Hewlett Packard Enterprise Porter's Five Forces Analysis

Don't Miss the Bigger Picture

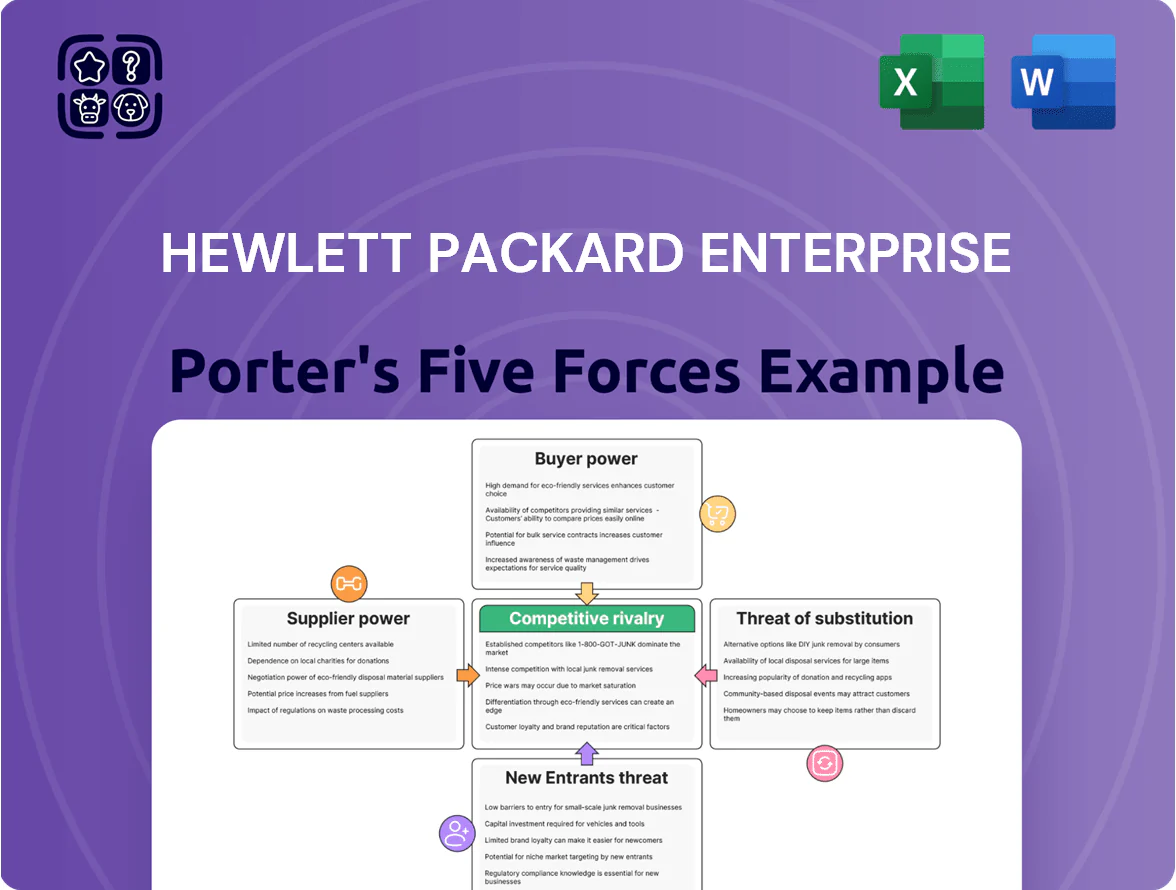

Hewlett Packard Enterprise faces intense rivalry from major cloud and infrastructure players, moderate supplier leverage for specialized components, and growing buyer bargaining as enterprises demand integrated hybrid solutions; new entrants are constrained by scale, but substitutes from hyperscalers pose a real threat. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore HPE’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of High-Performance Chip Providers

HPE depends on a few chip suppliers—NVIDIA, AMD, and Intel—for AI accelerators and CPUs; together they supplied over 85% of hyperscale AI accelerator shipments in 2025, giving them strong leverage over price and allocation.

Scarcity and surging demand for GPUs and custom accelerators at end-2025 pushed average supplier lead times to 16–24 weeks and spot price premiums of 12–25%, pressuring HPE margins.

This supplier concentration creates a bottleneck risk that could delay fulfillment of large AI infrastructure contracts and force HPE to absorb higher costs or face revenue timing hits.

Strategic Importance of Proprietary Software Vendors

Integration of specialized OS and virtualization software into HPE’s hybrid cloud and edge stack gives proprietary vendors strong leverage; for example, VMware and Microsoft accounted for critical components across GreenLake deployments, and third-party license spend can exceed 10% of service COGS in enterprise offers (2024 internal benchmarks).

Impact of Global Supply Chain Resilience

HPE has diversified manufacturing but still depends on specialized memory, storage and networking suppliers concentrated in Taiwan and South Korea, creating supplier leverage during geopolitical or logistic shocks. Suppliers pushed price premiums up to 12% in 2024 during capacity tightness; HPE paid higher component costs, squeezing gross margin by ~80–120 basis points in FY2024. By end-2025, HPE reports rising procurement spend as localized sourcing raised unit costs ~6–9% while securing tier-one capacity.

Influence of Emerging AI Infrastructure Partners

- Liquid cooling cut PUE ~0.2–0.4 (2024)

- Top 5 specialty vendors <40% market share (2024)

- Higher supplier margins vs. standard rack gear

- Switching costs and contract rigidity rise

Labor Market Pressures for Specialized Engineering Talent

The supply of engineers who can build edge-to-cloud systems is a critical input for HPE’s innovation; global demand for AI and cybersecurity talent rose ~35% from 2020–2024, tightening supply.

AI and security specialists command premium pay—median total compensation for senior AI engineers reached ~$230k in 2024—giving suppliers strong bargaining power over pay and remote/flex terms.

HPE must keep investing in recruiting, training, retention, and equity to stop talent flight to hyperscalers or startups; turnover in top engineering roles above 12% raises project delays and IP loss risk.

- High demand: +35% AI/security hires (2020–2024)

- Senior AI pay: ~$230k median (2024)

- Top-engineer turnover: >12% raises IP risk

- Action: sustained hiring, upskilling, equity

Chip oligopoly fuels lead times, spot premiums and squeezes HPE margins

Supplier power is high: a few chip vendors (NVIDIA, AMD, Intel) supplied >85% of hyperscale AI accelerators in 2025, causing 16–24 week lead times and 12–25% spot premiums that squeezed HPE margins.

Specialized software, liquid-cooling, and memory/storage vendors exert pricing leverage; supplier-driven price moves added ~80–120 bps to gross-margin pressure in FY2024 and localized sourcing raised unit costs ~6–9% by end-2025.

| Metric | Value |

|---|---|

| Top chip share (2025) | >85% |

| Lead times (end-2025) | 16–24 weeks |

| Spot premiums | 12–25% |

| Gross margin hit (FY2024) | 80–120 bps |

| Unit cost rise (local sourcing, 2025) | 6–9% |

What is included in the product

Tailored exclusively for Hewlett Packard Enterprise, this Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer power, substitution risks, and entry barriers to evaluate HPE’s pricing leverage and long-term profitability.

A concise Porter's Five Forces snapshot for Hewlett Packard Enterprise—clarifies competitive pressures and strategic levers at a glance to speed executive decisions.

Customers Bargaining Power

Consolidation of Large Enterprise Accounts

Large corporate and government clients provide roughly 60% of Hewlett Packard Enterprise’s fiscal 2024 revenue, giving them strong bargaining power.

They press HPE for tailored solutions, steep discounts and multi-year service SLAs, often cutting gross margins by 3–6 percentage points on major bids.

Access to rivals like Dell Technologies and Lenovo means HPE must match pricing and offer value-added services to win contracts, driving intense competitive bidding.

Low Switching Costs in Standardized Hardware Segments

In commodity servers and basic storage, switching costs are low—buyers can compare specs and often choose price, which cut HPE’s hardware gross margin to about 22% in FY2024 (HPE fiscal year ended Oct 31, 2024). Price-driven churn pressures margins, so HPE bundles GreenLake management software and services to raise effective switching costs, growing as‑a‑service revenue to $5.3bn in FY2024 and improving customer stickiness.

Influence of Managed Service Providers and Channel Partners

A large share of HPEs revenue—about 60% in FY2024—flows through third-party distributors and managed service providers (MSPs) who bundle demand from SMBs, giving these partners leverage to steer buyers toward competitors offering higher margins or better incentives. If MSPs shift 10–15% of their spend, HPE could lose meaningful market share, so HPE invests in partner rebates, co-marketing, and a partner loyalty program that supported $7.8B in channel bookings in 2024 to retain ecosystem allegiance.

Demand for Consumption-Based Financial Models

By late 2025, enterprise buyers prefer OpEx consumption models like HPE GreenLake—driving demand for flexible scaling and reducing CapEx buys; IDC reported consumption-based infrastructure grew ~22% YoY in 2024, raising buyer leverage over contract terms.

This shift lets customers cut hardware-cycle lock-in and move workloads by performance and cost, pressuring HPE to absorb financing and operational risk; HPE reported $1.2B in GreenLake deferred revenue in FY2024, showing rising exposure.

- Customers demand utility-style IT and flexible scaling

- Consumption infra grew ~22% YoY (2024, IDC)

- HPE GreenLake deferred revenue ~$1.2B (FY2024)

- HPE bears more financial and operational risk

Sophistication of Cloud-Native Decision Makers

Modern IT leaders know cloud architectures and run multi-clouds to avoid vendor lock-in; 2024 Flexera found 92% of enterprises use multi-cloud, raising HPE bargaining pressure.

That sophistication lets buyers threaten moves to AWS, Azure, Google, or open-source stacks, forcing HPE to offer better pricing and SLAs; HPE reported 2024 revenue of $29.1B, so retention matters.

HPE must prove superior hybrid orchestration and data sovereignty—areas where customers pay premiums—to keep these demanding buyers.

- 92% enterprises use multi-cloud (Flexera 2024)

- HPE 2024 revenue $29.1B

- Buyers push for stronger SLAs, lower TCO

- Data sovereignty and hybrid orchestration are key retention levers

HPE: Corporate buyer power, GreenLake growth squeeze hardware margins

Large corporate/government clients (~60% of HPE FY2024 revenue) have strong leverage, forcing discounts and SLAs that cut hardware margins 3–6 pts; commodity servers/storage see ~22% hardware gross margin in FY2024. Consumption models (GreenLake revenue $5.3B, deferred rev ~$1.2B) and 22% YoY growth in consumption infra (IDC 2024) raise buyer power; channels drove $7.8B bookings in 2024.

| Metric | 2024 |

|---|---|

| HPE revenue | $29.1B |

| Corp/Gov share | ~60% |

| GreenLake revenue | $5.3B |

| Deferred rev | $1.2B |

| Channel bookings | $7.8B |

| Consumption infra growth | ~22% YoY |

| Hardware gross margin | ~22% |

Preview Before You Purchase

Hewlett Packard Enterprise Porter's Five Forces Analysis

This preview shows the exact Hewlett Packard Enterprise Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with clear, actionable insights and data-driven conclusions.

The document displayed is the full, professionally formatted file—ready for instant download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Hewlett Packard Enterprise faces intense rivalry from major cloud and infrastructure players, moderate supplier leverage for specialized components, and growing buyer bargaining as enterprises demand integrated hybrid solutions; new entrants are constrained by scale, but substitutes from hyperscalers pose a real threat. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore HPE’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of High-Performance Chip Providers

HPE depends on a few chip suppliers—NVIDIA, AMD, and Intel—for AI accelerators and CPUs; together they supplied over 85% of hyperscale AI accelerator shipments in 2025, giving them strong leverage over price and allocation.

Scarcity and surging demand for GPUs and custom accelerators at end-2025 pushed average supplier lead times to 16–24 weeks and spot price premiums of 12–25%, pressuring HPE margins.

This supplier concentration creates a bottleneck risk that could delay fulfillment of large AI infrastructure contracts and force HPE to absorb higher costs or face revenue timing hits.

Strategic Importance of Proprietary Software Vendors

Integration of specialized OS and virtualization software into HPE’s hybrid cloud and edge stack gives proprietary vendors strong leverage; for example, VMware and Microsoft accounted for critical components across GreenLake deployments, and third-party license spend can exceed 10% of service COGS in enterprise offers (2024 internal benchmarks).

Impact of Global Supply Chain Resilience

HPE has diversified manufacturing but still depends on specialized memory, storage and networking suppliers concentrated in Taiwan and South Korea, creating supplier leverage during geopolitical or logistic shocks. Suppliers pushed price premiums up to 12% in 2024 during capacity tightness; HPE paid higher component costs, squeezing gross margin by ~80–120 basis points in FY2024. By end-2025, HPE reports rising procurement spend as localized sourcing raised unit costs ~6–9% while securing tier-one capacity.

Influence of Emerging AI Infrastructure Partners

- Liquid cooling cut PUE ~0.2–0.4 (2024)

- Top 5 specialty vendors <40% market share (2024)

- Higher supplier margins vs. standard rack gear

- Switching costs and contract rigidity rise

Labor Market Pressures for Specialized Engineering Talent

The supply of engineers who can build edge-to-cloud systems is a critical input for HPE’s innovation; global demand for AI and cybersecurity talent rose ~35% from 2020–2024, tightening supply.

AI and security specialists command premium pay—median total compensation for senior AI engineers reached ~$230k in 2024—giving suppliers strong bargaining power over pay and remote/flex terms.

HPE must keep investing in recruiting, training, retention, and equity to stop talent flight to hyperscalers or startups; turnover in top engineering roles above 12% raises project delays and IP loss risk.

- High demand: +35% AI/security hires (2020–2024)

- Senior AI pay: ~$230k median (2024)

- Top-engineer turnover: >12% raises IP risk

- Action: sustained hiring, upskilling, equity

Chip oligopoly fuels lead times, spot premiums and squeezes HPE margins

Supplier power is high: a few chip vendors (NVIDIA, AMD, Intel) supplied >85% of hyperscale AI accelerators in 2025, causing 16–24 week lead times and 12–25% spot premiums that squeezed HPE margins.

Specialized software, liquid-cooling, and memory/storage vendors exert pricing leverage; supplier-driven price moves added ~80–120 bps to gross-margin pressure in FY2024 and localized sourcing raised unit costs ~6–9% by end-2025.

| Metric | Value |

|---|---|

| Top chip share (2025) | >85% |

| Lead times (end-2025) | 16–24 weeks |

| Spot premiums | 12–25% |

| Gross margin hit (FY2024) | 80–120 bps |

| Unit cost rise (local sourcing, 2025) | 6–9% |

What is included in the product

Tailored exclusively for Hewlett Packard Enterprise, this Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer power, substitution risks, and entry barriers to evaluate HPE’s pricing leverage and long-term profitability.

A concise Porter's Five Forces snapshot for Hewlett Packard Enterprise—clarifies competitive pressures and strategic levers at a glance to speed executive decisions.

Customers Bargaining Power

Consolidation of Large Enterprise Accounts

Large corporate and government clients provide roughly 60% of Hewlett Packard Enterprise’s fiscal 2024 revenue, giving them strong bargaining power.

They press HPE for tailored solutions, steep discounts and multi-year service SLAs, often cutting gross margins by 3–6 percentage points on major bids.

Access to rivals like Dell Technologies and Lenovo means HPE must match pricing and offer value-added services to win contracts, driving intense competitive bidding.

Low Switching Costs in Standardized Hardware Segments

In commodity servers and basic storage, switching costs are low—buyers can compare specs and often choose price, which cut HPE’s hardware gross margin to about 22% in FY2024 (HPE fiscal year ended Oct 31, 2024). Price-driven churn pressures margins, so HPE bundles GreenLake management software and services to raise effective switching costs, growing as‑a‑service revenue to $5.3bn in FY2024 and improving customer stickiness.

Influence of Managed Service Providers and Channel Partners

A large share of HPEs revenue—about 60% in FY2024—flows through third-party distributors and managed service providers (MSPs) who bundle demand from SMBs, giving these partners leverage to steer buyers toward competitors offering higher margins or better incentives. If MSPs shift 10–15% of their spend, HPE could lose meaningful market share, so HPE invests in partner rebates, co-marketing, and a partner loyalty program that supported $7.8B in channel bookings in 2024 to retain ecosystem allegiance.

Demand for Consumption-Based Financial Models

By late 2025, enterprise buyers prefer OpEx consumption models like HPE GreenLake—driving demand for flexible scaling and reducing CapEx buys; IDC reported consumption-based infrastructure grew ~22% YoY in 2024, raising buyer leverage over contract terms.

This shift lets customers cut hardware-cycle lock-in and move workloads by performance and cost, pressuring HPE to absorb financing and operational risk; HPE reported $1.2B in GreenLake deferred revenue in FY2024, showing rising exposure.

- Customers demand utility-style IT and flexible scaling

- Consumption infra grew ~22% YoY (2024, IDC)

- HPE GreenLake deferred revenue ~$1.2B (FY2024)

- HPE bears more financial and operational risk

Sophistication of Cloud-Native Decision Makers

Modern IT leaders know cloud architectures and run multi-clouds to avoid vendor lock-in; 2024 Flexera found 92% of enterprises use multi-cloud, raising HPE bargaining pressure.

That sophistication lets buyers threaten moves to AWS, Azure, Google, or open-source stacks, forcing HPE to offer better pricing and SLAs; HPE reported 2024 revenue of $29.1B, so retention matters.

HPE must prove superior hybrid orchestration and data sovereignty—areas where customers pay premiums—to keep these demanding buyers.

- 92% enterprises use multi-cloud (Flexera 2024)

- HPE 2024 revenue $29.1B

- Buyers push for stronger SLAs, lower TCO

- Data sovereignty and hybrid orchestration are key retention levers

HPE: Corporate buyer power, GreenLake growth squeeze hardware margins

Large corporate/government clients (~60% of HPE FY2024 revenue) have strong leverage, forcing discounts and SLAs that cut hardware margins 3–6 pts; commodity servers/storage see ~22% hardware gross margin in FY2024. Consumption models (GreenLake revenue $5.3B, deferred rev ~$1.2B) and 22% YoY growth in consumption infra (IDC 2024) raise buyer power; channels drove $7.8B bookings in 2024.

| Metric | 2024 |

|---|---|

| HPE revenue | $29.1B |

| Corp/Gov share | ~60% |

| GreenLake revenue | $5.3B |

| Deferred rev | $1.2B |

| Channel bookings | $7.8B |

| Consumption infra growth | ~22% YoY |

| Hardware gross margin | ~22% |

Preview Before You Purchase

Hewlett Packard Enterprise Porter's Five Forces Analysis

This preview shows the exact Hewlett Packard Enterprise Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

It covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with clear, actionable insights and data-driven conclusions.

The document displayed is the full, professionally formatted file—ready for instant download and use the moment you buy.