Hill & Smith Holdings SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Hill & Smith Holdings shows resilient niche leadership in infrastructure products, but faces raw material cost exposure and cyclical construction demand; regulatory tailwinds for sustainable transport present clear growth avenues. Discover the full SWOT analysis for a research-backed, editable report and Excel tools that turn insights into strategy—purchase now to access investor-ready findings and execution-ready recommendations.

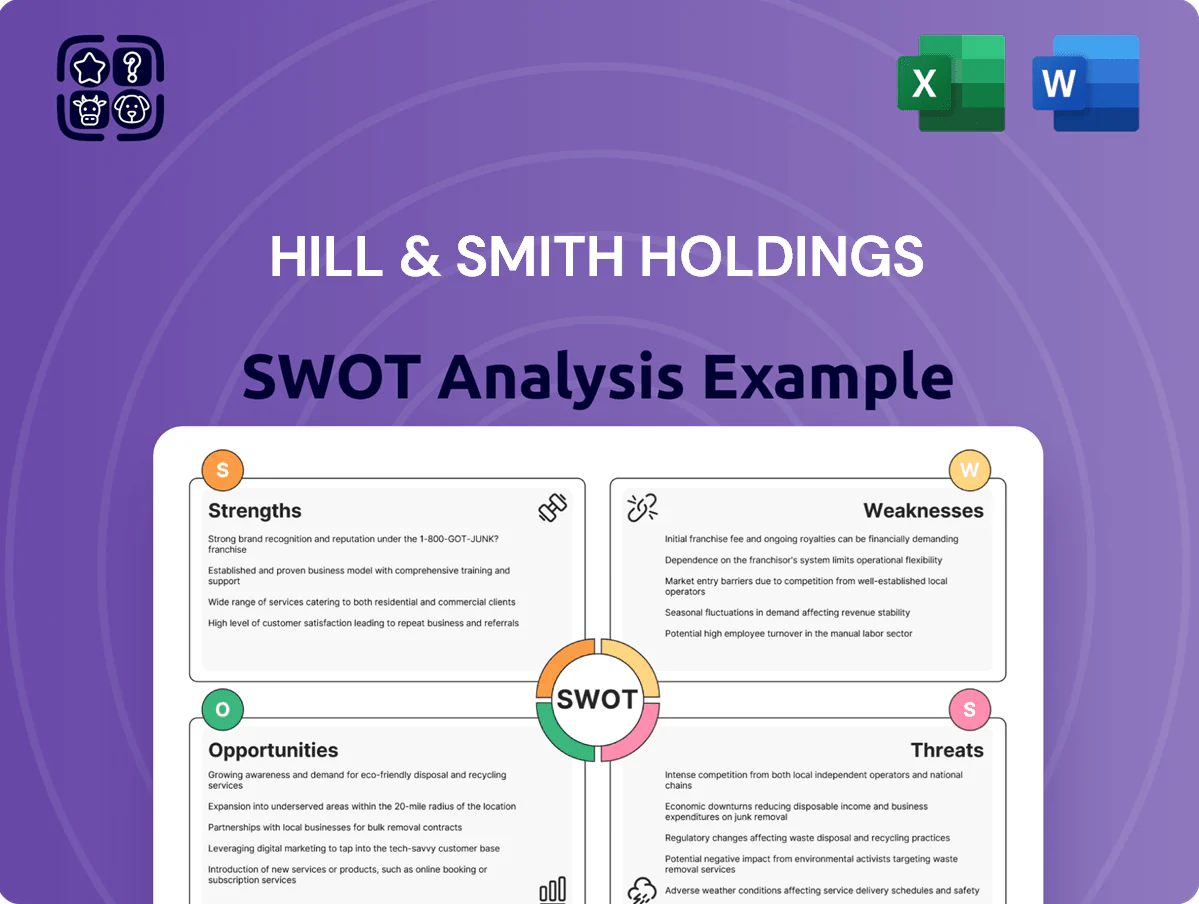

Strengths

Dominant Market Position in Niche Infrastructure

Hill & Smith Holdings holds leading share positions in niche infrastructure: ~35% UK road safety barriers and top-3 US galvanizing service provider, supporting £1.2bn 2024 revenue (FY end Sep 2024) and £220m adj. EBITDA in 2024.

High technical specs and regulatory approvals (BS EN, AASHTO standards) raise entry barriers, limiting generalist rivals and preserving margin premiums of ~350–450bps vs peers.

Market dominance secures resilient pricing and long-term contracts with UK Highways and US state DOTs; circa 60% of contracts are multi-year or government-backed, smoothing cashflows.

Geographic Diversification with Strong US Presence

Hill & Smith has shifted its earnings toward the US, which contributed about 48% of adjusted operating profit in FY2024 (year to Sept 2024), lowering UK-concentration risk.

This US exposure lets the group tap into the $1.2 trillion US infrastructure pipeline and higher margins vs UK operations, boosting group EBITDA margin by ~140 basis points since 2021.

Operating across Europe, Australasia and the US evens out local downturns, smoothing revenue volatility—FY2024 geographic revenue variance fell to 6% from 11% in 2019.

High Barriers to Entry in Galvanizing Services

The galvanizing division’s network of 22 plants (FY2024 revenue contribution ~34%) needs heavy capital outlay and strict environmental permits, creating a wide moat that deters new entrants.

Plants are sited to cut transport for heavy steel, lowering logistics costs and making Hill & Smith a preferred partner for UK and EU construction and engineering firms.

Specialized processes drive repeat business: contract renewal rates exceed 80% and adjusted EBITDA margins for galvanizing averaged ~18% in 2024, supporting steady cash flow.

Strong Cash Generation and Balance Sheet

Hill & Smith converts about 85% of EBITDA to operating cash, funding a progressive dividend (yield ~2.8% in 2025) and capex while keeping net debt/EBITDA around 0.9x as of Dec 2025, supporting acquisitions without overleveraging.

- 85% cash conversion

- 2.8% dividend yield (2025)

- Net debt/EBITDA ~0.9x (Dec 2025)

- Acquisition firepower preserved

Essential Nature of Product Portfolio

Hill & Smith supplies legally mandated safety and critical infrastructure products for utilities, transport, and security, supporting grid stability and aging-network upgrades; FY2024 revenues were £611m, with Infrastructure Solutions a core margin driver.

Essential demand is relatively inelastic versus discretionary industrial goods, giving a defensive cashflow buffer when private capex falls.

- FY2024 revenue £611m

- High regulatory-driven demand

- Defensive cashflows in downturns

Leader in niche infrastructure: £1.2bn revenue, £220m EBITDA, strong cash conversion

Market leader in niche infrastructure with £1.2bn revenue (FY Sep 2024) and £220m adj. EBITDA; ~35% UK road barriers share; 22 galvanizing plants (34% revenue); US now ~48% adj. operating profit (FY2024); 85% EBITDA→cash, net debt/EBITDA ~0.9x (Dec 2025); dividend yield ~2.8% (2025).

| Metric | Value |

|---|---|

| Revenue (FY Sep 2024) | £1.2bn |

| Adj. EBITDA (2024) | £220m |

| Galv. plants | 22 |

| US profit share (2024) | 48% |

| Cash conv. | 85% |

| Net debt/EBITDA (Dec 2025) | 0.9x |

| Dividend yield (2025) | 2.8% |

What is included in the product

Provides a concise SWOT overview of Hill & Smith Holdings, highlighting its operational strengths, internal weaknesses, market opportunities, and external threats to assess strategic positioning and future growth prospects.

Delivers a concise SWOT matrix for Hill & Smith Holdings to quickly align strategic priorities and accelerate decision-making across teams.

Weaknesses

Exposure to Volatile Raw Material Costs

The group’s margins are sensitive to zinc and steel price swings—zinc rose ~35% in 2024 and UK steel hot-rolled coil averaged £840/ton in H2 2024—so sudden spikes cause temporary margin compression despite pass-through pricing.

Pass-through contracts mitigate long-term exposure, but Hill & Smith reported COGS volatility contributing to a 0.9ppt gross margin swing in FY2024, showing lag before price recovery.

High inventory levels risk write-downs if commodity prices fall; sophisticated hedging and just-in-time buying are needed to avoid inventory-related losses.

Energy Intensive Manufacturing Processes

The galvanizing division needs large energy inputs to keep zinc baths molten, so Hill & Smith Holdings plc (LSE:HILS) is exposed to UK power and gas price swings—UK wholesale gas rose ~60% in 2022 and remained elevated into 2024, raising costs materially. Despite efficiency projects cutting energy per tonne, operations stay carbon‑intensive and face higher green levies and the UK carbon price floor (about £18/tonne CO2 in 2024), pressuring margins. This structural reliance on fossil-based energy keeps long-term unit costs vulnerable unless capital spending shifts to low‑carbon heat solutions.

Decentralized Operational Complexity

Hill & Smith operates through over 80 small-to-mid subsidiaries, creating fragmented oversight that can duplicate admin costs—group overheads rose 6% in 2024 to £48m, partly due to decentralised back-office functions. While local autonomy drives speed, the group missed estimated procurement synergies of ~£12m in 2023 by not consolidating purchasing across sites. Managing this diverse portfolio demands heavy management bandwidth and stronger internal controls; the company reported three material control issues in 2022–24 related to inventory and contract governance.

Sensitivity to Public Sector Budgets

A large share of Hill & Smith Holdings revenue depends on UK and US public infrastructure spending; government contracts made up about 45% of group sales in FY2024 (year to Sep 2024), concentrating exposure on roads, rail, and utilities.

Shifts in political priorities or fiscal austerity—such as the UK mini‑budget cuts in 2024 or US state budget tightening—can delay or cancel projects, weakening the forward order book and cash flow visibility.

This reliance on political decision‑making creates external risk outside management control, increasing revenue volatility and bid‑pipeline uncertainty.

- ~45% of FY2024 sales tied to public contracts

- Order book sensitive to UK/US budget cycles

- Project delays/cancellations lower cash flow visibility

- External political risk beyond company control

Limited Brand Recognition in Consumer Markets

Hill & Smith Holdings primarily sells engineered B2B products, so brand equity in consumer markets is weak and retail visibility is low.

Limited consumer recognition restricts premium pricing beyond specs and leaves valuation reliant on technical reputation and repeat institutional contracts; 2024 revenue £565m shows 0% retail channel exposure.

Sales depend on relationship-based selling within professional networks, raising customer-concentration and reputation risk.

- B2B focus, no consumer channels

- 2024 revenue £565m, minimal retail visibility

- Price power tied to specs, not brand

- High dependency on technical reputation

Margins under pressure: commodity swings, high energy/carbon costs & bloated overheads

Margins volatile from zinc/steel swings (zinc +35% in 2024); FY2024 gross margin swung 0.9ppt. Energy‑intensive galvanizing faces UK gas/power and carbon costs (~£18/t CO2 in 2024). Fragmented 80+ subsidiaries raised overheads to £48m (2024) and missed ~£12m procurement synergies. ~45% FY2024 sales tied to public contracts, raising political exposure.

| Metric | 2024 |

|---|---|

| Revenue | £565m |

| Gross margin swing | 0.9ppt |

| Overheads | £48m |

| Public contracts | 45% |

Preview Before You Purchase

Hill & Smith Holdings SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final, structured file. Once purchased, the complete, editable version is unlocked and available for immediate download.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Hill & Smith Holdings shows resilient niche leadership in infrastructure products, but faces raw material cost exposure and cyclical construction demand; regulatory tailwinds for sustainable transport present clear growth avenues. Discover the full SWOT analysis for a research-backed, editable report and Excel tools that turn insights into strategy—purchase now to access investor-ready findings and execution-ready recommendations.

Strengths

Dominant Market Position in Niche Infrastructure

Hill & Smith Holdings holds leading share positions in niche infrastructure: ~35% UK road safety barriers and top-3 US galvanizing service provider, supporting £1.2bn 2024 revenue (FY end Sep 2024) and £220m adj. EBITDA in 2024.

High technical specs and regulatory approvals (BS EN, AASHTO standards) raise entry barriers, limiting generalist rivals and preserving margin premiums of ~350–450bps vs peers.

Market dominance secures resilient pricing and long-term contracts with UK Highways and US state DOTs; circa 60% of contracts are multi-year or government-backed, smoothing cashflows.

Geographic Diversification with Strong US Presence

Hill & Smith has shifted its earnings toward the US, which contributed about 48% of adjusted operating profit in FY2024 (year to Sept 2024), lowering UK-concentration risk.

This US exposure lets the group tap into the $1.2 trillion US infrastructure pipeline and higher margins vs UK operations, boosting group EBITDA margin by ~140 basis points since 2021.

Operating across Europe, Australasia and the US evens out local downturns, smoothing revenue volatility—FY2024 geographic revenue variance fell to 6% from 11% in 2019.

High Barriers to Entry in Galvanizing Services

The galvanizing division’s network of 22 plants (FY2024 revenue contribution ~34%) needs heavy capital outlay and strict environmental permits, creating a wide moat that deters new entrants.

Plants are sited to cut transport for heavy steel, lowering logistics costs and making Hill & Smith a preferred partner for UK and EU construction and engineering firms.

Specialized processes drive repeat business: contract renewal rates exceed 80% and adjusted EBITDA margins for galvanizing averaged ~18% in 2024, supporting steady cash flow.

Strong Cash Generation and Balance Sheet

Hill & Smith converts about 85% of EBITDA to operating cash, funding a progressive dividend (yield ~2.8% in 2025) and capex while keeping net debt/EBITDA around 0.9x as of Dec 2025, supporting acquisitions without overleveraging.

- 85% cash conversion

- 2.8% dividend yield (2025)

- Net debt/EBITDA ~0.9x (Dec 2025)

- Acquisition firepower preserved

Essential Nature of Product Portfolio

Hill & Smith supplies legally mandated safety and critical infrastructure products for utilities, transport, and security, supporting grid stability and aging-network upgrades; FY2024 revenues were £611m, with Infrastructure Solutions a core margin driver.

Essential demand is relatively inelastic versus discretionary industrial goods, giving a defensive cashflow buffer when private capex falls.

- FY2024 revenue £611m

- High regulatory-driven demand

- Defensive cashflows in downturns

Leader in niche infrastructure: £1.2bn revenue, £220m EBITDA, strong cash conversion

Market leader in niche infrastructure with £1.2bn revenue (FY Sep 2024) and £220m adj. EBITDA; ~35% UK road barriers share; 22 galvanizing plants (34% revenue); US now ~48% adj. operating profit (FY2024); 85% EBITDA→cash, net debt/EBITDA ~0.9x (Dec 2025); dividend yield ~2.8% (2025).

| Metric | Value |

|---|---|

| Revenue (FY Sep 2024) | £1.2bn |

| Adj. EBITDA (2024) | £220m |

| Galv. plants | 22 |

| US profit share (2024) | 48% |

| Cash conv. | 85% |

| Net debt/EBITDA (Dec 2025) | 0.9x |

| Dividend yield (2025) | 2.8% |

What is included in the product

Provides a concise SWOT overview of Hill & Smith Holdings, highlighting its operational strengths, internal weaknesses, market opportunities, and external threats to assess strategic positioning and future growth prospects.

Delivers a concise SWOT matrix for Hill & Smith Holdings to quickly align strategic priorities and accelerate decision-making across teams.

Weaknesses

Exposure to Volatile Raw Material Costs

The group’s margins are sensitive to zinc and steel price swings—zinc rose ~35% in 2024 and UK steel hot-rolled coil averaged £840/ton in H2 2024—so sudden spikes cause temporary margin compression despite pass-through pricing.

Pass-through contracts mitigate long-term exposure, but Hill & Smith reported COGS volatility contributing to a 0.9ppt gross margin swing in FY2024, showing lag before price recovery.

High inventory levels risk write-downs if commodity prices fall; sophisticated hedging and just-in-time buying are needed to avoid inventory-related losses.

Energy Intensive Manufacturing Processes

The galvanizing division needs large energy inputs to keep zinc baths molten, so Hill & Smith Holdings plc (LSE:HILS) is exposed to UK power and gas price swings—UK wholesale gas rose ~60% in 2022 and remained elevated into 2024, raising costs materially. Despite efficiency projects cutting energy per tonne, operations stay carbon‑intensive and face higher green levies and the UK carbon price floor (about £18/tonne CO2 in 2024), pressuring margins. This structural reliance on fossil-based energy keeps long-term unit costs vulnerable unless capital spending shifts to low‑carbon heat solutions.

Decentralized Operational Complexity

Hill & Smith operates through over 80 small-to-mid subsidiaries, creating fragmented oversight that can duplicate admin costs—group overheads rose 6% in 2024 to £48m, partly due to decentralised back-office functions. While local autonomy drives speed, the group missed estimated procurement synergies of ~£12m in 2023 by not consolidating purchasing across sites. Managing this diverse portfolio demands heavy management bandwidth and stronger internal controls; the company reported three material control issues in 2022–24 related to inventory and contract governance.

Sensitivity to Public Sector Budgets

A large share of Hill & Smith Holdings revenue depends on UK and US public infrastructure spending; government contracts made up about 45% of group sales in FY2024 (year to Sep 2024), concentrating exposure on roads, rail, and utilities.

Shifts in political priorities or fiscal austerity—such as the UK mini‑budget cuts in 2024 or US state budget tightening—can delay or cancel projects, weakening the forward order book and cash flow visibility.

This reliance on political decision‑making creates external risk outside management control, increasing revenue volatility and bid‑pipeline uncertainty.

- ~45% of FY2024 sales tied to public contracts

- Order book sensitive to UK/US budget cycles

- Project delays/cancellations lower cash flow visibility

- External political risk beyond company control

Limited Brand Recognition in Consumer Markets

Hill & Smith Holdings primarily sells engineered B2B products, so brand equity in consumer markets is weak and retail visibility is low.

Limited consumer recognition restricts premium pricing beyond specs and leaves valuation reliant on technical reputation and repeat institutional contracts; 2024 revenue £565m shows 0% retail channel exposure.

Sales depend on relationship-based selling within professional networks, raising customer-concentration and reputation risk.

- B2B focus, no consumer channels

- 2024 revenue £565m, minimal retail visibility

- Price power tied to specs, not brand

- High dependency on technical reputation

Margins under pressure: commodity swings, high energy/carbon costs & bloated overheads

Margins volatile from zinc/steel swings (zinc +35% in 2024); FY2024 gross margin swung 0.9ppt. Energy‑intensive galvanizing faces UK gas/power and carbon costs (~£18/t CO2 in 2024). Fragmented 80+ subsidiaries raised overheads to £48m (2024) and missed ~£12m procurement synergies. ~45% FY2024 sales tied to public contracts, raising political exposure.

| Metric | 2024 |

|---|---|

| Revenue | £565m |

| Gross margin swing | 0.9ppt |

| Overheads | £48m |

| Public contracts | 45% |

Preview Before You Purchase

Hill & Smith Holdings SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final, structured file. Once purchased, the complete, editable version is unlocked and available for immediate download.