Holmen PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and sustainability trends are reshaping Holmen’s prospects in our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable context. Purchase the full PESTLE Analysis to access detailed risk assessments, regulatory impacts, and market opportunities you can use in boardroom decks or investment models. Buy now for immediate, editable insights.

Political factors

European Union Forest Strategy 2030

The EU Forest Strategy 2030 pressures Swedish forestry by prioritizing biodiversity and carbon sinks, threatening Holmen’s 2024 roundwood sales (Sweden exported ~36 million m3 in 2023) as harvesting restrictions rise.

Harmonization directives aim to standardize management across the EU, creating regulatory divergence with Sweden’s intensive logging models that underpin Holmen’s SEK 14.6bn 2024 net sales in forest products.

Holmen must increase policy engagement and report ecosystem services value—EU funding for biodiversity reached €7.5bn in 2024—to ensure forests’ economic contributions are recognized alongside environmental goals.

Swedish Land Use and Rights Policies

Political debates over Sami land rights and wind power sit at the center of Holmen’s Swedish operations; contested permits have delayed multiple projects, with Sweden reporting a 2024 target to add 20 TWh of wind by 2030, intensifying land-use conflicts.

Energy Security and Subsidy Frameworks

The Swedish government's push for energy independence has expanded subsidies for renewables, with 2024 support schemes allocating roughly SEK 15–20 billion to wind and hydro projects; Holmen’s ~1.1 TWh of annual in-house generation benefits from these policies, but shifts toward solar or altered grid-connection priorities could reduce margins. Active lobbying ensures Holmen seeks fair compensation and protection for its energy contributions to the national grid.

International Trade and Geopolitical Stability

As an export-oriented group, Holmen is exposed to trade barriers and geopolitical tensions that can hinder shipments of wood products and paperboard; in 2024 exports accounted for about 60% of net sales (SEK 20.8bn of SEK 34.6bn), amplifying vulnerability to tariffs and logistics disruption.

Political instability in Eastern Europe and EU trade disputes with key partners risk supply-chain interruptions and input-cost spikes; 2024 saw shipping rates and timber prices fluctuate ~15–25%, impacting margins.

Holmen must monitor diplomatic shifts to mitigate tariff risks and restricted market access in Asia and North America, where demand represents a significant share of export volumes.

- 2024 exports ≈60% of net sales (SEK 20.8bn of 34.6bn)

- Shipping/timber price swings ~15–25% in 2024

- High exposure to Asia/North America export markets

National Environmental Permitting Processes

The Swedish government’s 2024 target to halve environmental permitting times for energy projects could shorten approvals for Holmen’s wind and mill upgrades, but local NIMBY-driven zoning restrictions rose 12% in 2023, risking site delays.

Holmen’s SEK 6.5bn capex plan for 2024–2026 depends on predictable permitting to secure long-term forest and energy returns; regulatory volatility raises discount-rate and project-timeline risk.

- 2024 policy: aim −50% permit time

- Local zoning disputes +12% (2023)

- Holmen capex SEK 6.5bn (2024–26)

EU Forest Rules, Energy Policy Clash Threaten Holmen: Exports & Capex Under Pressure

EU Forest Strategy 2030 and harmonization increase harvesting restrictions, threatening Holmen’s roundwood sales amid Sweden’s 2023 exports ~36m m3; 2024 exports ≈60% of net sales (SEK 20.8bn of 34.6bn). Energy policies (SEK 15–20bn 2024 renewables support) aid Holmen’s ~1.1 TWh generation but permit volatility (target −50% time) and local zoning +12% risk capex SEK 6.5bn (2024–26).

| Metric | Value (2023–24) |

|---|---|

| Sweden roundwood exports | ~36m m3 (2023) |

| Exports share | 60% (SEK 20.8bn/34.6bn 2024) |

| Holmen generation | ~1.1 TWh |

| Renewables support | SEK 15–20bn (2024) |

| Capex plan | SEK 6.5bn (2024–26) |

What is included in the product

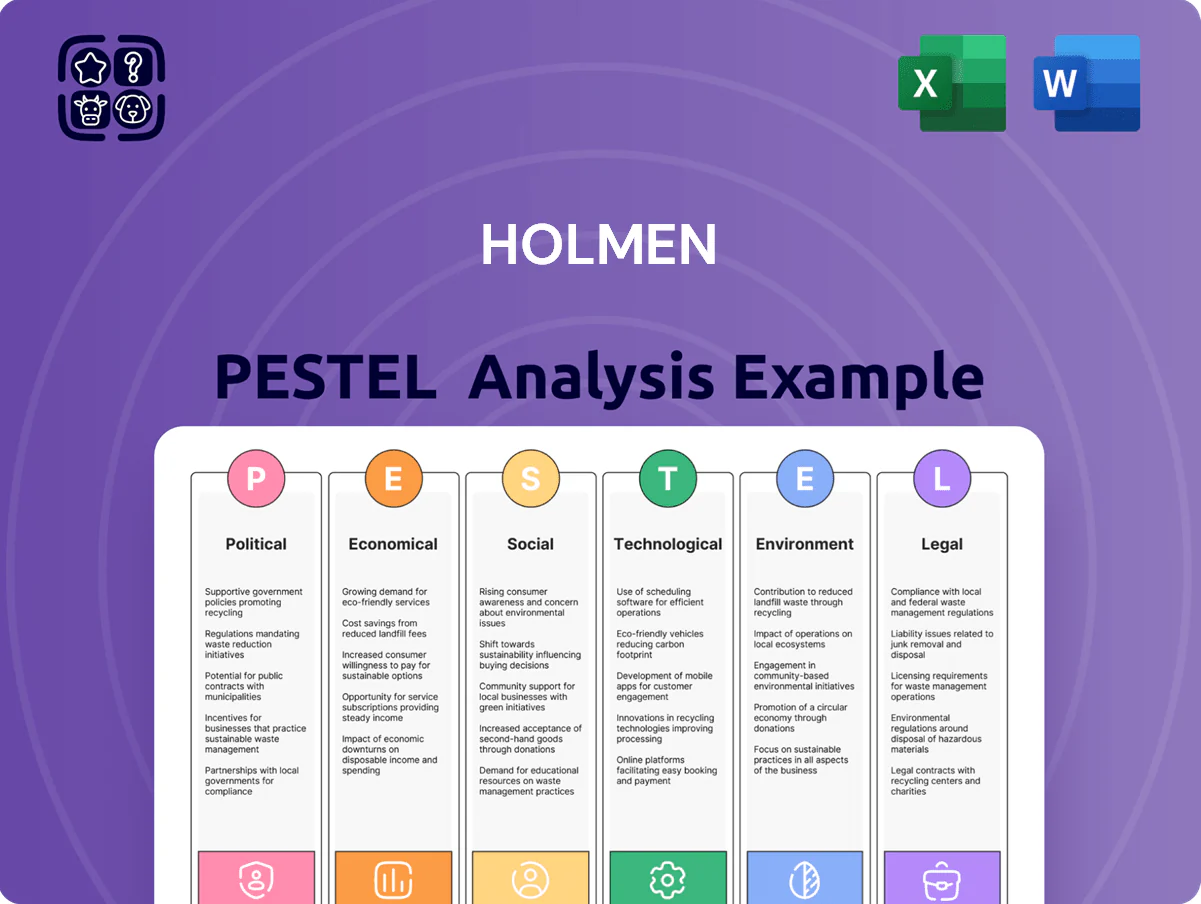

Explores how external macro-environmental factors uniquely affect Holmen across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Provides a concise, PESTLE-segmented summary of Holmen’s external risks and opportunities, ready to drop into presentations or planning sessions for quick team alignment.

Economic factors

Interest Rate Environment and Capital Costs

As of late 2025, rising global rates—Swedish 10-year government yield near 3.8% and Riksbank policy at 4.0%—push Holmen's financing costs higher, increasing capex expenses for energy projects and sawmill modernization and raising discount rates applied to biological forest asset valuations.

Currency Exchange Rate Volatility

Holmen earns ~40–50% of revenue in EUR and USD while major costs remain in SEK; a 10% SEK depreciation vs EUR/USD raised reported operating profit by roughly SEK 200–400m in 2023–2024 scenarios per company sensitivity analyses.

Construction Sector Demand Cycles

The economic health of the European construction industry directly dictates demand for Holmen’s sawn timber and joinery products; EU construction output fell 2.4% YoY in H1 2025, reducing near-term orders for structural timber.

Slowdowns in residential or commercial building create inventory surpluses and pressure timber prices—European softwood pulpwood prices dropped ~8% in 2024–25, squeezing margins.

Holmen’s push into value-added products (e.g., CLT, planed timber) and a 2024–25 target to raise processed-wood sales share to ~40% provides buffer against raw commodity cyclicality and steadier cash flows.

Energy Market Pricing and Revenue

Holmen’s large hydro and wind portfolio links earnings to Nord Pool price swings; average Nordic system price rose to about EUR 61/MWh in 2024 versus EUR 49/MWh in 2023, boosting energy segment margins and 2024 energy EBITDA growth reported by Holmen.

Higher power prices increase input costs for paper and paperboard mills, but Holmen disclosed net power generation of roughly 6.5 TWh in 2024, which partly offsets volatility and raises group cash flow resilience.

- Nordic system price ~EUR 61/MWh (2024)

- 2024 Holmen net generation ~6.5 TWh

- Energy segment drove EBITDA uplift in 2024

- Acts as a natural hedge vs peers without own generation

Inflationary Pressure on Operational Costs

Persistent inflation in labor, logistics and inputs like chemicals and spare parts erodes Holmen's cost-efficiency; Swedish CPI rose ~10.8% 2022–2023 while producer and input price inflation remained elevated into 2024, pressuring margins.

Holmen's timber self-sufficiency limits raw-wood exposure, but rising transport costs and global supply-chain inflation—container freight up >50% vs pre‑pandemic peaks in 2021–23—fuel input cost risk through 2026.

Operational excellence, productivity gains and selective price increases in paperboard and forest products are needed to protect operating margin targets (Holmen reported 2023 operating margin ~8–9%); failure to offset input inflation could compress margins further.

- Swedish CPI ~10.8% (2022–23)

- Container freight >50% above pre‑pandemic peaks in 2021–23

- Holmen 2023 operating margin ~8–9%

Holmen faces rate, FX and pulpheadwinds; power generation and processed wood provide buffers

Rising rates (Sweden 10y ~3.8%, Riksbank 4.0%) and EUR/USD exposure (40–50% revenue) raise financing costs and FX sensitivity; EU construction weakness (output -2.4% H1 2025) and softwood pulpwood price decline (~8% 2024–25) pressure timber demand and margins, while Holmen’s ~6.5 TWh generation (2024) and move to ~40% processed-wood sales buffer volatility.

| Metric | Value |

|---|---|

| Sweden 10y | ~3.8% |

| Riksbank policy | 4.0% |

| Net generation (2024) | ~6.5 TWh |

| Processed-wood target | ~40% |

Preview Before You Purchase

Holmen PESTLE Analysis

The preview shown here is the exact Holmen PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and sustainability trends are reshaping Holmen’s prospects in our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable context. Purchase the full PESTLE Analysis to access detailed risk assessments, regulatory impacts, and market opportunities you can use in boardroom decks or investment models. Buy now for immediate, editable insights.

Political factors

European Union Forest Strategy 2030

The EU Forest Strategy 2030 pressures Swedish forestry by prioritizing biodiversity and carbon sinks, threatening Holmen’s 2024 roundwood sales (Sweden exported ~36 million m3 in 2023) as harvesting restrictions rise.

Harmonization directives aim to standardize management across the EU, creating regulatory divergence with Sweden’s intensive logging models that underpin Holmen’s SEK 14.6bn 2024 net sales in forest products.

Holmen must increase policy engagement and report ecosystem services value—EU funding for biodiversity reached €7.5bn in 2024—to ensure forests’ economic contributions are recognized alongside environmental goals.

Swedish Land Use and Rights Policies

Political debates over Sami land rights and wind power sit at the center of Holmen’s Swedish operations; contested permits have delayed multiple projects, with Sweden reporting a 2024 target to add 20 TWh of wind by 2030, intensifying land-use conflicts.

Energy Security and Subsidy Frameworks

The Swedish government's push for energy independence has expanded subsidies for renewables, with 2024 support schemes allocating roughly SEK 15–20 billion to wind and hydro projects; Holmen’s ~1.1 TWh of annual in-house generation benefits from these policies, but shifts toward solar or altered grid-connection priorities could reduce margins. Active lobbying ensures Holmen seeks fair compensation and protection for its energy contributions to the national grid.

International Trade and Geopolitical Stability

As an export-oriented group, Holmen is exposed to trade barriers and geopolitical tensions that can hinder shipments of wood products and paperboard; in 2024 exports accounted for about 60% of net sales (SEK 20.8bn of SEK 34.6bn), amplifying vulnerability to tariffs and logistics disruption.

Political instability in Eastern Europe and EU trade disputes with key partners risk supply-chain interruptions and input-cost spikes; 2024 saw shipping rates and timber prices fluctuate ~15–25%, impacting margins.

Holmen must monitor diplomatic shifts to mitigate tariff risks and restricted market access in Asia and North America, where demand represents a significant share of export volumes.

- 2024 exports ≈60% of net sales (SEK 20.8bn of 34.6bn)

- Shipping/timber price swings ~15–25% in 2024

- High exposure to Asia/North America export markets

National Environmental Permitting Processes

The Swedish government’s 2024 target to halve environmental permitting times for energy projects could shorten approvals for Holmen’s wind and mill upgrades, but local NIMBY-driven zoning restrictions rose 12% in 2023, risking site delays.

Holmen’s SEK 6.5bn capex plan for 2024–2026 depends on predictable permitting to secure long-term forest and energy returns; regulatory volatility raises discount-rate and project-timeline risk.

- 2024 policy: aim −50% permit time

- Local zoning disputes +12% (2023)

- Holmen capex SEK 6.5bn (2024–26)

EU Forest Rules, Energy Policy Clash Threaten Holmen: Exports & Capex Under Pressure

EU Forest Strategy 2030 and harmonization increase harvesting restrictions, threatening Holmen’s roundwood sales amid Sweden’s 2023 exports ~36m m3; 2024 exports ≈60% of net sales (SEK 20.8bn of 34.6bn). Energy policies (SEK 15–20bn 2024 renewables support) aid Holmen’s ~1.1 TWh generation but permit volatility (target −50% time) and local zoning +12% risk capex SEK 6.5bn (2024–26).

| Metric | Value (2023–24) |

|---|---|

| Sweden roundwood exports | ~36m m3 (2023) |

| Exports share | 60% (SEK 20.8bn/34.6bn 2024) |

| Holmen generation | ~1.1 TWh |

| Renewables support | SEK 15–20bn (2024) |

| Capex plan | SEK 6.5bn (2024–26) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Holmen across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Provides a concise, PESTLE-segmented summary of Holmen’s external risks and opportunities, ready to drop into presentations or planning sessions for quick team alignment.

Economic factors

Interest Rate Environment and Capital Costs

As of late 2025, rising global rates—Swedish 10-year government yield near 3.8% and Riksbank policy at 4.0%—push Holmen's financing costs higher, increasing capex expenses for energy projects and sawmill modernization and raising discount rates applied to biological forest asset valuations.

Currency Exchange Rate Volatility

Holmen earns ~40–50% of revenue in EUR and USD while major costs remain in SEK; a 10% SEK depreciation vs EUR/USD raised reported operating profit by roughly SEK 200–400m in 2023–2024 scenarios per company sensitivity analyses.

Construction Sector Demand Cycles

The economic health of the European construction industry directly dictates demand for Holmen’s sawn timber and joinery products; EU construction output fell 2.4% YoY in H1 2025, reducing near-term orders for structural timber.

Slowdowns in residential or commercial building create inventory surpluses and pressure timber prices—European softwood pulpwood prices dropped ~8% in 2024–25, squeezing margins.

Holmen’s push into value-added products (e.g., CLT, planed timber) and a 2024–25 target to raise processed-wood sales share to ~40% provides buffer against raw commodity cyclicality and steadier cash flows.

Energy Market Pricing and Revenue

Holmen’s large hydro and wind portfolio links earnings to Nord Pool price swings; average Nordic system price rose to about EUR 61/MWh in 2024 versus EUR 49/MWh in 2023, boosting energy segment margins and 2024 energy EBITDA growth reported by Holmen.

Higher power prices increase input costs for paper and paperboard mills, but Holmen disclosed net power generation of roughly 6.5 TWh in 2024, which partly offsets volatility and raises group cash flow resilience.

- Nordic system price ~EUR 61/MWh (2024)

- 2024 Holmen net generation ~6.5 TWh

- Energy segment drove EBITDA uplift in 2024

- Acts as a natural hedge vs peers without own generation

Inflationary Pressure on Operational Costs

Persistent inflation in labor, logistics and inputs like chemicals and spare parts erodes Holmen's cost-efficiency; Swedish CPI rose ~10.8% 2022–2023 while producer and input price inflation remained elevated into 2024, pressuring margins.

Holmen's timber self-sufficiency limits raw-wood exposure, but rising transport costs and global supply-chain inflation—container freight up >50% vs pre‑pandemic peaks in 2021–23—fuel input cost risk through 2026.

Operational excellence, productivity gains and selective price increases in paperboard and forest products are needed to protect operating margin targets (Holmen reported 2023 operating margin ~8–9%); failure to offset input inflation could compress margins further.

- Swedish CPI ~10.8% (2022–23)

- Container freight >50% above pre‑pandemic peaks in 2021–23

- Holmen 2023 operating margin ~8–9%

Holmen faces rate, FX and pulpheadwinds; power generation and processed wood provide buffers

Rising rates (Sweden 10y ~3.8%, Riksbank 4.0%) and EUR/USD exposure (40–50% revenue) raise financing costs and FX sensitivity; EU construction weakness (output -2.4% H1 2025) and softwood pulpwood price decline (~8% 2024–25) pressure timber demand and margins, while Holmen’s ~6.5 TWh generation (2024) and move to ~40% processed-wood sales buffer volatility.

| Metric | Value |

|---|---|

| Sweden 10y | ~3.8% |

| Riksbank policy | 4.0% |

| Net generation (2024) | ~6.5 TWh |

| Processed-wood target | ~40% |

Preview Before You Purchase

Holmen PESTLE Analysis

The preview shown here is the exact Holmen PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.