HomeStreet Business Model Canvas

HomeStreet Business Model Canvas: Strategy, Value, Risk & Revenue in One View

Unlock the full strategic blueprint behind HomeStreet's business model with our concise Business Model Canvas—discover how it creates customer value, manages risk, and monetizes core services.

Partnerships

Government Sponsored Enterprises

HomeStreet maintains critical ties with Fannie Mae, Freddie Mac, and Ginnie Mae to sell originated residential loans into the secondary market, freeing capital and supporting liquidity management; in 2024 HomeStreet sold roughly $1.1 billion of mortgage loans to agencies, sustaining capital ratios. By late 2025 these partnerships remain central to offering competitive mortgage pricing to its Western U.S. customers, helping keep mortgage yields aligned with agency-driven benchmarks.

Fintech and Technology Providers

HomeStreet partners with fintechs like Jack Henry (core processing) and Plaid-style API providers to run its digital banking and mobile apps, cutting development costs—HomeStreet reported 18% of deposit growth in 2024 tied to digital channels. These integrations enable real-time payments and multi-factor encryption, letting the bank compete with national banks and digital challengers without full in-house build.

Insurance and Investment Third-Parties

By 2025 HomeStreet partners with external insurance underwriters and investment platform providers to offer wealth management and protection products that complement core banking, driving cross-sell: insurer-backed life and property coverage and platform-based advisory services now represent about 12% of non-interest income (up from 6% in 2020), improving fee revenue and average revenue per retail customer by ~18% year-over-year.

Federal Home Loan Bank System

As a member of the Federal Home Loan Bank of Des Moines, HomeStreet secures a stable source of wholesale funding and liquidity, supporting lending through cycles; at YE 2024 HomeStreet reported $1.9B in FHLB borrowings (per 10-K) that strengthen its balance sheet and backstop obligations.

- Provides liquidity backstop

- $1.9B FHLB borrowings at 2024 year-end

- Supports commercial and residential lending

Strategic Real Estate Developers

The bank partners with regional real estate developers and construction firms across Hawaii and the Western US to source commercial real estate and construction loans, which made up roughly 28% of HomeStreet's loan portfolio in 2024 (about $1.1bn of $3.9bn total loans).

These local ties let HomeStreet join high-value urban projects and residential expansions, capturing higher-yield CRE spreads (average CRE yield ~5.2% in 2024) and shortening origination cycles.

- Partners: regional developers, contractors

- 2024 CRE share: ~28% ($1.1bn of $3.9bn)

- Average CRE yield 2024: ~5.2%

- Geography: Hawaii + Western US

HomeStreet: $1.1B mortgages sold, $1.9B FHLB liquidity, 18% digital deposit growth

HomeStreet relies on agency buyers (Fannie/Freddie/Ginnie) to sell ~$1.1B mortgages in 2024, Jack Henry and API partners for digital delivery (18% deposit growth from digital in 2024), FHLB Des Moines borrowings of $1.9B at YE2024 for liquidity, and regional CRE/developer ties (28% of loans, ~$1.1B; CRE yield ~5.2% in 2024).

| Partner | 2024 metric |

|---|---|

| Agency buyers | $1.1B mortgages sold |

| Digital providers | 18% deposit growth |

| FHLB Des Moines | $1.9B borrowings |

| Regional CRE partners | 28% loans; $1.1B; 5.2% yield |

What is included in the product

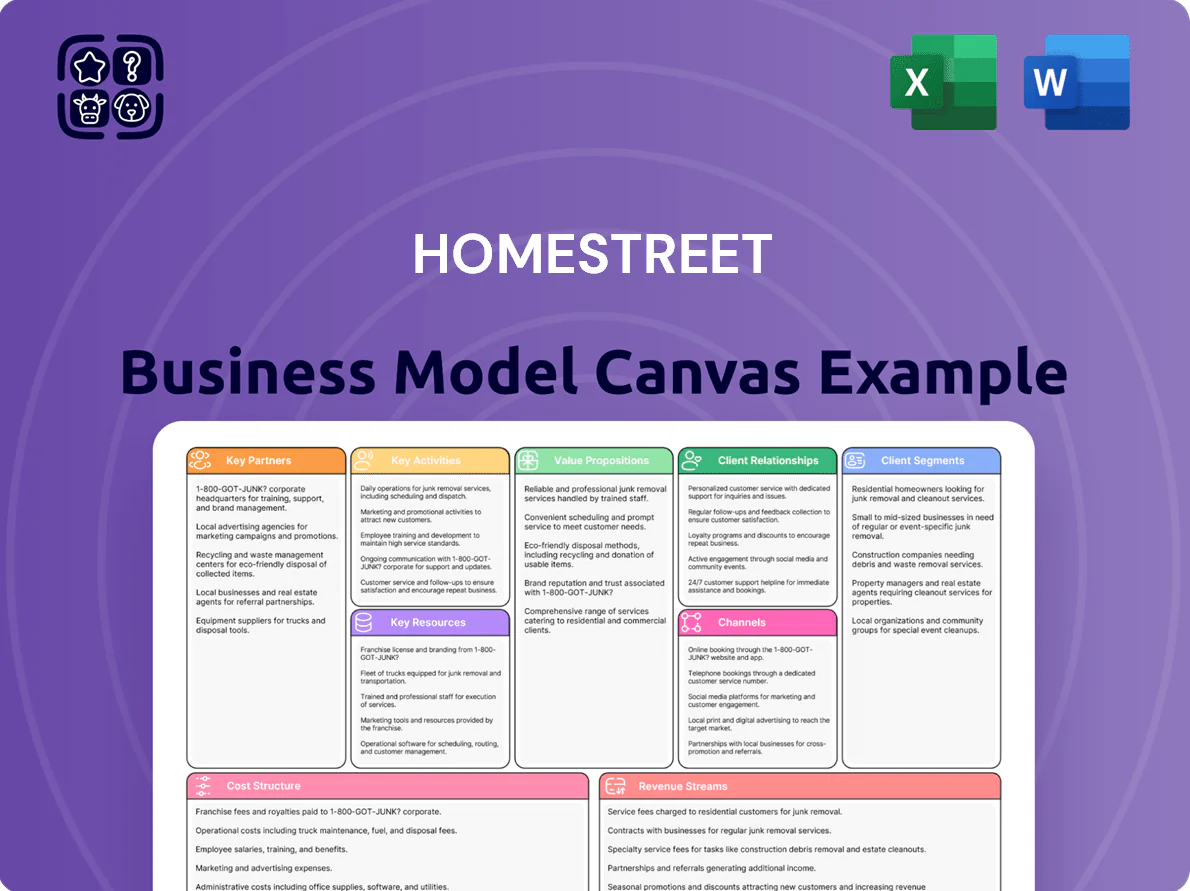

A focused Business Model Canvas for HomeStreet that maps its retail and commercial banking segments across the 9 BMC blocks, detailing customer segments, value propositions, channels, revenue streams and key resources to mirror real-world operations and strategic priorities.

High-level view of HomeStreet’s business model with editable cells, condensing lending, deposit, and fee strategies into a one-page snapshot to save hours of formatting and enable fast comparison, collaboration, and boardroom-ready summaries.

Activities

Mortgage Loan Origination and Servicing

HomeStreet processes residential mortgages end-to-end—origination, underwriting, closing, then servicing or sale—handling ~$4.2B mortgage loans outstanding as of 2025 and focusing on the Pacific Northwest and California to source higher-credit borrowers.

By end-2025 automation shortened average time-to-close from ~45 to ~28 days, cutting processing costs per loan by ~15% and improving servicing efficiency for long-term portfolio returns.

Commercial and Industrial Lending

HomeStreet provides capital to SMBs for equipment, operations, and expansion, underwriting with deep credit analysis and active relationship management to keep its C&I loan book diversified; as of YE 2024 HomeStreet reported $3.1B in total loans, with business lending a core contributor to net interest income. The bank targets regional industries—commercial real estate, healthcare, and manufacturing—driving steady interest revenue and client loyalty.

Deposit Gathering and Management

HomeStreet gathers and manages core deposits via 44 retail branches and digital channels, targeting low-cost funding to support $3.2B in loans; in 2025 it pushes high-yield savings and specialized checking to grow retail deposits after 2024 saw deposits at $4.1B, aiming for a 3–5% retail deposit growth to offset wholesale funding costs.

Risk Management and Compliance

Risk Management and Compliance consumes a large share of HomeStreet’s daily operations to meet strict financial-sector rules, including AML monitoring, loan-portfolio stress tests, and client data-privacy controls; in 2024 HomeStreet reported regulatory provisioning and compliance costs totaling roughly $18 million, protecting capital and reputation.

Effective risk oversight reduced non-performing assets to 0.9% of loans in 2024 and supported a CET1-like capital cushion above regulatory minimums; this preserves stakeholder trust and avoids fines.

- AML monitoring: continuous transaction screening

- Stress tests: quarterly portfolio scenarios

- Data privacy: GDPR/GLBA-aligned controls

- 2024 costs: ~$18M; NPLs: 0.9%

Asset and Wealth Management Services

HomeStreet provides tailored advisory services—investment strategies, ongoing market analysis, portfolio rebalancing, and financial planning—for individual and institutional clients, generating fee-based revenue that offsets interest-rate sensitivity.

In 2025 HomeStreet reported wealth-management fees of $38.4 million, up 7% YoY, representing about 12% of noninterest income and stabilizing net revenue amid loan yield pressure.

- Tailored strategies: individual + institutional

- Ongoing: market analysis + rebalancing

- Client meetings: financial planning sessions

- 2025 fees: $38.4M (+7% YoY)

- Fees ≈12% of noninterest income

HomeStreet: $4.2B mortgages, $4.1B deposits, low NPLs and rising wealth fees

HomeStreet runs end-to-end mortgage origination/servicing (~$4.2B loans 2025), C&I lending (~$3.1B loans YE2024), retail deposits $4.1B (2024) aiming 3–5% growth, strong risk/compliance (~$18M costs 2024, NPLs 0.9%), and wealth fees $38.4M (2025, +7%).

| Metric | Value |

|---|---|

| Mortgages | $4.2B (2025) |

| Total loans | $3.1B (YE2024) |

| Deposits | $4.1B (2024) |

| Compliance cost | $18M (2024) |

| NPLs | 0.9% (2024) |

| Wealth fees | $38.4M (2025) |

Full Document Unlocks After Purchase

Business Model Canvas

The HomeStreet Business Model Canvas preview you see is the actual deliverable—not a mockup or sample—and reflects the same content and structure you’ll receive after purchase.

When you complete your order, you’ll get this exact document ready to use, edit, and present in the provided formats with no hidden pages or altered layouts.

We provide transparent previews so you can buy with confidence: what’s shown here is what you’ll download and own.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

HomeStreet Business Model Canvas: Strategy, Value, Risk & Revenue in One View

Unlock the full strategic blueprint behind HomeStreet's business model with our concise Business Model Canvas—discover how it creates customer value, manages risk, and monetizes core services.

Partnerships

Government Sponsored Enterprises

HomeStreet maintains critical ties with Fannie Mae, Freddie Mac, and Ginnie Mae to sell originated residential loans into the secondary market, freeing capital and supporting liquidity management; in 2024 HomeStreet sold roughly $1.1 billion of mortgage loans to agencies, sustaining capital ratios. By late 2025 these partnerships remain central to offering competitive mortgage pricing to its Western U.S. customers, helping keep mortgage yields aligned with agency-driven benchmarks.

Fintech and Technology Providers

HomeStreet partners with fintechs like Jack Henry (core processing) and Plaid-style API providers to run its digital banking and mobile apps, cutting development costs—HomeStreet reported 18% of deposit growth in 2024 tied to digital channels. These integrations enable real-time payments and multi-factor encryption, letting the bank compete with national banks and digital challengers without full in-house build.

Insurance and Investment Third-Parties

By 2025 HomeStreet partners with external insurance underwriters and investment platform providers to offer wealth management and protection products that complement core banking, driving cross-sell: insurer-backed life and property coverage and platform-based advisory services now represent about 12% of non-interest income (up from 6% in 2020), improving fee revenue and average revenue per retail customer by ~18% year-over-year.

Federal Home Loan Bank System

As a member of the Federal Home Loan Bank of Des Moines, HomeStreet secures a stable source of wholesale funding and liquidity, supporting lending through cycles; at YE 2024 HomeStreet reported $1.9B in FHLB borrowings (per 10-K) that strengthen its balance sheet and backstop obligations.

- Provides liquidity backstop

- $1.9B FHLB borrowings at 2024 year-end

- Supports commercial and residential lending

Strategic Real Estate Developers

The bank partners with regional real estate developers and construction firms across Hawaii and the Western US to source commercial real estate and construction loans, which made up roughly 28% of HomeStreet's loan portfolio in 2024 (about $1.1bn of $3.9bn total loans).

These local ties let HomeStreet join high-value urban projects and residential expansions, capturing higher-yield CRE spreads (average CRE yield ~5.2% in 2024) and shortening origination cycles.

- Partners: regional developers, contractors

- 2024 CRE share: ~28% ($1.1bn of $3.9bn)

- Average CRE yield 2024: ~5.2%

- Geography: Hawaii + Western US

HomeStreet: $1.1B mortgages sold, $1.9B FHLB liquidity, 18% digital deposit growth

HomeStreet relies on agency buyers (Fannie/Freddie/Ginnie) to sell ~$1.1B mortgages in 2024, Jack Henry and API partners for digital delivery (18% deposit growth from digital in 2024), FHLB Des Moines borrowings of $1.9B at YE2024 for liquidity, and regional CRE/developer ties (28% of loans, ~$1.1B; CRE yield ~5.2% in 2024).

| Partner | 2024 metric |

|---|---|

| Agency buyers | $1.1B mortgages sold |

| Digital providers | 18% deposit growth |

| FHLB Des Moines | $1.9B borrowings |

| Regional CRE partners | 28% loans; $1.1B; 5.2% yield |

What is included in the product

A focused Business Model Canvas for HomeStreet that maps its retail and commercial banking segments across the 9 BMC blocks, detailing customer segments, value propositions, channels, revenue streams and key resources to mirror real-world operations and strategic priorities.

High-level view of HomeStreet’s business model with editable cells, condensing lending, deposit, and fee strategies into a one-page snapshot to save hours of formatting and enable fast comparison, collaboration, and boardroom-ready summaries.

Activities

Mortgage Loan Origination and Servicing

HomeStreet processes residential mortgages end-to-end—origination, underwriting, closing, then servicing or sale—handling ~$4.2B mortgage loans outstanding as of 2025 and focusing on the Pacific Northwest and California to source higher-credit borrowers.

By end-2025 automation shortened average time-to-close from ~45 to ~28 days, cutting processing costs per loan by ~15% and improving servicing efficiency for long-term portfolio returns.

Commercial and Industrial Lending

HomeStreet provides capital to SMBs for equipment, operations, and expansion, underwriting with deep credit analysis and active relationship management to keep its C&I loan book diversified; as of YE 2024 HomeStreet reported $3.1B in total loans, with business lending a core contributor to net interest income. The bank targets regional industries—commercial real estate, healthcare, and manufacturing—driving steady interest revenue and client loyalty.

Deposit Gathering and Management

HomeStreet gathers and manages core deposits via 44 retail branches and digital channels, targeting low-cost funding to support $3.2B in loans; in 2025 it pushes high-yield savings and specialized checking to grow retail deposits after 2024 saw deposits at $4.1B, aiming for a 3–5% retail deposit growth to offset wholesale funding costs.

Risk Management and Compliance

Risk Management and Compliance consumes a large share of HomeStreet’s daily operations to meet strict financial-sector rules, including AML monitoring, loan-portfolio stress tests, and client data-privacy controls; in 2024 HomeStreet reported regulatory provisioning and compliance costs totaling roughly $18 million, protecting capital and reputation.

Effective risk oversight reduced non-performing assets to 0.9% of loans in 2024 and supported a CET1-like capital cushion above regulatory minimums; this preserves stakeholder trust and avoids fines.

- AML monitoring: continuous transaction screening

- Stress tests: quarterly portfolio scenarios

- Data privacy: GDPR/GLBA-aligned controls

- 2024 costs: ~$18M; NPLs: 0.9%

Asset and Wealth Management Services

HomeStreet provides tailored advisory services—investment strategies, ongoing market analysis, portfolio rebalancing, and financial planning—for individual and institutional clients, generating fee-based revenue that offsets interest-rate sensitivity.

In 2025 HomeStreet reported wealth-management fees of $38.4 million, up 7% YoY, representing about 12% of noninterest income and stabilizing net revenue amid loan yield pressure.

- Tailored strategies: individual + institutional

- Ongoing: market analysis + rebalancing

- Client meetings: financial planning sessions

- 2025 fees: $38.4M (+7% YoY)

- Fees ≈12% of noninterest income

HomeStreet: $4.2B mortgages, $4.1B deposits, low NPLs and rising wealth fees

HomeStreet runs end-to-end mortgage origination/servicing (~$4.2B loans 2025), C&I lending (~$3.1B loans YE2024), retail deposits $4.1B (2024) aiming 3–5% growth, strong risk/compliance (~$18M costs 2024, NPLs 0.9%), and wealth fees $38.4M (2025, +7%).

| Metric | Value |

|---|---|

| Mortgages | $4.2B (2025) |

| Total loans | $3.1B (YE2024) |

| Deposits | $4.1B (2024) |

| Compliance cost | $18M (2024) |

| NPLs | 0.9% (2024) |

| Wealth fees | $38.4M (2025) |

Full Document Unlocks After Purchase

Business Model Canvas

The HomeStreet Business Model Canvas preview you see is the actual deliverable—not a mockup or sample—and reflects the same content and structure you’ll receive after purchase.

When you complete your order, you’ll get this exact document ready to use, edit, and present in the provided formats with no hidden pages or altered layouts.

We provide transparent previews so you can buy with confidence: what’s shown here is what you’ll download and own.