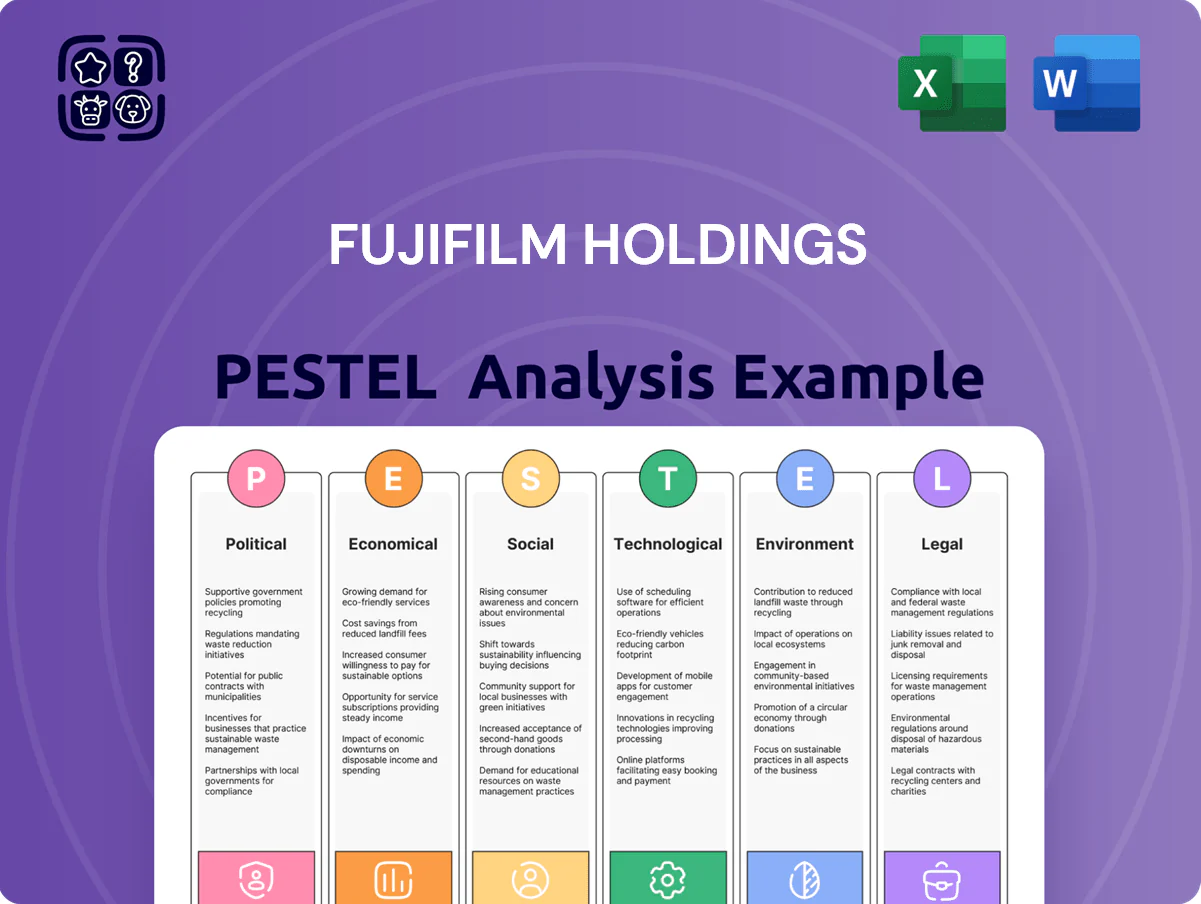

FUJIFILM Holdings PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE Analysis of FUJIFILM Holdings reveals how political regulation, shifting economic cycles, rapid technological innovation, social trends toward healthcare and imaging, and tightening environmental laws together shape strategic risk and opportunity; get the full, actionable report to inform investments, strategy, or competitive analysis—download the complete version now.

Political factors

Geopolitical Trade Relations

Fujifilm must navigate complex trade dynamics between Japan, the United States, and China, especially for semiconductor materials and advanced optics where cross-border sales accounted for roughly 45% of Materials segment revenue in FY2024 (¥232bn).

Recent US export controls on high-tech components constrain distribution of specialized photoresists and CMP pads, raising compliance costs estimated at several billion yen annually for industry peers in 2024.

Management closely monitors geopolitical tensions to mitigate risks of sudden tariff hikes or supply chain blockades that could compress segment operating margin (Materials margin was 12.8% in FY2024) and disrupt global chip manufacturing customers.

Government Healthcare Subsidies

Fujifilm benefits from Japan’s and the US’s targeted subsidies—Japan’s 2024 Industrial Competitiveness grants and the US CHIPS+Biomanufacturing initiatives, which allocated over ¥100 billion and $2.5 billion respectively in 2024–2025—to expand CDMO capacity for vaccines and cell therapies; public funding has supported Fujifilm Diosynth Biotechnologies’ capital projects, helping sustain a competitive edge versus global peers in contract biomanufacturing.

Regulatory Healthcare Policies

Stability in Southeast Asia

As Fujifilm shifts more manufacturing to Southeast Asia, political stability is critical for continuity; in 2024 about 28% of Asia-based manufacturing capacity moved toward Vietnam, Thailand and Malaysia.

Political unrest or abrupt labor-law changes can disrupt imaging and document production lines, risking supply delays that could affect FY2024 revenues (¥2.6 trillion imaging & healthcare combined).

Diversified hubs across multiple Southeast Asian countries hedge localized volatility, lowering country-concentration risk and protecting output and margins.

- ~28% of Asia capacity relocated to SE Asia by 2024

- FY2024 imaging & healthcare revenue ~¥2.6 trillion

- Diversification reduces single-country operational risk

Environmental Policy Integration

Strict mandates on carbon neutrality and plastic reduction push Fujifilm to speed sustainable manufacturing; Japan targets net-zero by 2050 and the company reported a 21% reduction in CO2 intensity from 2019–2023, prompting capex toward low-carbon tech.

Political pressure from the Paris Agreement and local green deals forces large investments: Fujifilm’s 2024 sustainability roadmap includes JPY 50 billion planned green investments through 2027 for energy-efficient infrastructure.

Noncompliance risks heavy fines and lost government contracts; in 2022 Japan and EU procurement rules tightened green criteria, making alignment critical to protect revenues—public-sector sales exposure could exceed several hundred million USD annually.

- 21% CO2 intensity cut (2019–2023)

- JPY 50 billion planned green capex to 2027

- Net-zero target alignment required by 2050

- Procurement risk: potential loss of public-sector contracts worth hundreds of millions USD

Fujifilm: Subsidies and SE Asia shift cushion export-control risks in materials & imaging

Geopolitical export controls and trade tensions (US-China-Japan) affect Fujifilm’s materials and optics (Materials: ¥232bn, 45% cross-border, margin 12.8% FY2024); subsidies (Japan ¥100bn 2024, US CHIPS $2.5bn 2024–25) aid CDMO expansion; healthcare reimbursement shifts influence imaging demand (Imaging & healthcare revenue ¥2.6T FY2024); SE Asia relocation (~28% capacity) mitigates country risk.

| Metric | Value |

|---|---|

| Materials revenue FY2024 | ¥232bn |

| Materials cross-border share | 45% |

| Materials margin FY2024 | 12.8% |

| Imaging & healthcare revenue FY2024 | ¥2.6T |

| SE Asia capacity by 2024 | ~28% |

| Japan industrial grants 2024 | ¥100bn |

| US CHIPS funding 2024–25 | $2.5bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect FUJIFILM Holdings, with data-backed trends and industry-specific examples to identify risks, opportunities, and strategic responses for executives, investors, and advisors.

A concise, neatly organized FUJIFILM Holdings PESTLE summary that’s easy to drop into presentations, share across teams, and adapt with region- or business-specific notes to streamline risk discussions and strategic planning.

Economic factors

Currency Exchange Rate Volatility

As a Japanese multinational, FUJIFILM (FY2024 revenue ¥3.1 trillion overseas share ~55%) is sensitive to JPY/USD and JPY/EUR swings; a weaker yen improves export competitiveness but raises imported raw material costs, pressuring domestic margins. In FY2023 FX translation reduced operating profit by about ¥24.5 billion; management uses forward contracts, FX options and natural hedges—hedge coverage often exceeds 60% of forecasted exposure—to stabilize consolidated results.

Global Inflationary Pressures

Rising energy and raw-material costs, including silver and specialty chemicals, squeezed Fujifilm’s margins in 2024—silver prices rose ~15% YoY and average global industrial energy prices were up ~20%—forcing selective price increases across imaging and materials science lines while risking share loss. Management reported R&D and capital spending cuts in some regions as corporate capex weakened in late 2024, with global capex growth slowing to ~2% in 2024, dampening demand for innovation services.

Healthcare Spending Trends

The economic health of governments and insurers directly shapes investment in diagnostic infrastructure; global healthcare spending reached about $10.4 trillion in 2024, supporting demand for upgrades. In growth periods Fujifilm sees higher adoption of digital radiography and endoscopy—global imaging market CAGR ~6% (2024–2029). Conversely, downturns prompt deferred maintenance and delayed hardware upgrades in developed and emerging markets, reducing near-term capital purchases.

Interest Rate Environments

Global shifts in interest rates affect Fujifilm's cost of capital for CDMO expansion; Fed hikes to ~5.25–5.50% in 2023–24 raised borrowing costs for capital-intensive projects.

Higher rates can delay acquisitions and new biopharma facility builds, raising weighted average cost of capital and project payback periods.

Fujifilm's strong balance sheet—net cash/low leverage and ¥671.8 billion cash & equivalents at FY2023—helps fund growth when credit tightens.

- Fed rate ~5.25–5.50% (2023–24) increasing borrowing costs

- FY2023 cash & equivalents ¥671.8 billion

- CDMO expansion capital intensity raises sensitivity to rates

Consumer Discretionary Spending

Consumer discretionary spending directly affects demand for Fujifilm’s Instax and premium X-series cameras; global disposable income drops correlate with lower sales of hobbyist and luxury imaging goods—e.g., global consumer spending fell in 2023 with OECD real disposable income down 0.5% in several major markets, pressuring discretionary categories.

Fujifilm counters cyclicality through continuous product innovation, ecosystem services (Instax film and accessories) and loyalty programs, helping sustain revenue; imaging segment revenue was ¥259.5bn in FY2024 H1, showing resilience despite economic pressure.

- High sensitivity to disposable income—sales dip in recessions

- Instax ecosystem creates recurring revenue (film/accessories)

- FY2024 H1 imaging revenue ¥259.5bn signals resilience

Weak JPY boosts exports but costs rise—FY23 FX hit ¥24.5bn; cash ¥671.8bn cushions risk

FX swings (weaker JPY boosts exports but raises import costs; FY2023 FX hit OP ~¥24.5bn; hedge coverage >60%), rising input/energy costs (silver +15% YoY, energy +20% in 2024) pressured margins, higher rates (Fed ~5.25–5.50%) increased WACC delaying CDMO capex; strong balance sheet (cash ¥671.8bn FY2023) cushions risk; imaging revenue ¥259.5bn H1 FY2024 showed resilience.

| Metric | Value |

|---|---|

| Cash | ¥671.8bn |

| Imaging Rev H1 FY2024 | ¥259.5bn |

| FX OP Impact FY2023 | ¥24.5bn |

| Silver change 2024 | +15% YoY |

| Fed rate | ~5.25–5.50% |

What You See Is What You Get

FUJIFILM Holdings PESTLE Analysis

The preview shown here is the exact FUJIFILM Holdings PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

This is a real screenshot of the product you’re buying; the content and structure visible here match the downloadable file you’ll get immediately after payment.

No placeholders or teasers—what you see is the finished, comprehensive PESTLE report you’ll own after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE Analysis of FUJIFILM Holdings reveals how political regulation, shifting economic cycles, rapid technological innovation, social trends toward healthcare and imaging, and tightening environmental laws together shape strategic risk and opportunity; get the full, actionable report to inform investments, strategy, or competitive analysis—download the complete version now.

Political factors

Geopolitical Trade Relations

Fujifilm must navigate complex trade dynamics between Japan, the United States, and China, especially for semiconductor materials and advanced optics where cross-border sales accounted for roughly 45% of Materials segment revenue in FY2024 (¥232bn).

Recent US export controls on high-tech components constrain distribution of specialized photoresists and CMP pads, raising compliance costs estimated at several billion yen annually for industry peers in 2024.

Management closely monitors geopolitical tensions to mitigate risks of sudden tariff hikes or supply chain blockades that could compress segment operating margin (Materials margin was 12.8% in FY2024) and disrupt global chip manufacturing customers.

Government Healthcare Subsidies

Fujifilm benefits from Japan’s and the US’s targeted subsidies—Japan’s 2024 Industrial Competitiveness grants and the US CHIPS+Biomanufacturing initiatives, which allocated over ¥100 billion and $2.5 billion respectively in 2024–2025—to expand CDMO capacity for vaccines and cell therapies; public funding has supported Fujifilm Diosynth Biotechnologies’ capital projects, helping sustain a competitive edge versus global peers in contract biomanufacturing.

Regulatory Healthcare Policies

Stability in Southeast Asia

As Fujifilm shifts more manufacturing to Southeast Asia, political stability is critical for continuity; in 2024 about 28% of Asia-based manufacturing capacity moved toward Vietnam, Thailand and Malaysia.

Political unrest or abrupt labor-law changes can disrupt imaging and document production lines, risking supply delays that could affect FY2024 revenues (¥2.6 trillion imaging & healthcare combined).

Diversified hubs across multiple Southeast Asian countries hedge localized volatility, lowering country-concentration risk and protecting output and margins.

- ~28% of Asia capacity relocated to SE Asia by 2024

- FY2024 imaging & healthcare revenue ~¥2.6 trillion

- Diversification reduces single-country operational risk

Environmental Policy Integration

Strict mandates on carbon neutrality and plastic reduction push Fujifilm to speed sustainable manufacturing; Japan targets net-zero by 2050 and the company reported a 21% reduction in CO2 intensity from 2019–2023, prompting capex toward low-carbon tech.

Political pressure from the Paris Agreement and local green deals forces large investments: Fujifilm’s 2024 sustainability roadmap includes JPY 50 billion planned green investments through 2027 for energy-efficient infrastructure.

Noncompliance risks heavy fines and lost government contracts; in 2022 Japan and EU procurement rules tightened green criteria, making alignment critical to protect revenues—public-sector sales exposure could exceed several hundred million USD annually.

- 21% CO2 intensity cut (2019–2023)

- JPY 50 billion planned green capex to 2027

- Net-zero target alignment required by 2050

- Procurement risk: potential loss of public-sector contracts worth hundreds of millions USD

Fujifilm: Subsidies and SE Asia shift cushion export-control risks in materials & imaging

Geopolitical export controls and trade tensions (US-China-Japan) affect Fujifilm’s materials and optics (Materials: ¥232bn, 45% cross-border, margin 12.8% FY2024); subsidies (Japan ¥100bn 2024, US CHIPS $2.5bn 2024–25) aid CDMO expansion; healthcare reimbursement shifts influence imaging demand (Imaging & healthcare revenue ¥2.6T FY2024); SE Asia relocation (~28% capacity) mitigates country risk.

| Metric | Value |

|---|---|

| Materials revenue FY2024 | ¥232bn |

| Materials cross-border share | 45% |

| Materials margin FY2024 | 12.8% |

| Imaging & healthcare revenue FY2024 | ¥2.6T |

| SE Asia capacity by 2024 | ~28% |

| Japan industrial grants 2024 | ¥100bn |

| US CHIPS funding 2024–25 | $2.5bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect FUJIFILM Holdings, with data-backed trends and industry-specific examples to identify risks, opportunities, and strategic responses for executives, investors, and advisors.

A concise, neatly organized FUJIFILM Holdings PESTLE summary that’s easy to drop into presentations, share across teams, and adapt with region- or business-specific notes to streamline risk discussions and strategic planning.

Economic factors

Currency Exchange Rate Volatility

As a Japanese multinational, FUJIFILM (FY2024 revenue ¥3.1 trillion overseas share ~55%) is sensitive to JPY/USD and JPY/EUR swings; a weaker yen improves export competitiveness but raises imported raw material costs, pressuring domestic margins. In FY2023 FX translation reduced operating profit by about ¥24.5 billion; management uses forward contracts, FX options and natural hedges—hedge coverage often exceeds 60% of forecasted exposure—to stabilize consolidated results.

Global Inflationary Pressures

Rising energy and raw-material costs, including silver and specialty chemicals, squeezed Fujifilm’s margins in 2024—silver prices rose ~15% YoY and average global industrial energy prices were up ~20%—forcing selective price increases across imaging and materials science lines while risking share loss. Management reported R&D and capital spending cuts in some regions as corporate capex weakened in late 2024, with global capex growth slowing to ~2% in 2024, dampening demand for innovation services.

Healthcare Spending Trends

The economic health of governments and insurers directly shapes investment in diagnostic infrastructure; global healthcare spending reached about $10.4 trillion in 2024, supporting demand for upgrades. In growth periods Fujifilm sees higher adoption of digital radiography and endoscopy—global imaging market CAGR ~6% (2024–2029). Conversely, downturns prompt deferred maintenance and delayed hardware upgrades in developed and emerging markets, reducing near-term capital purchases.

Interest Rate Environments

Global shifts in interest rates affect Fujifilm's cost of capital for CDMO expansion; Fed hikes to ~5.25–5.50% in 2023–24 raised borrowing costs for capital-intensive projects.

Higher rates can delay acquisitions and new biopharma facility builds, raising weighted average cost of capital and project payback periods.

Fujifilm's strong balance sheet—net cash/low leverage and ¥671.8 billion cash & equivalents at FY2023—helps fund growth when credit tightens.

- Fed rate ~5.25–5.50% (2023–24) increasing borrowing costs

- FY2023 cash & equivalents ¥671.8 billion

- CDMO expansion capital intensity raises sensitivity to rates

Consumer Discretionary Spending

Consumer discretionary spending directly affects demand for Fujifilm’s Instax and premium X-series cameras; global disposable income drops correlate with lower sales of hobbyist and luxury imaging goods—e.g., global consumer spending fell in 2023 with OECD real disposable income down 0.5% in several major markets, pressuring discretionary categories.

Fujifilm counters cyclicality through continuous product innovation, ecosystem services (Instax film and accessories) and loyalty programs, helping sustain revenue; imaging segment revenue was ¥259.5bn in FY2024 H1, showing resilience despite economic pressure.

- High sensitivity to disposable income—sales dip in recessions

- Instax ecosystem creates recurring revenue (film/accessories)

- FY2024 H1 imaging revenue ¥259.5bn signals resilience

Weak JPY boosts exports but costs rise—FY23 FX hit ¥24.5bn; cash ¥671.8bn cushions risk

FX swings (weaker JPY boosts exports but raises import costs; FY2023 FX hit OP ~¥24.5bn; hedge coverage >60%), rising input/energy costs (silver +15% YoY, energy +20% in 2024) pressured margins, higher rates (Fed ~5.25–5.50%) increased WACC delaying CDMO capex; strong balance sheet (cash ¥671.8bn FY2023) cushions risk; imaging revenue ¥259.5bn H1 FY2024 showed resilience.

| Metric | Value |

|---|---|

| Cash | ¥671.8bn |

| Imaging Rev H1 FY2024 | ¥259.5bn |

| FX OP Impact FY2023 | ¥24.5bn |

| Silver change 2024 | +15% YoY |

| Fed rate | ~5.25–5.50% |

What You See Is What You Get

FUJIFILM Holdings PESTLE Analysis

The preview shown here is the exact FUJIFILM Holdings PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

This is a real screenshot of the product you’re buying; the content and structure visible here match the downloadable file you’ll get immediately after payment.

No placeholders or teasers—what you see is the finished, comprehensive PESTLE report you’ll own after checkout.