Huaneng Power International Boston Consulting Group Matrix

Actionable Strategy Starts Here

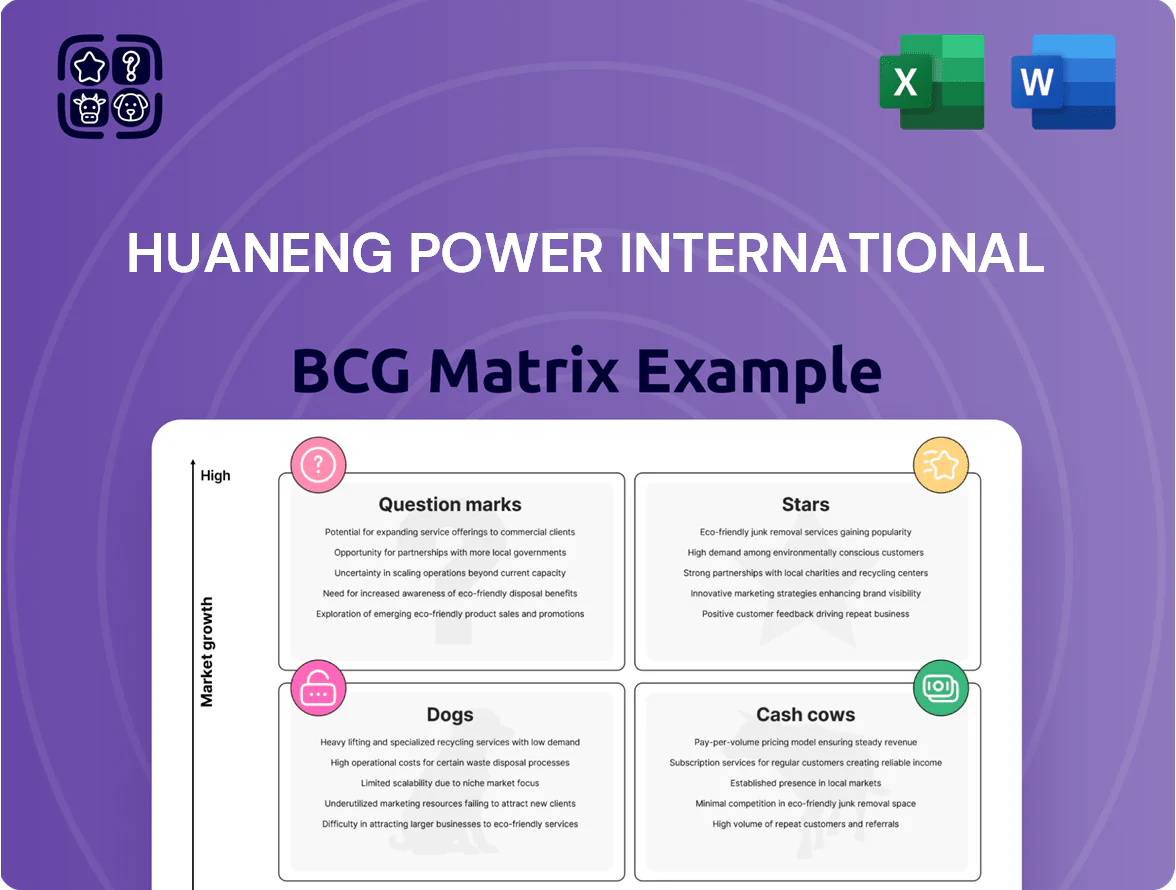

Huaneng Power International sits at a pivotal crossroads with assets spanning conventional coal, renewables, and grid services—our BCG Matrix preview highlights which units are driving growth and which may need reevaluation as China shifts toward decarbonization. This snapshot teases quadrant placements and high-level strategic implications, but the full BCG Matrix delivers quadrant-by-quadrant data, investment priorities, and actionable recommendations. Purchase the complete report to get a polished Word analysis plus an Excel summary you can use to reallocate capital and sharpen competitive strategy.

Stars

Offshore Wind Power

Huaneng Power International has scaled offshore wind to about 5.2 GW by Dec 2025, targeting China’s high-load coastal demand and achieving >3,800 annual utilization hours on flagship farms.

Projects receive strong national subsidies and grid priority, boosting levelized value despite CNY 40–55 million/MW capex; payback aided by merchant prices rising ~12% since 2023.

By late 2025 offshore wind accounts for roughly 28% of Huaneng’s renewable capacity and is the firm’s primary growth engine in the energy transition.

Large-scale Photovoltaic Hubs

Huaneng Power International has built >5 GW of utility-scale solar across western China and coastal provinces to hit China’s 2030 renewable target; these large-scale photovoltaic hubs lifted renewable segment revenue by ~28% YoY to RMB 21.4 billion in 2024.

Falling module costs (module prices down ~55% since 2019) and a 12% rise in plant load factor improved margins, making these hubs cash-generative and positioning Huaneng as a growth leader.

Strategic land deals and priority grid connections secured ~3 GW of queued capacity for 2025–27, keeping Huaneng in pole position within the high-growth solar quadrant.

Integrated Energy Services

Integrated Energy Services combines heating, cooling and electricity for industrial parks and sits in Huaneng Power International’s BCG Stars quadrant as a high-growth frontier, targeting a corporate energy management market projected to reach US$98 billion by 2026 (source: industry analyst consensus).

By using digital platforms and demand-response controls, Huaneng reduced client energy intensity by up to 15% in 2024 pilots, helping capture a growing share of commercial energy services.

The unit needs heavy upfront capex—estimated RMB 4–6 billion for a 100 MW integrated campus—but offers leadership potential as China expands smart energy zones under 14th Five-Year Plan policies.

Utility-scale Battery Storage

Utility-scale battery storage is a Star for Huaneng Power International: grid flexibility needs rose 32% in China 2024, and Huaneng committed 1.2 GW/3.6 GWh of large-scale storage projects by Dec 2025 to firm wind and solar output, reinforcing its reliable-provider position.

- High demand: frequency regulation market up 45% YoY (2024)

- Capacity: 1.2 GW / 3.6 GWh committed by Huaneng

- Revenue impact: storage tariffs improving NPV vs peaker plants

- Outlook: remains Star through end-2025 due to grid stability needs

Green Hydrogen Production

Huaneng Power International leverages a 2025 renewables base (over 25 GW wind+solar) to pilot industrial-scale green hydrogen for transport and chemicals, aligning with China’s 2030 heavy-industry decarbonization push and a forecasted national hydrogen demand of ~31 Mt H2 by 2030.

Projects are cash‑intensive—electrolyser CAPEX ~800–1,200 USD/kW—but position Huaneng as a future clean-fuel supplier as China targets 50% green hydrogen share in key sectors by 2035.

- 25+ GW renewables (2025)

- China hydrogen demand ~31 Mt H2 by 2030

- Electrolyser CAPEX ~800–1,200 USD/kW

- Target: 50% green H2 in sectors by 2035

Huaneng’s Growth Engines: 5+GW Wind & Solar, 1.2GW Storage Powering Transition

Stars: Offshore wind (5.2 GW by Dec 2025), utility solar (5+ GW, RMB 21.4b renewables rev in 2024), utility storage (1.2 GW/3.6 GWh committed) and integrated energy services (pilot energy intensity cut 15%); all high-growth, high-share units driving Huaneng’s transition.

| Asset | Size | Key metric |

|---|---|---|

| Offshore wind | 5.2 GW | 3,800+ hrs |

| Solar | 5+ GW | RMB 21.4b rev (2024) |

| Storage | 1.2 GW/3.6 GWh | Grid flex +32% (2024) |

What is included in the product

In-depth BCG review of Huaneng Power: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, and divest recommendations.

One-page BCG Matrix mapping Huaneng Power units to quadrants for quick strategic decisions and investor presentations.

Cash Cows

Ultra-supercritical Coal Units

Huaneng Power’s ultra-supercritical coal units supply stable base-load power for China’s industry, running >60% capacity factors in 2024 and providing roughly 35–40% of the company’s EBITDA (about CNY 28–32 bn in 2024).

These mature, high-efficiency units emit ~10–15% less CO2 per MWh than subcritical plants, need limited capex (maintenance + upgrades ~CNY 3–4 bn/yr) and free cash to fund renewable investments.

With >50% market share in key provincial grids, they generate predictable FCF that underwrites Huaneng’s 2030 renewables target (20 GW owned by 2025 plan continuation) while sustaining dividend capacity.

District Heating Operations

Huaneng Power International’s district heating operations supply heat to ~12 million residents and industrial sites in northern China, delivering stable, captive demand; heat sales accounted for about CNY 8.5 billion in 2024, per company disclosures.

Long-term concession contracts and owned pipe networks give high gross margins—estimated 25–30%—and predictable cash flow, supporting CAPEX-light maintenance spending of ~CNY 1.1 billion in 2024.

With regional heating demand growth near 1% annually and no major expansion drivers, this low-growth, high-cash-generating segment is a textbook BCG cash cow for Huaneng.

Hydropower Generation

Huaneng Power International’s hydropower fleet delivered steady low-cost generation, with 2024 hydropower output ~48 TWh (≈22% of total 2024 generation) and operating margins near 45%, keeping O&M per MWh low and capex minimal by late 2025.

Coal Port Logistics

Huaneng Power International runs captive coal transport and port assets that secure fuel for ~70 GW thermal capacity; 2024 segment EBITDA margin estimated ~28% vs industry 12–18%, generating steady cash in a mature logistics market.

These ports also serve third-party clients, adding high-margin external revenue; cash flows in 2024 reportedly supported ¥7.2bn in interest payments and ¥1.1bn R&D spend, easing corporate leverage.

- Captive supply: secures fuel for ~70 GW fleet

- Margin: segment EBITDA ~28% (2024 est.)

- Market: mature, low capex growth

- Use of cash: ¥7.2bn interest, ¥1.1bn R&D (2024)

Power Sales and Trading

Huaneng Power International’s Power Sales and Trading arm sells ~220 TWh annually to the national grid and large industrial users across provinces, leveraging a dominant market share and long-term contracts that keep incremental sales costs under 5 RMB/MWh.

Its high-volume trades generated ~RMB 28.5 billion operating cash flow in FY2024, providing steady liquidity to fund R&D and pilot projects in green hydrogen and carbon capture.

- Annual volume: ~220 TWh

- FY2024 operating cash: RMB 28.5 billion

- Incremental cost: <5 RMB/MWh

- Use of cash: R&D in hydrogen/CCS

Huaneng: CNY 50–58bn EBITDA cash cows fuel CNY 32–36bn FCF for renewables

Huaneng’s coal ultra-supercritical fleet, district heating, hydro, ports/logistics, and Power Trading are stable cash cows: combined 2024 EBITDA ~CNY 50–58bn, FCF funding renewables (2024 free cash ~CNY 32–36bn), maintenance capex ~CNY 5–6bn, and dividends sustained; heat sales CNY 8.5bn; hydropower ~48 TWh; trading cash ~RMB 28.5bn.

| Segment | 2024 Metric | Cash/EBITDA |

|---|---|---|

| Coal fleet | >60% CF; 35–40% EBITDA | CNY 28–32bn |

| District heating | 12M users; CNY 8.5bn | 25–30% margin |

| Hydro | ~48 TWh | ~45% margin |

| Ports/logistics | serves ~70 GW | ~28% EBITDA |

| Trading | ~220 TWh sold | RMB 28.5bn OCF |

What You See Is What You Get

Huaneng Power International BCG Matrix

The Huaneng Power International BCG Matrix you’re previewing is the exact file you’ll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready report tailored for strategic decision-making. This preview mirrors the final deliverable, crafted with market-backed insights and clear visuals so you can immediately edit, print, or present without additional adjustments. Purchase grants instant download and direct delivery to your inbox for immediate use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Huaneng Power International sits at a pivotal crossroads with assets spanning conventional coal, renewables, and grid services—our BCG Matrix preview highlights which units are driving growth and which may need reevaluation as China shifts toward decarbonization. This snapshot teases quadrant placements and high-level strategic implications, but the full BCG Matrix delivers quadrant-by-quadrant data, investment priorities, and actionable recommendations. Purchase the complete report to get a polished Word analysis plus an Excel summary you can use to reallocate capital and sharpen competitive strategy.

Stars

Offshore Wind Power

Huaneng Power International has scaled offshore wind to about 5.2 GW by Dec 2025, targeting China’s high-load coastal demand and achieving >3,800 annual utilization hours on flagship farms.

Projects receive strong national subsidies and grid priority, boosting levelized value despite CNY 40–55 million/MW capex; payback aided by merchant prices rising ~12% since 2023.

By late 2025 offshore wind accounts for roughly 28% of Huaneng’s renewable capacity and is the firm’s primary growth engine in the energy transition.

Large-scale Photovoltaic Hubs

Huaneng Power International has built >5 GW of utility-scale solar across western China and coastal provinces to hit China’s 2030 renewable target; these large-scale photovoltaic hubs lifted renewable segment revenue by ~28% YoY to RMB 21.4 billion in 2024.

Falling module costs (module prices down ~55% since 2019) and a 12% rise in plant load factor improved margins, making these hubs cash-generative and positioning Huaneng as a growth leader.

Strategic land deals and priority grid connections secured ~3 GW of queued capacity for 2025–27, keeping Huaneng in pole position within the high-growth solar quadrant.

Integrated Energy Services

Integrated Energy Services combines heating, cooling and electricity for industrial parks and sits in Huaneng Power International’s BCG Stars quadrant as a high-growth frontier, targeting a corporate energy management market projected to reach US$98 billion by 2026 (source: industry analyst consensus).

By using digital platforms and demand-response controls, Huaneng reduced client energy intensity by up to 15% in 2024 pilots, helping capture a growing share of commercial energy services.

The unit needs heavy upfront capex—estimated RMB 4–6 billion for a 100 MW integrated campus—but offers leadership potential as China expands smart energy zones under 14th Five-Year Plan policies.

Utility-scale Battery Storage

Utility-scale battery storage is a Star for Huaneng Power International: grid flexibility needs rose 32% in China 2024, and Huaneng committed 1.2 GW/3.6 GWh of large-scale storage projects by Dec 2025 to firm wind and solar output, reinforcing its reliable-provider position.

- High demand: frequency regulation market up 45% YoY (2024)

- Capacity: 1.2 GW / 3.6 GWh committed by Huaneng

- Revenue impact: storage tariffs improving NPV vs peaker plants

- Outlook: remains Star through end-2025 due to grid stability needs

Green Hydrogen Production

Huaneng Power International leverages a 2025 renewables base (over 25 GW wind+solar) to pilot industrial-scale green hydrogen for transport and chemicals, aligning with China’s 2030 heavy-industry decarbonization push and a forecasted national hydrogen demand of ~31 Mt H2 by 2030.

Projects are cash‑intensive—electrolyser CAPEX ~800–1,200 USD/kW—but position Huaneng as a future clean-fuel supplier as China targets 50% green hydrogen share in key sectors by 2035.

- 25+ GW renewables (2025)

- China hydrogen demand ~31 Mt H2 by 2030

- Electrolyser CAPEX ~800–1,200 USD/kW

- Target: 50% green H2 in sectors by 2035

Huaneng’s Growth Engines: 5+GW Wind & Solar, 1.2GW Storage Powering Transition

Stars: Offshore wind (5.2 GW by Dec 2025), utility solar (5+ GW, RMB 21.4b renewables rev in 2024), utility storage (1.2 GW/3.6 GWh committed) and integrated energy services (pilot energy intensity cut 15%); all high-growth, high-share units driving Huaneng’s transition.

| Asset | Size | Key metric |

|---|---|---|

| Offshore wind | 5.2 GW | 3,800+ hrs |

| Solar | 5+ GW | RMB 21.4b rev (2024) |

| Storage | 1.2 GW/3.6 GWh | Grid flex +32% (2024) |

What is included in the product

In-depth BCG review of Huaneng Power: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, and divest recommendations.

One-page BCG Matrix mapping Huaneng Power units to quadrants for quick strategic decisions and investor presentations.

Cash Cows

Ultra-supercritical Coal Units

Huaneng Power’s ultra-supercritical coal units supply stable base-load power for China’s industry, running >60% capacity factors in 2024 and providing roughly 35–40% of the company’s EBITDA (about CNY 28–32 bn in 2024).

These mature, high-efficiency units emit ~10–15% less CO2 per MWh than subcritical plants, need limited capex (maintenance + upgrades ~CNY 3–4 bn/yr) and free cash to fund renewable investments.

With >50% market share in key provincial grids, they generate predictable FCF that underwrites Huaneng’s 2030 renewables target (20 GW owned by 2025 plan continuation) while sustaining dividend capacity.

District Heating Operations

Huaneng Power International’s district heating operations supply heat to ~12 million residents and industrial sites in northern China, delivering stable, captive demand; heat sales accounted for about CNY 8.5 billion in 2024, per company disclosures.

Long-term concession contracts and owned pipe networks give high gross margins—estimated 25–30%—and predictable cash flow, supporting CAPEX-light maintenance spending of ~CNY 1.1 billion in 2024.

With regional heating demand growth near 1% annually and no major expansion drivers, this low-growth, high-cash-generating segment is a textbook BCG cash cow for Huaneng.

Hydropower Generation

Huaneng Power International’s hydropower fleet delivered steady low-cost generation, with 2024 hydropower output ~48 TWh (≈22% of total 2024 generation) and operating margins near 45%, keeping O&M per MWh low and capex minimal by late 2025.

Coal Port Logistics

Huaneng Power International runs captive coal transport and port assets that secure fuel for ~70 GW thermal capacity; 2024 segment EBITDA margin estimated ~28% vs industry 12–18%, generating steady cash in a mature logistics market.

These ports also serve third-party clients, adding high-margin external revenue; cash flows in 2024 reportedly supported ¥7.2bn in interest payments and ¥1.1bn R&D spend, easing corporate leverage.

- Captive supply: secures fuel for ~70 GW fleet

- Margin: segment EBITDA ~28% (2024 est.)

- Market: mature, low capex growth

- Use of cash: ¥7.2bn interest, ¥1.1bn R&D (2024)

Power Sales and Trading

Huaneng Power International’s Power Sales and Trading arm sells ~220 TWh annually to the national grid and large industrial users across provinces, leveraging a dominant market share and long-term contracts that keep incremental sales costs under 5 RMB/MWh.

Its high-volume trades generated ~RMB 28.5 billion operating cash flow in FY2024, providing steady liquidity to fund R&D and pilot projects in green hydrogen and carbon capture.

- Annual volume: ~220 TWh

- FY2024 operating cash: RMB 28.5 billion

- Incremental cost: <5 RMB/MWh

- Use of cash: R&D in hydrogen/CCS

Huaneng: CNY 50–58bn EBITDA cash cows fuel CNY 32–36bn FCF for renewables

Huaneng’s coal ultra-supercritical fleet, district heating, hydro, ports/logistics, and Power Trading are stable cash cows: combined 2024 EBITDA ~CNY 50–58bn, FCF funding renewables (2024 free cash ~CNY 32–36bn), maintenance capex ~CNY 5–6bn, and dividends sustained; heat sales CNY 8.5bn; hydropower ~48 TWh; trading cash ~RMB 28.5bn.

| Segment | 2024 Metric | Cash/EBITDA |

|---|---|---|

| Coal fleet | >60% CF; 35–40% EBITDA | CNY 28–32bn |

| District heating | 12M users; CNY 8.5bn | 25–30% margin |

| Hydro | ~48 TWh | ~45% margin |

| Ports/logistics | serves ~70 GW | ~28% EBITDA |

| Trading | ~220 TWh sold | RMB 28.5bn OCF |

What You See Is What You Get

Huaneng Power International BCG Matrix

The Huaneng Power International BCG Matrix you’re previewing is the exact file you’ll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready report tailored for strategic decision-making. This preview mirrors the final deliverable, crafted with market-backed insights and clear visuals so you can immediately edit, print, or present without additional adjustments. Purchase grants instant download and direct delivery to your inbox for immediate use.