Tianshui Huatian Technology Porter's Five Forces Analysis

From Overview to Strategy Blueprint

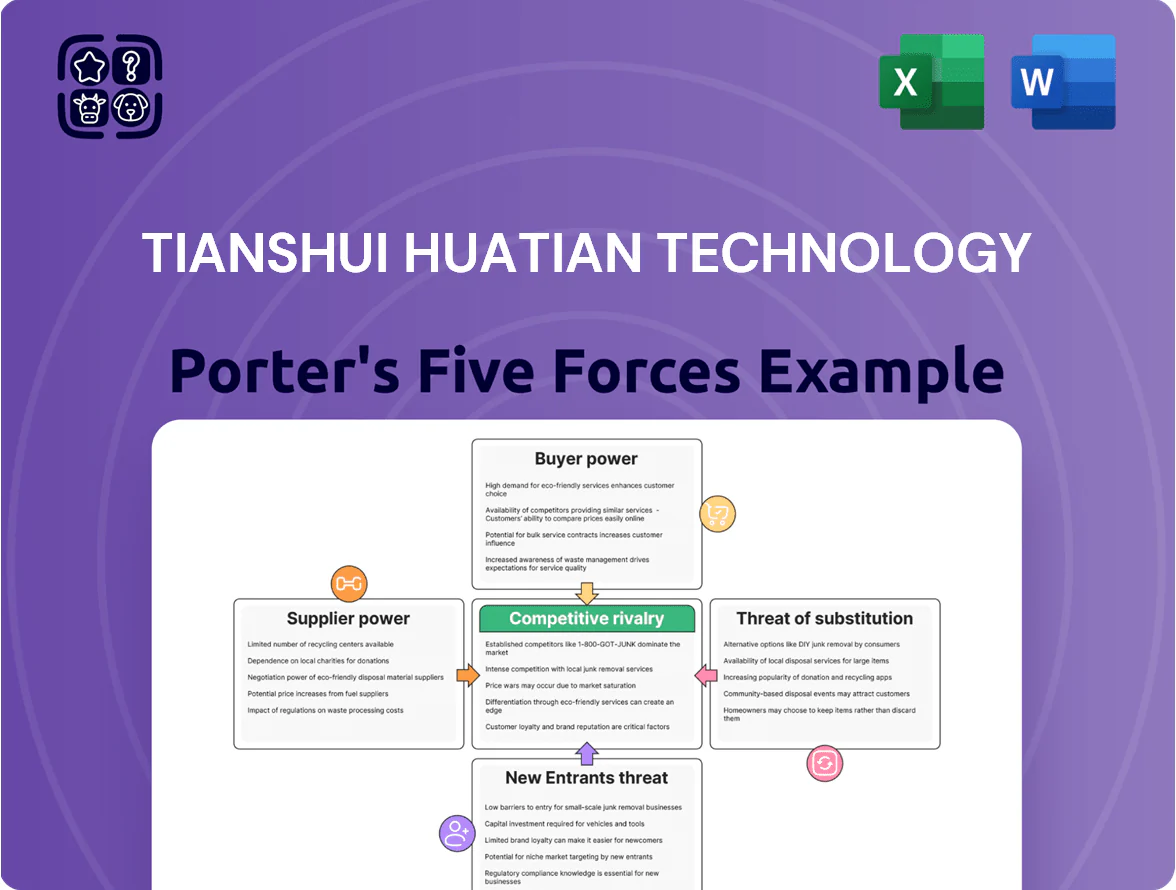

Tianshui Huatian navigates a capital-intensive semiconductor supply chain with moderate supplier power, rising buyer expectations for quality and price, and significant rivalry from domestic and global wafer foundries—while barriers to entry remain high due to tech and scale requirements. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of specialized equipment vendors

The market for high-end semiconductor assembly and test machinery is concentrated among a few global suppliers from Japan, the US, and Europe, with the top 5 vendors controlling roughly 70–80% of advanced wire bonders and lithography tool sales as of 2025.

Tianshui Huatian depends on these specific vendors for advanced wire bonders and lithography tools, which limits its ability to negotiate price or secure favorable lead times.

Switching vendors is technically hard and capital-intensive: a new bonder or lithography system costs $3–15 million and requires 6–18 months of process requalification, raising supplier bargaining power markedly.

Volatility in raw material pricing

Key inputs—gold, copper, and epoxy molding compounds—track global commodity swings: gold rose ~12% in 2024 and copper averaged $9,200/ton in 2024, pushing COGS up ~6–9% for semiconductor packaging peers. Suppliers gain leverage in tight demand cycles; Huatian often absorbs price rises to keep production running or pays premiums, squeezing gross margins that were 22.7% in 2024 for the firm’s sector peers.

Technological exclusivity of chemicals and substrates

Advanced packaging for Tianshui Huatian depends on patented chemical precursors and high-density substrates from a handful of global suppliers; these firms capture strong bargaining power since their materials are essential to meet node-specific specs and failure rates under 0.1% yield targets. In 2024, China imported ~80% of high-end substrates by value, and suppliers’ price premiums reached 15–30%, leaving limited room for negotiation.

Energy dependency and utility costs

Energy dependency is high: Tianshui Huatian’s testing fabs need continuous power and gases, with electricity use likely in the tens of MW range and gas volumes large for process stability.

Local utilities in Gansu are often state-controlled, limiting rate negotiation and exposing margins to tariff moves; a 10% electricity price rise could cut operating margin several percentage points.

Policy shifts—subsidy removal or peak pricing—would directly raise per-wafer test costs and capitalize into higher break-even thresholds.

- High constant load: tens of MW typical

- State/local utility dominance limits bargaining

- 10% power hike → several ppt margin hit

- Policy changes raise per-wafer test cost

Intellectual property and licensing fees

Access to proprietary packaging architectures forces Tianshui Huatian Technology to sign licensing deals with IP holders; in 2024 Huatian paid an estimated 2–4% of revenue in royalty-like fees for certain wafer-packaging tech, cutting margins on advanced service lines.

These licensors act as suppliers of IP and wield high bargaining power because firms without licenses lose global competitiveness; dependence on a few patent families concentrates negotiation leverage and risks higher fees or restrictive terms.

Here’s the quick math: if licensed lines generate 30% of revenue and royalties average 3%, gross margin falls ~0.9 percentage points; what this hides: fee tiers can jump sharply for next-gen nodes.

- Licensing fees ~2–4% revenue (2024 est.)

- Licensed lines ≈30% of revenue

- Estimated margin hit ≈0.9 pp

- Few patent holders ⇒ concentrated supplier power

Supplier concentration, commodity costs & energy risk squeeze margins

Suppliers hold high bargaining power: top 5 tool vendors control ~70–80% of advanced equipment (2025), key materials (substrates, gold, copper, epoxy) drove COGS +6–9% in 2024, and IP royalties (~2–4% of revenue, 2024 est.) cut gross margin ~0.9 ppt; energy (tens of MW) from state utilities adds tariff risk—10% electricity rise can shave several ppt off operating margin.

| Metric | Value (year) |

|---|---|

| Top-5 tool share | 70–80% (2025) |

| COGS impact from commodities | +6–9% (2024) |

| Royalty rate | 2–4% rev (2024 est.) |

| Royalty margin hit | ~0.9 ppt |

| Electricity load | tens of MW |

| 10% power rise effect | several ppt margin loss |

What is included in the product

Tailored Porter's Five Forces analysis of Tianshui Huatian Technology uncovering competitive drivers, buyer and supplier power, threat of substitutes and entrants, and strategic levers to protect market share and pricing power.

A concise Porter's Five Forces snapshot for Tianshui Huatian—quickly highlights supplier, buyer, competitor, entrant, and substitution pressures to speed strategic decisions.

Customers Bargaining Power

High concentration of major fabless clients

A large share—about 62% of Tianshui Huatian Technology’s 2024 revenue—came from just three fabless customers, giving them strong bargaining power to demand volume discounts of 5–12% and extended payment terms beyond 90 days.

Those customers’ scale also pressures margins: gross margin fell 240 basis points year‑over‑year in 2024 when one client renegotiated pricing.

If a primary customer representing ~20% of sales shifts to a rival, Tianshui Huatian would face an immediate revenue shortfall and likely may need price cuts or capacity underutilization to retain other clients.

Standardization of legacy packaging services

For mature packaging technologies, Tianshui Huatian faces high buyer power: industry surveys show commoditized OSAT services drive 70–80% of customers to choose solely on price and 20–30% shorter lead times (2024 data), so clients can switch vendors with minimal friction. This standardization compresses margins; price-sensitive buyers push for discounts of 5–15% on back-end fees, increasing negotiation leverage and raising churn risk if Huatian cannot match peers on cost or speed.

Threat of customer backward integration

Large integrated device makers and tech giants like Apple and Samsung (who spent >$12B on chip-related capex in 2023–24) can and have moved packaging and testing in-house, cutting reliance on providers such as Tianshui Huatian; this trend pressured OSAT pricing by ~3–6% in 2024 industry reports.

Strict quality and performance requirements

Customers in automotive and industrial segments insist on ISO/TS 16949-equivalent testing and 1–5 million-cycle reliability proofs, giving them leverage to specify production processes and incoming inspection metrics.

These strict specs raise entry barriers and force Huatian to absorb compliance costs—testing, rework, and certification—often 3–8% of contract value; losing certification risks multimillion-yuan penalties and order cancellations.

Availability of alternative global OSAT providers

Customers benefit from many large OSAT (outsourced semiconductor assembly and test) providers across Taiwan, Southeast Asia, and mainland China, giving them clear alternatives to Tianshui Huatian Technology and lowering switching costs.

Buyers leverage global OSAT capacity—Taiwan, ASE Technology Holding leads with 2024 revenues of US$7.3B, while JCET Group reported RMB 32.1B (2024)—to pressure pricing and terms during contract talks.

Market pricing transparency and excess capacity in 2024 (industry utilisation near 80% vs peak 95%) concentrate bargaining power with customers, forcing tighter margins for smaller OSATs like Tianshui Huatian.

- Multiple regional giants: Taiwan, SEA, China

- ASE 2024 rev US$7.3B; JCET 2024 rev RMB 32.1B

- Industry utilization ~80% in 2024

- High buyer leverage on price and terms

Customer Concentration & Pricing Pressure: Top-3 = 62%, Buyers Extract 5–15% Discounts

Customers hold high bargaining power: three clients drove ~62% of 2024 revenue, extracting 5–12% discounts and >90-day terms; one renegotiation cut gross margin by 240 bps. Commoditized OSAT services and ~80% industry utilization in 2024 give buyers pricing leverage (5–15% typical discounts); large players (ASE US$7.3B, JCET RMB32.1B in 2024) and in‑house moves trimmed OSAT pricing 3–6%.

| Metric | 2024 |

|---|---|

| Top‑3 customer share | ~62% |

| Industry util. | ~80% |

| ASE rev | US$7.3B |

| JCET rev | RMB32.1B |

What You See Is What You Get

Tianshui Huatian Technology Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Tianshui Huatian Technology you'll receive—no placeholders, no mockups, fully formatted for immediate use.

The document displayed is part of the full, final version available for instant download upon purchase and contains complete evaluation of competitive rivalry, supplier and buyer power, threats of entry and substitutes.

You're viewing the actual deliverable: concise, professional, and ready to inform strategic or investment decisions the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Tianshui Huatian navigates a capital-intensive semiconductor supply chain with moderate supplier power, rising buyer expectations for quality and price, and significant rivalry from domestic and global wafer foundries—while barriers to entry remain high due to tech and scale requirements. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of specialized equipment vendors

The market for high-end semiconductor assembly and test machinery is concentrated among a few global suppliers from Japan, the US, and Europe, with the top 5 vendors controlling roughly 70–80% of advanced wire bonders and lithography tool sales as of 2025.

Tianshui Huatian depends on these specific vendors for advanced wire bonders and lithography tools, which limits its ability to negotiate price or secure favorable lead times.

Switching vendors is technically hard and capital-intensive: a new bonder or lithography system costs $3–15 million and requires 6–18 months of process requalification, raising supplier bargaining power markedly.

Volatility in raw material pricing

Key inputs—gold, copper, and epoxy molding compounds—track global commodity swings: gold rose ~12% in 2024 and copper averaged $9,200/ton in 2024, pushing COGS up ~6–9% for semiconductor packaging peers. Suppliers gain leverage in tight demand cycles; Huatian often absorbs price rises to keep production running or pays premiums, squeezing gross margins that were 22.7% in 2024 for the firm’s sector peers.

Technological exclusivity of chemicals and substrates

Advanced packaging for Tianshui Huatian depends on patented chemical precursors and high-density substrates from a handful of global suppliers; these firms capture strong bargaining power since their materials are essential to meet node-specific specs and failure rates under 0.1% yield targets. In 2024, China imported ~80% of high-end substrates by value, and suppliers’ price premiums reached 15–30%, leaving limited room for negotiation.

Energy dependency and utility costs

Energy dependency is high: Tianshui Huatian’s testing fabs need continuous power and gases, with electricity use likely in the tens of MW range and gas volumes large for process stability.

Local utilities in Gansu are often state-controlled, limiting rate negotiation and exposing margins to tariff moves; a 10% electricity price rise could cut operating margin several percentage points.

Policy shifts—subsidy removal or peak pricing—would directly raise per-wafer test costs and capitalize into higher break-even thresholds.

- High constant load: tens of MW typical

- State/local utility dominance limits bargaining

- 10% power hike → several ppt margin hit

- Policy changes raise per-wafer test cost

Intellectual property and licensing fees

Access to proprietary packaging architectures forces Tianshui Huatian Technology to sign licensing deals with IP holders; in 2024 Huatian paid an estimated 2–4% of revenue in royalty-like fees for certain wafer-packaging tech, cutting margins on advanced service lines.

These licensors act as suppliers of IP and wield high bargaining power because firms without licenses lose global competitiveness; dependence on a few patent families concentrates negotiation leverage and risks higher fees or restrictive terms.

Here’s the quick math: if licensed lines generate 30% of revenue and royalties average 3%, gross margin falls ~0.9 percentage points; what this hides: fee tiers can jump sharply for next-gen nodes.

- Licensing fees ~2–4% revenue (2024 est.)

- Licensed lines ≈30% of revenue

- Estimated margin hit ≈0.9 pp

- Few patent holders ⇒ concentrated supplier power

Supplier concentration, commodity costs & energy risk squeeze margins

Suppliers hold high bargaining power: top 5 tool vendors control ~70–80% of advanced equipment (2025), key materials (substrates, gold, copper, epoxy) drove COGS +6–9% in 2024, and IP royalties (~2–4% of revenue, 2024 est.) cut gross margin ~0.9 ppt; energy (tens of MW) from state utilities adds tariff risk—10% electricity rise can shave several ppt off operating margin.

| Metric | Value (year) |

|---|---|

| Top-5 tool share | 70–80% (2025) |

| COGS impact from commodities | +6–9% (2024) |

| Royalty rate | 2–4% rev (2024 est.) |

| Royalty margin hit | ~0.9 ppt |

| Electricity load | tens of MW |

| 10% power rise effect | several ppt margin loss |

What is included in the product

Tailored Porter's Five Forces analysis of Tianshui Huatian Technology uncovering competitive drivers, buyer and supplier power, threat of substitutes and entrants, and strategic levers to protect market share and pricing power.

A concise Porter's Five Forces snapshot for Tianshui Huatian—quickly highlights supplier, buyer, competitor, entrant, and substitution pressures to speed strategic decisions.

Customers Bargaining Power

High concentration of major fabless clients

A large share—about 62% of Tianshui Huatian Technology’s 2024 revenue—came from just three fabless customers, giving them strong bargaining power to demand volume discounts of 5–12% and extended payment terms beyond 90 days.

Those customers’ scale also pressures margins: gross margin fell 240 basis points year‑over‑year in 2024 when one client renegotiated pricing.

If a primary customer representing ~20% of sales shifts to a rival, Tianshui Huatian would face an immediate revenue shortfall and likely may need price cuts or capacity underutilization to retain other clients.

Standardization of legacy packaging services

For mature packaging technologies, Tianshui Huatian faces high buyer power: industry surveys show commoditized OSAT services drive 70–80% of customers to choose solely on price and 20–30% shorter lead times (2024 data), so clients can switch vendors with minimal friction. This standardization compresses margins; price-sensitive buyers push for discounts of 5–15% on back-end fees, increasing negotiation leverage and raising churn risk if Huatian cannot match peers on cost or speed.

Threat of customer backward integration

Large integrated device makers and tech giants like Apple and Samsung (who spent >$12B on chip-related capex in 2023–24) can and have moved packaging and testing in-house, cutting reliance on providers such as Tianshui Huatian; this trend pressured OSAT pricing by ~3–6% in 2024 industry reports.

Strict quality and performance requirements

Customers in automotive and industrial segments insist on ISO/TS 16949-equivalent testing and 1–5 million-cycle reliability proofs, giving them leverage to specify production processes and incoming inspection metrics.

These strict specs raise entry barriers and force Huatian to absorb compliance costs—testing, rework, and certification—often 3–8% of contract value; losing certification risks multimillion-yuan penalties and order cancellations.

Availability of alternative global OSAT providers

Customers benefit from many large OSAT (outsourced semiconductor assembly and test) providers across Taiwan, Southeast Asia, and mainland China, giving them clear alternatives to Tianshui Huatian Technology and lowering switching costs.

Buyers leverage global OSAT capacity—Taiwan, ASE Technology Holding leads with 2024 revenues of US$7.3B, while JCET Group reported RMB 32.1B (2024)—to pressure pricing and terms during contract talks.

Market pricing transparency and excess capacity in 2024 (industry utilisation near 80% vs peak 95%) concentrate bargaining power with customers, forcing tighter margins for smaller OSATs like Tianshui Huatian.

- Multiple regional giants: Taiwan, SEA, China

- ASE 2024 rev US$7.3B; JCET 2024 rev RMB 32.1B

- Industry utilization ~80% in 2024

- High buyer leverage on price and terms

Customer Concentration & Pricing Pressure: Top-3 = 62%, Buyers Extract 5–15% Discounts

Customers hold high bargaining power: three clients drove ~62% of 2024 revenue, extracting 5–12% discounts and >90-day terms; one renegotiation cut gross margin by 240 bps. Commoditized OSAT services and ~80% industry utilization in 2024 give buyers pricing leverage (5–15% typical discounts); large players (ASE US$7.3B, JCET RMB32.1B in 2024) and in‑house moves trimmed OSAT pricing 3–6%.

| Metric | 2024 |

|---|---|

| Top‑3 customer share | ~62% |

| Industry util. | ~80% |

| ASE rev | US$7.3B |

| JCET rev | RMB32.1B |

What You See Is What You Get

Tianshui Huatian Technology Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Tianshui Huatian Technology you'll receive—no placeholders, no mockups, fully formatted for immediate use.

The document displayed is part of the full, final version available for instant download upon purchase and contains complete evaluation of competitive rivalry, supplier and buyer power, threats of entry and substitutes.

You're viewing the actual deliverable: concise, professional, and ready to inform strategic or investment decisions the moment you buy.