Hubbell Porter's Five Forces Analysis

Don't Miss the Bigger Picture

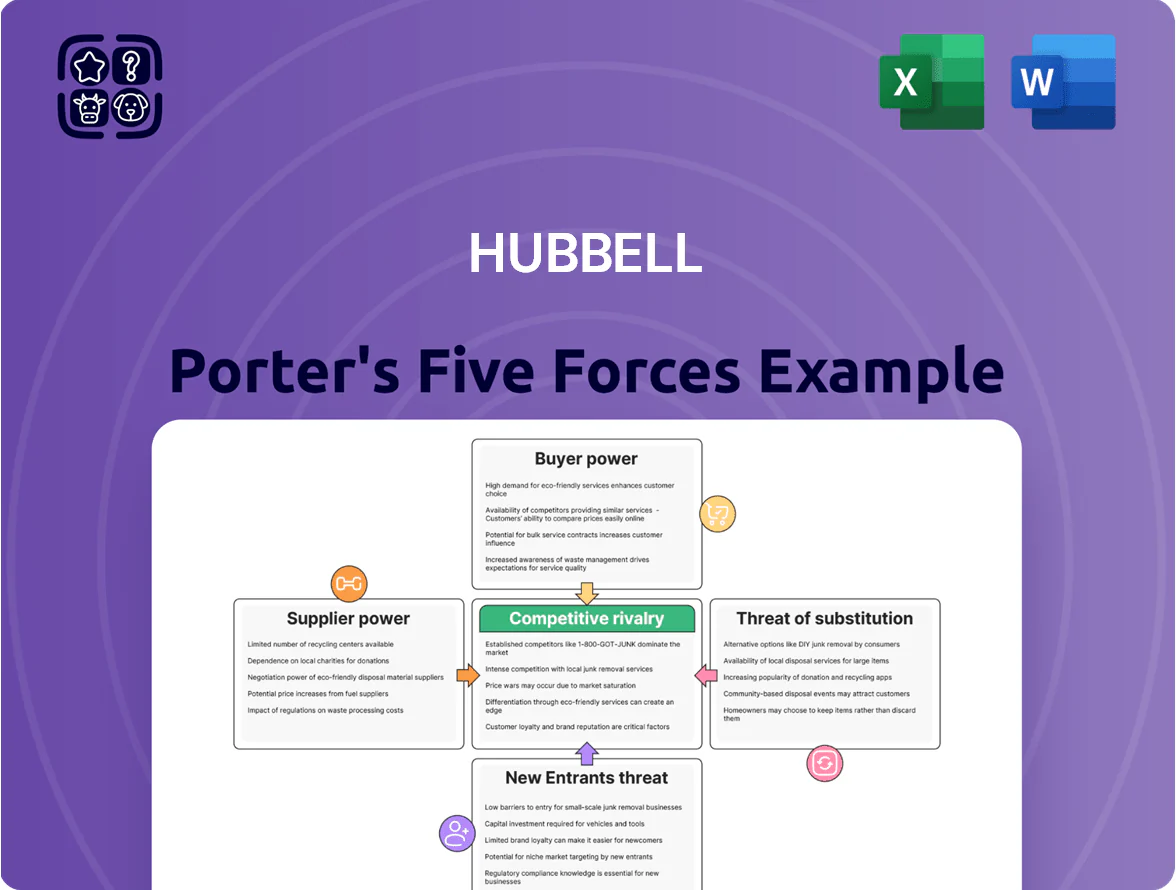

Hubbell’s Porter's Five Forces snapshot highlights its solid supplier relationships, moderate buyer power, and durable barriers to entry driven by scale and regulation, while flagging potential threats from substitutes and selective competition in niche segments. This brief overview points to where strategic advantages and vulnerabilities lie across the value chain. Ready to move beyond the basics? Get a full strategic breakdown of Hubbell’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Raw Material Price Volatility

Hubbell depends on copper, steel, aluminum and plastics; copper surged ~40% in 2021–2023 and was ~$9,000/ton in 2024, so raw-material swings materially affect COGS and margins.

Suppliers hold moderate power: Hubbell needs certified, high-quality inputs to meet NEC and UL standards, limiting supplier substitution and giving suppliers pricing leverage.

Specialized Component Dependencies

Certain Hubbell products need specialized semiconductors and proprietary sub-components from few vendors; supplier concentration gives those vendors pricing and lead-time leverage—Hubbell disclosed supply-chain pressures cut Q3 2025 sales by ~2.1% and added ~$12m in procurement premiums.

Dependency is sharpest in Utility Solutions, where precision and reliability are non-negotiable; 68% of that segment’s key parts sourced from three suppliers raises risk of single-vendor disruption and margin compression.

Global Supply Chain Logistics

Hubbell sources materials from Asia, Europe, and North America, so 2024 shipping disruptions (container rates up 42% in Q3 2024) and geopolitical risks raise supplier leverage.

Suppliers in specialized regions—semiconductor fabs in Taiwan, copper smelters in Chile—can dictate prices when substitution is hard; Hubbell reported 6–8 week lead-time spikes in 2024.

Hubbell must manage contracts, dual-sourcing, and inventory: in 2024 working capital tied to inventory rose 12%, so supply continuity is critical.

Supplier Concentration in High-Tech Segments

As Hubbell adds smart sensors and comms to fixtures, qualified suppliers shrink—GlobalData noted ~12 major suppliers for industrial IoT modules in 2024, concentrating pricing power.

Those suppliers can demand 8–15% higher ASPs or stricter IP/volume clauses; Hubbell counters by signing multi-year contracts to secure capacity and limit spot-price shocks.

- ~12 key IoT module suppliers (2024)

- 8–15% higher average selling price imposed

- Multi-year contracts used to hedge supply shortages

Impact of Environmental Regulations on Upstream Partners

Suppliers face tighter environmental and labor rules—EU carbon pricing and US industrial air standards raised costs; steel and aluminum input prices rose ~18% in 2024, pressuring margins and raising quoted component prices to Hubbell.

Hubbell’s sustainability vetting narrows approved vendors, increasing supplier bargaining power and procurement lead times; in 2025 certified-supplier spend rose to ~32% of purchases.

- Higher input costs: steel/aluminum +18% (2024)

- Certified-supplier share: ~32% of spend (2025)

- Smaller vendor pool → higher prices, longer lead times

Suppliers Hold Sway: Input Costs Surge (Copper $9k) & Lead Times Spike, Hubbell Mitigates

Suppliers exert moderate-to-high power: key inputs (copper/steel/aluminum/plastics) and specialized IoT/semiconductor parts are concentrated, driving input-cost swings (copper ~$9,000/ton in 2024; steel/aluminum +18% in 2024) and lead-time spikes (6–8 weeks in 2024); Hubbell uses multi-year contracts and dual-sourcing to limit 8–15% spot-price premia.

| Metric | Value |

|---|---|

| Copper price (2024) | $9,000/ton |

| Steel/Aluminum change (2024) | +18% |

| Lead-time spikes (2024) | 6–8 weeks |

| IoT suppliers (2024) | ~12 |

| Spot-price premia | 8–15% |

| Certified-supplier spend (2025) | ~32% |

What is included in the product

Tailored for Hubbell, this Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and emerging disruptors to assess pricing pressure and long-term profitability.

Hubbell Porter's Five Forces in one compact sheet—instantly visualize competitive pressure, tweak force weights with live data, and drop the clean chart into decks for faster strategic decisions.

Customers Bargaining Power

Concentration of Large Electrical Distributors

Utility Sector Procurement Processes

In Hubbell’s Utility Solutions, customers—mainly investor-owned utilities and state-linked entities—use centralized procurement to force competitive bids; the top 50 US utilities account for ~60% of sector spend, pushing prices down via long-term contracts. These buyers demand strict reliability and safety: 2024 NERC data show >90% of outages tied to equipment standards, so customers secure rigorous testing and custom specs with limited price concessions.

Low Switching Costs for Standardized Products

For basic wiring devices and standard fittings, switching costs are low: contractors can swap brands with minimal retraining or retrofit cost, so a price rise by Hubbell above peers Eaton or Legrand risks immediate churn. In 2024 U.S. trade data, commodity electrical sku margins averaged ~8–12%, constraining price hikes; a 5–10% premium versus competitors often triggers volume loss in tender-driven projects.

Price Transparency in Digital Marketplaces

Project-Based Buying Power in Construction

Project-based buying in construction gives developers and GCs strong leverage; for example, a 2024 Turner Construction survey found 62% of large projects consolidate electrical purchases worth >$5M, driving aggressive price competition.

Buyers pit manufacturers to lower total-package bids, so Hubbell often bundles lighting, wiring, and services or offers extended warranties and logistics to protect margins.

Bundling and value-added services reduced contract churn by 15% for comparable firms in 2023, so Hubbell must match those offers to win bids.

- 62% of large projects consolidate electrical buys (> $5M)

- Buyers drive price-down by competitive total-package bidding

- Hubbell uses bundling, warranties, logistics to defend margins

- Comparable firms cut churn ~15% with value-added services (2023)

Buyer Power, Marketplaces Pressuring Hubbell — Gross Margin Falls to 24.8%

| Metric | 2024 |

|---|---|

| Distributor revenue share | 20–25% |

| Top 50 utilities spend | ~60% |

| Contractors using marketplaces | 58% |

| Hubbell gross margin | 24.8% |

What You See Is What You Get

Hubbell Porter's Five Forces Analysis

This preview shows the exact Hubbell Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders; it includes supplier and buyer power, rivalry intensity, threat of entry and substitutes, and strategic implications.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy, complete with concise conclusions and actionable recommendations.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Hubbell’s Porter's Five Forces snapshot highlights its solid supplier relationships, moderate buyer power, and durable barriers to entry driven by scale and regulation, while flagging potential threats from substitutes and selective competition in niche segments. This brief overview points to where strategic advantages and vulnerabilities lie across the value chain. Ready to move beyond the basics? Get a full strategic breakdown of Hubbell’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Raw Material Price Volatility

Hubbell depends on copper, steel, aluminum and plastics; copper surged ~40% in 2021–2023 and was ~$9,000/ton in 2024, so raw-material swings materially affect COGS and margins.

Suppliers hold moderate power: Hubbell needs certified, high-quality inputs to meet NEC and UL standards, limiting supplier substitution and giving suppliers pricing leverage.

Specialized Component Dependencies

Certain Hubbell products need specialized semiconductors and proprietary sub-components from few vendors; supplier concentration gives those vendors pricing and lead-time leverage—Hubbell disclosed supply-chain pressures cut Q3 2025 sales by ~2.1% and added ~$12m in procurement premiums.

Dependency is sharpest in Utility Solutions, where precision and reliability are non-negotiable; 68% of that segment’s key parts sourced from three suppliers raises risk of single-vendor disruption and margin compression.

Global Supply Chain Logistics

Hubbell sources materials from Asia, Europe, and North America, so 2024 shipping disruptions (container rates up 42% in Q3 2024) and geopolitical risks raise supplier leverage.

Suppliers in specialized regions—semiconductor fabs in Taiwan, copper smelters in Chile—can dictate prices when substitution is hard; Hubbell reported 6–8 week lead-time spikes in 2024.

Hubbell must manage contracts, dual-sourcing, and inventory: in 2024 working capital tied to inventory rose 12%, so supply continuity is critical.

Supplier Concentration in High-Tech Segments

As Hubbell adds smart sensors and comms to fixtures, qualified suppliers shrink—GlobalData noted ~12 major suppliers for industrial IoT modules in 2024, concentrating pricing power.

Those suppliers can demand 8–15% higher ASPs or stricter IP/volume clauses; Hubbell counters by signing multi-year contracts to secure capacity and limit spot-price shocks.

- ~12 key IoT module suppliers (2024)

- 8–15% higher average selling price imposed

- Multi-year contracts used to hedge supply shortages

Impact of Environmental Regulations on Upstream Partners

Suppliers face tighter environmental and labor rules—EU carbon pricing and US industrial air standards raised costs; steel and aluminum input prices rose ~18% in 2024, pressuring margins and raising quoted component prices to Hubbell.

Hubbell’s sustainability vetting narrows approved vendors, increasing supplier bargaining power and procurement lead times; in 2025 certified-supplier spend rose to ~32% of purchases.

- Higher input costs: steel/aluminum +18% (2024)

- Certified-supplier share: ~32% of spend (2025)

- Smaller vendor pool → higher prices, longer lead times

Suppliers Hold Sway: Input Costs Surge (Copper $9k) & Lead Times Spike, Hubbell Mitigates

Suppliers exert moderate-to-high power: key inputs (copper/steel/aluminum/plastics) and specialized IoT/semiconductor parts are concentrated, driving input-cost swings (copper ~$9,000/ton in 2024; steel/aluminum +18% in 2024) and lead-time spikes (6–8 weeks in 2024); Hubbell uses multi-year contracts and dual-sourcing to limit 8–15% spot-price premia.

| Metric | Value |

|---|---|

| Copper price (2024) | $9,000/ton |

| Steel/Aluminum change (2024) | +18% |

| Lead-time spikes (2024) | 6–8 weeks |

| IoT suppliers (2024) | ~12 |

| Spot-price premia | 8–15% |

| Certified-supplier spend (2025) | ~32% |

What is included in the product

Tailored for Hubbell, this Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and emerging disruptors to assess pricing pressure and long-term profitability.

Hubbell Porter's Five Forces in one compact sheet—instantly visualize competitive pressure, tweak force weights with live data, and drop the clean chart into decks for faster strategic decisions.

Customers Bargaining Power

Concentration of Large Electrical Distributors

Utility Sector Procurement Processes

In Hubbell’s Utility Solutions, customers—mainly investor-owned utilities and state-linked entities—use centralized procurement to force competitive bids; the top 50 US utilities account for ~60% of sector spend, pushing prices down via long-term contracts. These buyers demand strict reliability and safety: 2024 NERC data show >90% of outages tied to equipment standards, so customers secure rigorous testing and custom specs with limited price concessions.

Low Switching Costs for Standardized Products

For basic wiring devices and standard fittings, switching costs are low: contractors can swap brands with minimal retraining or retrofit cost, so a price rise by Hubbell above peers Eaton or Legrand risks immediate churn. In 2024 U.S. trade data, commodity electrical sku margins averaged ~8–12%, constraining price hikes; a 5–10% premium versus competitors often triggers volume loss in tender-driven projects.

Price Transparency in Digital Marketplaces

Project-Based Buying Power in Construction

Project-based buying in construction gives developers and GCs strong leverage; for example, a 2024 Turner Construction survey found 62% of large projects consolidate electrical purchases worth >$5M, driving aggressive price competition.

Buyers pit manufacturers to lower total-package bids, so Hubbell often bundles lighting, wiring, and services or offers extended warranties and logistics to protect margins.

Bundling and value-added services reduced contract churn by 15% for comparable firms in 2023, so Hubbell must match those offers to win bids.

- 62% of large projects consolidate electrical buys (> $5M)

- Buyers drive price-down by competitive total-package bidding

- Hubbell uses bundling, warranties, logistics to defend margins

- Comparable firms cut churn ~15% with value-added services (2023)

Buyer Power, Marketplaces Pressuring Hubbell — Gross Margin Falls to 24.8%

| Metric | 2024 |

|---|---|

| Distributor revenue share | 20–25% |

| Top 50 utilities spend | ~60% |

| Contractors using marketplaces | 58% |

| Hubbell gross margin | 24.8% |

What You See Is What You Get

Hubbell Porter's Five Forces Analysis

This preview shows the exact Hubbell Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders; it includes supplier and buyer power, rivalry intensity, threat of entry and substitutes, and strategic implications.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy, complete with concise conclusions and actionable recommendations.