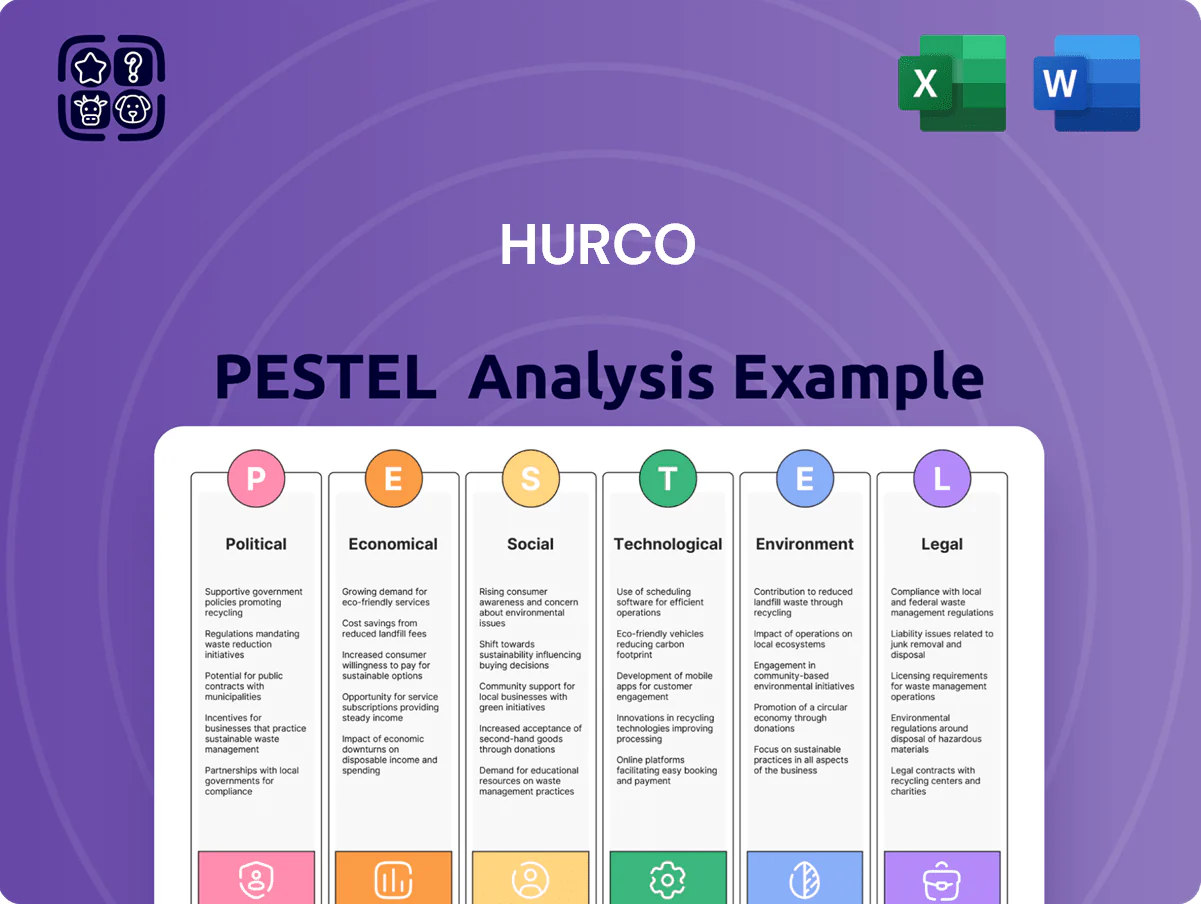

Hurco PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our PESTLE Analysis of Hurco—concise, research-backed insights into political, economic, social, technological, legal and environmental forces shaping the company’s future; ideal for investors and strategists. Purchase the full report to unlock actionable intelligence, editable templates, and risk/opportunity scenarios you can deploy immediately.

Political factors

Geopolitical Trade Tensions

Ongoing US-China trade disputes and tariffs continue to strain the global machine tool market; Hurco, with manufacturing in Taiwan and China, saw China-related supply costs rise ~4–6% during 2023–2024 tariff adjustments, reducing gross margins modestly in FY2024.

Shifts in US trade policy and Section 301 tariff risks directly affect Hurco’s production costs and market access; in 2024 exports to the US from China/Taiwan faced average tariff differentials of 2–5 percentage points.

Fluctuating international relations force agile supply chain management—Hurco increased dual-sourcing and inventory buffers in 2024, raising working capital by roughly 3% to mitigate protectionist disruptions.

Government Infrastructure Spending

Rising US and EU government infrastructure and re-shoring programs—US Inflation Reduction Act and CHIPS Act plus EU IPCEI funding—are driving demand for precision machining; US manufacturing investment rose 6.3% in 2024 and EU industrial investment grew 4.1%, supporting CNC demand. Subsidies and tax incentives (e.g., US bonus depreciation, EU state aid) lower capex costs, improving adoption prospects for Hurco’s CNC solutions and aftermarket services.

Export Control Regulations

Strict export controls on high-end and dual-use machinery limit Hurco’s ability to sell advanced 5-axis machines to regions like China and Russia; US BIS actions since 2023 expanded controls affecting ~$150m of US CNC exports in 2024.

Stability in European Markets

Taxation Policies and Incentives

Changes in US corporate tax rates and R&D tax credits affect Hurco’s net margins; US federal rate reductions from 21% to potential proposals could shift after-tax ROI, while Taiwan’s headline corporate tax of 20% and enhanced R&D credits (up to 15% locally) support margins.

Accelerated depreciation and Section 179 expensing in the US and Taiwan’s fixed-asset incentives boost CNC purchases, increasing equipment demand and revenue recognition.

Global minimum tax rules (OECD Pillar Two, 15% effective rate) could require Hurco to revise cross-border tax planning, impacting long-term investment returns and repatriation strategies.

- US corporate tax baseline 21% (current), Section 179 enables immediate expensing

- Taiwan corporate tax ~20%, R&D credits up to ~15%

- OECD Pillar Two 15% global minimum tax may reduce tax arbitrage

Geo-policy shocks lift costs 4–6% and $150M export risk as US capex +6.3%

Political risks: US-China tariffs raised Hurco China/Taiwan production costs ~4–6% in 2023–24; US export controls affected ~$150m of CNC trade in 2024; Germany = ~28% of EU sales (2024) amid EU industrial output -1.2% YoY; US infrastructure and tax incentives (Section 179) boosted US capex +6.3% (2024).

| Metric | 2024 |

|---|---|

| Tariff impact | +4–6% |

| Export controls exposure | $150m |

| Germany share | 28% |

| EU output YoY | -1.2% |

| US manufacturing investment | +6.3% |

What is included in the product

Explores how macro-environmental factors uniquely affect Hurco across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region/industry relevance to reveal risks and opportunities for executives and investors.

Provides a concise, visually segmented PESTLE summary of Hurco’s external environment, ideal for quick reference in meetings or slide decks to align teams on regulatory, economic, and technological risks.

Economic factors

Global Manufacturing Output

The demand for Hurco’s CNC machines is highly cyclical and tracks global manufacturing output; global industrial production fell 0.8% y/y in 2024, pressuring capital expenditures by job shops and OEMs and contributing to Hurco’s 2024 revenue decline of 12% year-over-year. Economic expansions historically boost CAPEX—global manufacturing PMI averaged 51.2 in 2021–23—driving machine sales, while slowdowns typically lead to deferred purchases and weaker order intake for Hurco.

Currency Exchange Rate Volatility

As a global firm, Hurco faces USD volatility versus the EUR, TWD and CNY; EUR/USD moved ~3.8% in 2024 and USD/CNY shifted ~2.5% YTD (2025), affecting product pricing competitiveness in Europe, Taiwan and China.

Exchange swings can materially alter reported international earnings—Hurco’s 2024 foreign revenue share (~38%) means a 5% USD appreciation could cut consolidated revenue by ~1.9% in USD terms.

Hedging—forward contracts and currency options—remains essential; industry practice shows top manufacturers hedge 50–80% of forecasted exposures to stabilize margins.

Interest Rates and Financing Costs

High US interest rates—Federal Funds at 5.25–5.50% in 2024—raise borrowing costs for Hurco’s customers, increasing average equipment financing rates to 7–10%, which can depress orders from SMEs that finance capital purchases; Bank lending standards tightened since 2023, with small business loan approval rates near 20% below pre‑pandemic levels. Conversely, if rates fall toward 3%–4%, industry capex and automation investment historically rise 15%–25% year‑over‑year.

Inflation and Input Costs

Rising input costs—cast iron and steel up ~18% and electronic components up ~22% in 2024 vs 2023—threaten Hurco’s margins if price increases cannot be passed to customers; Hurco reported gross margin of 23.5% in FY2024, down from 25.1% in FY2023.

Inflation-driven wage pressure (average manufacturing labor cost growth ~6% globally in 2024) raises operating expenses across Hurco’s plants, tightening operating margin and cash flow flexibility.

Balancing competitive pricing with rising production costs remains a persistent economic challenge requiring supply-chain sourcing, automation, and selective price adjustments.

- Raw material price rises: steel +18%, electronics +22% (2024 v 2023)

- Hurco gross margin: 23.5% FY2024 (down from 25.1% FY2023)

- Manufacturing labor cost growth ~6% globally in 2024

- Mitigation: sourcing, automation, selective price increases

Supply Chain Resilience

Global logistics volatility and semiconductor shortages affected Hurco’s production timelines in 2024, with global container rates peaking 120% above pre-pandemic levels in 2021–22 and semiconductor lead times averaging 18–22 weeks in 2024, causing periodic machine delivery delays.

Logistics disruptions pushed freight and input costs higher, squeezing margins; diversified suppliers and dual-sourcing reduced revenue volatility—companies with resilient chains reported 15–25% lower delivery delays in 2024.

- Semiconductor lead times ~18–22 weeks (2024)

- Container rates peaked +120% vs 2019

- Diversified suppliers cut delays 15–25%

Hurco hit by slumping global demand, soaring input costs and FX risk—revenues down 12%

Hurco’s sales track global manufacturing cycles—global industrial production fell 0.8% y/y in 2024, contributing to Hurco’s 12% revenue decline in 2024; high US rates (5.25–5.50% in 2024) pushed equipment financing to 7–10%, weakening SME orders.

Input inflation (steel +18%, electronics +22% in 2024) and wage growth (~6%) cut gross margin to 23.5% in FY2024; USD moves (EUR/USD ±3.8% in 2024) and 38% foreign revenue amplify FX risk, typically hedged 50–80%.

| Metric | Value (2024) |

|---|---|

| Revenue change | -12% |

| Gross margin | 23.5% |

| Steel price change | +18% |

| Electronics price change | +22% |

| Labor cost growth | ~6% |

| USD sensitivity | 38% foreign rev |

What You See Is What You Get

Hurco PESTLE Analysis

The preview shown here is the exact Hurco PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our PESTLE Analysis of Hurco—concise, research-backed insights into political, economic, social, technological, legal and environmental forces shaping the company’s future; ideal for investors and strategists. Purchase the full report to unlock actionable intelligence, editable templates, and risk/opportunity scenarios you can deploy immediately.

Political factors

Geopolitical Trade Tensions

Ongoing US-China trade disputes and tariffs continue to strain the global machine tool market; Hurco, with manufacturing in Taiwan and China, saw China-related supply costs rise ~4–6% during 2023–2024 tariff adjustments, reducing gross margins modestly in FY2024.

Shifts in US trade policy and Section 301 tariff risks directly affect Hurco’s production costs and market access; in 2024 exports to the US from China/Taiwan faced average tariff differentials of 2–5 percentage points.

Fluctuating international relations force agile supply chain management—Hurco increased dual-sourcing and inventory buffers in 2024, raising working capital by roughly 3% to mitigate protectionist disruptions.

Government Infrastructure Spending

Rising US and EU government infrastructure and re-shoring programs—US Inflation Reduction Act and CHIPS Act plus EU IPCEI funding—are driving demand for precision machining; US manufacturing investment rose 6.3% in 2024 and EU industrial investment grew 4.1%, supporting CNC demand. Subsidies and tax incentives (e.g., US bonus depreciation, EU state aid) lower capex costs, improving adoption prospects for Hurco’s CNC solutions and aftermarket services.

Export Control Regulations

Strict export controls on high-end and dual-use machinery limit Hurco’s ability to sell advanced 5-axis machines to regions like China and Russia; US BIS actions since 2023 expanded controls affecting ~$150m of US CNC exports in 2024.

Stability in European Markets

Taxation Policies and Incentives

Changes in US corporate tax rates and R&D tax credits affect Hurco’s net margins; US federal rate reductions from 21% to potential proposals could shift after-tax ROI, while Taiwan’s headline corporate tax of 20% and enhanced R&D credits (up to 15% locally) support margins.

Accelerated depreciation and Section 179 expensing in the US and Taiwan’s fixed-asset incentives boost CNC purchases, increasing equipment demand and revenue recognition.

Global minimum tax rules (OECD Pillar Two, 15% effective rate) could require Hurco to revise cross-border tax planning, impacting long-term investment returns and repatriation strategies.

- US corporate tax baseline 21% (current), Section 179 enables immediate expensing

- Taiwan corporate tax ~20%, R&D credits up to ~15%

- OECD Pillar Two 15% global minimum tax may reduce tax arbitrage

Geo-policy shocks lift costs 4–6% and $150M export risk as US capex +6.3%

Political risks: US-China tariffs raised Hurco China/Taiwan production costs ~4–6% in 2023–24; US export controls affected ~$150m of CNC trade in 2024; Germany = ~28% of EU sales (2024) amid EU industrial output -1.2% YoY; US infrastructure and tax incentives (Section 179) boosted US capex +6.3% (2024).

| Metric | 2024 |

|---|---|

| Tariff impact | +4–6% |

| Export controls exposure | $150m |

| Germany share | 28% |

| EU output YoY | -1.2% |

| US manufacturing investment | +6.3% |

What is included in the product

Explores how macro-environmental factors uniquely affect Hurco across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region/industry relevance to reveal risks and opportunities for executives and investors.

Provides a concise, visually segmented PESTLE summary of Hurco’s external environment, ideal for quick reference in meetings or slide decks to align teams on regulatory, economic, and technological risks.

Economic factors

Global Manufacturing Output

The demand for Hurco’s CNC machines is highly cyclical and tracks global manufacturing output; global industrial production fell 0.8% y/y in 2024, pressuring capital expenditures by job shops and OEMs and contributing to Hurco’s 2024 revenue decline of 12% year-over-year. Economic expansions historically boost CAPEX—global manufacturing PMI averaged 51.2 in 2021–23—driving machine sales, while slowdowns typically lead to deferred purchases and weaker order intake for Hurco.

Currency Exchange Rate Volatility

As a global firm, Hurco faces USD volatility versus the EUR, TWD and CNY; EUR/USD moved ~3.8% in 2024 and USD/CNY shifted ~2.5% YTD (2025), affecting product pricing competitiveness in Europe, Taiwan and China.

Exchange swings can materially alter reported international earnings—Hurco’s 2024 foreign revenue share (~38%) means a 5% USD appreciation could cut consolidated revenue by ~1.9% in USD terms.

Hedging—forward contracts and currency options—remains essential; industry practice shows top manufacturers hedge 50–80% of forecasted exposures to stabilize margins.

Interest Rates and Financing Costs

High US interest rates—Federal Funds at 5.25–5.50% in 2024—raise borrowing costs for Hurco’s customers, increasing average equipment financing rates to 7–10%, which can depress orders from SMEs that finance capital purchases; Bank lending standards tightened since 2023, with small business loan approval rates near 20% below pre‑pandemic levels. Conversely, if rates fall toward 3%–4%, industry capex and automation investment historically rise 15%–25% year‑over‑year.

Inflation and Input Costs

Rising input costs—cast iron and steel up ~18% and electronic components up ~22% in 2024 vs 2023—threaten Hurco’s margins if price increases cannot be passed to customers; Hurco reported gross margin of 23.5% in FY2024, down from 25.1% in FY2023.

Inflation-driven wage pressure (average manufacturing labor cost growth ~6% globally in 2024) raises operating expenses across Hurco’s plants, tightening operating margin and cash flow flexibility.

Balancing competitive pricing with rising production costs remains a persistent economic challenge requiring supply-chain sourcing, automation, and selective price adjustments.

- Raw material price rises: steel +18%, electronics +22% (2024 v 2023)

- Hurco gross margin: 23.5% FY2024 (down from 25.1% FY2023)

- Manufacturing labor cost growth ~6% globally in 2024

- Mitigation: sourcing, automation, selective price increases

Supply Chain Resilience

Global logistics volatility and semiconductor shortages affected Hurco’s production timelines in 2024, with global container rates peaking 120% above pre-pandemic levels in 2021–22 and semiconductor lead times averaging 18–22 weeks in 2024, causing periodic machine delivery delays.

Logistics disruptions pushed freight and input costs higher, squeezing margins; diversified suppliers and dual-sourcing reduced revenue volatility—companies with resilient chains reported 15–25% lower delivery delays in 2024.

- Semiconductor lead times ~18–22 weeks (2024)

- Container rates peaked +120% vs 2019

- Diversified suppliers cut delays 15–25%

Hurco hit by slumping global demand, soaring input costs and FX risk—revenues down 12%

Hurco’s sales track global manufacturing cycles—global industrial production fell 0.8% y/y in 2024, contributing to Hurco’s 12% revenue decline in 2024; high US rates (5.25–5.50% in 2024) pushed equipment financing to 7–10%, weakening SME orders.

Input inflation (steel +18%, electronics +22% in 2024) and wage growth (~6%) cut gross margin to 23.5% in FY2024; USD moves (EUR/USD ±3.8% in 2024) and 38% foreign revenue amplify FX risk, typically hedged 50–80%.

| Metric | Value (2024) |

|---|---|

| Revenue change | -12% |

| Gross margin | 23.5% |

| Steel price change | +18% |

| Electronics price change | +22% |

| Labor cost growth | ~6% |

| USD sensitivity | 38% foreign rev |

What You See Is What You Get

Hurco PESTLE Analysis

The preview shown here is the exact Hurco PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.