Harvest Oil & Gas PESTLE Analysis

Your Competitive Advantage Starts with This Report

Understand how political shifts, market cycles, and environmental rules are shaping Harvest Oil & Gas’s strategic outlook—our concise PESTLE snapshot highlights the most critical external forces affecting operations and value. Ready-made for investors and strategists, the full report delivers deeper legal, technological, and social analysis with actionable recommendations. Purchase the complete PESTLE to access editable insights you can apply immediately.

Political factors

Federal Leasing and Permitting Policies

The regulatory environment for Harvest Oil & Gas is shaped by federal land-use and drilling-permit policy; as of 2024 federal onshore lease sales dropped 34% year-over-year and BLM permitting slowed 22% through Q3 2024.

By end-2025 projected administrative shifts could impose stricter oversight or further slow new federal-lease approvals, potentially reducing federal acreage additions by an estimated 25–40% versus 2023 levels.

This political pressure forces Harvest to prioritize private and state-owned acreage—where 68% of its 2024 production came from—to sustain output and preserve EBITDA margins.

Geopolitical Influence on Domestic Energy Security

Political instability in major exporters keeps U.S. domestic production a national security priority, with 2024 imports from OPEC+ nations still accounting for roughly 37% of US crude oil equivalents, reinforcing urgency for onshore output growth.

The federal government continues incentives for independents—2024 tax credits and permitting reforms aimed at midstream/upstream projects accelerated leasing, benefiting producers that bolster supply resilience.

Harvest can cite these policies and the 2023–2025 projected 4–6% annual domestic production growth in key basins to justify capital allocation toward proven assets and pipeline/processing infrastructure to shield against global shocks.

Taxation and Subsidy Frameworks

Legislative debates over removing intangible drilling cost deductions and other tax credits could reduce Harvest Oil & Gas free cash flow by an estimated 10–18% on development spending; in 2024 similar policy shifts cut sector cash flow by roughly $4–7 billion nationally. Conversely, US political support for domestic energy has produced incentives—IRA-era and 2024 DOE grants—targeting enhanced oil recovery and methane reduction, potentially offsetting up to 5–12% of capital costs. Navigating these fiscal changes is critical for multi‑year capital allocation and protecting projected 2025–2027 shareholder returns.

Trade Policies and Export Markets

Political decisions on LNG and crude exports shape Harvest Oil & Gas revenue; U.S. crude export capacity rose to ~8.5 mb/d in 2024, influencing inland differentials and realized prices.

Tariffs or import restrictions from major partners can create regional oversupply—midcontinent WTI discounts widened to ~$6–9/bbl vs Brent in 2024—squeezing margins for inland producers like Harvest.

Tracking trade agreements (USMCA updates, EU/U.K. policies, and free‑trade talks) is vital as shifts can reallocate ~10–20% of North American export flows seasonally.

- Export capacity ~8.5 mb/d (2024) impacts domestic price realization

- Midcontinent WTI discount ~$6–9/bbl vs Brent (2024)

- Tariffs/restrictions risk localized oversupply and margin compression

- Monitor USMCA, EU, U.K. trade moves affecting 10–20% of export flows

State-Level Political Dynamics

Operating across 10 US states, Harvest faces divergent state agendas on hydraulic fracturing and land rights; for example, California and New York have tightened restrictions while Texas and Oklahoma remain pro-industry, affecting ~40% of Harvest’s US acreage exposure.

States pushing aggressive climate goals (e.g., California’s 2035 clean-fuel targets) can increase compliance costs—industry estimates suggest state-level mandates can raise operating costs 5–12%—while pro-industry states offer faster permitting and lower regulatory drag.

Maintaining strong relationships with state regulators is vital: timely permits reduce project delays that can cost $0.5–2M per well in holding costs; Harvest’s regulatory engagement strategy should prioritize top-acreage states to secure longevity and minimize bureaucracy.

- 10 states exposure; ~40% acreage in restrictive states

- State mandates may increase costs 5–12%

- Permit delays can cost $0.5–2M per well

- Prioritize regulator relationships in highest-acreage states

Federal permitting slump cuts supply; Harvest leans on private/state assets, margins hit

Federal permitting fell 22% YTD through Q3 2024; onshore lease sales dropped 34% YoY (2024), pushing Harvest to rely on private/state assets (68% of 2024 production). Federal acreage additions may decline 25–40% by end-2025; US crude export capacity ~8.5 mb/d (2024) and midcontinent WTI discount ~$6–9/bbl (2024) affect realized prices.

| Metric | 2024 |

|---|---|

| Federal permitting change | -22% YTD Q3 |

| Lease sales | -34% YoY |

| Private/state share | 68% production |

| Export capacity | 8.5 mb/d |

| WTI discount | $6–9/bbl |

What is included in the product

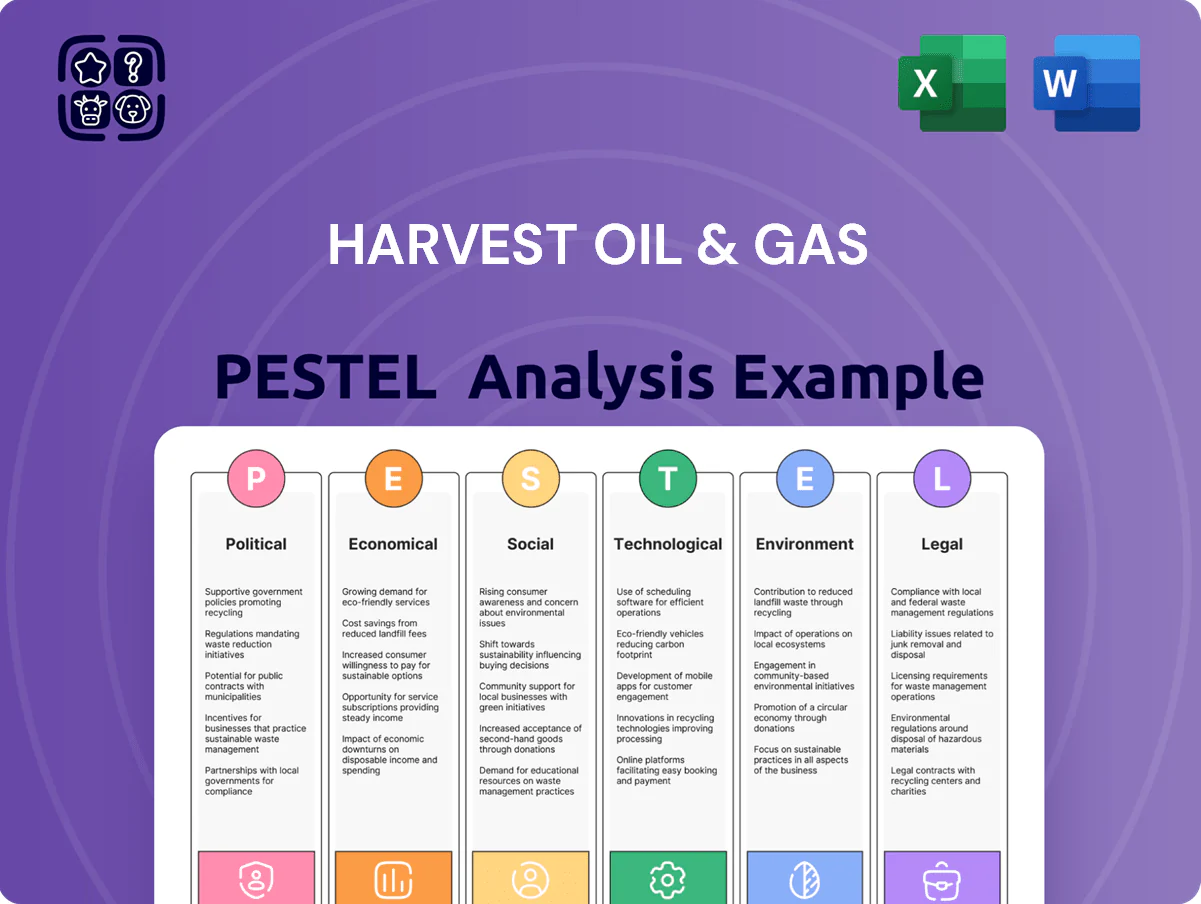

Explores how external macro-environmental factors uniquely affect Harvest Oil & Gas across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats, opportunities, and forward-looking scenarios for executives, investors, and strategists.

A concise, PESTLE-segmented summary of Harvest Oil & Gas that simplifies external risk assessment for meetings, easily dropped into presentations or shared across teams to support strategic planning and client reports.

Economic factors

Commodity Price Volatility

Harvests revenue hinges on Brent and Henry Hub prices; Brent averaged about 86 USD/bbl in 2024 and Henry Hub near 3.50 USD/MMBtu, but late‑2025 demand cooling in China, EU and US could shave global oil demand growth from ~2.0 mb/d (2024) to near zero, while OPEC+ cuts of ~1.5 mb/d in 2024‑25 have supported a price floor; Harvest must use disciplined hedging (swaps, collars) to stabilize EBITDA margins against these swings.

Interest Rate Environment and Capital Costs

After elevated Fed funds peaks at 5.25–5.50% in 2023–24, servicing debt remains costly for independents; US oilfield E&P borrowing costs averaged ~8–9% in 2024, increasing interest expense for Harvest and peers. High rates raise the internal hurdle for new development drilling, pushing breakeven WTI thresholds higher and curbing ROI on projects requiring >10% returns. Large-scale acquisitions face tighter feasibility as acquisition financing terms compressed; disciplined net debt/EBITDA targets (e.g., <2.5x) are essential for Harvest to access capital markets at favorable spreads.

Inflationary Pressures on Operational Expenses

Although headline inflation eased to about 3.2% in 2025, oilfield services, labor and specialist equipment costs remain elevated, with rig dayrates up ~18% YoY and skilled labor premiums rising ~12% in 2024–25.

Higher steel (+25% from 2021 peaks), chemical and on-site fuel costs compress margins on enhanced production projects, reducing IRR on well workovers by an estimated 200–400 basis points.

Harvest Oil & Gas must pursue strategic procurement, hedging and multi-year service contracts to lock prices and protect free cash flow against persistent input-cost inflation.

Labor Market Tightness in the Energy Sector

Labor market tightness in the energy sector has increased as renewables poach talent; US Bureau of Labor Statistics data to 2025 show petroleum engineering employment stagnant while wind/solar technician roles grew ~18% 2020–2024, pressuring wages for skilled engineers and technicians.

Economic growth in tech and construction drove regional wage inflation of 4–6% annually in 2023–2024, contributing to shortages for targeted development drilling projects.

Harvest must invest in retention (training, bonuses) and automation; automation can cut labor hours by 10–25% on drilling sites per industry case studies, helping control long-term personnel costs.

- Renewables growth ~18% (2020–2024) increased competition for talent

- Regional wage inflation 4–6% (2023–2024) strains hiring

- Automation reduces drilling labor hours ~10–25%

Regional Economic Health and Infrastructure

The economic viability of Harvest Oil & Gas assets depends on local infrastructure such as pipeline capacity and processing plants; US EIA data show US Gulf Coast takeaway constraints lifted in 2024 but Midwest bottlenecks kept differential prices up to $6/bbl in 2024, affecting realized rates.

Regional downturns can cut midstream investment—North American midstream capex fell ~8% YoY in 2024—raising transport costs and causing production curtailments.

Tracking regional GDP growth, rig counts (US rig count averaged 740 in 2024), and transport spreads helps Harvest prioritize assets with shortest, lowest-cost routes to market.

- Pipeline capacity and processing access determine asset cashflow sensitivity

- Midstream capex down ~8% YoY in 2024 increased transport spreads

- Price differentials reached ~$6/bbl in some US regions in 2024

- Rig count trends (avg 740 in 2024) guide regional demand assessment

Harvest faces volatile oil prices; disciplined hedging vital to protect EBITDA

Harvest faces price risk as Brent averaged ~86 USD/bbl in 2024 and Henry Hub ~3.50 USD/MMBtu; demand slowdown to ~0 mb/d growth in 2025 and OPEC+ cuts ~1.5 mb/d support a volatile floor, requiring disciplined hedging to protect EBITDA.

| Metric | 2024/25 |

|---|---|

| Brent | ~86 USD/bbl (2024) |

| Henry Hub | ~3.50 USD/MMBtu (2024) |

| US rig count | ~740 avg (2024) |

| Midstream capex | -8% YoY (2024) |

Preview Before You Purchase

Harvest Oil & Gas PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use, with the Harvest Oil & Gas PESTLE Analysis presented in its final, professional layout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Understand how political shifts, market cycles, and environmental rules are shaping Harvest Oil & Gas’s strategic outlook—our concise PESTLE snapshot highlights the most critical external forces affecting operations and value. Ready-made for investors and strategists, the full report delivers deeper legal, technological, and social analysis with actionable recommendations. Purchase the complete PESTLE to access editable insights you can apply immediately.

Political factors

Federal Leasing and Permitting Policies

The regulatory environment for Harvest Oil & Gas is shaped by federal land-use and drilling-permit policy; as of 2024 federal onshore lease sales dropped 34% year-over-year and BLM permitting slowed 22% through Q3 2024.

By end-2025 projected administrative shifts could impose stricter oversight or further slow new federal-lease approvals, potentially reducing federal acreage additions by an estimated 25–40% versus 2023 levels.

This political pressure forces Harvest to prioritize private and state-owned acreage—where 68% of its 2024 production came from—to sustain output and preserve EBITDA margins.

Geopolitical Influence on Domestic Energy Security

Political instability in major exporters keeps U.S. domestic production a national security priority, with 2024 imports from OPEC+ nations still accounting for roughly 37% of US crude oil equivalents, reinforcing urgency for onshore output growth.

The federal government continues incentives for independents—2024 tax credits and permitting reforms aimed at midstream/upstream projects accelerated leasing, benefiting producers that bolster supply resilience.

Harvest can cite these policies and the 2023–2025 projected 4–6% annual domestic production growth in key basins to justify capital allocation toward proven assets and pipeline/processing infrastructure to shield against global shocks.

Taxation and Subsidy Frameworks

Legislative debates over removing intangible drilling cost deductions and other tax credits could reduce Harvest Oil & Gas free cash flow by an estimated 10–18% on development spending; in 2024 similar policy shifts cut sector cash flow by roughly $4–7 billion nationally. Conversely, US political support for domestic energy has produced incentives—IRA-era and 2024 DOE grants—targeting enhanced oil recovery and methane reduction, potentially offsetting up to 5–12% of capital costs. Navigating these fiscal changes is critical for multi‑year capital allocation and protecting projected 2025–2027 shareholder returns.

Trade Policies and Export Markets

Political decisions on LNG and crude exports shape Harvest Oil & Gas revenue; U.S. crude export capacity rose to ~8.5 mb/d in 2024, influencing inland differentials and realized prices.

Tariffs or import restrictions from major partners can create regional oversupply—midcontinent WTI discounts widened to ~$6–9/bbl vs Brent in 2024—squeezing margins for inland producers like Harvest.

Tracking trade agreements (USMCA updates, EU/U.K. policies, and free‑trade talks) is vital as shifts can reallocate ~10–20% of North American export flows seasonally.

- Export capacity ~8.5 mb/d (2024) impacts domestic price realization

- Midcontinent WTI discount ~$6–9/bbl vs Brent (2024)

- Tariffs/restrictions risk localized oversupply and margin compression

- Monitor USMCA, EU, U.K. trade moves affecting 10–20% of export flows

State-Level Political Dynamics

Operating across 10 US states, Harvest faces divergent state agendas on hydraulic fracturing and land rights; for example, California and New York have tightened restrictions while Texas and Oklahoma remain pro-industry, affecting ~40% of Harvest’s US acreage exposure.

States pushing aggressive climate goals (e.g., California’s 2035 clean-fuel targets) can increase compliance costs—industry estimates suggest state-level mandates can raise operating costs 5–12%—while pro-industry states offer faster permitting and lower regulatory drag.

Maintaining strong relationships with state regulators is vital: timely permits reduce project delays that can cost $0.5–2M per well in holding costs; Harvest’s regulatory engagement strategy should prioritize top-acreage states to secure longevity and minimize bureaucracy.

- 10 states exposure; ~40% acreage in restrictive states

- State mandates may increase costs 5–12%

- Permit delays can cost $0.5–2M per well

- Prioritize regulator relationships in highest-acreage states

Federal permitting slump cuts supply; Harvest leans on private/state assets, margins hit

Federal permitting fell 22% YTD through Q3 2024; onshore lease sales dropped 34% YoY (2024), pushing Harvest to rely on private/state assets (68% of 2024 production). Federal acreage additions may decline 25–40% by end-2025; US crude export capacity ~8.5 mb/d (2024) and midcontinent WTI discount ~$6–9/bbl (2024) affect realized prices.

| Metric | 2024 |

|---|---|

| Federal permitting change | -22% YTD Q3 |

| Lease sales | -34% YoY |

| Private/state share | 68% production |

| Export capacity | 8.5 mb/d |

| WTI discount | $6–9/bbl |

What is included in the product

Explores how external macro-environmental factors uniquely affect Harvest Oil & Gas across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats, opportunities, and forward-looking scenarios for executives, investors, and strategists.

A concise, PESTLE-segmented summary of Harvest Oil & Gas that simplifies external risk assessment for meetings, easily dropped into presentations or shared across teams to support strategic planning and client reports.

Economic factors

Commodity Price Volatility

Harvests revenue hinges on Brent and Henry Hub prices; Brent averaged about 86 USD/bbl in 2024 and Henry Hub near 3.50 USD/MMBtu, but late‑2025 demand cooling in China, EU and US could shave global oil demand growth from ~2.0 mb/d (2024) to near zero, while OPEC+ cuts of ~1.5 mb/d in 2024‑25 have supported a price floor; Harvest must use disciplined hedging (swaps, collars) to stabilize EBITDA margins against these swings.

Interest Rate Environment and Capital Costs

After elevated Fed funds peaks at 5.25–5.50% in 2023–24, servicing debt remains costly for independents; US oilfield E&P borrowing costs averaged ~8–9% in 2024, increasing interest expense for Harvest and peers. High rates raise the internal hurdle for new development drilling, pushing breakeven WTI thresholds higher and curbing ROI on projects requiring >10% returns. Large-scale acquisitions face tighter feasibility as acquisition financing terms compressed; disciplined net debt/EBITDA targets (e.g., <2.5x) are essential for Harvest to access capital markets at favorable spreads.

Inflationary Pressures on Operational Expenses

Although headline inflation eased to about 3.2% in 2025, oilfield services, labor and specialist equipment costs remain elevated, with rig dayrates up ~18% YoY and skilled labor premiums rising ~12% in 2024–25.

Higher steel (+25% from 2021 peaks), chemical and on-site fuel costs compress margins on enhanced production projects, reducing IRR on well workovers by an estimated 200–400 basis points.

Harvest Oil & Gas must pursue strategic procurement, hedging and multi-year service contracts to lock prices and protect free cash flow against persistent input-cost inflation.

Labor Market Tightness in the Energy Sector

Labor market tightness in the energy sector has increased as renewables poach talent; US Bureau of Labor Statistics data to 2025 show petroleum engineering employment stagnant while wind/solar technician roles grew ~18% 2020–2024, pressuring wages for skilled engineers and technicians.

Economic growth in tech and construction drove regional wage inflation of 4–6% annually in 2023–2024, contributing to shortages for targeted development drilling projects.

Harvest must invest in retention (training, bonuses) and automation; automation can cut labor hours by 10–25% on drilling sites per industry case studies, helping control long-term personnel costs.

- Renewables growth ~18% (2020–2024) increased competition for talent

- Regional wage inflation 4–6% (2023–2024) strains hiring

- Automation reduces drilling labor hours ~10–25%

Regional Economic Health and Infrastructure

The economic viability of Harvest Oil & Gas assets depends on local infrastructure such as pipeline capacity and processing plants; US EIA data show US Gulf Coast takeaway constraints lifted in 2024 but Midwest bottlenecks kept differential prices up to $6/bbl in 2024, affecting realized rates.

Regional downturns can cut midstream investment—North American midstream capex fell ~8% YoY in 2024—raising transport costs and causing production curtailments.

Tracking regional GDP growth, rig counts (US rig count averaged 740 in 2024), and transport spreads helps Harvest prioritize assets with shortest, lowest-cost routes to market.

- Pipeline capacity and processing access determine asset cashflow sensitivity

- Midstream capex down ~8% YoY in 2024 increased transport spreads

- Price differentials reached ~$6/bbl in some US regions in 2024

- Rig count trends (avg 740 in 2024) guide regional demand assessment

Harvest faces volatile oil prices; disciplined hedging vital to protect EBITDA

Harvest faces price risk as Brent averaged ~86 USD/bbl in 2024 and Henry Hub ~3.50 USD/MMBtu; demand slowdown to ~0 mb/d growth in 2025 and OPEC+ cuts ~1.5 mb/d support a volatile floor, requiring disciplined hedging to protect EBITDA.

| Metric | 2024/25 |

|---|---|

| Brent | ~86 USD/bbl (2024) |

| Henry Hub | ~3.50 USD/MMBtu (2024) |

| US rig count | ~740 avg (2024) |

| Midstream capex | -8% YoY (2024) |

Preview Before You Purchase

Harvest Oil & Gas PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use, with the Harvest Oil & Gas PESTLE Analysis presented in its final, professional layout.