Harvest Oil & Gas Boston Consulting Group Matrix

See the Bigger Picture

Harvest Oil & Gas sits at a pivotal crossroads—some assets behave like cash cows delivering steady cash flow, while newer plays show question-mark potential amid shifting energy markets and capital constraints. This concise preview highlights strategic implications for portfolio allocation, capital expenditure, and divestment choices. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and downloadable Word + Excel files so you can act fast with confidence.

Stars

Permian Basin Core Assets

The Permian Basin remains Harvest Oil & Gas’s primary growth engine, with ~350,000 net acres and 2025 projected production of 120 mboe/d (60% oil), driven by Wolfcamp and Bone Spring high-quality reservoirs.

These core assets need ~$650–750 million annual CAPEX for drilling/completion but deliver the portfolio’s highest production growth—forecast +18% CAGR 2025–2028.

Maintaining ~8% regional market share and low $14–18/boe cash costs positions these wells to become stable cash generators as the basin matures by the early 2030s.

Advanced Enhanced Oil Recovery Projects

Harvest Oil & Gas uses tertiary recovery (CO2 flooding and polymer EOR) across 12 primary liquid-rich fields, boosting recovery by ~18%-25% and adding ~45 MMbbl estimated reserves as of Dec 31, 2025.

These Advanced EOR projects grew segment production 22% YoY in 2025, classifying them as Stars in the BCG matrix due to high market share and high market growth driven by tech gains.

They consumed ~42% of Harvest’s 2025 capital budget (~$340 million), a heavy spend but vital to keep Harvest the largest domestic producer in its peer set.

Digital Oilfield Integration

The deployment of real-time monitoring and automated drilling systems is a high-growth frontier for Harvest Oil & Gas, aligning with industry digital investments that grew 18% YoY in 2024 and where capex for automation reached $9.2B globally in 2024.

These initiatives sit in the high-growth BCG Stars quadrant, needing continuous software updates and 24/7 technical support—estimated at 6–8% of project capex annually—to keep pace with API and ISO standards.

Successful integration delivers 10–25% uptime gains and up to 12% lower operating costs per well, reinforcing Harvest’s operational efficiency and positioning it as a modern energy market leader.

Methane Mitigation Technologies

Harvest Oil & Gas positions Methane Mitigation Technologies as a Stars quadrant asset, with 2025 revenue growth projected at 22% year-over-year after a $45m capex injection in 2024 for advanced leak detection and repair systems.

Stronger regulation (US EPA finalized rules in 2024 cutting oil-gas methane emissions 60% by 2030) makes these systems critical to retain operating permits and access to $1.2bn of ESG-linked financing Harvest targets.

Market leadership drives partner wins: Harvest claims ~12% market share of North American methane monitoring contracts in 2025, attracting green investors and lifting EV/EBITDA multiple by ~0.8x versus peers.

- 2024 capex $45m; 2025 revenue growth +22%

- EPA rules: 60% methane cut by 2030

- 2025 market share ~12% North America

- ESG financing target $1.2bn; EV/EBITDA premium +0.8x

Strategic Midstream Partnerships

Harvest Oil & Gas has pursued joint ventures in pipeline and storage, securing takeaway capacity for 2025 growth; partners include two regional MLPs funding $420m of midstream buildouts to serve +120 mboe/d of new production.

These assets are in high-growth mode as three new fields ramp this year, preventing bottlenecks and increasing realized prices by ~4–6 USD/boe versus spot due to reduced basis risk.

- Secured $420m capex with partners

- Supports +120 mboe/d new supply

- Estimated +4–6 USD/boe realized uplift

Harvest Permian: 120 mboe/d (60% oil), +18% CAGR, $650–750M CAPEX, +45MMbbl EOR

Harvest’s Permian Stars—350k net acres, 2025 prod ~120 mboe/d (60% oil), +18% CAGR 2025–28—consume $650–750M/yr CAPEX; Advanced EOR added ~45 MMbbl reserves (Dec 31, 2025) and grew segment prod 22% in 2025; methane tech rev +22% in 2025, 12% NA market share; midstream JV funded $420M supporting +120 mboe/d and +$4–6/boe realized uplift.

| Metric | 2025 |

|---|---|

| Prod | 120 mboe/d |

| Oil% | 60% |

| CAPEX | $650–750M/yr |

| EOR reserves | +45 MMbbl |

| Methane rev growth | +22% |

| Midstream JV | $420M |

What is included in the product

Comprehensive BCG Matrix review of Harvest Oil & Gas with quadrant strategies, investment recommendations, and trend-based risks/opportunities.

One-page BCG matrix placing Harvest Oil & Gas units in quadrants for quick portfolio clarity and strategic action.

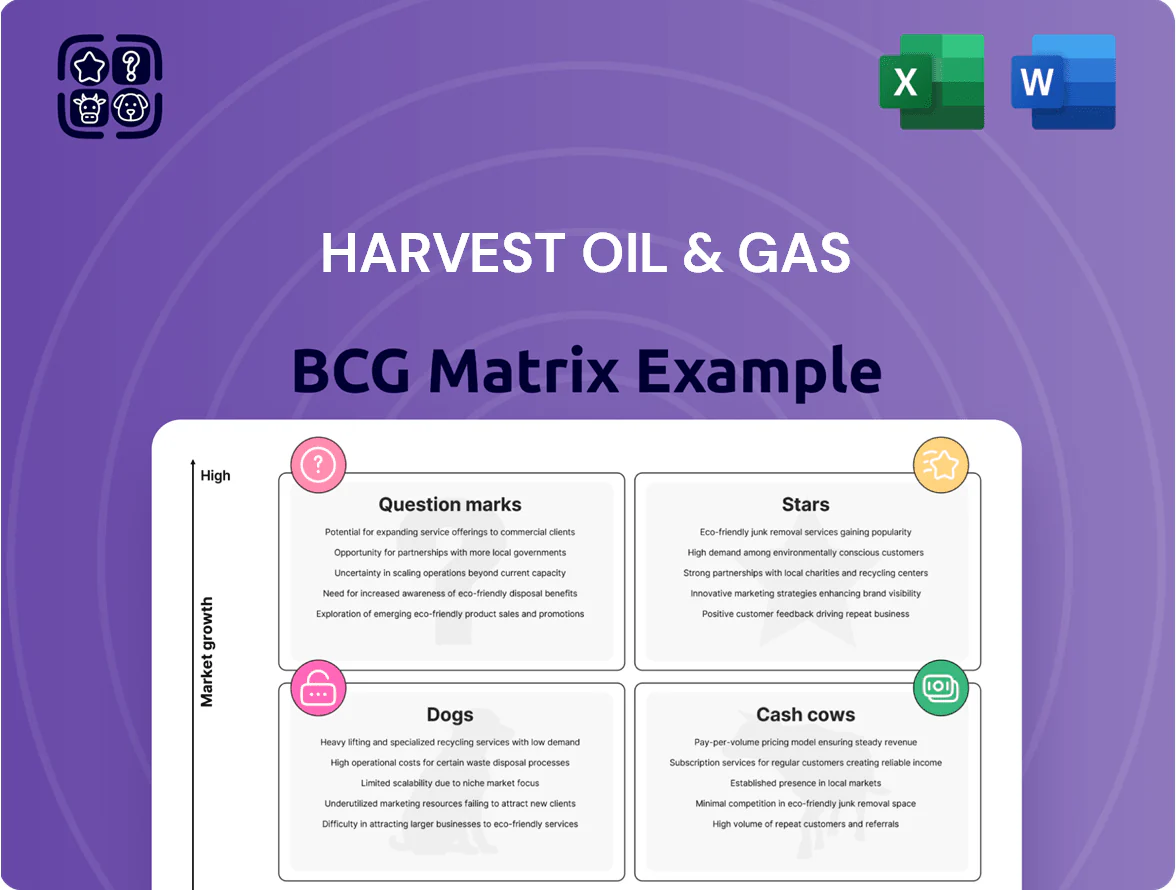

Cash Cows

Appalachian Natural Gas Production

Harvest’s Appalachian natural gas assets sit in a mature Marcellus/Utica market where the company holds roughly 12% regional market share and produces about 220 MMcf/d (2025 avg), delivering stable volumes with decline rates under 18%/yr. These wells generate roughly $110–130 million annual free cash flow after LOE and transport (2025 est), with minimal capex for development drilling. That liquidity funds growth in Stars and Question Marks, covering ~45% of discretionary R&D and drilling budgets.

Mid-Continent Conventional Reservoirs

Mid-Continent conventional reservoirs, with average decline rates under 10%/yr and 2025 realized oil margins near $48/bbl on $68/bbl WTI, supply steady cash flow that anchors Harvest Oil & Gas’s balance sheet.

Nearly fully depreciated infrastructure cuts operating overhead to about $6–8/boe, producing EBITDA margins >55% that management uses to service $420M net debt and fund $0.12/SH dividends.

San Juan Basin Gas Assets

Harvest Oil & Gas holds ~35% operated working interest across San Juan Basin assets, a mature low-growth region where 2024 production averaged ~42,000 boe/d (70% gas); focus is on uptime, well interventions, and 10–15% LOE (lease operating expense) cuts to boost free cash flow.

Michigan Basin Operations

The Michigan Basin operations are a cash cow: Harvest Oil & Gas holds an estimated 65% regional market share in 2025 production, yielding ~12,000 boe/d and generating roughly $58M annual EBITDA, while regional decline and permitting limits keep new competition and growth low.

Maintenance capital runs near $8–10M/year (2025 guidance), minimizing reinvestment so free cash funds corporate G&A and debt service, and smoothing volatility compared with shale wells.

- 65% regional share, ~12,000 boe/d (2025)

- ~$58M annual EBITDA (2025)

- $8–10M maintenance capex (2025)

- Stable cash flow vs shale volatility

Legacy Hedging Portfolios

Harvest Oil & Gas’s Legacy Hedging Portfolios lock in average realized prices 18% above spot in 2025, creating predictable cash flows that act as a financial cash cow.

This hedging cuts revenue volatility—standard deviation of monthly cash receipts fell from 12% (2019–21) to 4% in 2024–25—so short-term oil and gas swings have limited cash impact.

The steady inflow funds capex and debt service: hedged cash covered 72% of 2025 interest and maintenance capex, keeping the corporate structure solvent during market stress.

- Average realized hedge premium: +18% in 2025

- Cash volatility reduced: 12% → 4%

- Hedged cash covered 72% of 2025 interest+maintenance capex

Harvest’s cash cows: ~54k boe/d, $168–188M FCF (2025) — hedges +18%, low volatility

Harvest’s cash cows (Appalachian gas, Mid-Continent oil, Michigan Basin, legacy hedges) deliver ~244 MMcf/d equiv / ~54,000 boe/d (2025), ~$168–188M free cash flow, ~$58M Michigan EBITDA, maintenance capex $8–10M, hedges +18% realized, cash-volatility down to 4%, funding 45% discretionary capex and covering 72% interest+maintenance.

| Asset | 2025 Prod | FCF/EBITDA | Maint Capex | Hedge |

|---|---|---|---|---|

| Appalachian | 220 MMcf/d | $110–130M FCF | minimal | — |

| Mid‑Continent | ~42,000 boe/d | anchors cash | — | — |

| Michigan | 12,000 boe/d | $58M EBITDA | $8–10M | — |

| Hedging | — | stabilizes cash | — | +18% realized |

What You See Is What You Get

Harvest Oil & Gas BCG Matrix

The file you're previewing is the exact Harvest Oil & Gas BCG Matrix report you'll receive after purchase—no watermarks, no draft notes—just a fully formatted, analysis-ready document designed for strategic decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Harvest Oil & Gas sits at a pivotal crossroads—some assets behave like cash cows delivering steady cash flow, while newer plays show question-mark potential amid shifting energy markets and capital constraints. This concise preview highlights strategic implications for portfolio allocation, capital expenditure, and divestment choices. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and downloadable Word + Excel files so you can act fast with confidence.

Stars

Permian Basin Core Assets

The Permian Basin remains Harvest Oil & Gas’s primary growth engine, with ~350,000 net acres and 2025 projected production of 120 mboe/d (60% oil), driven by Wolfcamp and Bone Spring high-quality reservoirs.

These core assets need ~$650–750 million annual CAPEX for drilling/completion but deliver the portfolio’s highest production growth—forecast +18% CAGR 2025–2028.

Maintaining ~8% regional market share and low $14–18/boe cash costs positions these wells to become stable cash generators as the basin matures by the early 2030s.

Advanced Enhanced Oil Recovery Projects

Harvest Oil & Gas uses tertiary recovery (CO2 flooding and polymer EOR) across 12 primary liquid-rich fields, boosting recovery by ~18%-25% and adding ~45 MMbbl estimated reserves as of Dec 31, 2025.

These Advanced EOR projects grew segment production 22% YoY in 2025, classifying them as Stars in the BCG matrix due to high market share and high market growth driven by tech gains.

They consumed ~42% of Harvest’s 2025 capital budget (~$340 million), a heavy spend but vital to keep Harvest the largest domestic producer in its peer set.

Digital Oilfield Integration

The deployment of real-time monitoring and automated drilling systems is a high-growth frontier for Harvest Oil & Gas, aligning with industry digital investments that grew 18% YoY in 2024 and where capex for automation reached $9.2B globally in 2024.

These initiatives sit in the high-growth BCG Stars quadrant, needing continuous software updates and 24/7 technical support—estimated at 6–8% of project capex annually—to keep pace with API and ISO standards.

Successful integration delivers 10–25% uptime gains and up to 12% lower operating costs per well, reinforcing Harvest’s operational efficiency and positioning it as a modern energy market leader.

Methane Mitigation Technologies

Harvest Oil & Gas positions Methane Mitigation Technologies as a Stars quadrant asset, with 2025 revenue growth projected at 22% year-over-year after a $45m capex injection in 2024 for advanced leak detection and repair systems.

Stronger regulation (US EPA finalized rules in 2024 cutting oil-gas methane emissions 60% by 2030) makes these systems critical to retain operating permits and access to $1.2bn of ESG-linked financing Harvest targets.

Market leadership drives partner wins: Harvest claims ~12% market share of North American methane monitoring contracts in 2025, attracting green investors and lifting EV/EBITDA multiple by ~0.8x versus peers.

- 2024 capex $45m; 2025 revenue growth +22%

- EPA rules: 60% methane cut by 2030

- 2025 market share ~12% North America

- ESG financing target $1.2bn; EV/EBITDA premium +0.8x

Strategic Midstream Partnerships

Harvest Oil & Gas has pursued joint ventures in pipeline and storage, securing takeaway capacity for 2025 growth; partners include two regional MLPs funding $420m of midstream buildouts to serve +120 mboe/d of new production.

These assets are in high-growth mode as three new fields ramp this year, preventing bottlenecks and increasing realized prices by ~4–6 USD/boe versus spot due to reduced basis risk.

- Secured $420m capex with partners

- Supports +120 mboe/d new supply

- Estimated +4–6 USD/boe realized uplift

Harvest Permian: 120 mboe/d (60% oil), +18% CAGR, $650–750M CAPEX, +45MMbbl EOR

Harvest’s Permian Stars—350k net acres, 2025 prod ~120 mboe/d (60% oil), +18% CAGR 2025–28—consume $650–750M/yr CAPEX; Advanced EOR added ~45 MMbbl reserves (Dec 31, 2025) and grew segment prod 22% in 2025; methane tech rev +22% in 2025, 12% NA market share; midstream JV funded $420M supporting +120 mboe/d and +$4–6/boe realized uplift.

| Metric | 2025 |

|---|---|

| Prod | 120 mboe/d |

| Oil% | 60% |

| CAPEX | $650–750M/yr |

| EOR reserves | +45 MMbbl |

| Methane rev growth | +22% |

| Midstream JV | $420M |

What is included in the product

Comprehensive BCG Matrix review of Harvest Oil & Gas with quadrant strategies, investment recommendations, and trend-based risks/opportunities.

One-page BCG matrix placing Harvest Oil & Gas units in quadrants for quick portfolio clarity and strategic action.

Cash Cows

Appalachian Natural Gas Production

Harvest’s Appalachian natural gas assets sit in a mature Marcellus/Utica market where the company holds roughly 12% regional market share and produces about 220 MMcf/d (2025 avg), delivering stable volumes with decline rates under 18%/yr. These wells generate roughly $110–130 million annual free cash flow after LOE and transport (2025 est), with minimal capex for development drilling. That liquidity funds growth in Stars and Question Marks, covering ~45% of discretionary R&D and drilling budgets.

Mid-Continent Conventional Reservoirs

Mid-Continent conventional reservoirs, with average decline rates under 10%/yr and 2025 realized oil margins near $48/bbl on $68/bbl WTI, supply steady cash flow that anchors Harvest Oil & Gas’s balance sheet.

Nearly fully depreciated infrastructure cuts operating overhead to about $6–8/boe, producing EBITDA margins >55% that management uses to service $420M net debt and fund $0.12/SH dividends.

San Juan Basin Gas Assets

Harvest Oil & Gas holds ~35% operated working interest across San Juan Basin assets, a mature low-growth region where 2024 production averaged ~42,000 boe/d (70% gas); focus is on uptime, well interventions, and 10–15% LOE (lease operating expense) cuts to boost free cash flow.

Michigan Basin Operations

The Michigan Basin operations are a cash cow: Harvest Oil & Gas holds an estimated 65% regional market share in 2025 production, yielding ~12,000 boe/d and generating roughly $58M annual EBITDA, while regional decline and permitting limits keep new competition and growth low.

Maintenance capital runs near $8–10M/year (2025 guidance), minimizing reinvestment so free cash funds corporate G&A and debt service, and smoothing volatility compared with shale wells.

- 65% regional share, ~12,000 boe/d (2025)

- ~$58M annual EBITDA (2025)

- $8–10M maintenance capex (2025)

- Stable cash flow vs shale volatility

Legacy Hedging Portfolios

Harvest Oil & Gas’s Legacy Hedging Portfolios lock in average realized prices 18% above spot in 2025, creating predictable cash flows that act as a financial cash cow.

This hedging cuts revenue volatility—standard deviation of monthly cash receipts fell from 12% (2019–21) to 4% in 2024–25—so short-term oil and gas swings have limited cash impact.

The steady inflow funds capex and debt service: hedged cash covered 72% of 2025 interest and maintenance capex, keeping the corporate structure solvent during market stress.

- Average realized hedge premium: +18% in 2025

- Cash volatility reduced: 12% → 4%

- Hedged cash covered 72% of 2025 interest+maintenance capex

Harvest’s cash cows: ~54k boe/d, $168–188M FCF (2025) — hedges +18%, low volatility

Harvest’s cash cows (Appalachian gas, Mid-Continent oil, Michigan Basin, legacy hedges) deliver ~244 MMcf/d equiv / ~54,000 boe/d (2025), ~$168–188M free cash flow, ~$58M Michigan EBITDA, maintenance capex $8–10M, hedges +18% realized, cash-volatility down to 4%, funding 45% discretionary capex and covering 72% interest+maintenance.

| Asset | 2025 Prod | FCF/EBITDA | Maint Capex | Hedge |

|---|---|---|---|---|

| Appalachian | 220 MMcf/d | $110–130M FCF | minimal | — |

| Mid‑Continent | ~42,000 boe/d | anchors cash | — | — |

| Michigan | 12,000 boe/d | $58M EBITDA | $8–10M | — |

| Hedging | — | stabilizes cash | — | +18% realized |

What You See Is What You Get

Harvest Oil & Gas BCG Matrix

The file you're previewing is the exact Harvest Oil & Gas BCG Matrix report you'll receive after purchase—no watermarks, no draft notes—just a fully formatted, analysis-ready document designed for strategic decision-making.