Harvest Oil & Gas Business Model Canvas

Harvest Oil & Gas: Ready-to-Use Business Model Canvas for Investors & Strategists

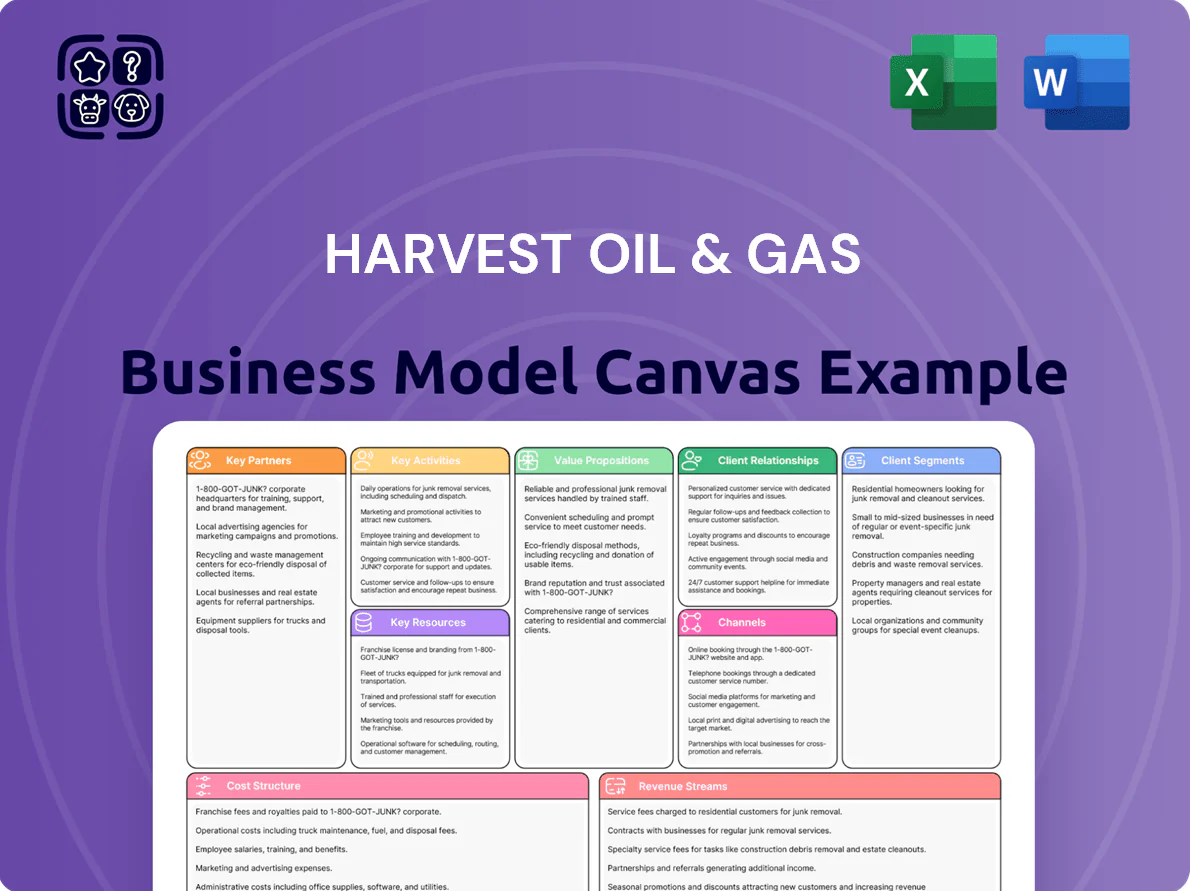

Unlock the full strategic blueprint behind Harvest Oil & Gas’s business model—this concise Business Model Canvas maps value propositions, customer segments, key partnerships, and revenue drivers to reveal how the company scales and mitigates industry risks; ideal for investors, consultants, and entrepreneurs seeking actionable, ready-to-use insights—download the full Word/Excel canvas to benchmark, adapt, and execute with confidence.

Partnerships

Midstream Infrastructure Operators

Harvest partners with midstream operators who run pipelines and processing plants, securing takeaway capacity that cut realized differentials by up to 18% in 2024 and reduced downtime <5% annually; long-term contracts and volume commitments helped lock 85% of expected 2025 throughput. Collaborative planning aligns Harvest’s production forecasts with pipeline maintenance windows, trimming flaring and storage costs by an estimated $3.6M in 2024.

Oilfield Service Providers

Specialized oilfield service firms supply technical crews and heavy rigs for maintenance and development drilling, letting Harvest avoid $12–18m capex per new pad by outsourcing; top-tier partners bring drill-rate gains of 10–20% and latest techniques like automated drill controls (2024 industry average rig productivity up 14%). Outsourcing creates a flexible cost base—converting fixed asset expense into variable service fees tied to well count and uptime.

Financial Institutions and Lenders

Access to capital is critical for an acquisition-heavy strategy, so banks and private equity firms provide credit facilities and debt financing—U.S. oil & gas M&A saw $56.2 billion in deals in 2024, underscoring funding needs for buying producing properties in proven basins.

Joint Venture Partners

Collaborating with independent energy firms shares capital and geological risk—Harvest reduced per-well capex by ~30% in its 2024 JV in the Permian, while accessing partners’ drilling rigs and seismic teams to cut cycle time 18%.

These JVs target complex basins where pooled acreage and tech raise recovery rates; Harvest used JV slots to join three 2025 Gulf of Mexico developments, keeping portfolio diversified and growing production 12% without sole funding burden.

- Reduced per-well capex ~30% (2024 Permian JV)

- CYCLE TIME cut ~18% via shared tech

- Production +12% (2025 via Gulf JV participation)

- Enables larger developments with lower balance-sheet exposure

Regulatory and Environmental Agencies

Proactive engagement with state and federal agencies (EPA, BLM, state oil commissions) reduces permitting time—avg. 25% faster in 2023 EPA statistics—and lowers legal risk through routine compliance audits and transparent emissions reporting (Scope 1/2 reporting, methane intensity targets under 2024 EPA rules).

- 25% faster permitting (EPA 2023)

- Routine compliance audits—maintain operating licenses

- Scope 1/2 and methane reporting per 2024 rules

Harvest partnerships cut costs, boost production & speed—85% throughput, $3.6M saved

Harvest’s partners (midstream, service firms, banks, JVs, regulators) cut costs and risk: 85% 2025 throughput secured, ~$3.6M saved in 2024 on flaring/storage, per-well capex down ~30% (2024 Permian JV), cycle time −18%, production +12% via 2025 Gulf JVs, and 25% faster permitting (EPA 2023).

| Partnership | Key metric | 2024/2025 |

|---|---|---|

| Midstream | Throughput locked | 85% (2025) |

| Ops savings | Flaring/storage | $3.6M (2024) |

| JV (Permian) | Per-well capex | −30% (2024) |

| JV tech | Cycle time | −18% |

| Gulf JVs | Production | +12% (2025) |

| Regulatory | Permitting speed | +25% (EPA 2023) |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Harvest Oil & Gas covering customer segments, channels, value propositions, key activities, resources, partnerships, cost structure, and revenue streams with strategic insights and competitive analysis for investor presentations and internal planning.

High-level view of Harvest Oil & Gas’s business model with editable cells, saving hours of formatting while condensing strategy into a clean, shareable one-page snapshot ideal for boardrooms, teams, or quick competitive comparisons.

Activities

Strategic Asset Acquisition

The team targets undervalued or mature producing properties across the continental United States, using financial models and geological due diligence; in 2025 the U.S. independent E&P buyout market saw ~$18.5 billion in transactions through Q3, underscoring deal flow and pricing benchmarks.

Production Optimization

Harvest boosts asset output by upgrading wellheads, retrofitting artificial-lift systems, and streamlining logistics, yielding a typical 15–30% uplift in production within 12 months; recent projects cut operating costs by 10% and raised EUR (estimated ultimate recovery) by 8% per well. Continuous SCADA and downhole sensor monitoring enables real-time tweaks that increase uptime to 96% and add ~$2.5M annual net revenue per 1,000 boe/d asset.

Targeted Development Drilling

Executing targeted development drilling in proven basins drives organic growth by adding 8–12% annual reserve replacement through infill wells and step-out pads; Harvest Oil & Gas plans 45 net wells in 2025 at an average all-in cost of $4.2m/well, boosting 2P reserves and lowering unit lifting costs. This approach cuts technical risk versus wildcatting and aims to lift 2025 EBITDA by an estimated $38–50m.

Commodity Risk Management

Harvest Oil & Gas uses active hedging, locking prices on ~40% of 2026 projected production via swaps and collars to stabilize revenue against the 2025–26 Brent range of $60–90/bbl.

This keeps cash flow steady for servicing $420m term debt (as of Dec 31, 2025) and funding 2026 capex of $120m.

- Hedges cover ~40% 2026 output

- Instruments: swaps, collars, options

- Targets: secure debt service, fund $120m capex

- Debt level: $420m (Dec 31, 2025)

Regulatory Compliance and Safety

Managing daily operations demands strict adherence to health, safety, and environmental protocols, including daily site inspections, quarterly HSE (health, safety, environment) training for 100% of field staff, and spill-prevention systems that cut incident rates—lost-time injury frequency rate (LTIFR) target ≤0.5 per million hours. These measures protect reputation and avoid disruptions that can cost $2–5 million per major spill.

- Daily site inspections

- Quarterly HSE training for all field staff

- Spill prevention systems and containment

- LTIFR target ≤0.5 per million hours

- Major-spill avoidance saves $2–5M each incident

Harvest boosts US output—45 wells, $420M debt, $120M capex; 15–30% uplift, 96% uptime

Harvest acquires underpriced US producing assets, upgrades wells and controls, drills 45 net wells in 2025 (avg $4.2M/well), and hedges ~40% 2026 output to protect cash flow for $420M debt and $120M capex, targeting 15–30% production uplift and 96% uptime.

| Metric | Value |

|---|---|

| 2025 M&A market | $18.5B (Q1–Q3) |

| Wells 2025 | 45 net |

| All‑in cost/well | $4.2M |

| Debt (Dec 31, 2025) | $420M |

| 2026 capex | $120M |

Delivered as Displayed

Business Model Canvas

The preview you see is the authentic Harvest Oil & Gas Business Model Canvas — not a mockup or sample — and it matches the exact document delivered after purchase; upon ordering you’ll receive this same professionally formatted file ready for editing and presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Harvest Oil & Gas: Ready-to-Use Business Model Canvas for Investors & Strategists

Unlock the full strategic blueprint behind Harvest Oil & Gas’s business model—this concise Business Model Canvas maps value propositions, customer segments, key partnerships, and revenue drivers to reveal how the company scales and mitigates industry risks; ideal for investors, consultants, and entrepreneurs seeking actionable, ready-to-use insights—download the full Word/Excel canvas to benchmark, adapt, and execute with confidence.

Partnerships

Midstream Infrastructure Operators

Harvest partners with midstream operators who run pipelines and processing plants, securing takeaway capacity that cut realized differentials by up to 18% in 2024 and reduced downtime <5% annually; long-term contracts and volume commitments helped lock 85% of expected 2025 throughput. Collaborative planning aligns Harvest’s production forecasts with pipeline maintenance windows, trimming flaring and storage costs by an estimated $3.6M in 2024.

Oilfield Service Providers

Specialized oilfield service firms supply technical crews and heavy rigs for maintenance and development drilling, letting Harvest avoid $12–18m capex per new pad by outsourcing; top-tier partners bring drill-rate gains of 10–20% and latest techniques like automated drill controls (2024 industry average rig productivity up 14%). Outsourcing creates a flexible cost base—converting fixed asset expense into variable service fees tied to well count and uptime.

Financial Institutions and Lenders

Access to capital is critical for an acquisition-heavy strategy, so banks and private equity firms provide credit facilities and debt financing—U.S. oil & gas M&A saw $56.2 billion in deals in 2024, underscoring funding needs for buying producing properties in proven basins.

Joint Venture Partners

Collaborating with independent energy firms shares capital and geological risk—Harvest reduced per-well capex by ~30% in its 2024 JV in the Permian, while accessing partners’ drilling rigs and seismic teams to cut cycle time 18%.

These JVs target complex basins where pooled acreage and tech raise recovery rates; Harvest used JV slots to join three 2025 Gulf of Mexico developments, keeping portfolio diversified and growing production 12% without sole funding burden.

- Reduced per-well capex ~30% (2024 Permian JV)

- CYCLE TIME cut ~18% via shared tech

- Production +12% (2025 via Gulf JV participation)

- Enables larger developments with lower balance-sheet exposure

Regulatory and Environmental Agencies

Proactive engagement with state and federal agencies (EPA, BLM, state oil commissions) reduces permitting time—avg. 25% faster in 2023 EPA statistics—and lowers legal risk through routine compliance audits and transparent emissions reporting (Scope 1/2 reporting, methane intensity targets under 2024 EPA rules).

- 25% faster permitting (EPA 2023)

- Routine compliance audits—maintain operating licenses

- Scope 1/2 and methane reporting per 2024 rules

Harvest partnerships cut costs, boost production & speed—85% throughput, $3.6M saved

Harvest’s partners (midstream, service firms, banks, JVs, regulators) cut costs and risk: 85% 2025 throughput secured, ~$3.6M saved in 2024 on flaring/storage, per-well capex down ~30% (2024 Permian JV), cycle time −18%, production +12% via 2025 Gulf JVs, and 25% faster permitting (EPA 2023).

| Partnership | Key metric | 2024/2025 |

|---|---|---|

| Midstream | Throughput locked | 85% (2025) |

| Ops savings | Flaring/storage | $3.6M (2024) |

| JV (Permian) | Per-well capex | −30% (2024) |

| JV tech | Cycle time | −18% |

| Gulf JVs | Production | +12% (2025) |

| Regulatory | Permitting speed | +25% (EPA 2023) |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Harvest Oil & Gas covering customer segments, channels, value propositions, key activities, resources, partnerships, cost structure, and revenue streams with strategic insights and competitive analysis for investor presentations and internal planning.

High-level view of Harvest Oil & Gas’s business model with editable cells, saving hours of formatting while condensing strategy into a clean, shareable one-page snapshot ideal for boardrooms, teams, or quick competitive comparisons.

Activities

Strategic Asset Acquisition

The team targets undervalued or mature producing properties across the continental United States, using financial models and geological due diligence; in 2025 the U.S. independent E&P buyout market saw ~$18.5 billion in transactions through Q3, underscoring deal flow and pricing benchmarks.

Production Optimization

Harvest boosts asset output by upgrading wellheads, retrofitting artificial-lift systems, and streamlining logistics, yielding a typical 15–30% uplift in production within 12 months; recent projects cut operating costs by 10% and raised EUR (estimated ultimate recovery) by 8% per well. Continuous SCADA and downhole sensor monitoring enables real-time tweaks that increase uptime to 96% and add ~$2.5M annual net revenue per 1,000 boe/d asset.

Targeted Development Drilling

Executing targeted development drilling in proven basins drives organic growth by adding 8–12% annual reserve replacement through infill wells and step-out pads; Harvest Oil & Gas plans 45 net wells in 2025 at an average all-in cost of $4.2m/well, boosting 2P reserves and lowering unit lifting costs. This approach cuts technical risk versus wildcatting and aims to lift 2025 EBITDA by an estimated $38–50m.

Commodity Risk Management

Harvest Oil & Gas uses active hedging, locking prices on ~40% of 2026 projected production via swaps and collars to stabilize revenue against the 2025–26 Brent range of $60–90/bbl.

This keeps cash flow steady for servicing $420m term debt (as of Dec 31, 2025) and funding 2026 capex of $120m.

- Hedges cover ~40% 2026 output

- Instruments: swaps, collars, options

- Targets: secure debt service, fund $120m capex

- Debt level: $420m (Dec 31, 2025)

Regulatory Compliance and Safety

Managing daily operations demands strict adherence to health, safety, and environmental protocols, including daily site inspections, quarterly HSE (health, safety, environment) training for 100% of field staff, and spill-prevention systems that cut incident rates—lost-time injury frequency rate (LTIFR) target ≤0.5 per million hours. These measures protect reputation and avoid disruptions that can cost $2–5 million per major spill.

- Daily site inspections

- Quarterly HSE training for all field staff

- Spill prevention systems and containment

- LTIFR target ≤0.5 per million hours

- Major-spill avoidance saves $2–5M each incident

Harvest boosts US output—45 wells, $420M debt, $120M capex; 15–30% uplift, 96% uptime

Harvest acquires underpriced US producing assets, upgrades wells and controls, drills 45 net wells in 2025 (avg $4.2M/well), and hedges ~40% 2026 output to protect cash flow for $420M debt and $120M capex, targeting 15–30% production uplift and 96% uptime.

| Metric | Value |

|---|---|

| 2025 M&A market | $18.5B (Q1–Q3) |

| Wells 2025 | 45 net |

| All‑in cost/well | $4.2M |

| Debt (Dec 31, 2025) | $420M |

| 2026 capex | $120M |

Delivered as Displayed

Business Model Canvas

The preview you see is the authentic Harvest Oil & Gas Business Model Canvas — not a mockup or sample — and it matches the exact document delivered after purchase; upon ordering you’ll receive this same professionally formatted file ready for editing and presentation.