Hologic Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

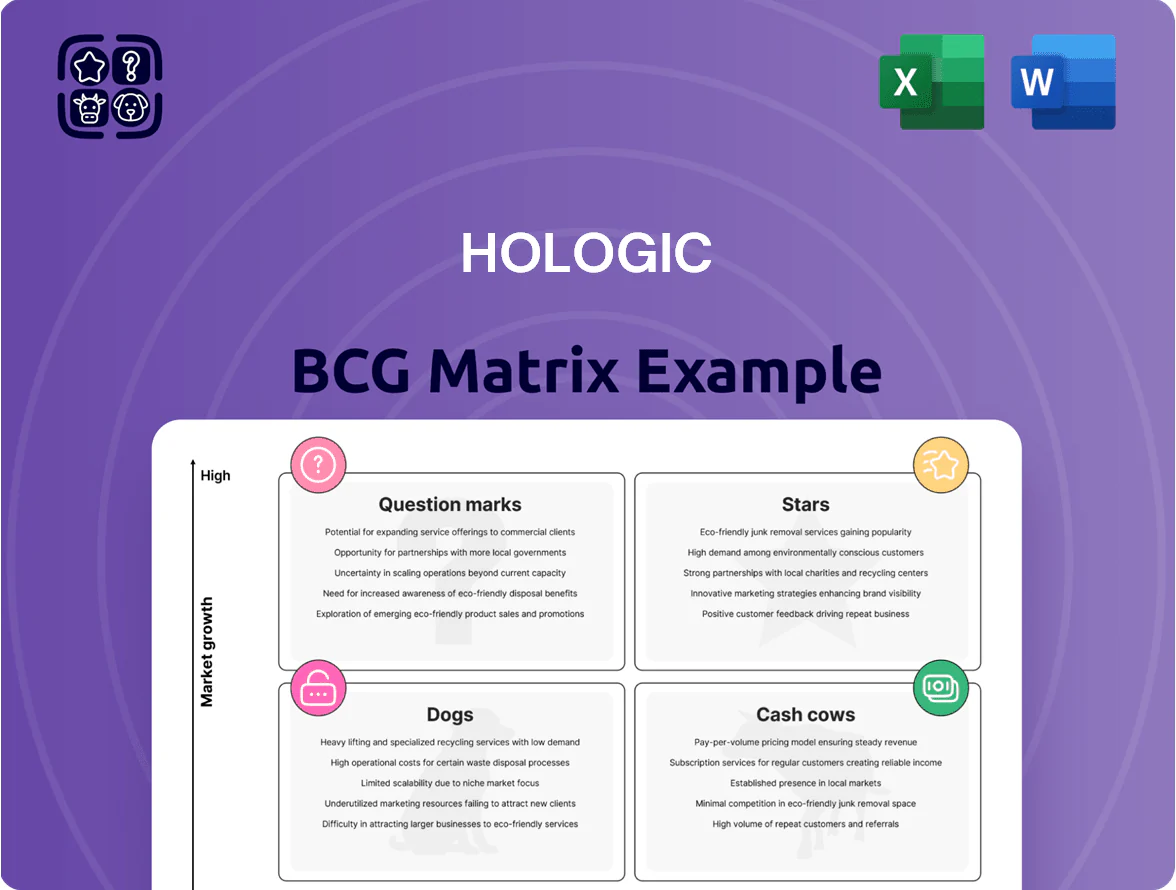

Hologic’s preliminary BCG Matrix highlights which diagnostic and surgical product lines are driving growth and which may be underperforming amid shifting healthcare demands. This snapshot helps spot potential Stars and Cash Cows, but the full BCG Matrix delivers quadrant-level placements, revenue shares, and tactical recommendations. Purchase the complete report for a Word + Excel package with actionable strategy, visual maps, and data-backed guidance to inform investment and portfolio decisions.

Stars

Molecular Diagnostics Fusion Assays

The Panther Fusion system is Hologic’s high-growth engine in molecular diagnostics, driving a projected $400–450M in assay revenue in FY2025 and capturing roughly 12–15% of the global molecular respiratory/GI testing market by Q4 2025.

These assays give labs a consolidated platform for respiratory, gastrointestinal, and viral-load testing, reducing workflow steps by ~30% and supporting >1,200 lab installs worldwide as of Nov 2025.

Revenue is strong but R&D spend must stay high—Hologic allocated ~10–12% of diagnostics revenue to R&D in 2024–2025—to monitor variants and counter competitors like Roche and Abbott.

Given double-digit segment growth (estimated 11–14% CAGR 2023–2026) and sustained market dominance, Panther Fusion stands as a Star in Hologic’s BCG matrix.

Genius AI Detection 2.0 Software

Hologic’s Genius AI Detection 2.0 has turned its breast-health hardware into a high-margin software ecosystem, reaching >150 hospital systems and driving recurring subscription revenue that lifted imaging-software margins to ~65% by Q3 2025.

By late 2025 the platform shows a +12% relative cancer-detection improvement in FDA-submitted pivotal studies, cementing its role as a product Stars in the BCG matrix within a >20% CAGR healthcare-AI market.

Hologic keeps first-to-market edge but is spending ~$120–150M through 2026 on multicenter clinical validation and regulatory filings across EU, UK, Japan, and China to protect market share.

International GYN Surgical Portfolio

Hologic’s international surgical business is a Star in the BCG matrix, with year-over-year growth over 20% in Europe and Asia by end-2025 and segment revenue up ~24% YoY to an estimated $560M in 2025.

Devices like the MyoSure tissue removal system are gaining rapid traction as providers shift to minimally invasive gynecologic procedures, driving unit growth of ~30% in key markets.

Hologic leads the category but is boosting global commercial spend—adding ~$75M in 2024–25—to expand market access and training.

If the >20% growth rate persists, these surgical solutions could convert to Cash Cows, generating sustained free cash flow and margin expansion by 2027.

Biotheranostics Oncology Testing

Acquired to boost Hologic’s precision-medicine footprint, Biotheranostics Oncology (Breast Cancer Index) delivered high double-digit revenue growth through 2025, with the personalized oncology market expanding ~18% CAGR 2020–2025 and the test capturing a leading niche share while still reaching only ~10–20% of eligible patients.

This high-share, high-growth asset requires ongoing marketing and clinical validation; it burned cash in 2025 to fund guideline adoption and lab capacity expansion, positioning it as a star needing continued investment to secure long-term dominance.

- High double-digit revenue growth through 2025

- Personalized oncology market ~18% CAGR (2020–2025)

- Test penetration ~10–20% of eligible patients

- High market share in a niche; currently cash-consuming

Digital Cytology Systems

The Genius Digital Diagnostics System pairs high-resolution imaging with deep-learning analysis, driving a shift from manual microscopy to total lab automation in cervical screening. As of late 2025, adoption rose ~45% year-over-year in advanced U.S. and European labs, with Hologic holding an estimated >50% share of installed cytology base—making this upgrade a high-growth Stars segment in the BCG matrix.

The system needs substantial placement support and training—installation and onboarding costs average $150–250k per site—yet is essential for Hologic to defend leadership as diagnostics move digital and automated.

- Adoption +45% YoY (late 2025)

- Hologic installed-base >50%

- Placement/training cost $150–250k/site

- High growth, strategic Stars category

Hologic linchpins: Panther Fusion, Genius AI/Digital, surgical & Biotheranostics surge

Panther Fusion, Genius AI Detection 2.0, surgical devices, Biotheranostics, and Genius Digital Diagnostics are Stars for Hologic—each >20% growth or high-share in fast-growing markets (Panther Fusion $400–450M FY2025; surgical ~$560M 2025; Genius imaging margins ~65%; Biotheranostics penetration 10–20%; Genius Digital adoption +45% YoY).

| Asset | 2025 metric | Growth/Share |

|---|---|---|

| Panther Fusion | $400–450M | 12–15% market share, 11–14% CAGR |

| Surgical | $560M | +24% YoY, >20% regional growth |

| Genius AI | Margins ~65% | 150+ systems, +12% detection |

| Biotheranostics | High double-digit growth | 10–20% penetration, ~18% market CAGR |

| Genius Digital | Installed-base >50% | Adoption +45% YoY, $150–250k/site |

What is included in the product

Comprehensive BCG Matrix review of Hologic’s portfolio with quadrant strategies, investment recommendations, and trend-driven risks and advantages.

One-page Hologic BCG Matrix mapping each business unit into quadrants for quick strategic clarity and stakeholder alignment.

Cash Cows

Aptima Women's Health Assays

The Aptima family of STI assays (Chlamydia, Gonorrhea) on Hologic’s Panther platform is Hologic’s top cash generator, with an installed base of ~17,000 Panther systems globally and Aptima test volumes driving roughly $1.2bn of reagent revenue in 2024.

By end-2025 Aptima holds a dominant share in a mature nucleic-acid amplification test market, delivering gross margins north of 65% and low incremental marketing spend.

That steady, high-volume recurring revenue funds Hologic’s R&D and M&A, covering a large share of annual innovation spend (Hologic spent $420m on R&D in FY2024).

It’s the quintessential Cash Cow: minimal upkeep, high cash conversion, and the primary capital source to grow newer Stars in the portfolio.

Selenia Dimensions 3D Mammography

Hologic’s Selenia Dimensions 3D tomosynthesis remains the gold standard, holding roughly a 40%–50% share of the global digital mammography installed base by 2025 and generating strong recurring revenue from service and software upsells.

With North American 3D hardware market maturation by 2025, new unit growth slowed to low single digits, shifting margin expansion to high-margin service contracts and software subscriptions that now contribute an estimated 60% of unit-level gross profit.

The large installed footprint in hospitals and imaging centers produces massive cash flow—Hologic reported medical imaging recurring revenue rising mid-teens in 2024—so the razor-and-blade model keeps Selenia Dimensions a core cash cow for the firm.

ThinPrep Pap Test

The ThinPrep Pap test remains Hologic’s cash cow, holding roughly 40–50% share of global cervical cytology by 2025 and generating steady revenue near $700–900M annual run‑rate, despite rising primary HPV testing.

It stays standard of care in many regions, needs minimal R&D, and by late 2025 Hologic is milking high margins to fund digital cytology and AI investments, keeping maintenance capex low while preserving strong EBITDA contribution.

NovaSure Endometrial Ablation

NovaSure endometrial ablation is a dominant, well-established brand for heavy menstrual bleeding with strong physician loyalty; by end-2025 the endometrial ablation market is mature and NovaSure remains the preferred choice for many surgeons.

High market share plus streamlined manufacturing drive excellent profit margins—Hologic reported ablative-device gross margins above 55% in 2024—so cash from NovaSure funds higher-growth surgical buys like the 2023 Gynesonics deal.

- Market: mature by 2025

- Brand: high physician loyalty

- Margin: ablative devices >55% gross (2024)

- Use of cash: funds acquisitions (Gynesonics, 2023)

Skeletal Health DXA Systems

Hologic’s skeletal health segment, anchored by DXA (dual-energy X-ray absorptiometry) systems, dominates the mature osteoporosis-diagnosis market with ~35–40% global share in 2025 and limited direct competition from GE and OsteoSys; sales growth is low but stable.

DXA needs minimal capex for marketing and placement; recurring maintenance and software updates keep gross margins healthy, contributing roughly $300–400M annual operating cash flow to Hologic in 2025.

- Market share ~35–40% (2025)

- Annual cash flow contribution ~$300–400M (2025)

- Low investment needs; mature tech

- Stable demand driven by aging populations

High‑margin diagnostics lineup: Aptima, Selenia 3D, ThinPrep, NovaSure, DXA cash generators

Aptima (Panther): ~$1.2B reagent revenue (2024), >65% gross margin, ~17,000 systems; Selenia 3D: 40–50% share, service/software = ~60% unit gross profit; ThinPrep: $700–900M run‑rate, 40–50% share; NovaSure: ablative margins >55% (2024); DXA: 35–40% share, ~$300–400M cash flow (2025).

| Product | 2024–25 | Margin/CF |

|---|---|---|

| Aptima | $1.2B rev; 17,000 systems | >65% |

| Selenia 3D | 40–50% share | 60% unit GP |

| ThinPrep | $700–900M | high |

| NovaSure | market leader | >55% |

| DXA | 35–40% share | $300–400M CF |

Preview = Final Product

Hologic BCG Matrix

The file you're previewing on this page is the final Hologic BCG Matrix you'll receive after purchase—no watermarks, no demo placeholders—just a fully formatted, analysis-ready report tailored for strategic clarity and professional use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Hologic’s preliminary BCG Matrix highlights which diagnostic and surgical product lines are driving growth and which may be underperforming amid shifting healthcare demands. This snapshot helps spot potential Stars and Cash Cows, but the full BCG Matrix delivers quadrant-level placements, revenue shares, and tactical recommendations. Purchase the complete report for a Word + Excel package with actionable strategy, visual maps, and data-backed guidance to inform investment and portfolio decisions.

Stars

Molecular Diagnostics Fusion Assays

The Panther Fusion system is Hologic’s high-growth engine in molecular diagnostics, driving a projected $400–450M in assay revenue in FY2025 and capturing roughly 12–15% of the global molecular respiratory/GI testing market by Q4 2025.

These assays give labs a consolidated platform for respiratory, gastrointestinal, and viral-load testing, reducing workflow steps by ~30% and supporting >1,200 lab installs worldwide as of Nov 2025.

Revenue is strong but R&D spend must stay high—Hologic allocated ~10–12% of diagnostics revenue to R&D in 2024–2025—to monitor variants and counter competitors like Roche and Abbott.

Given double-digit segment growth (estimated 11–14% CAGR 2023–2026) and sustained market dominance, Panther Fusion stands as a Star in Hologic’s BCG matrix.

Genius AI Detection 2.0 Software

Hologic’s Genius AI Detection 2.0 has turned its breast-health hardware into a high-margin software ecosystem, reaching >150 hospital systems and driving recurring subscription revenue that lifted imaging-software margins to ~65% by Q3 2025.

By late 2025 the platform shows a +12% relative cancer-detection improvement in FDA-submitted pivotal studies, cementing its role as a product Stars in the BCG matrix within a >20% CAGR healthcare-AI market.

Hologic keeps first-to-market edge but is spending ~$120–150M through 2026 on multicenter clinical validation and regulatory filings across EU, UK, Japan, and China to protect market share.

International GYN Surgical Portfolio

Hologic’s international surgical business is a Star in the BCG matrix, with year-over-year growth over 20% in Europe and Asia by end-2025 and segment revenue up ~24% YoY to an estimated $560M in 2025.

Devices like the MyoSure tissue removal system are gaining rapid traction as providers shift to minimally invasive gynecologic procedures, driving unit growth of ~30% in key markets.

Hologic leads the category but is boosting global commercial spend—adding ~$75M in 2024–25—to expand market access and training.

If the >20% growth rate persists, these surgical solutions could convert to Cash Cows, generating sustained free cash flow and margin expansion by 2027.

Biotheranostics Oncology Testing

Acquired to boost Hologic’s precision-medicine footprint, Biotheranostics Oncology (Breast Cancer Index) delivered high double-digit revenue growth through 2025, with the personalized oncology market expanding ~18% CAGR 2020–2025 and the test capturing a leading niche share while still reaching only ~10–20% of eligible patients.

This high-share, high-growth asset requires ongoing marketing and clinical validation; it burned cash in 2025 to fund guideline adoption and lab capacity expansion, positioning it as a star needing continued investment to secure long-term dominance.

- High double-digit revenue growth through 2025

- Personalized oncology market ~18% CAGR (2020–2025)

- Test penetration ~10–20% of eligible patients

- High market share in a niche; currently cash-consuming

Digital Cytology Systems

The Genius Digital Diagnostics System pairs high-resolution imaging with deep-learning analysis, driving a shift from manual microscopy to total lab automation in cervical screening. As of late 2025, adoption rose ~45% year-over-year in advanced U.S. and European labs, with Hologic holding an estimated >50% share of installed cytology base—making this upgrade a high-growth Stars segment in the BCG matrix.

The system needs substantial placement support and training—installation and onboarding costs average $150–250k per site—yet is essential for Hologic to defend leadership as diagnostics move digital and automated.

- Adoption +45% YoY (late 2025)

- Hologic installed-base >50%

- Placement/training cost $150–250k/site

- High growth, strategic Stars category

Hologic linchpins: Panther Fusion, Genius AI/Digital, surgical & Biotheranostics surge

Panther Fusion, Genius AI Detection 2.0, surgical devices, Biotheranostics, and Genius Digital Diagnostics are Stars for Hologic—each >20% growth or high-share in fast-growing markets (Panther Fusion $400–450M FY2025; surgical ~$560M 2025; Genius imaging margins ~65%; Biotheranostics penetration 10–20%; Genius Digital adoption +45% YoY).

| Asset | 2025 metric | Growth/Share |

|---|---|---|

| Panther Fusion | $400–450M | 12–15% market share, 11–14% CAGR |

| Surgical | $560M | +24% YoY, >20% regional growth |

| Genius AI | Margins ~65% | 150+ systems, +12% detection |

| Biotheranostics | High double-digit growth | 10–20% penetration, ~18% market CAGR |

| Genius Digital | Installed-base >50% | Adoption +45% YoY, $150–250k/site |

What is included in the product

Comprehensive BCG Matrix review of Hologic’s portfolio with quadrant strategies, investment recommendations, and trend-driven risks and advantages.

One-page Hologic BCG Matrix mapping each business unit into quadrants for quick strategic clarity and stakeholder alignment.

Cash Cows

Aptima Women's Health Assays

The Aptima family of STI assays (Chlamydia, Gonorrhea) on Hologic’s Panther platform is Hologic’s top cash generator, with an installed base of ~17,000 Panther systems globally and Aptima test volumes driving roughly $1.2bn of reagent revenue in 2024.

By end-2025 Aptima holds a dominant share in a mature nucleic-acid amplification test market, delivering gross margins north of 65% and low incremental marketing spend.

That steady, high-volume recurring revenue funds Hologic’s R&D and M&A, covering a large share of annual innovation spend (Hologic spent $420m on R&D in FY2024).

It’s the quintessential Cash Cow: minimal upkeep, high cash conversion, and the primary capital source to grow newer Stars in the portfolio.

Selenia Dimensions 3D Mammography

Hologic’s Selenia Dimensions 3D tomosynthesis remains the gold standard, holding roughly a 40%–50% share of the global digital mammography installed base by 2025 and generating strong recurring revenue from service and software upsells.

With North American 3D hardware market maturation by 2025, new unit growth slowed to low single digits, shifting margin expansion to high-margin service contracts and software subscriptions that now contribute an estimated 60% of unit-level gross profit.

The large installed footprint in hospitals and imaging centers produces massive cash flow—Hologic reported medical imaging recurring revenue rising mid-teens in 2024—so the razor-and-blade model keeps Selenia Dimensions a core cash cow for the firm.

ThinPrep Pap Test

The ThinPrep Pap test remains Hologic’s cash cow, holding roughly 40–50% share of global cervical cytology by 2025 and generating steady revenue near $700–900M annual run‑rate, despite rising primary HPV testing.

It stays standard of care in many regions, needs minimal R&D, and by late 2025 Hologic is milking high margins to fund digital cytology and AI investments, keeping maintenance capex low while preserving strong EBITDA contribution.

NovaSure Endometrial Ablation

NovaSure endometrial ablation is a dominant, well-established brand for heavy menstrual bleeding with strong physician loyalty; by end-2025 the endometrial ablation market is mature and NovaSure remains the preferred choice for many surgeons.

High market share plus streamlined manufacturing drive excellent profit margins—Hologic reported ablative-device gross margins above 55% in 2024—so cash from NovaSure funds higher-growth surgical buys like the 2023 Gynesonics deal.

- Market: mature by 2025

- Brand: high physician loyalty

- Margin: ablative devices >55% gross (2024)

- Use of cash: funds acquisitions (Gynesonics, 2023)

Skeletal Health DXA Systems

Hologic’s skeletal health segment, anchored by DXA (dual-energy X-ray absorptiometry) systems, dominates the mature osteoporosis-diagnosis market with ~35–40% global share in 2025 and limited direct competition from GE and OsteoSys; sales growth is low but stable.

DXA needs minimal capex for marketing and placement; recurring maintenance and software updates keep gross margins healthy, contributing roughly $300–400M annual operating cash flow to Hologic in 2025.

- Market share ~35–40% (2025)

- Annual cash flow contribution ~$300–400M (2025)

- Low investment needs; mature tech

- Stable demand driven by aging populations

High‑margin diagnostics lineup: Aptima, Selenia 3D, ThinPrep, NovaSure, DXA cash generators

Aptima (Panther): ~$1.2B reagent revenue (2024), >65% gross margin, ~17,000 systems; Selenia 3D: 40–50% share, service/software = ~60% unit gross profit; ThinPrep: $700–900M run‑rate, 40–50% share; NovaSure: ablative margins >55% (2024); DXA: 35–40% share, ~$300–400M cash flow (2025).

| Product | 2024–25 | Margin/CF |

|---|---|---|

| Aptima | $1.2B rev; 17,000 systems | >65% |

| Selenia 3D | 40–50% share | 60% unit GP |

| ThinPrep | $700–900M | high |

| NovaSure | market leader | >55% |

| DXA | 35–40% share | $300–400M CF |

Preview = Final Product

Hologic BCG Matrix

The file you're previewing on this page is the final Hologic BCG Matrix you'll receive after purchase—no watermarks, no demo placeholders—just a fully formatted, analysis-ready report tailored for strategic clarity and professional use.