Huntsman Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

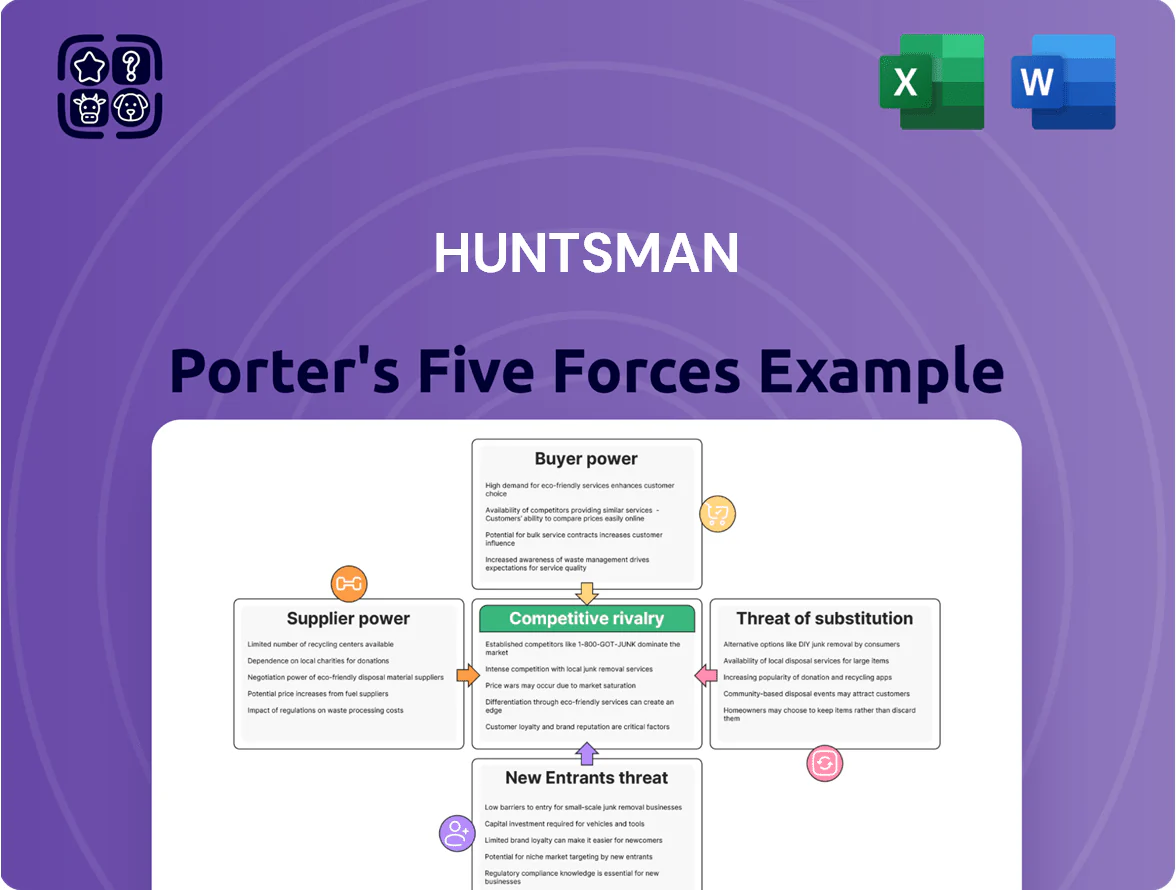

Huntsman faces moderate supplier power and intense rivalry in specialty chemicals, with manageable buyer bargaining thanks to differentiated products and a moderate threat from substitutes; regulatory and capital barriers limit new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Huntsman’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Petrochemical Feedstocks

Huntsman depends heavily on feedstocks from crude oil and natural gas—benzene, ethylene, propylene—which made up about 55–65% of variable cost per tonne for key polyurethanes in 2025.

Volatility in 2025 energy markets drove feedstock price swings: ethylene averaged $1,050/tonne in H1 then spiked to $1,420/tonne in Q3, squeezing margins.

Despite strategic sourcing and long‑term contracts, global supply shifts and OPEC+ actions meant suppliers held pricing power tied to macro moves, raising input cost risk for Huntsman.

Limited Availability of Specialty Precursors

For Huntsman’s Advanced Materials and Textile Effects, a handful of suppliers produce specialty chemical precursors, concentrating supply and raising supplier leverage over prices and contract terms.

In 2024 Huntsman reported adjusted EBIT margin of ~8.5% for Specialty Products, so supplier-driven price pressure on inputs worth >30% of COGS could cut segment profitability materially.

Huntsman must keep diversified sourcing, long-term contracts, and co‑development ties to avoid disruptions and preserve high-margin sales, as single-supplier outages historically cause 5–15% short‑term volume loss in the industry.

Energy Costs and Infrastructure

Manufacturing facilities need big energy inputs, so regional utility providers hold strong bargaining power—Huntsman faced 2023 European gas price spikes averaging 55% above 2019 levels and US industrial electricity costs ~12c/kWh in 2024, pressuring margins.

Higher electricity and natural gas costs in Europe and North America pushed Huntsman to invest in efficiency; capital spent on energy-saving projects reached low‑double‑digit millions in 2024, cutting unit energy use ~8% year-over-year.

The shift to renewables changes supplier dynamics: long-term PPAs (power purchase agreements) and onsite solar/wind require multi-year capital commitments and lock in prices, reducing short-term supplier leverage but increasing sunk costs and project risk.

Global Logistics and Transportation Constraints

Shipping and logistics firms move Huntsman’s hazardous chemicals globally, and industry consolidation plus port congestion let carriers raise rates—container freight rates spiked 175% in 2021 and remained 40% above pre‑pandemic levels through 2024.

Huntsman reduces supplier power by locating plants near customers and using regional hubs; this lowered average shipment distance by an estimated 12% from 2019–2024, cutting logistics spend per ton.

- Consolidation raises carrier bargaining power

- Port congestion drives volatile rates (peaks: +175% in 2021)

- Huntsman cut shipment distance ~12% (2019–2024)

- Regional hubs lower logistics cost per ton

Supplier Integration and Sustainability Demands

Suppliers face rising ESG (environmental, social, governance) compliance costs—certified green feedstocks can cost 10–30% more per tonne; this raises input prices for Huntsman as it pursues 2025 sustainability targets.

Huntsman must partner tightly with certified suppliers; reliance on a smaller sustainable supplier base increases those suppliers’ bargaining power and can compress Huntsman’s margin until supply scales.

- Certified feedstock premium: 10–30%/tonne

- Smaller supplier pool: higher price leverage

- 2025 targets raise short-term input cost risk

- Collaboration needed to secure supply, manage margins

High supplier power: volatile ethylene & premium feedstocks threaten Huntsman’s 8.5% EBIT

Suppliers hold high power: feedstocks (~55–65% of variable cost) and concentrated specialty precursor supply push input risk; ethylene jumped from $1,050/t (H1 2025) to $1,420/t (Q3 2025), and certified feedstocks cost 10–30% premium, so Huntsman must use long‑term contracts, regional hubs, and co‑development to protect ~8.5% Specialty EBIT margins.

| Metric | Value |

|---|---|

| Feedstock % of variable cost | 55–65% |

| Ethylene 2025 range | $1,050–$1,420/t |

| Certified feedstock premium | 10–30% |

| Specialty EBIT margin (2024) | ~8.5% |

What is included in the product

Tailored Porter’s Five Forces analysis of Huntsman that uncovers key competitive drivers, supplier and buyer power, substitute threats, entry barriers, and emerging disruptors to assess pricing influence and strategic vulnerability.

A concise Porter's Five Forces snapshot for Huntsman—instantly shows supplier, buyer, rivalry, entrant, and substitute pressures to speed strategic choices.

Customers Bargaining Power

Concentration in the Automotive and Aerospace Sectors

A large share of Huntsman’s 2024 revenue—about $2.8bn of its $9.1bn total—comes from automotive and aerospace OEMs and tier suppliers, who buy in high volumes and secure steep discounts and multi-year contracts. These buyers can force margin pressure via consolidated procurement: the top 20 customers account for roughly 35% of sales. They also can vertically integrate or shift to rivals if prices rise, raising supplier risk.

Product Differentiation and Switching Costs

Huntsman reduces customer bargaining power by selling differentiated specialty chemistries—54% of 2024 sales came from specialty segments—tailored to precise technical specs, making substitutions hard. When a formulation is embedded in a customer’s product, switching costs—requalification, testing, and downtime—can exceed months of margin, creating technical lock-in. That lock-in supported Huntsman’s adjusted EBITDA margin of ~10.5% in FY2024, higher than commodity peers.

Price Sensitivity in Construction and Housing

The construction sector buys most polyurethane insulation and coatings but is highly rate- and cycle-sensitive; as of Q4 2025, new housing starts in the US fell 9% year-over-year, pushing buyers to chase lower bids and compress margins. Customers now negotiate hard—Procurement often benchmarks 3–5 suppliers per project—so Huntsman stresses lifecycle value: independent studies show 20–30% energy savings over 10 years and 15% lower maintenance costs, justifying premium pricing.

Transparency and Digital Procurement

Demand for Sustainable and Low-Carbon Solutions

Modern corporate buyers demand lower-carbon chemicals to meet 2030 ESG targets; 72% of procurement teams prefer suppliers with verified Scope 1–3 reductions, shifting leverage toward customers.

This empowers buyers to set environmental specs; Huntsman reported 2024 sales of $6.6bn and must innovate green chemistries or lose share to agile rivals like Solvay and Covestro expanding low‑carbon lines.

- 72% procurement preference for low‑carbon suppliers

- Huntsman 2024 revenue $6.6bn

- Rivals scaling green portfolios

Buyers Tighten Grip: Top Customers & Digital Sourcing Shift Pricing Power

Buyers hold strong leverage: top 20 customers ≈35% sales, automotive/aerospace ~$2.8bn of $9.1bn (2024), consolidate procurement and benchmark 3–5 suppliers. Huntsman defends pricing via specialty chemistries (54% sales, 2024), technical lock‑in and services (service revenue +6% est. 2024), but digital sourcing (price discovery +30%) and 72% procurement ESG preference shift power to buyers.

| Metric | 2024 |

|---|---|

| Revenue | $9.1bn |

| Auto/aero sales | $2.8bn |

| Specialty % | 54% |

| Top20 customer % | 35% |

| Service rev growth | +6% est. |

Preview the Actual Deliverable

Huntsman Porter's Five Forces Analysis

This preview shows the exact Huntsman Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups—fully formatted and ready for download and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Huntsman faces moderate supplier power and intense rivalry in specialty chemicals, with manageable buyer bargaining thanks to differentiated products and a moderate threat from substitutes; regulatory and capital barriers limit new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Huntsman’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Petrochemical Feedstocks

Huntsman depends heavily on feedstocks from crude oil and natural gas—benzene, ethylene, propylene—which made up about 55–65% of variable cost per tonne for key polyurethanes in 2025.

Volatility in 2025 energy markets drove feedstock price swings: ethylene averaged $1,050/tonne in H1 then spiked to $1,420/tonne in Q3, squeezing margins.

Despite strategic sourcing and long‑term contracts, global supply shifts and OPEC+ actions meant suppliers held pricing power tied to macro moves, raising input cost risk for Huntsman.

Limited Availability of Specialty Precursors

For Huntsman’s Advanced Materials and Textile Effects, a handful of suppliers produce specialty chemical precursors, concentrating supply and raising supplier leverage over prices and contract terms.

In 2024 Huntsman reported adjusted EBIT margin of ~8.5% for Specialty Products, so supplier-driven price pressure on inputs worth >30% of COGS could cut segment profitability materially.

Huntsman must keep diversified sourcing, long-term contracts, and co‑development ties to avoid disruptions and preserve high-margin sales, as single-supplier outages historically cause 5–15% short‑term volume loss in the industry.

Energy Costs and Infrastructure

Manufacturing facilities need big energy inputs, so regional utility providers hold strong bargaining power—Huntsman faced 2023 European gas price spikes averaging 55% above 2019 levels and US industrial electricity costs ~12c/kWh in 2024, pressuring margins.

Higher electricity and natural gas costs in Europe and North America pushed Huntsman to invest in efficiency; capital spent on energy-saving projects reached low‑double‑digit millions in 2024, cutting unit energy use ~8% year-over-year.

The shift to renewables changes supplier dynamics: long-term PPAs (power purchase agreements) and onsite solar/wind require multi-year capital commitments and lock in prices, reducing short-term supplier leverage but increasing sunk costs and project risk.

Global Logistics and Transportation Constraints

Shipping and logistics firms move Huntsman’s hazardous chemicals globally, and industry consolidation plus port congestion let carriers raise rates—container freight rates spiked 175% in 2021 and remained 40% above pre‑pandemic levels through 2024.

Huntsman reduces supplier power by locating plants near customers and using regional hubs; this lowered average shipment distance by an estimated 12% from 2019–2024, cutting logistics spend per ton.

- Consolidation raises carrier bargaining power

- Port congestion drives volatile rates (peaks: +175% in 2021)

- Huntsman cut shipment distance ~12% (2019–2024)

- Regional hubs lower logistics cost per ton

Supplier Integration and Sustainability Demands

Suppliers face rising ESG (environmental, social, governance) compliance costs—certified green feedstocks can cost 10–30% more per tonne; this raises input prices for Huntsman as it pursues 2025 sustainability targets.

Huntsman must partner tightly with certified suppliers; reliance on a smaller sustainable supplier base increases those suppliers’ bargaining power and can compress Huntsman’s margin until supply scales.

- Certified feedstock premium: 10–30%/tonne

- Smaller supplier pool: higher price leverage

- 2025 targets raise short-term input cost risk

- Collaboration needed to secure supply, manage margins

High supplier power: volatile ethylene & premium feedstocks threaten Huntsman’s 8.5% EBIT

Suppliers hold high power: feedstocks (~55–65% of variable cost) and concentrated specialty precursor supply push input risk; ethylene jumped from $1,050/t (H1 2025) to $1,420/t (Q3 2025), and certified feedstocks cost 10–30% premium, so Huntsman must use long‑term contracts, regional hubs, and co‑development to protect ~8.5% Specialty EBIT margins.

| Metric | Value |

|---|---|

| Feedstock % of variable cost | 55–65% |

| Ethylene 2025 range | $1,050–$1,420/t |

| Certified feedstock premium | 10–30% |

| Specialty EBIT margin (2024) | ~8.5% |

What is included in the product

Tailored Porter’s Five Forces analysis of Huntsman that uncovers key competitive drivers, supplier and buyer power, substitute threats, entry barriers, and emerging disruptors to assess pricing influence and strategic vulnerability.

A concise Porter's Five Forces snapshot for Huntsman—instantly shows supplier, buyer, rivalry, entrant, and substitute pressures to speed strategic choices.

Customers Bargaining Power

Concentration in the Automotive and Aerospace Sectors

A large share of Huntsman’s 2024 revenue—about $2.8bn of its $9.1bn total—comes from automotive and aerospace OEMs and tier suppliers, who buy in high volumes and secure steep discounts and multi-year contracts. These buyers can force margin pressure via consolidated procurement: the top 20 customers account for roughly 35% of sales. They also can vertically integrate or shift to rivals if prices rise, raising supplier risk.

Product Differentiation and Switching Costs

Huntsman reduces customer bargaining power by selling differentiated specialty chemistries—54% of 2024 sales came from specialty segments—tailored to precise technical specs, making substitutions hard. When a formulation is embedded in a customer’s product, switching costs—requalification, testing, and downtime—can exceed months of margin, creating technical lock-in. That lock-in supported Huntsman’s adjusted EBITDA margin of ~10.5% in FY2024, higher than commodity peers.

Price Sensitivity in Construction and Housing

The construction sector buys most polyurethane insulation and coatings but is highly rate- and cycle-sensitive; as of Q4 2025, new housing starts in the US fell 9% year-over-year, pushing buyers to chase lower bids and compress margins. Customers now negotiate hard—Procurement often benchmarks 3–5 suppliers per project—so Huntsman stresses lifecycle value: independent studies show 20–30% energy savings over 10 years and 15% lower maintenance costs, justifying premium pricing.

Transparency and Digital Procurement

Demand for Sustainable and Low-Carbon Solutions

Modern corporate buyers demand lower-carbon chemicals to meet 2030 ESG targets; 72% of procurement teams prefer suppliers with verified Scope 1–3 reductions, shifting leverage toward customers.

This empowers buyers to set environmental specs; Huntsman reported 2024 sales of $6.6bn and must innovate green chemistries or lose share to agile rivals like Solvay and Covestro expanding low‑carbon lines.

- 72% procurement preference for low‑carbon suppliers

- Huntsman 2024 revenue $6.6bn

- Rivals scaling green portfolios

Buyers Tighten Grip: Top Customers & Digital Sourcing Shift Pricing Power

Buyers hold strong leverage: top 20 customers ≈35% sales, automotive/aerospace ~$2.8bn of $9.1bn (2024), consolidate procurement and benchmark 3–5 suppliers. Huntsman defends pricing via specialty chemistries (54% sales, 2024), technical lock‑in and services (service revenue +6% est. 2024), but digital sourcing (price discovery +30%) and 72% procurement ESG preference shift power to buyers.

| Metric | 2024 |

|---|---|

| Revenue | $9.1bn |

| Auto/aero sales | $2.8bn |

| Specialty % | 54% |

| Top20 customer % | 35% |

| Service rev growth | +6% est. |

Preview the Actual Deliverable

Huntsman Porter's Five Forces Analysis

This preview shows the exact Huntsman Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups—fully formatted and ready for download and use.