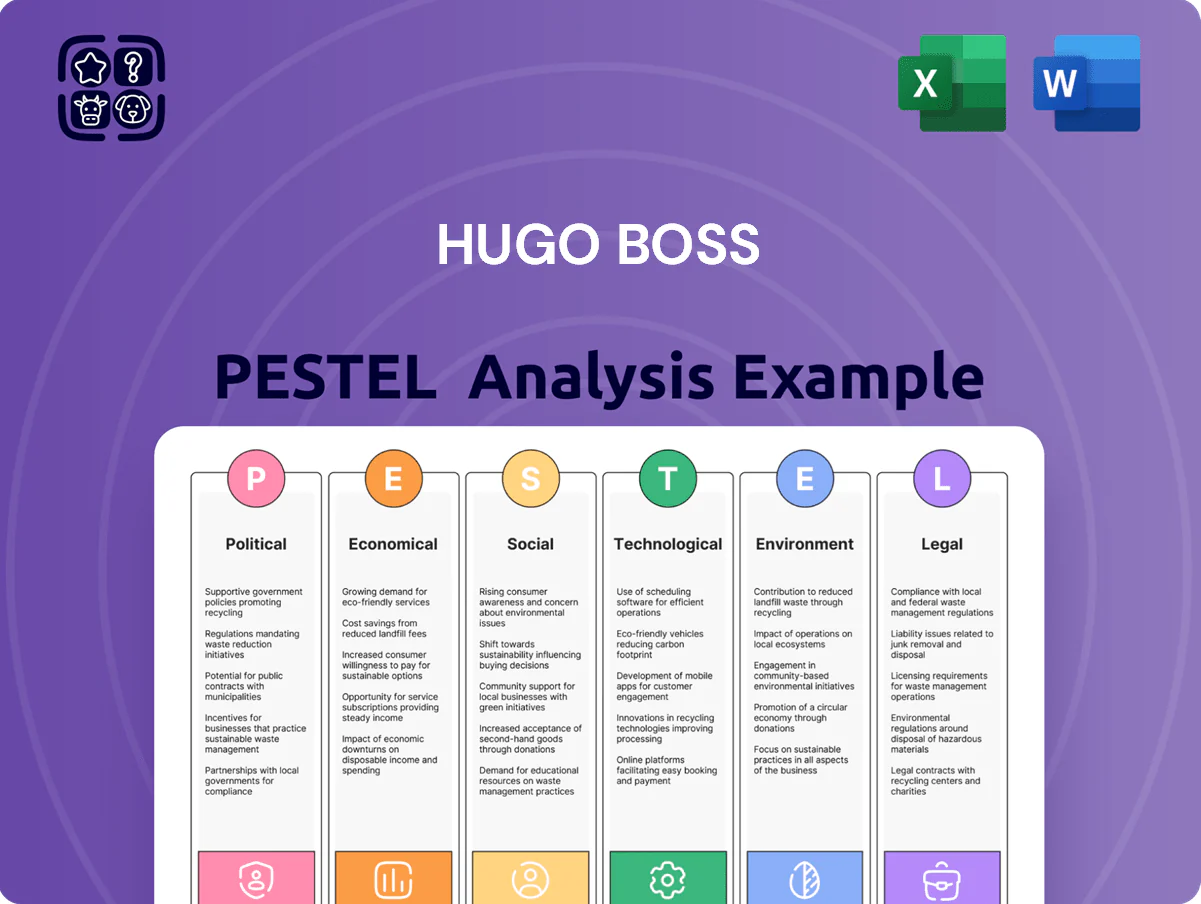

Hugo Boss PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Uncover how political shifts, economic cycles, social trends, technological advances, legal reforms, and environmental pressures are reshaping Hugo Boss’s strategy and market position—our concise PESTLE distills the implications for revenue, sourcing, and brand resilience. Purchase the full analysis to access data-driven insights, scenario implications, and ready-to-use recommendations for investors and strategists.

Political factors

Global Trade Policy and Tariffs

Changes in trade agreements and tariffs between the US, China and EU materially affect Hugo Boss’s landed costs; 2024 EU-US tariff threats and US-China frictions risk raising import duties by several percentage points, adding millions to supply-chain costs given 2023 group revenue of €2.76bn. As a global exporter, Hugo Boss must manage fluctuating duties via strategic sourcing and hedging; analysts watch tariff shifts to gauge required retail price hikes in premium markets and potential relocation of production hubs to lower-cost regions.

Geopolitical Stability in Sourcing Regions

Political instability in Asia and Eastern Europe—e.g., 2024 factory shutdowns in Bangladesh reducing apparel output by 12% and rising protest-related disruptions in Ukraine—threatens Hugo Boss’s supply-chain lead times and inventory flow.

Hugo Boss must diversify suppliers; as of FY2024 it sourced roughly 60% of production from Asia, so shifting toward multi-country sourcing can reduce single-region risk.

Ongoing regional political monitoring and scenario planning are required to protect seasonal collection deliveries to ~420 Hugo Boss retail locations worldwide and wholesale partners.

Labor Regulations and Minimum Wage Laws

Evolving labor laws in key manufacturing countries like Bangladesh and Vietnam increase apparel production costs; Bangladesh raised its minimum wage for garment workers to 8,000 BDT/month (~US$74) in 2024, and Vietnam has implemented tighter labor protections through 2023–24 reforms. Higher minimum wages and stricter safety rules force Hugo Boss to balance social responsibility with margins—labor represents ~20–30% of COGS in apparel supply chains. Adapting to mandates while preserving quality is critical for Hugo Boss’s operational resilience and brand ethics.

Export and Import Restrictions

Sanctions and trade barriers can restrict Hugo Boss’s access to high-growth markets; for example, Russia accounted for less than 1% of group sales in 2023 after sanctions-driven exits, while China represented about 15% of revenue, making tariff shifts consequential.

Political tensions often trigger sudden customs changes that delayed shipments in 2022–2024, raising logistics costs; Hugo Boss reported distribution and logistics expenses of €333m in FY2023, up year-on-year.

Navigating these risks requires a strong legal and logistics framework to ensure compliance, minimize entry barriers, and protect margins amid volatile trade policy environments.

- Sanctions can cut market access—Russia <1% of sales (2023); China ~15% of revenue (2023)

- Customs volatility increased logistics/distribution costs to €333m (FY2023)

- Requires robust legal compliance and resilient supply-chain logistics

Government Support for Sustainable Initiatives

Political agendas favoring the green transition are driving incentives and mandates; EU Green Deal measures and Fit for 55 increase support for sustainable business practices.

Hugo Boss taps EU grants and German tax incentives to fund eco-friendly tech and circular models, supporting its 2024 goal to reduce CO2 emissions by 55% (scope 1+2) versus 2019 and investing ~€150m in sustainability through 2023–2025.

Aligning strategy with these priorities secures funding, lowers capex via subsidies, and preserves competitive advantage as consumers and regulators favor low-carbon fashion.

- EU Green Deal + Fit for 55 drive incentives/mandates

- Hugo Boss: ~€150m sustainability investment (2023–2025)

- Target: −55% scope 1+2 CO2 vs 2019 by 2024

- Grants/tax breaks reduce capex and boost competitiveness

Hugo Boss: Political risks and Asia sourcing squeeze margins despite green investment

Political risks—tariffs, sanctions, labor-law hikes and regional instability—raise Hugo Boss’s supply-chain and logistics costs (distribution €333m FY2023) and threaten margins given 2023 revenue €2.76bn and ~60% Asia sourcing; EU Green Deal incentives support ~€150m sustainability spend (2023–25) and a −55% scope1+2 CO2 target vs 2019.

| Metric | Value |

|---|---|

| Group revenue (2023) | €2.76bn |

| Distribution & logistics (FY2023) | €333m |

| Asia production share (FY2024) | ~60% |

| China revenue (2023) | ~15% |

| Sustainability investment (2023–25) | ~€150m |

| CO2 target (scope1+2) | −55% vs 2019 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Hugo Boss across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, consultants, and investors.

A concise, visually segmented Hugo Boss PESTLE summary that can be dropped into presentations or shared across teams for quick alignment, while allowing users to add region- or business-specific notes to support strategic planning and risk discussions.

Economic factors

Global Inflation and Disposable Income

Rising inflation—Eurozone HICP at 3.4% in 2025 and US CPI ~3.2% YTD—erodes disposable income for middle‑class and premium shoppers, pressuring Hugo Boss sales in core markets.

Hugo Boss must balance price increases against brand aspirationality; the group reported a 4% like‑for‑like price uplift in 2024 while maintaining full‑price sell‑through to protect margins.

During downturns consumers shift to timeless investment pieces over fast trends, supporting Hugo Boss’s focus on classics where gross margins remain higher and inventory risk is lower.

Exchange Rate Volatility

Hugo Boss reports in EUR but earned about 46% of 2023 revenue outside the Eurozone, notably in USD, CNY and GBP; FX swings caused a 2023 translational headwind of roughly EUR 22m on operating profit. Management uses forward contracts and options—hedging covered approximately 60–70% of near-term FX exposure in 2024—yet persistent USD strength or RMB volatility remains a material long-term risk for cash flow and reported earnings.

Economic Growth in Emerging Markets

Hugo Boss targets growth in Southeast Asia and India where luxury market value rose about 8–10% CAGR 2020–2024, with India luxury spend hitting ~$6.4bn in 2024; the brand increased investments in 2023–2025 to expand stores and digital marketing to capture rising middle/upper-income cohorts. Success depends on macro stability: GDP growth, inflation, and currency swings directly affect retail rollouts and localized campaigns, making sustained economic stability essential for store profitability.

Interest Rate Impact on Capital Expenditure

- Higher policy rates (~3.5% ECB, 2024) increase cost of debt

- Net debt/EBITDA ~1.2x (2024) signals moderate leverage

- Interest coverage trend monitored by investors for CAPEX flexibility

Raw Material Price Fluctuations

The prices of wool, cotton and leather rose notably in 2024–25; raw cotton futures gained ~18% YoY in 2024 while leather input costs increased ~12%, exposing Hugo Boss to commodity volatility that can compress gross margin if not managed.

Hugo Boss must choose between absorbing higher input costs or raising retail prices—FY 2024 gross margin was 57.0%, so procurement strategies and long-term supplier contracts are critical to stabilize costs and protect profitability.

- 2024 cotton futures +18% YoY

- Leather input costs +12% (2024)

- Hugo Boss FY24 gross margin 57.0%

- Long-term contracts and efficient procurement mitigate margin risk

Hugo Boss weathering inflation and FX headwinds—margins firm, hedges crucial

Economic headwinds—Eurozone HICP 3.4% (2025), US CPI ~3.2% YTD—squeeze disposable income and demand; Hugo Boss reported FY24 gross margin 57.0% and net debt/EBITDA ~1.2x, with 46% revenue outside EUR causing a EUR 22m translational headwind in 2023; procurement and hedging (60–70% FX cover in 2024) are key to managing input cost inflation (cotton +18% YoY 2024, leather +12% 2024).

| Metric | Value |

|---|---|

| Eurozone HICP (2025) | 3.4% |

| US CPI (YTD) | ~3.2% |

| FY24 gross margin | 57.0% |

| Net debt/EBITDA (2024) | ~1.2x |

| Revenue outside EUR (2023) | 46% |

| Translational headwind (2023) | ≈EUR 22m |

| Cotton futures (2024 YoY) | +18% |

| Leather costs (2024) | +12% |

| FX hedge coverage (2024) | 60–70% |

Preview Before You Purchase

Hugo Boss PESTLE Analysis

The preview shown here is the exact Hugo Boss PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Uncover how political shifts, economic cycles, social trends, technological advances, legal reforms, and environmental pressures are reshaping Hugo Boss’s strategy and market position—our concise PESTLE distills the implications for revenue, sourcing, and brand resilience. Purchase the full analysis to access data-driven insights, scenario implications, and ready-to-use recommendations for investors and strategists.

Political factors

Global Trade Policy and Tariffs

Changes in trade agreements and tariffs between the US, China and EU materially affect Hugo Boss’s landed costs; 2024 EU-US tariff threats and US-China frictions risk raising import duties by several percentage points, adding millions to supply-chain costs given 2023 group revenue of €2.76bn. As a global exporter, Hugo Boss must manage fluctuating duties via strategic sourcing and hedging; analysts watch tariff shifts to gauge required retail price hikes in premium markets and potential relocation of production hubs to lower-cost regions.

Geopolitical Stability in Sourcing Regions

Political instability in Asia and Eastern Europe—e.g., 2024 factory shutdowns in Bangladesh reducing apparel output by 12% and rising protest-related disruptions in Ukraine—threatens Hugo Boss’s supply-chain lead times and inventory flow.

Hugo Boss must diversify suppliers; as of FY2024 it sourced roughly 60% of production from Asia, so shifting toward multi-country sourcing can reduce single-region risk.

Ongoing regional political monitoring and scenario planning are required to protect seasonal collection deliveries to ~420 Hugo Boss retail locations worldwide and wholesale partners.

Labor Regulations and Minimum Wage Laws

Evolving labor laws in key manufacturing countries like Bangladesh and Vietnam increase apparel production costs; Bangladesh raised its minimum wage for garment workers to 8,000 BDT/month (~US$74) in 2024, and Vietnam has implemented tighter labor protections through 2023–24 reforms. Higher minimum wages and stricter safety rules force Hugo Boss to balance social responsibility with margins—labor represents ~20–30% of COGS in apparel supply chains. Adapting to mandates while preserving quality is critical for Hugo Boss’s operational resilience and brand ethics.

Export and Import Restrictions

Sanctions and trade barriers can restrict Hugo Boss’s access to high-growth markets; for example, Russia accounted for less than 1% of group sales in 2023 after sanctions-driven exits, while China represented about 15% of revenue, making tariff shifts consequential.

Political tensions often trigger sudden customs changes that delayed shipments in 2022–2024, raising logistics costs; Hugo Boss reported distribution and logistics expenses of €333m in FY2023, up year-on-year.

Navigating these risks requires a strong legal and logistics framework to ensure compliance, minimize entry barriers, and protect margins amid volatile trade policy environments.

- Sanctions can cut market access—Russia <1% of sales (2023); China ~15% of revenue (2023)

- Customs volatility increased logistics/distribution costs to €333m (FY2023)

- Requires robust legal compliance and resilient supply-chain logistics

Government Support for Sustainable Initiatives

Political agendas favoring the green transition are driving incentives and mandates; EU Green Deal measures and Fit for 55 increase support for sustainable business practices.

Hugo Boss taps EU grants and German tax incentives to fund eco-friendly tech and circular models, supporting its 2024 goal to reduce CO2 emissions by 55% (scope 1+2) versus 2019 and investing ~€150m in sustainability through 2023–2025.

Aligning strategy with these priorities secures funding, lowers capex via subsidies, and preserves competitive advantage as consumers and regulators favor low-carbon fashion.

- EU Green Deal + Fit for 55 drive incentives/mandates

- Hugo Boss: ~€150m sustainability investment (2023–2025)

- Target: −55% scope 1+2 CO2 vs 2019 by 2024

- Grants/tax breaks reduce capex and boost competitiveness

Hugo Boss: Political risks and Asia sourcing squeeze margins despite green investment

Political risks—tariffs, sanctions, labor-law hikes and regional instability—raise Hugo Boss’s supply-chain and logistics costs (distribution €333m FY2023) and threaten margins given 2023 revenue €2.76bn and ~60% Asia sourcing; EU Green Deal incentives support ~€150m sustainability spend (2023–25) and a −55% scope1+2 CO2 target vs 2019.

| Metric | Value |

|---|---|

| Group revenue (2023) | €2.76bn |

| Distribution & logistics (FY2023) | €333m |

| Asia production share (FY2024) | ~60% |

| China revenue (2023) | ~15% |

| Sustainability investment (2023–25) | ~€150m |

| CO2 target (scope1+2) | −55% vs 2019 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Hugo Boss across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, consultants, and investors.

A concise, visually segmented Hugo Boss PESTLE summary that can be dropped into presentations or shared across teams for quick alignment, while allowing users to add region- or business-specific notes to support strategic planning and risk discussions.

Economic factors

Global Inflation and Disposable Income

Rising inflation—Eurozone HICP at 3.4% in 2025 and US CPI ~3.2% YTD—erodes disposable income for middle‑class and premium shoppers, pressuring Hugo Boss sales in core markets.

Hugo Boss must balance price increases against brand aspirationality; the group reported a 4% like‑for‑like price uplift in 2024 while maintaining full‑price sell‑through to protect margins.

During downturns consumers shift to timeless investment pieces over fast trends, supporting Hugo Boss’s focus on classics where gross margins remain higher and inventory risk is lower.

Exchange Rate Volatility

Hugo Boss reports in EUR but earned about 46% of 2023 revenue outside the Eurozone, notably in USD, CNY and GBP; FX swings caused a 2023 translational headwind of roughly EUR 22m on operating profit. Management uses forward contracts and options—hedging covered approximately 60–70% of near-term FX exposure in 2024—yet persistent USD strength or RMB volatility remains a material long-term risk for cash flow and reported earnings.

Economic Growth in Emerging Markets

Hugo Boss targets growth in Southeast Asia and India where luxury market value rose about 8–10% CAGR 2020–2024, with India luxury spend hitting ~$6.4bn in 2024; the brand increased investments in 2023–2025 to expand stores and digital marketing to capture rising middle/upper-income cohorts. Success depends on macro stability: GDP growth, inflation, and currency swings directly affect retail rollouts and localized campaigns, making sustained economic stability essential for store profitability.

Interest Rate Impact on Capital Expenditure

- Higher policy rates (~3.5% ECB, 2024) increase cost of debt

- Net debt/EBITDA ~1.2x (2024) signals moderate leverage

- Interest coverage trend monitored by investors for CAPEX flexibility

Raw Material Price Fluctuations

The prices of wool, cotton and leather rose notably in 2024–25; raw cotton futures gained ~18% YoY in 2024 while leather input costs increased ~12%, exposing Hugo Boss to commodity volatility that can compress gross margin if not managed.

Hugo Boss must choose between absorbing higher input costs or raising retail prices—FY 2024 gross margin was 57.0%, so procurement strategies and long-term supplier contracts are critical to stabilize costs and protect profitability.

- 2024 cotton futures +18% YoY

- Leather input costs +12% (2024)

- Hugo Boss FY24 gross margin 57.0%

- Long-term contracts and efficient procurement mitigate margin risk

Hugo Boss weathering inflation and FX headwinds—margins firm, hedges crucial

Economic headwinds—Eurozone HICP 3.4% (2025), US CPI ~3.2% YTD—squeeze disposable income and demand; Hugo Boss reported FY24 gross margin 57.0% and net debt/EBITDA ~1.2x, with 46% revenue outside EUR causing a EUR 22m translational headwind in 2023; procurement and hedging (60–70% FX cover in 2024) are key to managing input cost inflation (cotton +18% YoY 2024, leather +12% 2024).

| Metric | Value |

|---|---|

| Eurozone HICP (2025) | 3.4% |

| US CPI (YTD) | ~3.2% |

| FY24 gross margin | 57.0% |

| Net debt/EBITDA (2024) | ~1.2x |

| Revenue outside EUR (2023) | 46% |

| Translational headwind (2023) | ≈EUR 22m |

| Cotton futures (2024 YoY) | +18% |

| Leather costs (2024) | +12% |

| FX hedge coverage (2024) | 60–70% |

Preview Before You Purchase

Hugo Boss PESTLE Analysis

The preview shown here is the exact Hugo Boss PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis and decision-making.