26) and $45B+ FAA grant pipeline secure predictable airport/campus work; state higher-ed capital up ~4% FY2023–24 (CA, NY, TX) boosting bids. Trade tariffs (steel ~25%, specialty imports +12% in 2024) and 8–10% schedule impacts from 2024 supply disruptions raise procurement risk; domestic sourcing mitigates. OSHA/state heat rules (heat citations +22% 2024) and CA/WA apprentice ratios (1–2% margin hit) require compliance investment to protect margins and insurance discounts (~10%).

| Metric | Value |

|---|---|

| FAA grant pipeline | $45B+ |

| Infrastructure funding FY24–26 | $120B+ |

| State higher-ed capital change FY23–24 | +4% (median) |

| Steel tariffs (2024) | ~25% |

| Specialty import cost spike (2024) | +12% |

| Supply-driven schedule impacts (2024) | 8–10% |

| Heat-related citations (2024) | +22% |

| Apprentice-ratio margin impact | 1–2% |

| Insurance premium reduction (safety leaders) | up to 10% |

What is included in the product

Explores how macro-environmental forces uniquely affect Holder Construction across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, consultants, and investors.

Provides a clean, visually segmented PESTLE summary for Holder Construction that’s easy to drop into presentations or share across teams, helping stakeholders quickly assess external risks and market positioning.

Economic factors

Interest Rate Environment

By end-2025 U.S. policy rates settled near 5.25–5.50%, but elevated borrowing costs keep cost of capital top concern for hospitality and corporate real estate clients; higher rates in 2024–25 pushed CRE transaction volumes down ~30% YoY in some markets.

For Holder, rate-driven delays or scope cuts mean demand for efficient preconstruction rises; providing value-engineered designs can preserve ROI amid 6–8% construction financing spreads.

Accurate cost forecasting—within +/-3% on recent midmarket projects—remains a key competitive advantage in winning fee-based early-stage work.

Skilled Labor Market Dynamics

The US construction sector faced a 2024 skilled labor shortfall of about 430,000 workers, pushing craft wages up roughly 6–8% year-over-year; Holder must expand apprenticeship and retention programs to secure talent and meet schedules.

Rising labor costs and a 2023–24 subcontractor margin squeeze (average gross margins down ~1.5–2 ppt) force Holder to deepen subcontractor partnerships and training investments to protect quality delivery.

Labor inflation requires Holder to adopt data-driven estimating and HR analytics—companies using AI-enabled estimating report up to 10% better margin accuracy, critical to preserving Holder’s project profitability.

Material Price Volatility

Fluctuations in prices for concrete, copper and data-center equipment—cement up ~18% and copper up ~22% 2022–2024—have forced Holder to increase agile supply-chain measures to protect margins.

By end-2025 Holder expanded early procurement and warehousing for long-lead items, covering an estimated 40–55% of project needs to lock prices and reduce exposure.

This economic pressure raises the preconstruction phase’s value: detailed cost modeling and procurement sequencing have lowered bid-to-complete variance by roughly 6–9 percentage points on complex builds.

Corporate Real Estate Demand

The shift to hybrid work cut U.S. downtown office occupancy to about 62% in 2024, driving Holder toward adaptive reuse and high-tech renovations to capture demand for flexible, collaborative spaces and build upgrades that command 10–20% higher rent premiums.

Commercial construction starts fell 8% year-over-year in 2024, so Holder is diversifying into healthcare and mission-critical facilities—sectors with projected CAGR >4% and lower vacancy volatility.

Monitoring metro office vacancy rates (national office vacancy ~17% in 2024) and corporate CAPEX trends—S&P 500 CAPEX down ~3% in 2024—remains vital for Holder’s long-term site selection and backlog management.

- Adaptation: focus on adaptive reuse, tech retrofits

- Diversification: healthcare, data centers, life sciences

- Metrics: track vacancy ~17%, occupancy ~62%, CAPEX trends

Energy Infrastructure Costs

Rising wholesale U.S. electricity prices rose ~12% in 2022–2024 in many markets, increasing operational costs for facilities Holder builds, notably data centers where energy is ~50%+ of OPEX.

Clients demand energy-efficient designs—PUE targets ≤1.2—to reduce total cost of ownership amid volatile natural gas and power markets.

Holder’s sustainable, high-performance delivery attracts institutional investors seeking lower lifecycle costs and ESG-aligned returns.

- U.S. electricity +12% (2022–2024)

- Data center energy ≈50%+ OPEX

- PUE target ≤1.2

- Investor demand for ESG infrastructure rising

Higher rates, squeezed CRE & rising input costs push preconstruction value plays—Holder boosts procurement

Higher 2024–25 rates (Fed 5.25–5.50%) and CRE volume down ~30% shifted demand to value-engineered preconstruction; labor shortfall ~430k raised wages 6–8%; cement +18%, copper +22% (2022–24); electricity +12% (2022–24); Holder expanded early procurement to cover 40–55% of long-lead items and targets PUE ≤1.2 for energy-sensitive builds.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| CRE volume change | ≈-30% YoY |

| Labor gap | ≈430,000 workers |

| Wage inflation | 6–8% |

| Cement / Copper | +18% / +22% |

| Electricity | +12% |

| Procurement cover | 40–55% |

| PUE target | ≤1.2 |

What You See Is What You Get

Holder Construction PESTLE Analysis

The preview shown here is the exact Holder Construction PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.