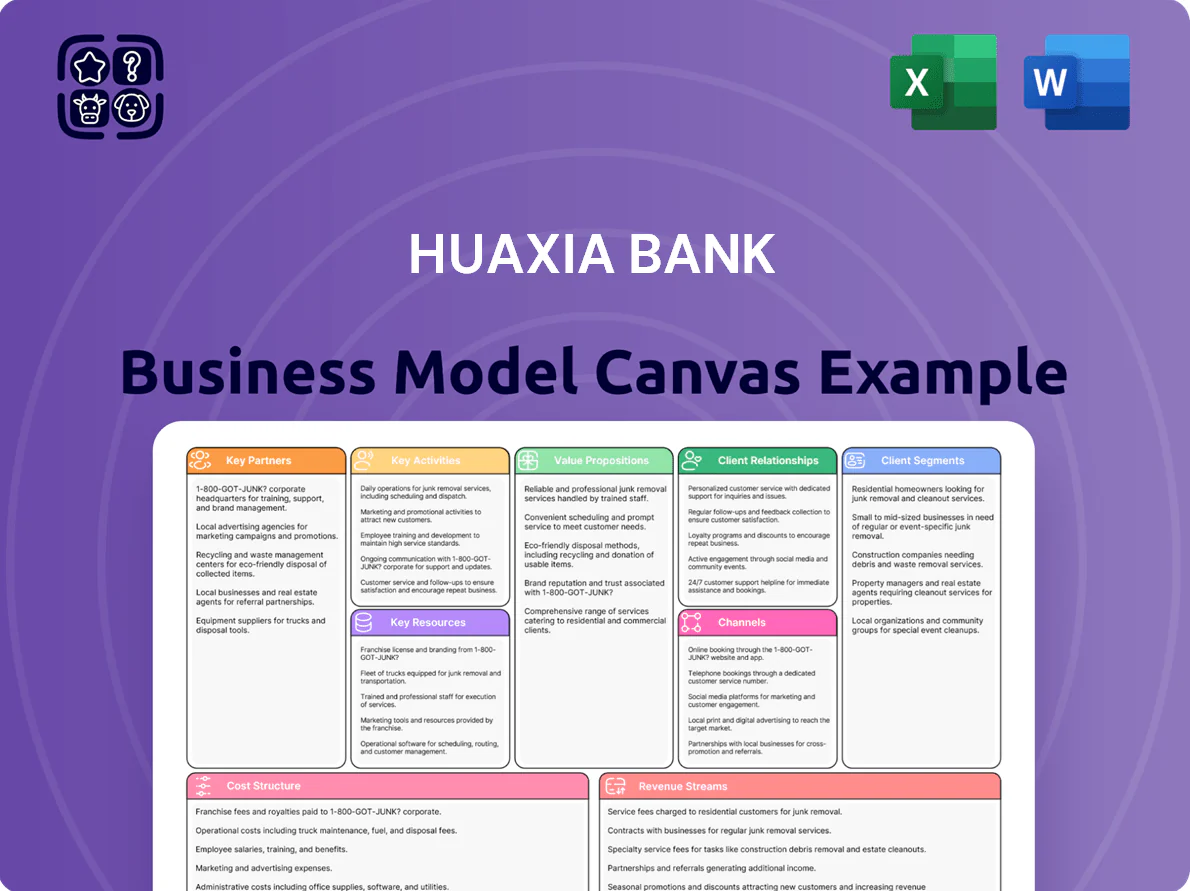

Huaxia Bank Business Model Canvas

Huaxia Bank Business Model Canvas: Key Value Drivers & Growth Blueprint

Unlock Huaxia Bank’s growth playbook with our concise Business Model Canvas—discover its core value propositions, customer segments, and revenue mechanics in a professionally structured format. Ideal for investors, consultants, and strategists, this download reveals operational levers, key partnerships, and profit drivers to inform benchmarking and decision-making. Purchase the full Word/Excel canvas for a complete, ready-to-use strategic blueprint.

Partnerships

State-Owned Enterprise Shareholders

Strategic alignment with state-owned shareholders such as Shougang Group gives Huaxia Bank a stable capital base and industrial links, supporting RMB 120+ billion in SOE-related corporate loans as of 2025; these partners open access to large infrastructure projects and supply-chain financing across China. By leveraging SOE relationships the bank secures steady flows of high-quality corporate clients and institutional deposits—SOE deposit balances represented about 18% of Huaxia’s total deposits in 2024.

FinTech and Technology Providers

Collaborations with Chinese tech giants (e.g., Alibaba Cloud, Tencent Cloud) let Huaxia Bank embed AI, cloud, and big-data analytics across operations—cutting loan processing time by ~40% and reducing default prediction error by ~10% in 2024.

Local Government Entities

Joint initiatives with municipal and provincial governments let Huaxia Bank take part in regional development and PPP projects, aligning lending with China’s 14th Five-Year Plan priorities; in 2024 Huaxia reported CNY 120bn in corporate loans tied to local government projects. These alliances often make the bank a preferred provider for government financial services and payroll, handling payrolls for over 2,300 public institutions as of Dec 2024.

International Banking Correspondents

- 200+ correspondent banks

- 60+ countries served

- CNY 120 billion international transactions in 2024

- ~30% faster settlements for BRI clients

Third-Party Payment Platforms

Integration with Alipay and WeChat Pay keeps Huaxia Bank inside daily Chinese payments, supporting ~1.3 billion monthly digital-wallet users and enabling instant transfers and QR payments directly from bank accounts.

This connectivity reduces churn—customers using mobile wallets have 25–30% higher transaction frequency—and preserves retail deposits by ensuring seamless interoperability between bank accounts and leading payment apps.

- Supports ~1.3B monthly wallet users

- Enables instant QR and peer transfers

- Boosts transaction frequency 25–30%

- Protects retail deposit stickiness

Huaxia's ecosystem powers CNY120B SOE loans, 1.3B wallets & 40% faster AI lending

Huaxia’s key partners—state-owned shareholders, tech platforms (Alibaba, Tencent), 200+ correspondent banks in 60+ countries, Alipay/WeChat Pay, and local governments—support CNY 120bn SOE-related loans (2025), CNY 120bn cross-border flows (2024), 1.3B monthly wallet users, ~18% SOE deposit share (2024), ~40% faster loan processing via cloud/AI.

| Partner | Metric |

|---|---|

| SOEs | CNY 120bn loans; 18% deposits |

| Correspondents | 200+ banks; CNY 120bn FX |

| Tech | ~40% faster processing |

| Wallets | 1.3B users |

What is included in the product

A concise Business Model Canvas for Huaxia Bank covering customer segments, channels, value propositions, revenue streams, key resources, partners, activities, cost structure, and customer relationships—aligned with real-world retail and corporate banking operations and strategic priorities to support investor presentations and internal planning.

High-level, editable Business Model Canvas for Huaxia Bank that condenses strategy into a digestible one-page snapshot—ideal for quick internal reviews, boardroom presentations, and collaborative adaptation.

Activities

Credit Risk Management and Assessment

Huaxia Bank uses data-driven credit scoring and machine-learning models to assess borrower creditworthiness, keeping gross non-performing loan (NPL) ratio near 1.15% at end-2024 and provisioning coverage around 240% to protect asset quality. The bank conducts continuous portfolio monitoring with an early-warning system flagging delinquency signals weekly, which helped reduce new NPL formation by 22% in 2024, supporting stable lending returns.

Digital Banking Product Development

Digital banking product development at Huaxia Bank focuses on continuous upgrades to mobile and online platforms, designing intuitive UIs and embedding automated financial-planning tools; in 2024 Huaxia reported 28% YoY growth in active mobile users to ~15.2 million, cutting branch transactions 21% and lowering service costs per customer by 12%.

Capital Mobilization and Deposit Management

Huaxia Bank actively attracts retail and corporate deposits to fund lending; by end-2025 it reported RMB 2.1 trillion in customer deposits, up 4.8% year-on-year, supporting liquidity and loan growth.

The bank offers tiered savings, time deposits, and wealth-management products to lock long-term funds and focuses on controlling deposit cost—deposit-to-loan spread and NIM targets keep funding cost pressures managed.

Wealth Management and Investment Services

The bank designs and manages diversified investment products across risk profiles, shifting toward net-asset-value (NAV) pricing to meet China’s asset management reform; by 2024 Huaxia Bank reported wealth management AUM of about CNY 1.2 trillion, with fee income up ~8% year-on-year.

- NAV shift: compliant with 2018–2023 AM reform

- AUM: ~CNY 1.2 trillion (2024)

- Fee income growth: +8% YoY (2024)

- Revenue mix: higher fee-based diversification

Regulatory Compliance and Internal Control

Huaxia Bank enforces continuous compliance with the People’s Bank of China and CSRC rules, investing over CNY 1.2 billion in 2024 in AML and reporting systems to meet evolving standards and reduce regulatory fines.

Strong corporate governance—board oversight, internal audit, and SOX-like controls—protects its banking license and reputation; noncompliance penalties in China averaged CNY 210 million for major banks in 2023, so controls are mission-critical.

- 2024 compliance spend: CNY 1.2 billion

- AML/system upgrades to reduce SARs and false positives

- Board/internal audit standardization across 100+ branches

- Benchmark fines (2023): CNY 210 million for major banks

Huaxia: Low NPLs, 240% coverage, 15.2M mobile users & RMB2.1T deposits

Huaxia runs data-driven credit scoring and weekly early-warning monitoring, keeping NPL ~1.15% (end-2024) and 240% provision coverage, while scaling digital banking (15.2M active mobile users, +28% YoY) to cut costs and boost fee income; deposits reached RMB 2.1T (end-2025) and wealth AUM ~CNY 1.2T (2024) with CNY 1.2B compliance spend in 2024.

| Metric | Value |

|---|---|

| Gross NPL | 1.15% (2024) |

| Provision coverage | 240% |

| Mobile users | 15.2M (+28% YoY) |

| Deposits | RMB 2.1T (end-2025) |

| Wealth AUM | CNY 1.2T (2024) |

| Compliance spend | CNY 1.2B (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The preview you see is the actual Huaxia Bank Business Model Canvas document, not a mockup or sample, and reflects the same structure, content, and formatting included in the final file.

After purchase you’ll receive this exact deliverable—fully editable and downloadable in Word and Excel—ready for presentation, analysis, or integration into your financial planning.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Huaxia Bank Business Model Canvas: Key Value Drivers & Growth Blueprint

Unlock Huaxia Bank’s growth playbook with our concise Business Model Canvas—discover its core value propositions, customer segments, and revenue mechanics in a professionally structured format. Ideal for investors, consultants, and strategists, this download reveals operational levers, key partnerships, and profit drivers to inform benchmarking and decision-making. Purchase the full Word/Excel canvas for a complete, ready-to-use strategic blueprint.

Partnerships

State-Owned Enterprise Shareholders

Strategic alignment with state-owned shareholders such as Shougang Group gives Huaxia Bank a stable capital base and industrial links, supporting RMB 120+ billion in SOE-related corporate loans as of 2025; these partners open access to large infrastructure projects and supply-chain financing across China. By leveraging SOE relationships the bank secures steady flows of high-quality corporate clients and institutional deposits—SOE deposit balances represented about 18% of Huaxia’s total deposits in 2024.

FinTech and Technology Providers

Collaborations with Chinese tech giants (e.g., Alibaba Cloud, Tencent Cloud) let Huaxia Bank embed AI, cloud, and big-data analytics across operations—cutting loan processing time by ~40% and reducing default prediction error by ~10% in 2024.

Local Government Entities

Joint initiatives with municipal and provincial governments let Huaxia Bank take part in regional development and PPP projects, aligning lending with China’s 14th Five-Year Plan priorities; in 2024 Huaxia reported CNY 120bn in corporate loans tied to local government projects. These alliances often make the bank a preferred provider for government financial services and payroll, handling payrolls for over 2,300 public institutions as of Dec 2024.

International Banking Correspondents

- 200+ correspondent banks

- 60+ countries served

- CNY 120 billion international transactions in 2024

- ~30% faster settlements for BRI clients

Third-Party Payment Platforms

Integration with Alipay and WeChat Pay keeps Huaxia Bank inside daily Chinese payments, supporting ~1.3 billion monthly digital-wallet users and enabling instant transfers and QR payments directly from bank accounts.

This connectivity reduces churn—customers using mobile wallets have 25–30% higher transaction frequency—and preserves retail deposits by ensuring seamless interoperability between bank accounts and leading payment apps.

- Supports ~1.3B monthly wallet users

- Enables instant QR and peer transfers

- Boosts transaction frequency 25–30%

- Protects retail deposit stickiness

Huaxia's ecosystem powers CNY120B SOE loans, 1.3B wallets & 40% faster AI lending

Huaxia’s key partners—state-owned shareholders, tech platforms (Alibaba, Tencent), 200+ correspondent banks in 60+ countries, Alipay/WeChat Pay, and local governments—support CNY 120bn SOE-related loans (2025), CNY 120bn cross-border flows (2024), 1.3B monthly wallet users, ~18% SOE deposit share (2024), ~40% faster loan processing via cloud/AI.

| Partner | Metric |

|---|---|

| SOEs | CNY 120bn loans; 18% deposits |

| Correspondents | 200+ banks; CNY 120bn FX |

| Tech | ~40% faster processing |

| Wallets | 1.3B users |

What is included in the product

A concise Business Model Canvas for Huaxia Bank covering customer segments, channels, value propositions, revenue streams, key resources, partners, activities, cost structure, and customer relationships—aligned with real-world retail and corporate banking operations and strategic priorities to support investor presentations and internal planning.

High-level, editable Business Model Canvas for Huaxia Bank that condenses strategy into a digestible one-page snapshot—ideal for quick internal reviews, boardroom presentations, and collaborative adaptation.

Activities

Credit Risk Management and Assessment

Huaxia Bank uses data-driven credit scoring and machine-learning models to assess borrower creditworthiness, keeping gross non-performing loan (NPL) ratio near 1.15% at end-2024 and provisioning coverage around 240% to protect asset quality. The bank conducts continuous portfolio monitoring with an early-warning system flagging delinquency signals weekly, which helped reduce new NPL formation by 22% in 2024, supporting stable lending returns.

Digital Banking Product Development

Digital banking product development at Huaxia Bank focuses on continuous upgrades to mobile and online platforms, designing intuitive UIs and embedding automated financial-planning tools; in 2024 Huaxia reported 28% YoY growth in active mobile users to ~15.2 million, cutting branch transactions 21% and lowering service costs per customer by 12%.

Capital Mobilization and Deposit Management

Huaxia Bank actively attracts retail and corporate deposits to fund lending; by end-2025 it reported RMB 2.1 trillion in customer deposits, up 4.8% year-on-year, supporting liquidity and loan growth.

The bank offers tiered savings, time deposits, and wealth-management products to lock long-term funds and focuses on controlling deposit cost—deposit-to-loan spread and NIM targets keep funding cost pressures managed.

Wealth Management and Investment Services

The bank designs and manages diversified investment products across risk profiles, shifting toward net-asset-value (NAV) pricing to meet China’s asset management reform; by 2024 Huaxia Bank reported wealth management AUM of about CNY 1.2 trillion, with fee income up ~8% year-on-year.

- NAV shift: compliant with 2018–2023 AM reform

- AUM: ~CNY 1.2 trillion (2024)

- Fee income growth: +8% YoY (2024)

- Revenue mix: higher fee-based diversification

Regulatory Compliance and Internal Control

Huaxia Bank enforces continuous compliance with the People’s Bank of China and CSRC rules, investing over CNY 1.2 billion in 2024 in AML and reporting systems to meet evolving standards and reduce regulatory fines.

Strong corporate governance—board oversight, internal audit, and SOX-like controls—protects its banking license and reputation; noncompliance penalties in China averaged CNY 210 million for major banks in 2023, so controls are mission-critical.

- 2024 compliance spend: CNY 1.2 billion

- AML/system upgrades to reduce SARs and false positives

- Board/internal audit standardization across 100+ branches

- Benchmark fines (2023): CNY 210 million for major banks

Huaxia: Low NPLs, 240% coverage, 15.2M mobile users & RMB2.1T deposits

Huaxia runs data-driven credit scoring and weekly early-warning monitoring, keeping NPL ~1.15% (end-2024) and 240% provision coverage, while scaling digital banking (15.2M active mobile users, +28% YoY) to cut costs and boost fee income; deposits reached RMB 2.1T (end-2025) and wealth AUM ~CNY 1.2T (2024) with CNY 1.2B compliance spend in 2024.

| Metric | Value |

|---|---|

| Gross NPL | 1.15% (2024) |

| Provision coverage | 240% |

| Mobile users | 15.2M (+28% YoY) |

| Deposits | RMB 2.1T (end-2025) |

| Wealth AUM | CNY 1.2T (2024) |

| Compliance spend | CNY 1.2B (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The preview you see is the actual Huaxia Bank Business Model Canvas document, not a mockup or sample, and reflects the same structure, content, and formatting included in the final file.

After purchase you’ll receive this exact deliverable—fully editable and downloadable in Word and Excel—ready for presentation, analysis, or integration into your financial planning.