Tianshui Huatian Technology PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

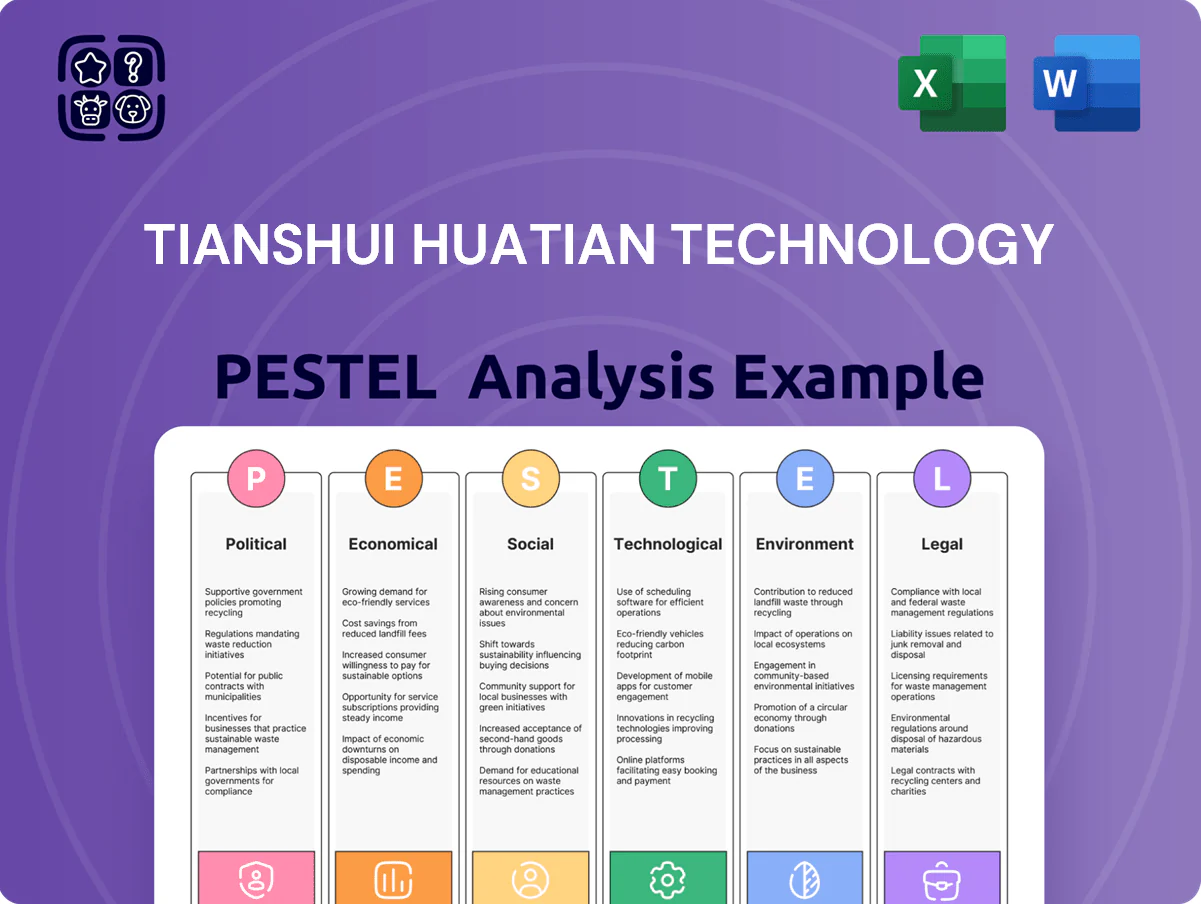

Our PESTLE Analysis for Tianshui Huatian Technology pinpoints the political, economic, social, technological, legal, and environmental forces shaping its trajectory—revealing regulatory risks, supply-chain pressures, and innovation opportunities that matter to investors and strategists; purchase the full report to access actionable insights, data-backed scenarios, and ready-to-use slides for strategic decisions.

Political factors

Geopolitical Trade Restrictions

The US-China semiconductor trade war imposes strict export controls on equipment and materials, forcing Tianshui Huatian to navigate licensing limits that affected 22% of its imported tools in 2024; by late 2025 the company accelerated sourcing domestic alternatives, raising local procurement to 35% of capex on critical production tools. The firm must monitor policy shifts continuously to mitigate cross-border supply chain disruption risks and potential revenue impact up to mid-single-digit percentage points.

Government Subsidies and Support

Domestic Industrial Policy

China's Made in China 2025 and 14th Five-Year Plan prioritize advanced IC packaging, driving policy support for localization; Tianshui Huatian benefits as government targets cut wafer-to-package import dependency and boost domestic OSATs, with state funding programs allocating over CNY 300 billion to semiconductor projects in 2023–2025. Aligning strategy to national goals secures state-backed contracts and collaborations with SOEs, supporting revenue stability and capex co-financing.

Regional Geopolitical Stability

Tianshui Huatian’s role in the semiconductor chain makes it vulnerable to East Asia instability, especially Taiwan Strait risks; a 2024 IHS estimate showed 60–70% of leading-edge wafers routed via Taiwan/SEA, exposing packaging hubs to disruption. Management must diversify logistics and maintain contingency plans; revenue at risk given the company’s 2024 gross margin sensitivity to supply delays.

- 60–70% wafers via Taiwan/SEA (2024 IHS)

- Maintain diversified routes and contingency plans

- Operational continuity critical to protect gross margins

International Standardization Compliance

- Engagement with JEDEC/ISO influenced by political relations

- 2024 export controls affected 12% of advanced packaging tool flows

- Domestic standard setting vs global compatibility for $600B market (2025)

China chips: 22% tool curbs, 35% local capex, Rmb1.2bn capex, >CNY300bn subsidies

US export controls hit 22% of imported tools in 2024; domestic sourcing rose to 35% of capex by late 2025, capex Rmb1.2bn in 2024 with subsidies covering 20–30%; central/local semiconductor subsidies >Rmb50bn in 2024 and >CNY300bn (2023–25); wafers routed via Taiwan/SEA 60–70% (2024); global advanced packaging market ~$600bn (2025).

| Metric | Value |

|---|---|

| Imported tools affected (2024) | 22% |

| Domestic capex sourcing (late 2025) | 35% |

| Capex (2024) | Rmb1.2bn |

| Subsidy share of capex | 20–30% |

| Semiconductor subsidies (2024) | >Rmb50bn |

| State projects funding (2023–25) | >CNY300bn |

| Wafers via Taiwan/SEA (2024) | 60–70% |

| Advanced packaging market (2025) | $600bn |

What is included in the product

Explores how macro-environmental factors uniquely affect Tianshui Huatian Technology across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current regional market and regulatory trends to identify risks and opportunities.

A concise PESTLE snapshot of Tianshui Huatian Technology that distills political, economic, social, technological, legal, and environmental factors for quick reference in meetings, aiding risk discussions and strategic alignment across teams.

Economic factors

Semiconductor Market Cyclicality

The semiconductor industry’s boom-and-bust cycles drive volatile demand for packaging and testing; global semiconductor revenue fell 13% in 2023 then recovered ~8% in 2024, underscoring volatility that directly affects Tianshui Huatian’s order flow. By end-2025 the company must optimize inventory and lift capacity utilization from its 2024 level (reported ~68%) to target >80% in downturns to protect margins. Robust economic forecasting and flexible production scheduling—including scalable subcontracting—are essential to navigate periodic shifts in global chip demand and preserve profitability.

Currency Exchange Rate Fluctuations

As an international exporter, Tianshui Huatian faces CNY/USD volatility—CNY moved about 6.8–7.3 per USD in 2024–2025—affecting price competitiveness and translating to ±5–8% swings in reported overseas revenue in recent quarters. Currency shifts also alter costs for imported high-end packaging machinery and specialty substrates, which comprise ~12% of COGS and rose 6% when CNY weakened in 2024. The company deploys hedges—forward contracts and FX options covering roughly 40–60% of expected FX exposure—to stabilize margins and cash flow.

Labor Cost Inflation

Rising wages in China’s industrial hubs—average manufacturing hourly wages up about 6.8% YoY in 2024—erode the low-cost edge OSATs enjoyed; Tianshui Huatian counters with a CNY 1.2bn (≈USD 170m) 2024–25 capex push into factory automation and smart manufacturing to reduce headcount growth and raise throughput by targeted 18% per line; balancing higher labor costs versus capital intensity remains a top economic priority for management.

Global Inflationary Pressures

Persistent global inflation raised commodity costs—copper up ~15% and gold ~8% in 2024 vs 2023; energy and chemical prices added ~10–20% to input costs for packaging suppliers.

Tianshui Huatian faces a trade-off between absorbing higher input costs or raising prices, risking margin compression or market-share loss; gross margin sensitivity to raw-material swings reached ~3–5 percentage points in 2024.

Company mitigation includes strategic procurement, hedging and multi-year supplier contracts covering ~40–60% of annual needs to reduce short-term volatility exposure.

- Copper +15% (2024 vs 2023)

- Gold +8% (2024 vs 2023)

- Energy/chemicals +10–20%

- Long-term contracts cover 40–60% of inputs

Interest Rate Environment

The prevailing interest rate environment in China directly affects Tianshui Huatian’s cost of debt for infrastructure and R&D; with the PBOC benchmark 1-year loan prime rate at 3.95% (2025 average) higher rates would constrain expansion, while easing toward 3.45% in 2024 would enable aggressive growth and acquisitions.

The firm actively manages capital structure and leverage—net debt/EBITDA targeted near 1.5x—to optimize financial health as credit conditions shift.

- 2024 LPR: 3.45%; 2025 avg LPR: 3.95%

- Target net debt/EBITDA ~1.5x

- Higher rates restrict capex and M&A

- Lower rates enable R&D and competitor acquisitions

Semiconductor recovery, rising utilization & input-cost pressure squeeze margins

Economic volatility (semiconductor revenue -13% in 2023, +8% in 2024) drives demand swings; utilization rose from ~68% (2024) target >80% by end-2025. CNY/USD ~6.8–7.3 (2024–25) produced ±5–8% revenue swings; hedges cover 40–60% exposure. Wages +6.8% (2024); capex CNY1.2bn to boost automation. Raw materials: copper +15%, gold +8%, energy/chemicals +10–20%; gross-margin sensitivity ~3–5pp.

| Metric | 2023 | 2024 | 2025 target |

|---|---|---|---|

| Global semiconductor rev | — | -13% / +8% recovery | — |

| Utilization | — | ~68% | >80% |

| CNY/USD | — | 6.8–7.3 | 6.8–7.3 |

| Wage growth | — | +6.8% | — |

| Capex | — | CNY1.2bn | — |

| Copper / Gold | — | +15% / +8% | — |

| Hedging / contracts | — | 40–60% coverage | — |

| Net debt/EBITDA target | — | ~1.5x | ~1.5x |

Same Document Delivered

Tianshui Huatian Technology PESTLE Analysis

The preview shown here is the exact Tianshui Huatian Technology PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and insights visible in this preview match the final downloadable file you’ll get immediately after payment, with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE Analysis for Tianshui Huatian Technology pinpoints the political, economic, social, technological, legal, and environmental forces shaping its trajectory—revealing regulatory risks, supply-chain pressures, and innovation opportunities that matter to investors and strategists; purchase the full report to access actionable insights, data-backed scenarios, and ready-to-use slides for strategic decisions.

Political factors

Geopolitical Trade Restrictions

The US-China semiconductor trade war imposes strict export controls on equipment and materials, forcing Tianshui Huatian to navigate licensing limits that affected 22% of its imported tools in 2024; by late 2025 the company accelerated sourcing domestic alternatives, raising local procurement to 35% of capex on critical production tools. The firm must monitor policy shifts continuously to mitigate cross-border supply chain disruption risks and potential revenue impact up to mid-single-digit percentage points.

Government Subsidies and Support

Domestic Industrial Policy

China's Made in China 2025 and 14th Five-Year Plan prioritize advanced IC packaging, driving policy support for localization; Tianshui Huatian benefits as government targets cut wafer-to-package import dependency and boost domestic OSATs, with state funding programs allocating over CNY 300 billion to semiconductor projects in 2023–2025. Aligning strategy to national goals secures state-backed contracts and collaborations with SOEs, supporting revenue stability and capex co-financing.

Regional Geopolitical Stability

Tianshui Huatian’s role in the semiconductor chain makes it vulnerable to East Asia instability, especially Taiwan Strait risks; a 2024 IHS estimate showed 60–70% of leading-edge wafers routed via Taiwan/SEA, exposing packaging hubs to disruption. Management must diversify logistics and maintain contingency plans; revenue at risk given the company’s 2024 gross margin sensitivity to supply delays.

- 60–70% wafers via Taiwan/SEA (2024 IHS)

- Maintain diversified routes and contingency plans

- Operational continuity critical to protect gross margins

International Standardization Compliance

- Engagement with JEDEC/ISO influenced by political relations

- 2024 export controls affected 12% of advanced packaging tool flows

- Domestic standard setting vs global compatibility for $600B market (2025)

China chips: 22% tool curbs, 35% local capex, Rmb1.2bn capex, >CNY300bn subsidies

US export controls hit 22% of imported tools in 2024; domestic sourcing rose to 35% of capex by late 2025, capex Rmb1.2bn in 2024 with subsidies covering 20–30%; central/local semiconductor subsidies >Rmb50bn in 2024 and >CNY300bn (2023–25); wafers routed via Taiwan/SEA 60–70% (2024); global advanced packaging market ~$600bn (2025).

| Metric | Value |

|---|---|

| Imported tools affected (2024) | 22% |

| Domestic capex sourcing (late 2025) | 35% |

| Capex (2024) | Rmb1.2bn |

| Subsidy share of capex | 20–30% |

| Semiconductor subsidies (2024) | >Rmb50bn |

| State projects funding (2023–25) | >CNY300bn |

| Wafers via Taiwan/SEA (2024) | 60–70% |

| Advanced packaging market (2025) | $600bn |

What is included in the product

Explores how macro-environmental factors uniquely affect Tianshui Huatian Technology across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current regional market and regulatory trends to identify risks and opportunities.

A concise PESTLE snapshot of Tianshui Huatian Technology that distills political, economic, social, technological, legal, and environmental factors for quick reference in meetings, aiding risk discussions and strategic alignment across teams.

Economic factors

Semiconductor Market Cyclicality

The semiconductor industry’s boom-and-bust cycles drive volatile demand for packaging and testing; global semiconductor revenue fell 13% in 2023 then recovered ~8% in 2024, underscoring volatility that directly affects Tianshui Huatian’s order flow. By end-2025 the company must optimize inventory and lift capacity utilization from its 2024 level (reported ~68%) to target >80% in downturns to protect margins. Robust economic forecasting and flexible production scheduling—including scalable subcontracting—are essential to navigate periodic shifts in global chip demand and preserve profitability.

Currency Exchange Rate Fluctuations

As an international exporter, Tianshui Huatian faces CNY/USD volatility—CNY moved about 6.8–7.3 per USD in 2024–2025—affecting price competitiveness and translating to ±5–8% swings in reported overseas revenue in recent quarters. Currency shifts also alter costs for imported high-end packaging machinery and specialty substrates, which comprise ~12% of COGS and rose 6% when CNY weakened in 2024. The company deploys hedges—forward contracts and FX options covering roughly 40–60% of expected FX exposure—to stabilize margins and cash flow.

Labor Cost Inflation

Rising wages in China’s industrial hubs—average manufacturing hourly wages up about 6.8% YoY in 2024—erode the low-cost edge OSATs enjoyed; Tianshui Huatian counters with a CNY 1.2bn (≈USD 170m) 2024–25 capex push into factory automation and smart manufacturing to reduce headcount growth and raise throughput by targeted 18% per line; balancing higher labor costs versus capital intensity remains a top economic priority for management.

Global Inflationary Pressures

Persistent global inflation raised commodity costs—copper up ~15% and gold ~8% in 2024 vs 2023; energy and chemical prices added ~10–20% to input costs for packaging suppliers.

Tianshui Huatian faces a trade-off between absorbing higher input costs or raising prices, risking margin compression or market-share loss; gross margin sensitivity to raw-material swings reached ~3–5 percentage points in 2024.

Company mitigation includes strategic procurement, hedging and multi-year supplier contracts covering ~40–60% of annual needs to reduce short-term volatility exposure.

- Copper +15% (2024 vs 2023)

- Gold +8% (2024 vs 2023)

- Energy/chemicals +10–20%

- Long-term contracts cover 40–60% of inputs

Interest Rate Environment

The prevailing interest rate environment in China directly affects Tianshui Huatian’s cost of debt for infrastructure and R&D; with the PBOC benchmark 1-year loan prime rate at 3.95% (2025 average) higher rates would constrain expansion, while easing toward 3.45% in 2024 would enable aggressive growth and acquisitions.

The firm actively manages capital structure and leverage—net debt/EBITDA targeted near 1.5x—to optimize financial health as credit conditions shift.

- 2024 LPR: 3.45%; 2025 avg LPR: 3.95%

- Target net debt/EBITDA ~1.5x

- Higher rates restrict capex and M&A

- Lower rates enable R&D and competitor acquisitions

Semiconductor recovery, rising utilization & input-cost pressure squeeze margins

Economic volatility (semiconductor revenue -13% in 2023, +8% in 2024) drives demand swings; utilization rose from ~68% (2024) target >80% by end-2025. CNY/USD ~6.8–7.3 (2024–25) produced ±5–8% revenue swings; hedges cover 40–60% exposure. Wages +6.8% (2024); capex CNY1.2bn to boost automation. Raw materials: copper +15%, gold +8%, energy/chemicals +10–20%; gross-margin sensitivity ~3–5pp.

| Metric | 2023 | 2024 | 2025 target |

|---|---|---|---|

| Global semiconductor rev | — | -13% / +8% recovery | — |

| Utilization | — | ~68% | >80% |

| CNY/USD | — | 6.8–7.3 | 6.8–7.3 |

| Wage growth | — | +6.8% | — |

| Capex | — | CNY1.2bn | — |

| Copper / Gold | — | +15% / +8% | — |

| Hedging / contracts | — | 40–60% coverage | — |

| Net debt/EBITDA target | — | ~1.5x | ~1.5x |

Same Document Delivered

Tianshui Huatian Technology PESTLE Analysis

The preview shown here is the exact Tianshui Huatian Technology PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and insights visible in this preview match the final downloadable file you’ll get immediately after payment, with no placeholders or surprises.