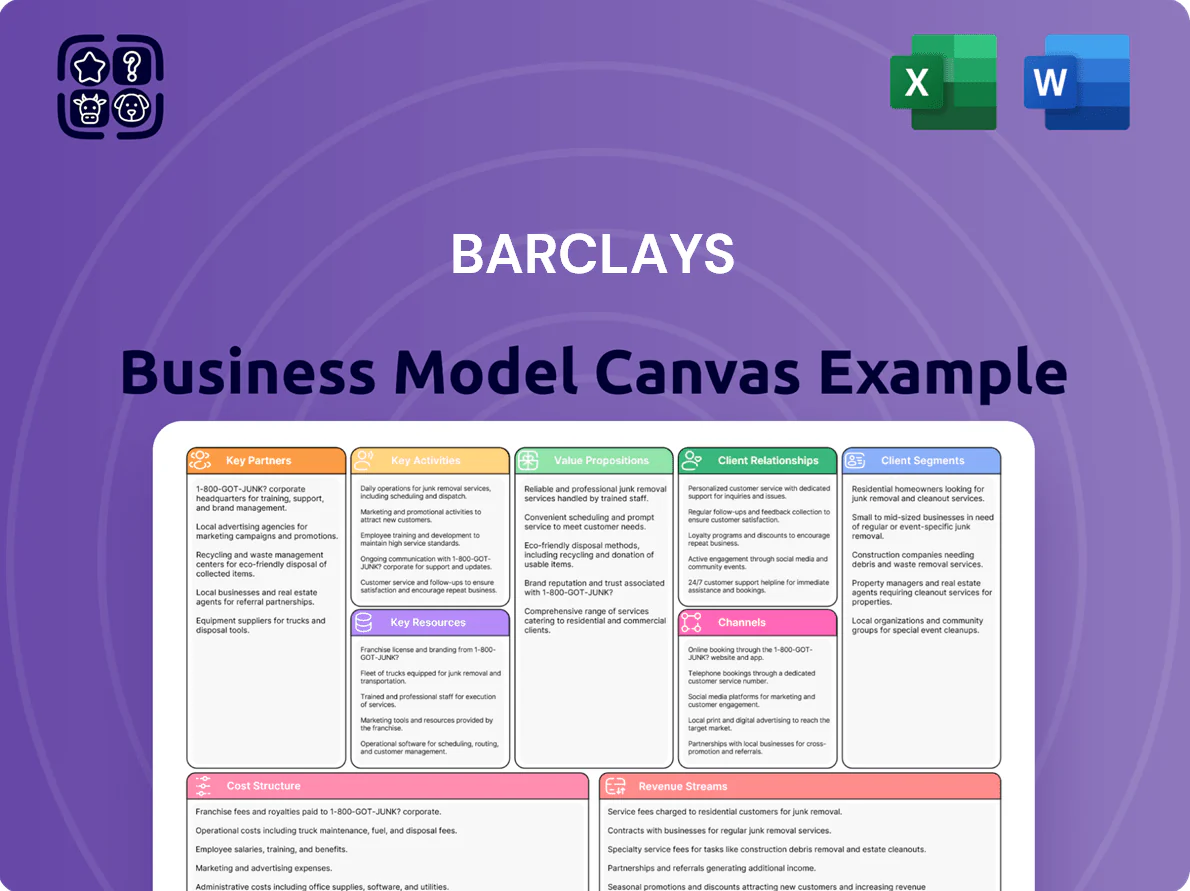

Barclays Business Model Canvas

Barclays Business Model Canvas: Strategic Blueprint for Investors & Strategists

Unlock the full strategic blueprint behind Barclays's business model—this in-depth Business Model Canvas uncovers how the bank creates value, scales revenue streams, and manages costs across retail, corporate, and investment banking; ideal for investors, consultants, and founders seeking actionable, company-specific insights.

Partnerships

Strategic Fintech Collaborations

Barclays partners with fintechs to embed payment and lending tech into its platforms, cutting internal build costs and matching neo-bank agility; by Dec 2025 these alliances covered 45+ fintechs, supporting £3.2bn in digital loan originations in 2024.

Global Payment Network Providers

Barclays retains long-standing links with Visa and Mastercard to power global card acceptance and merchant processing for retail and corporate clients, covering payments in 50+ currencies and >100 markets.

By 2025 those ties include integrated digital wallets and enhanced cross-border real-time rails, supporting instant FX-enabled transfers and reducing settlement times from days to seconds for targeted corridors.

Cloud Infrastructure and Data Partners

Barclays partners with Amazon Web Services and Microsoft Azure to supply the scalable compute for high-frequency trading and analytics, running an estimated 60% of its public-cloud workloads on these platforms by 2024; costs tied to cloud services reached about 0.4% of 2024 operating expenses. By 2025 Barclays is shifting to sovereign-cloud options in the UK/EU to meet stricter data-residency rules and reduce cross-border risk.

Co-Branded Commercial Partners

Barclays partners with retailers, airlines and tech firms like Apple to issue co-branded cards and point-of-sale financing, driving customer acquisition and card balances; co-branded cards accounted for about 22% of Barclays US card receivables (~$28bn) in 2025.

- Access to partner customer bases: millions of users

- Specialized rewards boost retention and spend

- Significant driver of 2025 credit volume and originations

Regulatory and Central Bank Liaisons

As a UK systemically important bank, Barclays engages continuously with the Bank of England and the Financial Conduct Authority, plus global regulators, to meet evolving Basel III/IV capital standards and ring-fencing rules; Barclays reported a CET1 ratio of 13.3% and leverage ratio of 4.4% at Q3 2025, guiding compliance decisions.

This collaborative oversight preserves market trust and helps manage cross-border resolution planning, liquidity buffers, and stress-test outcomes—Barclays held £222bn of high-quality liquid assets (HQLA) at end-2024.

- Regular dialogue with BoE and FCA

- CET1 ratio 13.3% (Q3 2025)

- Leverage ratio 4.4% (Q3 2025)

- HQLA £222bn (end-2024)

- Supports resolution, stress tests, capital planning

Barclays scales fintech partnerships, £3.2bn digital loans and $28bn US co‑brand receivables

Barclays leverages 45+ fintech partners (45 by Dec 2025) and major card networks (Visa, Mastercard) to drive £3.2bn digital loan originations (2024) and ~22% of US card receivables (~$28bn, 2025); public-cloud on AWS/Azure ~60% (2024) while shifting to sovereign-cloud (2025); CET1 13.3% and HQLA £222bn (end-2024).

| Metric | Value |

|---|---|

| Fintech partners | 45+ |

| Digital loans 2024 | £3.2bn |

| US card receivables (co-brand) | $28bn (22%) |

| Cloud share (2024) | ~60% |

| CET1 (Q3 2025) | 13.3% |

| HQLA (end-2024) | £222bn |

What is included in the product

A concise, pre-written Business Model Canvas for Barclays that maps nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned with the bank’s strategy, real-world operations, competitive advantages, SWOT insights, and designed for investor presentations and strategic decision-making.

Condenses Barclays’ strategy into a digestible one-page snapshot with editable cells, saving hours of setup and enabling quick comparison, collaboration, and board-ready presentations.

Activities

Lending and Credit Risk Management

Barclays extends credit via mortgages, personal loans and corporate finance while managing risks through advanced data models; in 2025 automated credit-scoring cuts decision time by ~40% and supports a CET1 ratio of 12.6% (H1 2025) to keep the balance sheet healthy. The bank aligns approvals with updated Basel III endgame rules and uses stress-testing and probability-of-default models to limit non-performing loan ratios, which stood near 1.0% in 2024.

Investment Banking and Advisory Services

Barclays provides mergers and acquisitions advisory, equity underwriting, and debt capital markets services, advising on deals worth over $120bn globally in 2024 and underwriting £15bn in equity issuance that year.

Digital Platform Development and Maintenance

Continuous investment in mobile and online banking is a core Barclays activity, supporting 35m active digital users and driving £1.2bn in 2024 tech spend; frequent updates deliver new features, tighter security, and a cleaner interface to reduce digital churn by ~18%. By end-2025, integrating generative AI assistants across apps became standard, improving self-service resolution rates from 62% to 78% in pilot markets and cutting call-centre volumes ~22%.

Wealth and Asset Management

- 270 billion GBP AUM (2025)

- Clients: HNWIs and institutions

- Quarterly performance & bespoke reporting

- Active allocation & market research

- ~35% discretionary AUM ESG-aligned (2025)

Regulatory Compliance and Financial Crime Prevention

Barclays dedicates large teams and ~£1.2bn annual compliance spend (2024 reported group control costs) to monitor transactions and meet global AML and KYC rules, protecting reputation and avoiding multi‑million fines.

The bank uses machine‑learning real‑time monitoring that flagged a 28% rise in suspicious activity alerts in 2024, improving detection and reducing false positives.

- £1.2bn compliance spend (2024)

- Real‑time ML monitoring

- 28% rise in alerts (2024)

- Reduces fines, protects reputation

Resilient bank: strong CET1, £270bn AUM, 35m users and £120bn deals in 2024–25

Key activities: lending and risk management (mortgages, corporate finance) with CET1 12.6% (H1 2025) and NPL ~1.0% (2024); capital markets advisory (£120bn deals 2024, £15bn equity underwritten); digital ops (35m users, £1.2bn tech spend 2024; gen‑AI raised self‑service to 78%); wealth AUM £270bn (2025, 35% ESG); compliance £1.2bn spend (2024), ML alerts +28% (2024).

| Metric | Value |

|---|---|

| CET1 | 12.6% (H1 2025) |

| AUM | £270bn (2025) |

| Digital users | 35m |

| Tech spend | £1.2bn (2024) |

| Compliance spend | £1.2bn (2024) |

| Deals advised | $120bn (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The Barclays Business Model Canvas shown here is the actual deliverable, not a mockup—what you see in this preview is a direct excerpt from the file you’ll receive after purchase.

On completion, you’ll instantly get the exact same document in editable formats, fully formatted and ready to use for presentations, planning, or analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Barclays Business Model Canvas: Strategic Blueprint for Investors & Strategists

Unlock the full strategic blueprint behind Barclays's business model—this in-depth Business Model Canvas uncovers how the bank creates value, scales revenue streams, and manages costs across retail, corporate, and investment banking; ideal for investors, consultants, and founders seeking actionable, company-specific insights.

Partnerships

Strategic Fintech Collaborations

Barclays partners with fintechs to embed payment and lending tech into its platforms, cutting internal build costs and matching neo-bank agility; by Dec 2025 these alliances covered 45+ fintechs, supporting £3.2bn in digital loan originations in 2024.

Global Payment Network Providers

Barclays retains long-standing links with Visa and Mastercard to power global card acceptance and merchant processing for retail and corporate clients, covering payments in 50+ currencies and >100 markets.

By 2025 those ties include integrated digital wallets and enhanced cross-border real-time rails, supporting instant FX-enabled transfers and reducing settlement times from days to seconds for targeted corridors.

Cloud Infrastructure and Data Partners

Barclays partners with Amazon Web Services and Microsoft Azure to supply the scalable compute for high-frequency trading and analytics, running an estimated 60% of its public-cloud workloads on these platforms by 2024; costs tied to cloud services reached about 0.4% of 2024 operating expenses. By 2025 Barclays is shifting to sovereign-cloud options in the UK/EU to meet stricter data-residency rules and reduce cross-border risk.

Co-Branded Commercial Partners

Barclays partners with retailers, airlines and tech firms like Apple to issue co-branded cards and point-of-sale financing, driving customer acquisition and card balances; co-branded cards accounted for about 22% of Barclays US card receivables (~$28bn) in 2025.

- Access to partner customer bases: millions of users

- Specialized rewards boost retention and spend

- Significant driver of 2025 credit volume and originations

Regulatory and Central Bank Liaisons

As a UK systemically important bank, Barclays engages continuously with the Bank of England and the Financial Conduct Authority, plus global regulators, to meet evolving Basel III/IV capital standards and ring-fencing rules; Barclays reported a CET1 ratio of 13.3% and leverage ratio of 4.4% at Q3 2025, guiding compliance decisions.

This collaborative oversight preserves market trust and helps manage cross-border resolution planning, liquidity buffers, and stress-test outcomes—Barclays held £222bn of high-quality liquid assets (HQLA) at end-2024.

- Regular dialogue with BoE and FCA

- CET1 ratio 13.3% (Q3 2025)

- Leverage ratio 4.4% (Q3 2025)

- HQLA £222bn (end-2024)

- Supports resolution, stress tests, capital planning

Barclays scales fintech partnerships, £3.2bn digital loans and $28bn US co‑brand receivables

Barclays leverages 45+ fintech partners (45 by Dec 2025) and major card networks (Visa, Mastercard) to drive £3.2bn digital loan originations (2024) and ~22% of US card receivables (~$28bn, 2025); public-cloud on AWS/Azure ~60% (2024) while shifting to sovereign-cloud (2025); CET1 13.3% and HQLA £222bn (end-2024).

| Metric | Value |

|---|---|

| Fintech partners | 45+ |

| Digital loans 2024 | £3.2bn |

| US card receivables (co-brand) | $28bn (22%) |

| Cloud share (2024) | ~60% |

| CET1 (Q3 2025) | 13.3% |

| HQLA (end-2024) | £222bn |

What is included in the product

A concise, pre-written Business Model Canvas for Barclays that maps nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned with the bank’s strategy, real-world operations, competitive advantages, SWOT insights, and designed for investor presentations and strategic decision-making.

Condenses Barclays’ strategy into a digestible one-page snapshot with editable cells, saving hours of setup and enabling quick comparison, collaboration, and board-ready presentations.

Activities

Lending and Credit Risk Management

Barclays extends credit via mortgages, personal loans and corporate finance while managing risks through advanced data models; in 2025 automated credit-scoring cuts decision time by ~40% and supports a CET1 ratio of 12.6% (H1 2025) to keep the balance sheet healthy. The bank aligns approvals with updated Basel III endgame rules and uses stress-testing and probability-of-default models to limit non-performing loan ratios, which stood near 1.0% in 2024.

Investment Banking and Advisory Services

Barclays provides mergers and acquisitions advisory, equity underwriting, and debt capital markets services, advising on deals worth over $120bn globally in 2024 and underwriting £15bn in equity issuance that year.

Digital Platform Development and Maintenance

Continuous investment in mobile and online banking is a core Barclays activity, supporting 35m active digital users and driving £1.2bn in 2024 tech spend; frequent updates deliver new features, tighter security, and a cleaner interface to reduce digital churn by ~18%. By end-2025, integrating generative AI assistants across apps became standard, improving self-service resolution rates from 62% to 78% in pilot markets and cutting call-centre volumes ~22%.

Wealth and Asset Management

- 270 billion GBP AUM (2025)

- Clients: HNWIs and institutions

- Quarterly performance & bespoke reporting

- Active allocation & market research

- ~35% discretionary AUM ESG-aligned (2025)

Regulatory Compliance and Financial Crime Prevention

Barclays dedicates large teams and ~£1.2bn annual compliance spend (2024 reported group control costs) to monitor transactions and meet global AML and KYC rules, protecting reputation and avoiding multi‑million fines.

The bank uses machine‑learning real‑time monitoring that flagged a 28% rise in suspicious activity alerts in 2024, improving detection and reducing false positives.

- £1.2bn compliance spend (2024)

- Real‑time ML monitoring

- 28% rise in alerts (2024)

- Reduces fines, protects reputation

Resilient bank: strong CET1, £270bn AUM, 35m users and £120bn deals in 2024–25

Key activities: lending and risk management (mortgages, corporate finance) with CET1 12.6% (H1 2025) and NPL ~1.0% (2024); capital markets advisory (£120bn deals 2024, £15bn equity underwritten); digital ops (35m users, £1.2bn tech spend 2024; gen‑AI raised self‑service to 78%); wealth AUM £270bn (2025, 35% ESG); compliance £1.2bn spend (2024), ML alerts +28% (2024).

| Metric | Value |

|---|---|

| CET1 | 12.6% (H1 2025) |

| AUM | £270bn (2025) |

| Digital users | 35m |

| Tech spend | £1.2bn (2024) |

| Compliance spend | £1.2bn (2024) |

| Deals advised | $120bn (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The Barclays Business Model Canvas shown here is the actual deliverable, not a mockup—what you see in this preview is a direct excerpt from the file you’ll receive after purchase.

On completion, you’ll instantly get the exact same document in editable formats, fully formatted and ready to use for presentations, planning, or analysis.