Hulu LLC PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, social behaviors, technological innovation, legal changes, and environmental pressures are reshaping Hulu LLC—our concise PESTLE highlights the most consequential external forces and strategic implications. Ideal for investors, strategists, and analysts, the full PESTLE delivers a detailed, actionable roadmap to mitigate risks and seize growth—purchase now to download the complete, ready-to-use analysis.

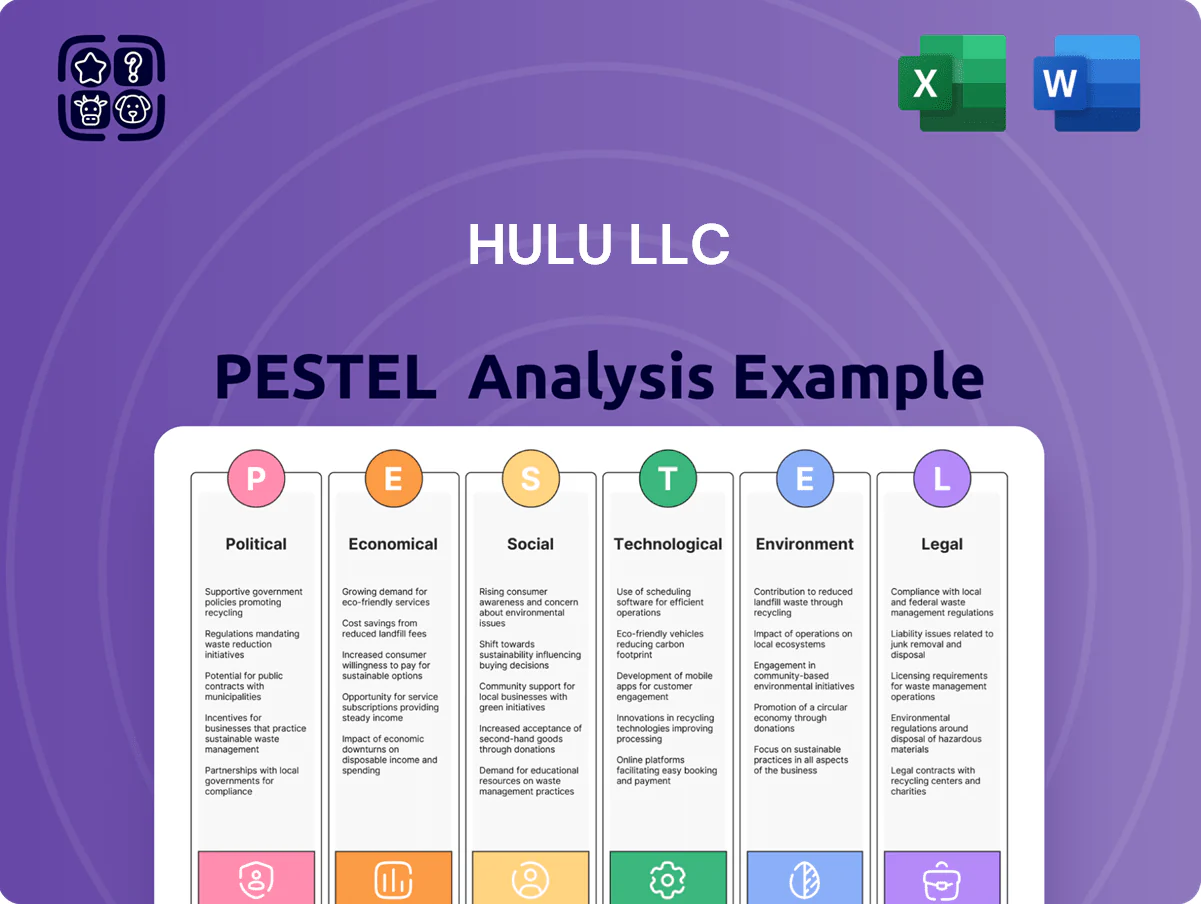

Political factors

Full Integration into Disney Corporate Strategy

The finalization of Disney’s full ownership of Hulu by end-2025 has streamlined political and strategic objectives, consolidating decision-making for a platform with roughly 54 million subscribers as of Q4 2025 and contributing to Disney Direct-to-Consumer revenue of $23.5 billion in FY2024. This consolidation allows a unified lobbying front on media regulation and digital distribution rights, leveraging Disney’s Washington presence and $8.2 million in federal lobbying spend in 2024-2025. However, Hulu now faces heightened exposure to political debates over Disney’s corporate stances and cultural influence, which could affect content approval and state-level regulatory scrutiny.

Regulatory Scrutiny of Media Consolidation

As Disney’s stake gives it control of Hulu, federal scrutiny of media consolidation has risen—DOJ and FTC reported 2024 reviews of major streaming deals as market share concentration grew, with Disney+ Bundle representing roughly 45% of U.S. streaming subscriptions by 2025; regulators may open antitrust probes to prevent bundling that harms smaller rivals, risking forced divestitures or operational restrictions that strategists must model into scenario planning.

Content Moderation and Censorship Pressures

Hulu faces sustained political pressure over content choices, with recent controversies—like 2024 calls to remove certain documentaries—prompting petitions totaling over 250,000 signatures and advertiser pauses that cost estimated ad revenue dents in the low millions. Decisions to host or remove divisive programming have triggered bipartisan backlash and boycott threats, risking churn among its ~48 million U.S. subscribers (2025 figure). Navigating these sensitivities is critical to retaining broad appeal without alienating key political demographics.

Net Neutrality and Infrastructure Policy

Changes in US net neutrality rules affect Hulu’s delivery costs and streaming quality; loss of protections could force Hulu to pay ISPs for priority delivery to sustain 4K/HD streams for 48+ million US subscribers (Q4 2025 est.).

Tiered access or fast lanes would raise operating expenses and capex for CDN and peering upgrades, pressuring EBITDA margins already sensitive after Disney’s 2024 streaming investments.

- Net neutrality rollback risk increases CDN/peering spend

- Potential higher OPEX to secure consistent QoS for 48M+ US users

- Political shifts pose material margin risk to Hulu’s long-term profitability

International Trade and Local Content Quotas

As Hulu, now integrated with Disney, pursues international growth it must comply with complex trade agreements and local content quotas; for example the EU Audiovisual Media Services Directive mandates 30% European works, and countries like Canada and Australia have similar thresholds, affecting curation and licensing costs.

Noncompliance risks include fines or revoked licenses—Brazil fined streaming services up to BRL 10m in recent cases—and revenue impact as local-content spend can raise costs by an estimated 10–15% of regional programming budgets.

- Must meet jurisdictional local-content percentages (EU 30%)

- Increased licensing spend ~10–15% regionally

- Fines/licensing risks (e.g., Brazil enforcement ~BRL 10m)

Hulu faces antitrust, lobbying scrutiny, net‑neutrality costs and advertiser backlash

Political risks for Hulu (Disney-owned): federal antitrust scrutiny of consolidation (DOJ/FTC reviews 2024), $8.2M Disney federal lobbying 2024–25, net neutrality rollback raising CDN/OPEX for ~54M subs (Q4 2025), content-related bipartisan backlash causing advertiser pauses (250k+ petition signings) and potential fines for noncompliance with local-content rules (EU 30%, regional spend +10–15%).

| Metric | Value |

|---|---|

| US subs (Q4 2025) | ~54M |

| Disney lobbying (2024–25) | $8.2M |

| Disney DTC rev FY2024 | $23.5B |

| Petition signings (2024) | 250k+ |

| EU local-content mandate | 30% |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—uniquely impact Hulu LLC, with data-driven insights, industry-specific examples, and forward-looking implications to inform strategy, risk management, and investor-facing materials.

A concise Hulu LLC PESTLE summary, segmented by category for rapid interpretation, that can be dropped into presentations or strategy packs to streamline decision-making and cross-team alignment.

Economic factors

Impact of Global Inflation on Discretionary Spending

Persistent economic volatility through 2025 has prompted US households to cut discretionary spending; 2024 Bureau of Labor Statistics data showed real disposable personal income down 1.2% YoY and CPI inflation averaging ~3.4% in 2024, pressuring subscription budgets.

Hulu’s ad-supported tier, priced as low as $7.99/month in 2025, acts as a low-cost entry point, helping retain price-sensitive customers amid downgrades from premium plans.

Analysts note the shift: Disney reported streaming advertising revenue up 18% in 2024, highlighting how macro trends are rebalancing revenue from subscriptions toward ads.

Volatility in the Digital Advertising Market

Hulu depends on advertising for lower-priced tiers and live TV, exposing it to cuts in marketing budgets; US digital ad spend fell 1.7% YoY in 2023 to about $211B and showed slower growth in 2024, pressuring fill rates and CPMs for streamers. During 2020–2023 downturns advertisers reduced spend, and Hulu must boost ad‑tech—addressable targeting and measurement—to sustain ROI and stabilize revenue.

Competitive Pricing and Market Saturation

The US streaming market shows high saturation with global subscribers hitting about 1.3 billion in 2025 and US SVOD ARPU pressures—Hulu faced estimated 2024 ARPU declines while Disney reported Disney+/Hulu bundle churn rising; intense price competition forces Hulu to weigh modest price hikes to offset rising content spend (Disney’s 2024 content cost >$8B) versus subscriber loss to cheaper rivals offering ad tiers; bundling and loyalty programs are being deployed to lift LTV and reduce churn.

Production Costs and Labor Union Negotiations

The rising cost of producing high-quality original content is a material headwind for Hulu, with average drama episode costs now ranging $3–6 million and flagship series budgets often exceeding $10 million per episode by 2024–2025.

Recent labor agreements—notably the 2023–2024 WGA and SAG-AFTRA deals—have lifted baseline compensation and residuals, increasing development budgets by an estimated 15–25% for new projects.

These higher fixed costs pressure Hulu’s margins as Disney reported increasing content spend to $11–12 billion annually across streaming in 2024, forcing tighter portfolio prioritization.

Maintaining a steady pipeline of must-watch content while managing escalations in production and talent costs is a primary executive challenge for preserving subscriber growth and profitability.

- Average drama episode cost: $3–6M; flagship series >$10M/episode

- Labor-driven budget rise: +15–25% (post‑WGA/SAG deals)

- Disney streaming content spend 2024: $11–12B

- Key challenge: balance cost control with high-impact content pipeline

Currency Exchange Fluctuations for Global Growth

As Hulu integrates into Disney’s global operations, exposure to a strong US dollar can reduce consolidated revenue when foreign earnings are converted; Disney reported ~45% of 2024 international revenue in non-USD currencies, making FX a material headwind.

Investors watch exchange-rate volatility—USD appreciation of ~6% vs major peers in 2024 trimmed international media margins, risking lower net profit contribution from Hulu’s expanding international footprint.

- USD strength reduces translated foreign revenue

- ~45% of Disney 2024 international revenue in non-USD

- ~6% USD appreciation in 2024 pressured margins

Inflation, costly content and a strong dollar squeeze Disney’s streaming margins

Economic pressures—real disposable income down 1.2% YoY (2024), CPI ~3.4%—push subscribers to ad tiers; Hulu ARPU fell in 2024 as ad revenue rose 18% for Disney. Content costs rose (avg drama $3–6M/ep; flagship >$10M; Disney streaming spend $11–12B in 2024) and labor deals increased budgets 15–25%, squeezing margins; USD up ~6% in 2024 reduced translated international revenue (~45% non‑USD).

| Metric | 2024/25 |

|---|---|

| Real DPI YoY | -1.2% |

| CPI (2024) | ~3.4% |

| Disney ad rev growth | +18% |

| Avg drama cost | $3–6M/ep |

| Disney streaming spend | $11–12B |

| USD strength | ~+6% |

Preview Before You Purchase

Hulu LLC PESTLE Analysis

The preview shown here is the exact Hulu LLC PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are exactly what you’ll download immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, social behaviors, technological innovation, legal changes, and environmental pressures are reshaping Hulu LLC—our concise PESTLE highlights the most consequential external forces and strategic implications. Ideal for investors, strategists, and analysts, the full PESTLE delivers a detailed, actionable roadmap to mitigate risks and seize growth—purchase now to download the complete, ready-to-use analysis.

Political factors

Full Integration into Disney Corporate Strategy

The finalization of Disney’s full ownership of Hulu by end-2025 has streamlined political and strategic objectives, consolidating decision-making for a platform with roughly 54 million subscribers as of Q4 2025 and contributing to Disney Direct-to-Consumer revenue of $23.5 billion in FY2024. This consolidation allows a unified lobbying front on media regulation and digital distribution rights, leveraging Disney’s Washington presence and $8.2 million in federal lobbying spend in 2024-2025. However, Hulu now faces heightened exposure to political debates over Disney’s corporate stances and cultural influence, which could affect content approval and state-level regulatory scrutiny.

Regulatory Scrutiny of Media Consolidation

As Disney’s stake gives it control of Hulu, federal scrutiny of media consolidation has risen—DOJ and FTC reported 2024 reviews of major streaming deals as market share concentration grew, with Disney+ Bundle representing roughly 45% of U.S. streaming subscriptions by 2025; regulators may open antitrust probes to prevent bundling that harms smaller rivals, risking forced divestitures or operational restrictions that strategists must model into scenario planning.

Content Moderation and Censorship Pressures

Hulu faces sustained political pressure over content choices, with recent controversies—like 2024 calls to remove certain documentaries—prompting petitions totaling over 250,000 signatures and advertiser pauses that cost estimated ad revenue dents in the low millions. Decisions to host or remove divisive programming have triggered bipartisan backlash and boycott threats, risking churn among its ~48 million U.S. subscribers (2025 figure). Navigating these sensitivities is critical to retaining broad appeal without alienating key political demographics.

Net Neutrality and Infrastructure Policy

Changes in US net neutrality rules affect Hulu’s delivery costs and streaming quality; loss of protections could force Hulu to pay ISPs for priority delivery to sustain 4K/HD streams for 48+ million US subscribers (Q4 2025 est.).

Tiered access or fast lanes would raise operating expenses and capex for CDN and peering upgrades, pressuring EBITDA margins already sensitive after Disney’s 2024 streaming investments.

- Net neutrality rollback risk increases CDN/peering spend

- Potential higher OPEX to secure consistent QoS for 48M+ US users

- Political shifts pose material margin risk to Hulu’s long-term profitability

International Trade and Local Content Quotas

As Hulu, now integrated with Disney, pursues international growth it must comply with complex trade agreements and local content quotas; for example the EU Audiovisual Media Services Directive mandates 30% European works, and countries like Canada and Australia have similar thresholds, affecting curation and licensing costs.

Noncompliance risks include fines or revoked licenses—Brazil fined streaming services up to BRL 10m in recent cases—and revenue impact as local-content spend can raise costs by an estimated 10–15% of regional programming budgets.

- Must meet jurisdictional local-content percentages (EU 30%)

- Increased licensing spend ~10–15% regionally

- Fines/licensing risks (e.g., Brazil enforcement ~BRL 10m)

Hulu faces antitrust, lobbying scrutiny, net‑neutrality costs and advertiser backlash

Political risks for Hulu (Disney-owned): federal antitrust scrutiny of consolidation (DOJ/FTC reviews 2024), $8.2M Disney federal lobbying 2024–25, net neutrality rollback raising CDN/OPEX for ~54M subs (Q4 2025), content-related bipartisan backlash causing advertiser pauses (250k+ petition signings) and potential fines for noncompliance with local-content rules (EU 30%, regional spend +10–15%).

| Metric | Value |

|---|---|

| US subs (Q4 2025) | ~54M |

| Disney lobbying (2024–25) | $8.2M |

| Disney DTC rev FY2024 | $23.5B |

| Petition signings (2024) | 250k+ |

| EU local-content mandate | 30% |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—uniquely impact Hulu LLC, with data-driven insights, industry-specific examples, and forward-looking implications to inform strategy, risk management, and investor-facing materials.

A concise Hulu LLC PESTLE summary, segmented by category for rapid interpretation, that can be dropped into presentations or strategy packs to streamline decision-making and cross-team alignment.

Economic factors

Impact of Global Inflation on Discretionary Spending

Persistent economic volatility through 2025 has prompted US households to cut discretionary spending; 2024 Bureau of Labor Statistics data showed real disposable personal income down 1.2% YoY and CPI inflation averaging ~3.4% in 2024, pressuring subscription budgets.

Hulu’s ad-supported tier, priced as low as $7.99/month in 2025, acts as a low-cost entry point, helping retain price-sensitive customers amid downgrades from premium plans.

Analysts note the shift: Disney reported streaming advertising revenue up 18% in 2024, highlighting how macro trends are rebalancing revenue from subscriptions toward ads.

Volatility in the Digital Advertising Market

Hulu depends on advertising for lower-priced tiers and live TV, exposing it to cuts in marketing budgets; US digital ad spend fell 1.7% YoY in 2023 to about $211B and showed slower growth in 2024, pressuring fill rates and CPMs for streamers. During 2020–2023 downturns advertisers reduced spend, and Hulu must boost ad‑tech—addressable targeting and measurement—to sustain ROI and stabilize revenue.

Competitive Pricing and Market Saturation

The US streaming market shows high saturation with global subscribers hitting about 1.3 billion in 2025 and US SVOD ARPU pressures—Hulu faced estimated 2024 ARPU declines while Disney reported Disney+/Hulu bundle churn rising; intense price competition forces Hulu to weigh modest price hikes to offset rising content spend (Disney’s 2024 content cost >$8B) versus subscriber loss to cheaper rivals offering ad tiers; bundling and loyalty programs are being deployed to lift LTV and reduce churn.

Production Costs and Labor Union Negotiations

The rising cost of producing high-quality original content is a material headwind for Hulu, with average drama episode costs now ranging $3–6 million and flagship series budgets often exceeding $10 million per episode by 2024–2025.

Recent labor agreements—notably the 2023–2024 WGA and SAG-AFTRA deals—have lifted baseline compensation and residuals, increasing development budgets by an estimated 15–25% for new projects.

These higher fixed costs pressure Hulu’s margins as Disney reported increasing content spend to $11–12 billion annually across streaming in 2024, forcing tighter portfolio prioritization.

Maintaining a steady pipeline of must-watch content while managing escalations in production and talent costs is a primary executive challenge for preserving subscriber growth and profitability.

- Average drama episode cost: $3–6M; flagship series >$10M/episode

- Labor-driven budget rise: +15–25% (post‑WGA/SAG deals)

- Disney streaming content spend 2024: $11–12B

- Key challenge: balance cost control with high-impact content pipeline

Currency Exchange Fluctuations for Global Growth

As Hulu integrates into Disney’s global operations, exposure to a strong US dollar can reduce consolidated revenue when foreign earnings are converted; Disney reported ~45% of 2024 international revenue in non-USD currencies, making FX a material headwind.

Investors watch exchange-rate volatility—USD appreciation of ~6% vs major peers in 2024 trimmed international media margins, risking lower net profit contribution from Hulu’s expanding international footprint.

- USD strength reduces translated foreign revenue

- ~45% of Disney 2024 international revenue in non-USD

- ~6% USD appreciation in 2024 pressured margins

Inflation, costly content and a strong dollar squeeze Disney’s streaming margins

Economic pressures—real disposable income down 1.2% YoY (2024), CPI ~3.4%—push subscribers to ad tiers; Hulu ARPU fell in 2024 as ad revenue rose 18% for Disney. Content costs rose (avg drama $3–6M/ep; flagship >$10M; Disney streaming spend $11–12B in 2024) and labor deals increased budgets 15–25%, squeezing margins; USD up ~6% in 2024 reduced translated international revenue (~45% non‑USD).

| Metric | 2024/25 |

|---|---|

| Real DPI YoY | -1.2% |

| CPI (2024) | ~3.4% |

| Disney ad rev growth | +18% |

| Avg drama cost | $3–6M/ep |

| Disney streaming spend | $11–12B |

| USD strength | ~+6% |

Preview Before You Purchase

Hulu LLC PESTLE Analysis

The preview shown here is the exact Hulu LLC PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are exactly what you’ll download immediately after checkout.