FUJIFILM Holdings Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

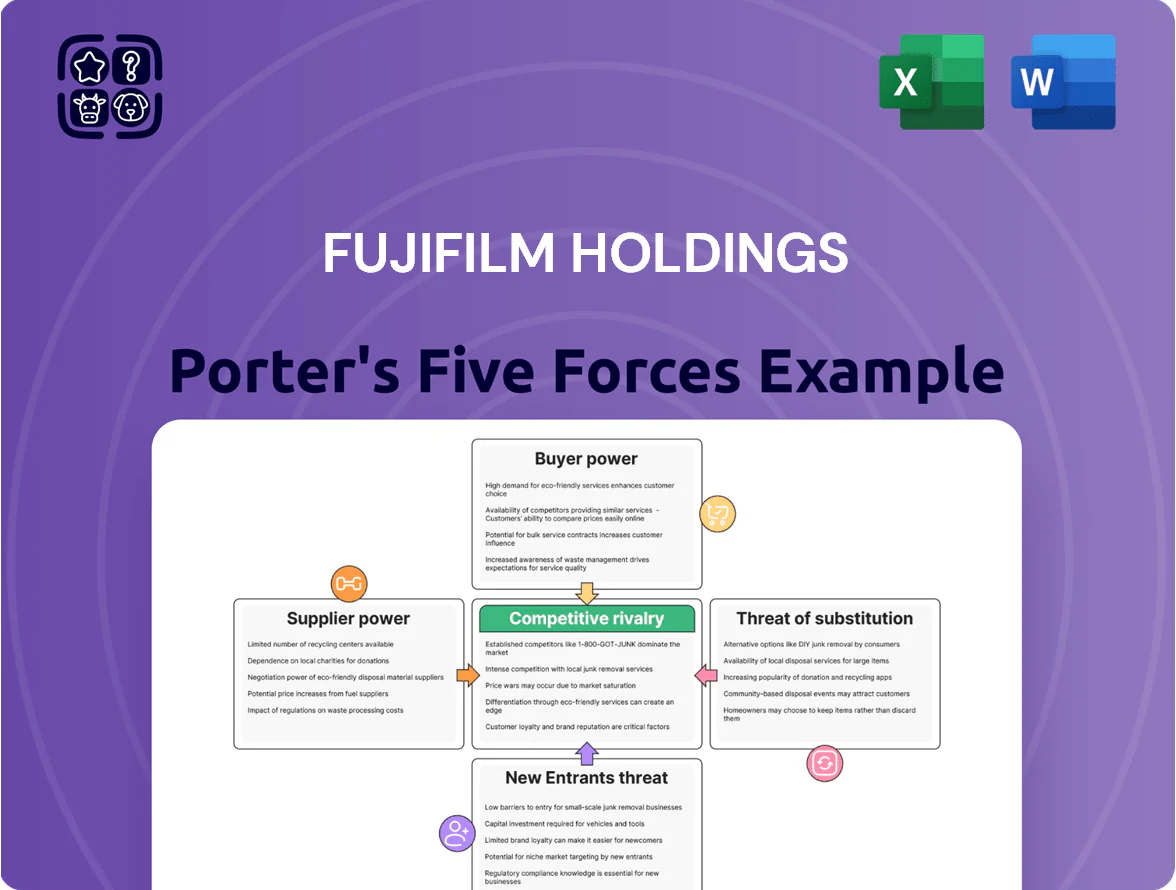

FUJIFILM Holdings faces moderate supplier power, strong brand-driven buyer loyalty, and intensified rivalry as it balances healthcare, imaging, and high-tech materials segments.

Threats from substitutes and new entrants vary by division—high in consumer imaging, lower in specialized medical and industrial businesses—shaping strategic priorities.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore FUJIFILM Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Providers for Biopharmaceuticals

Precision Optics and Electronic Component Manufacturers

Precision optics and sensor makers supply Fujifilm’s imaging and medical units with specialized glass, CMOS sensors and ASICs from a concentrated set of suppliers; global demand for advanced semiconductors rose ~20% in 2024, keeping supplier pricing power high.

Fujifilm offsets this via multi-year contracts and vertical moves in material sciences—R&D capex was ¥214.6bn in FY2024—yet top-tier component scarcity still constrains output and margin.

Chemical and Rare Earth Material Suppliers

Fujifilm’s functional materials unit relies heavily on rare earths and specialty chemicals for photoresists and display films; in Q3 2025 rare-earth oxide prices rose ~28% YoY and certain fluorinated solvents jumped 14% due to export curbs from key producers, boosting COGS pressure. Geopolitical tensions and trade policies in late 2025 tightened supply, giving suppliers pricing leverage and forcing Fujifilm to secure costly long-term contracts and diversify sources.

Energy and Utility Providers for Large Scale Manufacturing

- High energy use → margin sensitivity

- 2025: increased renewables investment (per filings)

- Japan/Europe: utility monopolies pass transition costs

- Spot and contract price exposure remains

Logistics and Distribution Network Partners

Fujifilm ships sensitive medical and chemical products worldwide, so a resilient logistics network is critical; in 2024 Fujifilm reported consolidated revenue of ¥2.05 trillion, implying large shipment volumes that give it negotiating leverage.

Major carriers—Maersk, MSC, DHL, FedEx—control key sea and air routes and fuel surcharges; global ocean container rates rose ~18% in 2023–24, shrinking Fujifilm's margin flexibility.

Industry consolidation limits specialized alternatives for temperature-controlled or hazardous transport, so Fujifilm balances reliance by multi-carrier contracts and long-term partnerships to manage supply risk.

- High shipment volume = bargaining leverage

- Carrier consolidation reduces alternatives

- Ocean rates +18% (2023–24) pressure costs

- Multi-carrier + long-term contracts mitigate risk

Fujifilm: Supplier Power & Rising Input Costs Strain Margins; R&D +¥214.6bn Mitigates

| Metric | Value |

|---|---|

| Revenue FY2024 | ¥2.05trn |

| R&D FY2024 | ¥214.6bn |

| Switch cost | 6–12 months; >¥50m |

| Rare-earths Q3 2025 | +28% YoY |

| Ocean rates 2023–24 | +18% |

What is included in the product

Tailored exclusively for FUJIFILM Holdings, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and strategic barriers that shape its pricing, profitability, and market resilience.

Compact Porter's Five Forces snapshot for FUJIFILM—quickly spot competitive threats, supplier/customer leverage, and substitution risks to inform strategic moves and M&A screening.

Customers Bargaining Power

Institutional Healthcare Providers and Hospital Groups

Large hospital networks and government healthcare systems are Fujifilm’s main buyers for imaging and diagnostics, and by Q4 2025 over 60% of procurement in key markets occurred via group purchasing organizations (GPOs) or competitive bids, pressuring list prices down by 8–12% on average.

Consolidation has concentrated buying power—top 10 hospital systems now control roughly 30% of US inpatient volume—forcing Fujifilm to win on both tech (AI-enabled modalities) and price, with service contracts and uptime guarantees becoming decisive bid levers.

Pharmaceutical and Biotech Companies in CDMO Services

As a major CDMO, Fujifilm serves top pharma clients who demand low cost and high efficiency; global CDMO top 5 captured ~45% of market in 2024, so customers can multi-source among rivals.

Clients are sophisticated and price-sensitive: 2024 pharma outsourcing spend reached ~$100B, and large firms shift volumes to save 5–15% per project, raising switching risk for Fujifilm.

Fujifilm must sustain GMP-level quality, 99% batch release reliability, and competitive margins—recent CDMO contract wins often hinge on

cost per batch and capacity lead times.

Corporate Clients in the Business Innovation Segment

Corporate clients in the business innovation segment wield high bargaining power as the office solutions market shifts to digital transformation; global vendors (Canon, Ricoh, HP) offer similar integrated software-hardware stacks and procurement pools often exceed $5m per account, so buyers can threaten switching. Fujifilm counters with customized, high-value services—managed print and workflow automation—that raised recurring revenue 12% YoY in FY2024 and create client lock-in, though initial contract wins stay fiercely price-competitive.

Consumer Sensitivity in the Imaging and Camera Market

Consumers face many choices from $200 smartphones to $5,000 mirrorless kits, so price sensitivity is high and brand switching costs are low outside loyal niches like Instax.

Fujifilm relies on product innovation to sustain premium pricing; global interchangeable-lens camera shipments fell ~15% from 2019–2023, increasing competitive pressure.

Semiconductor Manufacturers Purchasing Functional Materials

Major foundries—TSMC, Samsung, and GlobalFoundries—are few but huge, creating concentrated buyer power over Fujifilm Electronic Materials; TSMC alone accounted for ~20% of global wafer fab capacity in 2024.

They demand extreme precision and rapid innovation to reach sub-3nm nodes, so Fujifilm faces continuous R&D pressure and qualification cycles with high costs.

Technical stickiness exists due to complex chemistries, yet strategic importance of photoresists and CMP slurries makes customers push for volume discounts and long-term supply terms.

- Concentrated buyers: 3–5 foundries drive demand

- TSMC ~20% wafer capacity (2024)

- High R&D/qualification costs for sub-3nm

- Stickiness + bargaining for favorable terms

Fujifilm fights buyer pressure with AI, SLAs and recurring services amid heavy consolidation

Buyers across Fujifilm’s segments hold strong power: hospital GPOs cut prices 8–12% (Q4 2025; >60% procure via GPOs), top 10 US systems = ~30% inpatient volume, pharma CDMO top‑5 = ~45% market (2024) and outsourcing spend ~$100B (2024), foundries (TSMC ~20% wafer capacity 2024) demand discounts; Fujifilm counters with AI-enabled tech, service SLAs, and recurring managed‑services (Instax +5% FY2024).

| Metric | Value |

|---|---|

| GPO procurement | >60% (Q4 2025) |

| GPO price pressure | −8–12% |

| Top‑10 hospital share | ~30% US inpatient |

| CDMO top‑5 share | ~45% (2024) |

| Pharma outsourcing spend | ~$100B (2024) |

| TSMC wafer capacity | ~20% (2024) |

Full Version Awaits

FUJIFILM Holdings Porter's Five Forces Analysis

This preview shows the exact FUJIFILM Holdings Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.

The document covers supplier and buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable insights and concise scoring you can apply right away.

You're viewing the final deliverable; upon payment you’ll get instant access to this same file for download and implementation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

FUJIFILM Holdings faces moderate supplier power, strong brand-driven buyer loyalty, and intensified rivalry as it balances healthcare, imaging, and high-tech materials segments.

Threats from substitutes and new entrants vary by division—high in consumer imaging, lower in specialized medical and industrial businesses—shaping strategic priorities.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore FUJIFILM Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Providers for Biopharmaceuticals

Precision Optics and Electronic Component Manufacturers

Precision optics and sensor makers supply Fujifilm’s imaging and medical units with specialized glass, CMOS sensors and ASICs from a concentrated set of suppliers; global demand for advanced semiconductors rose ~20% in 2024, keeping supplier pricing power high.

Fujifilm offsets this via multi-year contracts and vertical moves in material sciences—R&D capex was ¥214.6bn in FY2024—yet top-tier component scarcity still constrains output and margin.

Chemical and Rare Earth Material Suppliers

Fujifilm’s functional materials unit relies heavily on rare earths and specialty chemicals for photoresists and display films; in Q3 2025 rare-earth oxide prices rose ~28% YoY and certain fluorinated solvents jumped 14% due to export curbs from key producers, boosting COGS pressure. Geopolitical tensions and trade policies in late 2025 tightened supply, giving suppliers pricing leverage and forcing Fujifilm to secure costly long-term contracts and diversify sources.

Energy and Utility Providers for Large Scale Manufacturing

- High energy use → margin sensitivity

- 2025: increased renewables investment (per filings)

- Japan/Europe: utility monopolies pass transition costs

- Spot and contract price exposure remains

Logistics and Distribution Network Partners

Fujifilm ships sensitive medical and chemical products worldwide, so a resilient logistics network is critical; in 2024 Fujifilm reported consolidated revenue of ¥2.05 trillion, implying large shipment volumes that give it negotiating leverage.

Major carriers—Maersk, MSC, DHL, FedEx—control key sea and air routes and fuel surcharges; global ocean container rates rose ~18% in 2023–24, shrinking Fujifilm's margin flexibility.

Industry consolidation limits specialized alternatives for temperature-controlled or hazardous transport, so Fujifilm balances reliance by multi-carrier contracts and long-term partnerships to manage supply risk.

- High shipment volume = bargaining leverage

- Carrier consolidation reduces alternatives

- Ocean rates +18% (2023–24) pressure costs

- Multi-carrier + long-term contracts mitigate risk

Fujifilm: Supplier Power & Rising Input Costs Strain Margins; R&D +¥214.6bn Mitigates

| Metric | Value |

|---|---|

| Revenue FY2024 | ¥2.05trn |

| R&D FY2024 | ¥214.6bn |

| Switch cost | 6–12 months; >¥50m |

| Rare-earths Q3 2025 | +28% YoY |

| Ocean rates 2023–24 | +18% |

What is included in the product

Tailored exclusively for FUJIFILM Holdings, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and strategic barriers that shape its pricing, profitability, and market resilience.

Compact Porter's Five Forces snapshot for FUJIFILM—quickly spot competitive threats, supplier/customer leverage, and substitution risks to inform strategic moves and M&A screening.

Customers Bargaining Power

Institutional Healthcare Providers and Hospital Groups

Large hospital networks and government healthcare systems are Fujifilm’s main buyers for imaging and diagnostics, and by Q4 2025 over 60% of procurement in key markets occurred via group purchasing organizations (GPOs) or competitive bids, pressuring list prices down by 8–12% on average.

Consolidation has concentrated buying power—top 10 hospital systems now control roughly 30% of US inpatient volume—forcing Fujifilm to win on both tech (AI-enabled modalities) and price, with service contracts and uptime guarantees becoming decisive bid levers.

Pharmaceutical and Biotech Companies in CDMO Services

As a major CDMO, Fujifilm serves top pharma clients who demand low cost and high efficiency; global CDMO top 5 captured ~45% of market in 2024, so customers can multi-source among rivals.

Clients are sophisticated and price-sensitive: 2024 pharma outsourcing spend reached ~$100B, and large firms shift volumes to save 5–15% per project, raising switching risk for Fujifilm.

Fujifilm must sustain GMP-level quality, 99% batch release reliability, and competitive margins—recent CDMO contract wins often hinge on

cost per batch and capacity lead times.

Corporate Clients in the Business Innovation Segment

Corporate clients in the business innovation segment wield high bargaining power as the office solutions market shifts to digital transformation; global vendors (Canon, Ricoh, HP) offer similar integrated software-hardware stacks and procurement pools often exceed $5m per account, so buyers can threaten switching. Fujifilm counters with customized, high-value services—managed print and workflow automation—that raised recurring revenue 12% YoY in FY2024 and create client lock-in, though initial contract wins stay fiercely price-competitive.

Consumer Sensitivity in the Imaging and Camera Market

Consumers face many choices from $200 smartphones to $5,000 mirrorless kits, so price sensitivity is high and brand switching costs are low outside loyal niches like Instax.

Fujifilm relies on product innovation to sustain premium pricing; global interchangeable-lens camera shipments fell ~15% from 2019–2023, increasing competitive pressure.

Semiconductor Manufacturers Purchasing Functional Materials

Major foundries—TSMC, Samsung, and GlobalFoundries—are few but huge, creating concentrated buyer power over Fujifilm Electronic Materials; TSMC alone accounted for ~20% of global wafer fab capacity in 2024.

They demand extreme precision and rapid innovation to reach sub-3nm nodes, so Fujifilm faces continuous R&D pressure and qualification cycles with high costs.

Technical stickiness exists due to complex chemistries, yet strategic importance of photoresists and CMP slurries makes customers push for volume discounts and long-term supply terms.

- Concentrated buyers: 3–5 foundries drive demand

- TSMC ~20% wafer capacity (2024)

- High R&D/qualification costs for sub-3nm

- Stickiness + bargaining for favorable terms

Fujifilm fights buyer pressure with AI, SLAs and recurring services amid heavy consolidation

Buyers across Fujifilm’s segments hold strong power: hospital GPOs cut prices 8–12% (Q4 2025; >60% procure via GPOs), top 10 US systems = ~30% inpatient volume, pharma CDMO top‑5 = ~45% market (2024) and outsourcing spend ~$100B (2024), foundries (TSMC ~20% wafer capacity 2024) demand discounts; Fujifilm counters with AI-enabled tech, service SLAs, and recurring managed‑services (Instax +5% FY2024).

| Metric | Value |

|---|---|

| GPO procurement | >60% (Q4 2025) |

| GPO price pressure | −8–12% |

| Top‑10 hospital share | ~30% US inpatient |

| CDMO top‑5 share | ~45% (2024) |

| Pharma outsourcing spend | ~$100B (2024) |

| TSMC wafer capacity | ~20% (2024) |

Full Version Awaits

FUJIFILM Holdings Porter's Five Forces Analysis

This preview shows the exact FUJIFILM Holdings Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.

The document covers supplier and buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable insights and concise scoring you can apply right away.

You're viewing the final deliverable; upon payment you’ll get instant access to this same file for download and implementation.