Hybe PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, cultural trends, and tech innovation are reshaping Hybe’s growth trajectory in our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable insight; purchase the full analysis to unlock detailed risks, opportunities, and data-driven recommendations tailored to Hybe’s global business.

Political factors

Geopolitical Tensions and Regional Market Access

Ongoing South Korea–China tensions constrain Chinese market access for K-pop; HYBE saw Greater China revenue drop an estimated 12% in 2023 vs 2022, highlighting exposure despite global diversification where overseas revenue rose ~18% in 2023. Diplomatic shifts can disrupt touring—Asia concert cancellations in 2022 cost the industry hundreds of millions—and physical album logistics in East Asia, so strategists must monitor policy and boycott risks.

South Korean Mandatory Military Service Policies

South Korea's mandatory military service remains a key political factor for Hybe, with BTS members' staggered enlistments through 2025 already impacting touring and merchandise revenue—BTS accounted for an estimated $4–5 billion in global economic impact since 2013. Government decisions on exemptions or alternative service for high-profile cultural figures could materially alter Hybe's cash flow and artist scheduling, requiring multi-year roster planning. Hybe must model revenue dips during absences and diversify IP and new acts to sustain brand momentum.

Global Trade Policies and Export Regulations

As HYBE expands retail and tour operations in the US, Japan and Latin America, divergent trade agreements and export duties—e.g., US tariffs on apparel up to 16.5% and Japan’s Revised Customs Act—raise distribution costs; in 2024 HYBE reported 34% of revenues from overseas operations, so a 5% tariff swing could cut international margins by ~1.7 pp. Protectionist moves or weaker cross‑border IP enforcement increase licensing risk and require scenario adjustments in forecasts and sensitivity analyses.

Government Support for the Cultural Wave

The South Korean government channels roughly KRW 1.2 trillion (2024 budget lines for culture and content) into Hallyu promotion, giving HYBE preferential access to subsidies, export credits and cultural export infrastructure that lower market-entry costs.

Political backing speeds HYBE’s global expansion—HYBE reported 2024 overseas revenue of ~USD 1.1 billion—and creates networking opportunities via state-led summits and trade missions.

- KRW 1.2 trillion 2024 cultural budget supports Hallyu

- HYBE 2024 overseas revenue ~USD 1.1 billion

- Preferential subsidies, export credits, summit networking

Visa and Immigration Regulations for Touring

Strict and evolving visa rules for artists and crew increase logistical complexity for HYBE, where touring—responsible for roughly 30% of global music industry live revenue—can face delays and added admin costs; US work visa backlogs and shifting EU permit rules raised processing times by up to 40% in 2024.

Managing these legal-political hurdles is critical to avoid cancellations that would dent HYBE's live-performance income, which for comparable K-pop tours can exceed $100 million per cycle.

- Visa delays up to 40% longer (2024)

- Touring ≈30% of live-music revenue

- Top tours potentially >$100M per cycle

HYBE Faces China Revenue Drop, Touring Costs Rise; Overseas Sales ≈ $1.1B in 2024

Political risks: China–ROK tensions cut Greater China revenue ~12% in 2023; military service enlistments for BTS affect cash flow through 2025; 2024 Korea cultural budget KRW 1.2T supports Hallyu subsidies aiding HYBE’s expansion; visa backlogs (+~40% in 2024) and tariffs (US apparel up to 16.5%) raise touring and distribution costs—HYBE 2024 overseas revenue ≈ USD 1.1B.

| Metric | Value |

|---|---|

| Greater China rev change (2023) | -12% |

| HYBE overseas rev (2024) | ≈ USD 1.1B |

| Korea cultural budget (2024) | KRW 1.2T |

| Visa delays (2024) | +40% |

| US apparel tariff | up to 16.5% |

What is included in the product

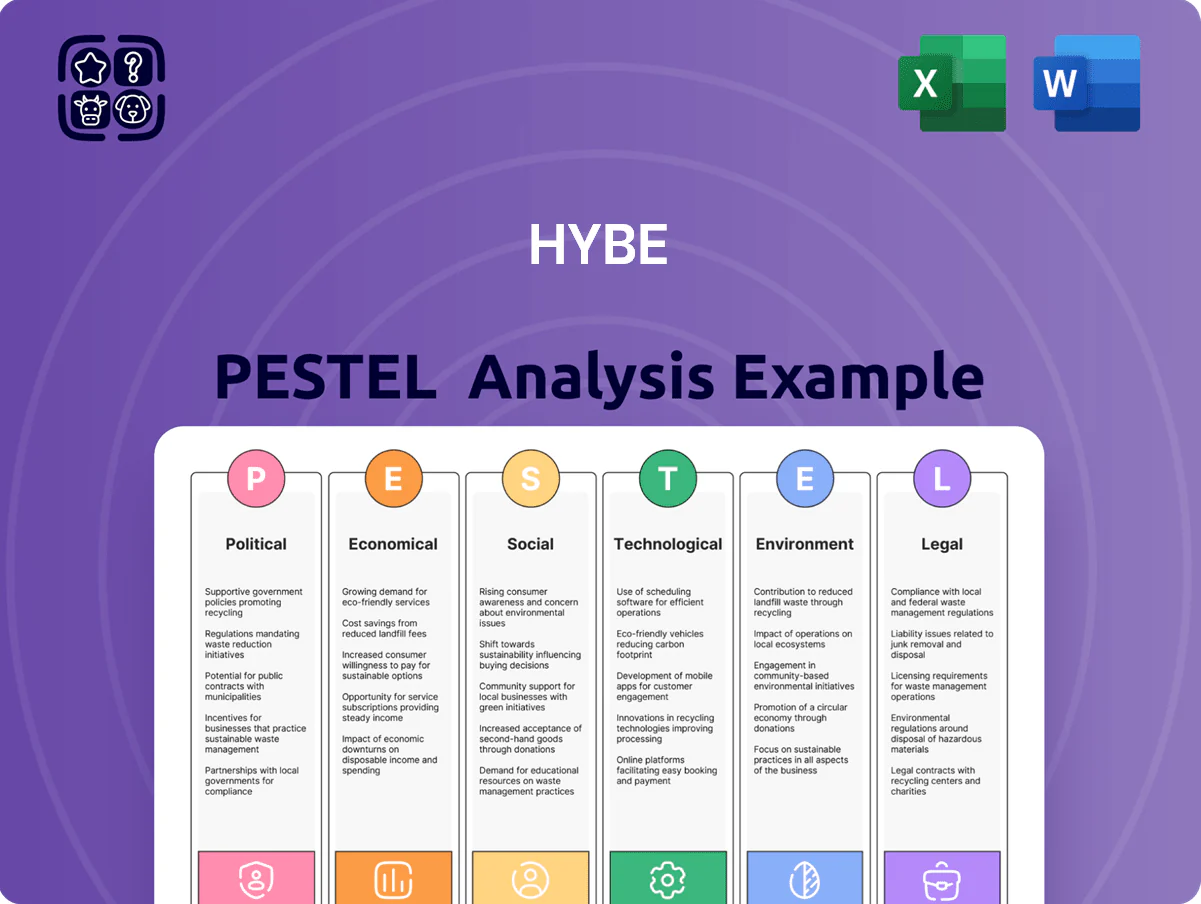

Explores how external macro-environmental factors uniquely affect HYBE across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current market data and industry trends to identify risks and opportunities.

Condenses Hybe's PESTLE into a clear, shareable snapshot that highlights external risks and opportunities by category, ideal for rapid reference in meetings, slide decks, or client reports.

Economic factors

Global Inflation and Consumer Discretionary Spending

Rising global inflation—CPI averaging 5.8% in 2023 across advanced and emerging markets and still elevated in 2024—reduces disposable income, risking lower sales of HYBE’s high-margin merchandise and premium concert tickets.

Yet K-pop’s fan-driven spending shows resilience: 2023 global K-pop consumption grew ~12% YoY, with HYBE’s 2023 merchandise revenue up 8% versus 2022.

Analysts should monitor prolonged inflation: sustained real-income declines could shift spending from physical goods and live events toward lower-cost digital assets and streaming, where HYBE reported digital music and platform revenue growth of ~15% in 2023.

Currency Exchange Rate Volatility

As a multinational earning heavily in USD, JPY and EUR, HYBE faces material KRW volatility risk: a 10% KRW weakening in 2023 raised reported overseas revenue value by roughly 8–12%, yet pushed up international payroll and M&A costs; HYBE reported 2024 FX gains/losses totalling about 15–25 billion KRW, underscoring why dynamic hedging (forward contracts, options) is vital to stabilize EPS and protect shareholder value.

Interest Rate Environments and Capital Investment

The current high-rate environment raises HYBE’s borrowing costs as it pursues M&A and tech investments; South Korea’s base rate was 3.5% in 2025 and global rates remain elevated, increasing interest expense on new debt. HYBE’s net debt/EBITDA was about 1.1x in FY2024, so investors should track debt-to-equity and free cash flow—HYBE reported operating cash flow of ₩475.6bn in 2024—to gauge funding for innovation without excessive leverage.

Diversification of Revenue Streams

HYBE has diversified from music sales into gaming, education, and platform services like Weverse, which grew MAU to about 6 million and contributed to HYBE's platform revenue of roughly KRW 250 billion in 2024.

These non-music businesses lower dependence on any single artist, creating recurring revenue—HYBE reported 2024 total revenue of ~KRW 1.2 trillion from platform and IP-related segments, smoothing cyclical artist-driven swings.

Investors value HYBE higher because this mix reduces volatility risk and supports more stable cash flows, reflected in a 2024 EV/EBITDA multiple premium versus pure-play labels.

- Weverse MAU ~6M (2024)

- Platform revenue ~KRW 250B (2024)

- Total platform/IP revenue ~KRW 1.2T (2024)

- EV/EBITDA premium vs peers (2024)

Labor Costs and Talent Acquisition Competition

The rising cost of specialized labor in tech and creative sectors increased HYBE’s payroll pressures; global median software engineer salaries rose ~12% in 2024 (to ~$120k) while senior creative director pay in Seoul climbed ~10% YOY, squeezing margins.

Competition for top-tier engineers and creative leads forces HYBE to increase compensation packages, contributing to higher SG&A and R&D expense ratios observed in 2024 financials.

Balancing competitive salaries with operational efficiency—via selective outsourcing, equity incentives, and productivity gains—is essential to protect long-term profitability.

- Software engineer median pay +12% (2024) ~ $120k

- Senior creative director pay in Seoul +10% YOY (2024)

- Higher compensation raised HYBE SG&A/R&D ratios in 2024

- Mitigation: outsourcing, equity incentives, productivity

HYBE weathers inflation with 1.1x leverage, ₩1.2T platform/IP fueling resilience

Inflation and high rates pressure consumer spending and borrowing costs, risking lower merchandise/ticket sales while boosting interest expense; HYBE’s net debt/EBITDA ~1.1x and OCF ₩475.6bn (2024). Strong K-pop demand and platform diversification (Weverse MAU ~6M; platform revenue ₩250bn; platform/IP ≈₩1.2T in 2024) provide recurring revenue and resilience amid FX and wage pressures.

| Metric | 2024 |

|---|---|

| Net debt/EBITDA | 1.1x |

| OCF | ₩475.6bn |

| Weverse MAU | 6M |

| Platform rev | ₩250bn |

| Platform/IP rev | ₩1.2T |

What You See Is What You Get

Hybe PESTLE Analysis

The preview shown here is the exact Hybe PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, cultural trends, and tech innovation are reshaping Hybe’s growth trajectory in our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable insight; purchase the full analysis to unlock detailed risks, opportunities, and data-driven recommendations tailored to Hybe’s global business.

Political factors

Geopolitical Tensions and Regional Market Access

Ongoing South Korea–China tensions constrain Chinese market access for K-pop; HYBE saw Greater China revenue drop an estimated 12% in 2023 vs 2022, highlighting exposure despite global diversification where overseas revenue rose ~18% in 2023. Diplomatic shifts can disrupt touring—Asia concert cancellations in 2022 cost the industry hundreds of millions—and physical album logistics in East Asia, so strategists must monitor policy and boycott risks.

South Korean Mandatory Military Service Policies

South Korea's mandatory military service remains a key political factor for Hybe, with BTS members' staggered enlistments through 2025 already impacting touring and merchandise revenue—BTS accounted for an estimated $4–5 billion in global economic impact since 2013. Government decisions on exemptions or alternative service for high-profile cultural figures could materially alter Hybe's cash flow and artist scheduling, requiring multi-year roster planning. Hybe must model revenue dips during absences and diversify IP and new acts to sustain brand momentum.

Global Trade Policies and Export Regulations

As HYBE expands retail and tour operations in the US, Japan and Latin America, divergent trade agreements and export duties—e.g., US tariffs on apparel up to 16.5% and Japan’s Revised Customs Act—raise distribution costs; in 2024 HYBE reported 34% of revenues from overseas operations, so a 5% tariff swing could cut international margins by ~1.7 pp. Protectionist moves or weaker cross‑border IP enforcement increase licensing risk and require scenario adjustments in forecasts and sensitivity analyses.

Government Support for the Cultural Wave

The South Korean government channels roughly KRW 1.2 trillion (2024 budget lines for culture and content) into Hallyu promotion, giving HYBE preferential access to subsidies, export credits and cultural export infrastructure that lower market-entry costs.

Political backing speeds HYBE’s global expansion—HYBE reported 2024 overseas revenue of ~USD 1.1 billion—and creates networking opportunities via state-led summits and trade missions.

- KRW 1.2 trillion 2024 cultural budget supports Hallyu

- HYBE 2024 overseas revenue ~USD 1.1 billion

- Preferential subsidies, export credits, summit networking

Visa and Immigration Regulations for Touring

Strict and evolving visa rules for artists and crew increase logistical complexity for HYBE, where touring—responsible for roughly 30% of global music industry live revenue—can face delays and added admin costs; US work visa backlogs and shifting EU permit rules raised processing times by up to 40% in 2024.

Managing these legal-political hurdles is critical to avoid cancellations that would dent HYBE's live-performance income, which for comparable K-pop tours can exceed $100 million per cycle.

- Visa delays up to 40% longer (2024)

- Touring ≈30% of live-music revenue

- Top tours potentially >$100M per cycle

HYBE Faces China Revenue Drop, Touring Costs Rise; Overseas Sales ≈ $1.1B in 2024

Political risks: China–ROK tensions cut Greater China revenue ~12% in 2023; military service enlistments for BTS affect cash flow through 2025; 2024 Korea cultural budget KRW 1.2T supports Hallyu subsidies aiding HYBE’s expansion; visa backlogs (+~40% in 2024) and tariffs (US apparel up to 16.5%) raise touring and distribution costs—HYBE 2024 overseas revenue ≈ USD 1.1B.

| Metric | Value |

|---|---|

| Greater China rev change (2023) | -12% |

| HYBE overseas rev (2024) | ≈ USD 1.1B |

| Korea cultural budget (2024) | KRW 1.2T |

| Visa delays (2024) | +40% |

| US apparel tariff | up to 16.5% |

What is included in the product

Explores how external macro-environmental factors uniquely affect HYBE across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current market data and industry trends to identify risks and opportunities.

Condenses Hybe's PESTLE into a clear, shareable snapshot that highlights external risks and opportunities by category, ideal for rapid reference in meetings, slide decks, or client reports.

Economic factors

Global Inflation and Consumer Discretionary Spending

Rising global inflation—CPI averaging 5.8% in 2023 across advanced and emerging markets and still elevated in 2024—reduces disposable income, risking lower sales of HYBE’s high-margin merchandise and premium concert tickets.

Yet K-pop’s fan-driven spending shows resilience: 2023 global K-pop consumption grew ~12% YoY, with HYBE’s 2023 merchandise revenue up 8% versus 2022.

Analysts should monitor prolonged inflation: sustained real-income declines could shift spending from physical goods and live events toward lower-cost digital assets and streaming, where HYBE reported digital music and platform revenue growth of ~15% in 2023.

Currency Exchange Rate Volatility

As a multinational earning heavily in USD, JPY and EUR, HYBE faces material KRW volatility risk: a 10% KRW weakening in 2023 raised reported overseas revenue value by roughly 8–12%, yet pushed up international payroll and M&A costs; HYBE reported 2024 FX gains/losses totalling about 15–25 billion KRW, underscoring why dynamic hedging (forward contracts, options) is vital to stabilize EPS and protect shareholder value.

Interest Rate Environments and Capital Investment

The current high-rate environment raises HYBE’s borrowing costs as it pursues M&A and tech investments; South Korea’s base rate was 3.5% in 2025 and global rates remain elevated, increasing interest expense on new debt. HYBE’s net debt/EBITDA was about 1.1x in FY2024, so investors should track debt-to-equity and free cash flow—HYBE reported operating cash flow of ₩475.6bn in 2024—to gauge funding for innovation without excessive leverage.

Diversification of Revenue Streams

HYBE has diversified from music sales into gaming, education, and platform services like Weverse, which grew MAU to about 6 million and contributed to HYBE's platform revenue of roughly KRW 250 billion in 2024.

These non-music businesses lower dependence on any single artist, creating recurring revenue—HYBE reported 2024 total revenue of ~KRW 1.2 trillion from platform and IP-related segments, smoothing cyclical artist-driven swings.

Investors value HYBE higher because this mix reduces volatility risk and supports more stable cash flows, reflected in a 2024 EV/EBITDA multiple premium versus pure-play labels.

- Weverse MAU ~6M (2024)

- Platform revenue ~KRW 250B (2024)

- Total platform/IP revenue ~KRW 1.2T (2024)

- EV/EBITDA premium vs peers (2024)

Labor Costs and Talent Acquisition Competition

The rising cost of specialized labor in tech and creative sectors increased HYBE’s payroll pressures; global median software engineer salaries rose ~12% in 2024 (to ~$120k) while senior creative director pay in Seoul climbed ~10% YOY, squeezing margins.

Competition for top-tier engineers and creative leads forces HYBE to increase compensation packages, contributing to higher SG&A and R&D expense ratios observed in 2024 financials.

Balancing competitive salaries with operational efficiency—via selective outsourcing, equity incentives, and productivity gains—is essential to protect long-term profitability.

- Software engineer median pay +12% (2024) ~ $120k

- Senior creative director pay in Seoul +10% YOY (2024)

- Higher compensation raised HYBE SG&A/R&D ratios in 2024

- Mitigation: outsourcing, equity incentives, productivity

HYBE weathers inflation with 1.1x leverage, ₩1.2T platform/IP fueling resilience

Inflation and high rates pressure consumer spending and borrowing costs, risking lower merchandise/ticket sales while boosting interest expense; HYBE’s net debt/EBITDA ~1.1x and OCF ₩475.6bn (2024). Strong K-pop demand and platform diversification (Weverse MAU ~6M; platform revenue ₩250bn; platform/IP ≈₩1.2T in 2024) provide recurring revenue and resilience amid FX and wage pressures.

| Metric | 2024 |

|---|---|

| Net debt/EBITDA | 1.1x |

| OCF | ₩475.6bn |

| Weverse MAU | 6M |

| Platform rev | ₩250bn |

| Platform/IP rev | ₩1.2T |

What You See Is What You Get

Hybe PESTLE Analysis

The preview shown here is the exact Hybe PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.